C9 Resin Market Report Scope & Overview:

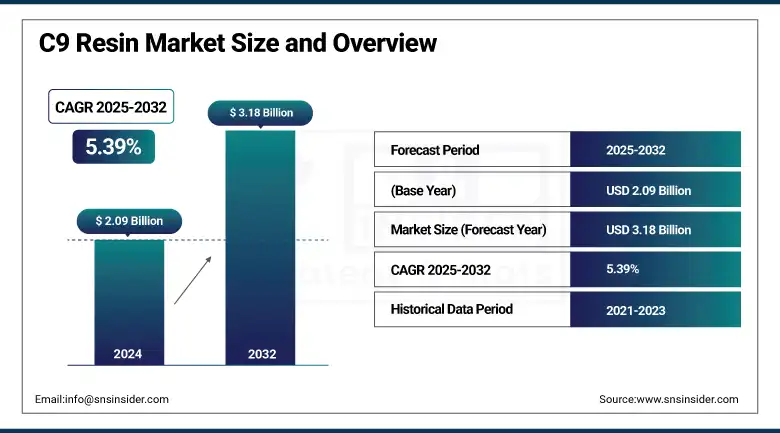

The C9 Resin Market size was valued at USD 2.09 billion in 2024 and is expected to reach USD 3.18 billion by 2032, growing at a CAGR of 5.39% over the forecast period of 2025-2032.

The C9 resin market is witnessing significant momentum, primarily driven by its adaptability across a broad range of industrial applications. As a resin made from petroleum, C9 resin serves as an important tackifier and performance enhancer, widely known for enhancing gloss, adhesion, thermal and color stability, and UV stability. As a result, it is the material of choice for adhesives, coatings, printing inks, and rubber compounding. The utilization of in hot melt adhesives in packaging & construction, and in low VOC, high solid automotive & industrial coatings is also aiding towards C9 Resin market growth.

C9 Resin Market Size and Forecast

-

Market Size in 2024: USD 2.09 Billion

-

Market Size by 2032: USD 3.18 Billion

-

CAGR: 5.39% from 2025 to 2032

-

Base Year: 2024

-

Forecast Period: 2025–2032

-

Historical Data: 2022–2024

To Get more information On C9 Resin Market - Request Free Sample Report

C9 Resin Market Trends

-

Rising demand from adhesives and sealants is driving C9 resin consumption, with the adhesives segment accounting for over 35% of total market share globally.

-

Growth in the paints and coatings industry, particularly in Asia-Pacific, is supporting market expansion, contributing to a projected CAGR of 5–6% for C9 resins over the forecast period.

-

Increasing use in rubber compounding and tire manufacturing is boosting demand, with rubber applications representing around 25% of total consumption.

-

Expansion of road marking and construction activities is accelerating adoption, as infrastructure spending in emerging economies grows at over 6% annually.

-

Technological advancements in hydrogenated and low-VOC C9 resins are gaining traction, with specialty grades witnessing demand growth of 7–8% CAGR due to environmental regulations.

The market is being reshaped by key C9 Resin Market Trends, including a rising focus on sustainability and technological innovation. Producers are focusing more on bio-based alternatives or customization of C9 resins for target segments, including electronics, medical, and aerospace. Advances in polymerization methods, such as cold and hydrogenated processing, improved color clarity, compatibility, and solubility and expanded their ranges of application. Although the competition from natural resins, including rosin, is increasing but the degradation of modified and high-performance C9 resins helps in keeping the market competitive. In general, the industry appears to be changing in accordance with shifting industrial and environmental needs, which is one more factor strengthening its value as a strategic asset.

In May 2025, Neville Chemical expanded its U.S. partnership with IMCD to strengthen the distribution of its NEVTAC tackifying resins used in adhesives and coatings. These resins offer excellent tack, low odor, and thermal/UV stability. The move aims to enhance supply chain access and technical support across the U.S. market.

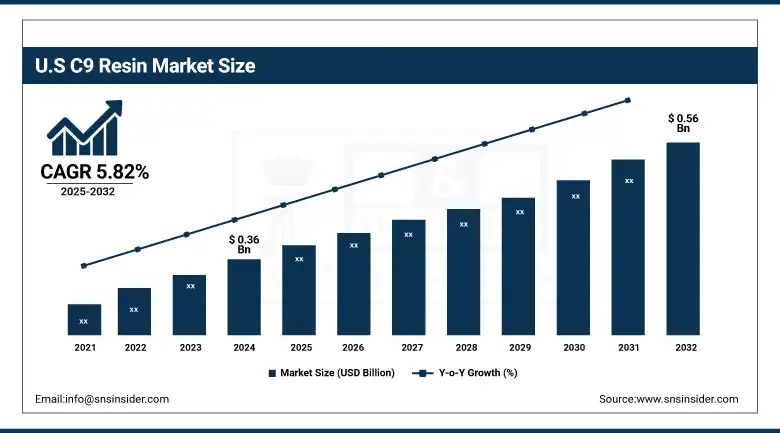

The U.S. dominates the North American C9 resin market, valued at USD 0.36 billion in 2024 and projected to reach USD 0.56 billion by 2032, growing at a CAGR of 5.82%. This growth is fueled by strong demand in adhesives, coatings, and inks. Industrial advancements and sustainability-focused formulations are enhancing market traction. The U.S. remains the key contributor to regional market expansion.

C9 Resin Market Drivers

-

C9 Resin Market Surges Globally on Rising Demand from Adhesives, Construction, And Flexible Packaging Sectors

The Global C9 Resin Market is witnessing strong demand, particularly in the adhesives and sealants segment, driven by its excellent tackiness, bonding strength, and flexibility. Half of the C9 resin goes into some of the hot-melt and pressure-sensitive adhesives used in packaging, construction, woodworking, and automotive industries. The booming construction sector is among the key drivers boosted by rapid urbanization and infrastructure development, whereas flexible packaging applications create an additional level of demand for the market. Significant players such as Specialty Polymers Limited are improving product formulations to meet these performance-driven needs. C9 resins also play a vital role in the production of the Hydrocarbon Resins Industry globally, and they are gaining momentum in the production of industrial applications for improved processing and adhesion properties. Such a trend serves the strategic role of adhesives, promoting the global infiltration of this C9 Resin Market, especially in the developing economies.

C9 Resin Market Restraint

-

Natural Resins Replace C9 Hydrocarbon Resins Amid Growing Demand for Bio-Based, Eco-Friendly Alternatives

In the C9 Resin Industry, one of the key restraints is rising competition from substitutes. Natural tackifiers like rosin-based resins are being used more as a replacement for petroleum-derived C9 resins particularly for applications that promote bio-based and sustainable-based adhesives and coatings. These alternatives provide similar adhesion, gloss, and flexibility while aligning with strengthening regulatory and consumer preference towards sustainable materials. With industries adjusting to low-VOC, renewable and environmentally compliant products, rosin resins derived from pine trees, is challenging traditional C9 hydrocarbon resin. So, we are noticing huge levels of this trend to take place in industries such as packaging, automotive, and construction, where green labeling and carbon footprint reduction are of special importance. As such, increased prevalence of natural substitutes are adding to the growing pressure on C9 resin market players to innovate or diversify resin formulations.

C9 Resin Market Segmentation Analysis

By Product Type

The Hydrogenated C9 segment dominated the market and accounted for 68% of the C9 Resin market share. The dominance of this is mainly due to its good stability in color and low odor and also is been used in high-performance applications including adhesives, coatings, inks. This increases UV resistance and thermal stability, making this type of film ideal for outdoor or other high-performance industrial applications. Furthermore, hydrogenated versions are the popular choice in premium applications demanding enhanced cosmetic and functional characteristics. Applications in various end-use industries are widening by their compatibility with other resins and polymers, which continues to consolidate their dominance in the C9 resin segment.

Non-hydrogenated C9 resin is projected to be the fastest-growing product type due to its cost-effectiveness and widespread use in applications that do not require high color or UV stability. These resins are suggested for budget-sensitive segments including printing inks, rubber compounding, and general-purpose adhesives. The demand for low-cost but effective resin solutions is picking pace, as industrial activity picks up in emerging economies. The rapid growth of the Asia-Pacific, Central, & South America market with the positive outlook will primarily drive the market, owing to the high traction for tackifying and compound performance and growing applications in road marking and packaging.

By Application

Adhesive and sealants emerge as the leading application segment in the C9 resin market due to the resin’s excellent tackifying properties. C9 resins add significantly to adhesion, flexibility, and bond strength, which is why they are a favorite with hot-melt and pressure-sensitive adhesives for packaging, construction, and automotive industries. This compatibility with synthetic rubbers and thermoplastics ensures better product performance, thus aiding in large-scale industrial applications. The growth of this segment is primarily attributed to its status as the most widely used market segment of all application areas, driven by the increasing need for reliable bonding solutions in infrastructure and manufacturing.

The printing ink segment is the fastest-growing application area for C9 resins. The trend is powered by increasing demand for flexible packaging and demand for high-quality printing in the food, beverage and e-commerce space. For fast-turnaround printing operations, C9 resins improve gloss, adhesion, and drying speed of inks which are essential. With the growing demand for resin additives compounds for clarity, consistency, and print durability in the digital and packaging printinvestments are further growing in the digital ink market, particularly in the Asia-Pacific regions. The economical price and design adaptability of the C9 resins are additional factors that contribute to the popularity of the C9 resin among printing ink manufacturers looking to optimize their cost to performance equation.

By Form

Granules dominate the C9 resin market by form due to their ease of handling, storage, and transportation. Special preference is offered to Granular form resins in industrial processing owing to their uniform melting and lower dust formation and better feeding for production as compared with their polymeric parts form resins. This is imperative in key applications where fill speed and stability is crucial, such as adhesives and coatings, there are many examples of wide spread popularity. Besides, granules have the best viability and packaging benefit over flake and fluid types which is one of the reasons why they are the benchmark in broad industrial applications. It is this convenience coupled with performance value that make them dominant in the market.

Solution or liquid form of C9 resin is witnessing the fastest growth owing to its superior dispersion characteristics and easier incorporation into formulations, especially in coatings and inks. Such form enables the needed uniformity and coverage on the surface, making it a material of choice in industrial coatings, road markings and printing applications. The growing demand for ready-to-use or low-viscosity products due to automation and accuracy in the production process, increases its growth. In addition to this, liquid resins are being increasingly used in solvent-borne systems which will add up to the market growth curve largely in the countries with developing regulatory environment.

By End-Use Industry

The building and construction segment dominates the end-use industry for C9 resins due to the wide application of adhesives, sealants, and waterproofing agents. C9 resin plays an important role in the manufacture of high-performance materials used in infrastructure development for bonding, insulation and protective coatings. This dominance earlier derives from the growing global requirement for commercial and residential construction projects, especially across developing economies. Also, the long-lasting and cost-effective solutions are highly required in construction adhesives and bitumen modification which in turn will support the widespread use of C9 resins.

Packaging is emerging as the fastest-growing end-use industry for C9 resins due to booming global demand for flexible, durable, and high-performance packaging solutions. Such resins are important in the production of pressure sensitive and hot-melt adhesives that are utilized in cartons, labels, and tapes. As e-commerce and FMCG (fast-moving consumer goods) sectors continue to expand in Asia and South America, the demand for the efficient packaging material is only going to grow. Besides, growing need for light weight, tamper-evident and attractive packaging also continues to drive the absorption of C9 resins, which in turn will continue to make it fastest growing end-use industry segment.

C9 Resin Market Regional Outlook

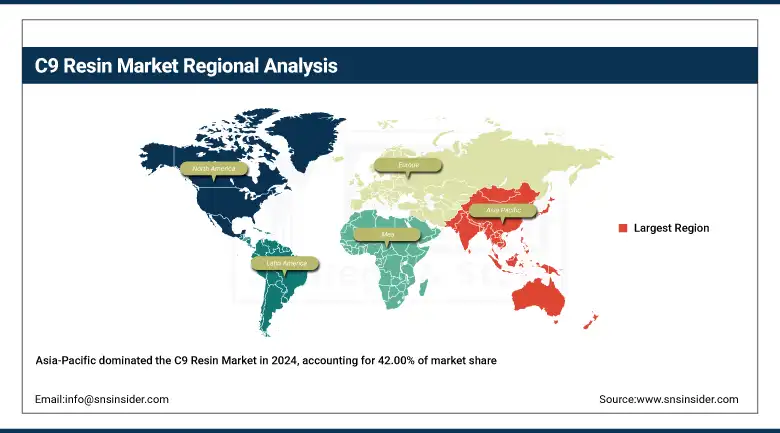

The Asia-Pacific region dominated the global C9 resin market in 2024, accounting for 42.00% of the total market share. The high industrial base in the region, particularly in China and India, where booming urbanization, infrastructure development, and an elevated demand of adhesives, coatings, and rubber compounding materials only fuel this leadership. Moreover, the large presence of some of the leading manufacturers, as well as available raw material, adds to its grim dominance. Moreover, increasing automotive production and demand for packaging and construction industries are propelling the application of C9 resins over a wide range of applications. Thanks to beneficial policies and increasing export, C9 resin production and consumption shifts to Asia-Pacific which is still the dominant region in the world.

Get Customized Report as per Your Business Requirement - Enquiry Now

China is the dominant country in the C9 resin market due to its large-scale production capacity, robust petrochemical infrastructure, and strong demand from industries like adhesives, coatings, and rubber. Its well-integrated supply chain and high domestic consumption secure its leading position in the region.

North America is emerging as the fastest-growing region in the global C9 resin market. Technological advancements in resin formulation coupled with high demand for adhesives, sealants, and coatings in automotive and construction applications, is expected to drive the growth during the forecast period. An increasing number of renovation projects and infrastructure upgrades in the U.S. and Canada is complementing the demand for materials with superior durability and UV resistance required for coating. In addition, strict environmental regulations and present trend features are incentivizing producers to invest in innovative, sustainable C9 resins solutions. North America is becoming a prime enabler of growth in the coming years with its burgeoning chemical and manufacturing sectors coupled with the specialty applications focus fuelling the market.

Europe holds a significant share in the global C9 resin market due to its mature industrial base and well-established coatings, adhesives, and printing ink sectors. Countries such as Germany, France, and Italy, where C9 resins are used for their adhesion, thermal stability, and gloss-enhancing properties. Research and development resulting in innovations in resin chemistry and sustainability product lines are robust as well in the region. Europe continues to be a major and stable market, with moderate growth compared to other regions, driven by consistent demand and regulatory alignment towards sustainability.

C9 Resin Market Companies are:

Arakawa Chemical Industries Ltd, Cray Valley, DuPont, Eastman Chemical Company, ECPlaza Network Inc., Exxon Mobil Corporation, Henan Anglxxon Chemical Co., Ltd, Henan Sanjiangyuan Chemical Co., Ltd., Kemipex, Kolon Industries, Inc., Lesco Chemical Limited, Neville Chemical Company, Puyang Ruisen Petroleum Resins Co., Ltd, Shanghai Jinsen Hydrocarbon Resins Co., Limited, ZEON CORPORATION, Formosan Union Chemical Corp. (FUCC), Qingdao Bater Chemical Co., Ltd, Shandong Landun New Material Co., Ltd, PetroChina Company Limited, Idemitsu Kosan Co., Ltd.

Recent Development

In February 2025, Idemitsu Kosan announced plans to build a large-scale lithium sulphide plant at its Chiba refinery to support Toyota's next-gen EV batteries. The plant, set to be completed by June 2027, will produce enough solid electrolytes for 50,000–60,000 EVs annually. A pilot facility is scheduled by the end of fiscal 2025.

In May 2023, South Korea’s Kolon Industries Inc., a leading industrial materials manufacturer, announced a USD 17.94 million investment to expand its high-purity aromatic petroleum resin (PMR) production facility at its Yeosu plant in South Jeolla Province.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 2.09 Billion |

| Market Size by 2032 | USD 3.18 Billion |

| CAGR | CAGR of 5.39% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Application (Paint & Coating, Adhesive & Sealants, Printing Ink, Rubber & Tire, Others [Tapes, Labels, etc]) • By Product Type (Hydrogenated C9 Resin, Non-Hydrogenated C9 Resin) • By Form (Granules, Flakes, Solution/Liquid) • By End-Use Industry (Automotive, Building & Construction, Packaging, Printing, Others [Electronics etc]) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Arakawa Chemical Industries Ltd, Cray Valley, DuPont, Eastman Chemical Company, ECPlaza Network Inc., Exxon Mobil Corporation, Henan Anglxxon Chemical Co., Ltd, Henan Sanjiangyuan Chemical Co., Ltd., Kemipex, Kolon Industries, Inc., Lesco Chemical Limited, Neville Chemical Company, Puyang Ruisen Petroleum Resins Co., Ltd, Shanghai Jinsen Hydrocarbon Resins Co., Limited, ZEON CORPORATION, Formosan Union Chemical Corp. (FUCC), Qingdao Bater Chemical Co., Ltd, Shandong Landun New Material Co., Ltd, PetroChina Company Limited, Idemitsu Kosan Co., Ltd. |

Frequently Asked Questions

The Asia-Pacific region dominated the C9 Resin market in 2024.

The “Hydrogenated C9” segment dominated the C9 Resin market.

C9 Resin Market Surges Globally on Rising Demand from Adhesives, Construction, And Flexible Packaging Sectors

The C9 Resin market was USD 2.09 billion in 2024 and is expected to reach USD 3.18 billion by 2032.

The C9 Resin market is expected to grow at a CAGR of 5.39% from 2025-2032.

Get in Touch