Cable Lugs Market Report Scope & Overview:

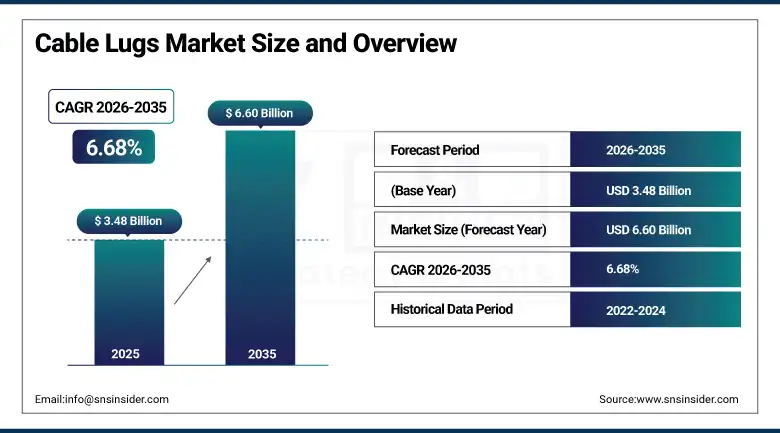

The Cable Lugs Market was valued at USD 3.48 Billion in 2025 and is expected to reach USD 6.60 Billion by 2035, growing at a CAGR of 6.68% from 2026 to 2035.

Cable lugs are essential electrical connectivity components used to terminate cable ends and connect them to electrical equipment, busbars, and connection points across a wide range of industrial, commercial, and infrastructure applications. The global cable lugs market has maintained steady growth momentum owing to the expansion of power transmission and distribution networks, accelerated installations of renewable energy sources, rapid urbanization fueled infrastructure development and the gradual industrial automation trend that is expanding electrical systems across manufacturing, process and heavy industries across the globe. From the wiring in our homes to the high voltage infrastructure in substations, cable lugs are a staple of any electrified system, assuring a steady replacement market as well as growth in volume from new installations.

TE Connectivity Ltd., a global leader in connectivity solutions, reported annual revenues exceeding USD 15 billion in its most recent fiscal year, with its Industrial Solutions segment identifying electrical connectivity components including cable lugs and terminal products as sustained growth contributors supported by global electrification infrastructure investment and industrial automation expansion.

Market Size and Forecast

-

Market Size in 2026E: USD 3.69 Billion

-

Market Size by 2035: USD 6.60 Billion

-

CAGR: 6.68% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information On Cable Lugs Market - Request Free Sample Report

Cable Lugs Market Trends

-

Renewable energy expansion is increasing demand for high-capacity cable lugs in solar and wind power installations.

-

Industrial automation growth is driving cable lug adoption in control panels, machinery, and motor systems.

-

Rising EV charging infrastructure deployment is boosting demand for high-current electrical connection solutions.

-

Grid modernization and transmission network upgrades are supporting growth in high-voltage cable lug applications.

-

Stricter electrical safety regulations are accelerating replacement demand for certified and insulated cable lugs.

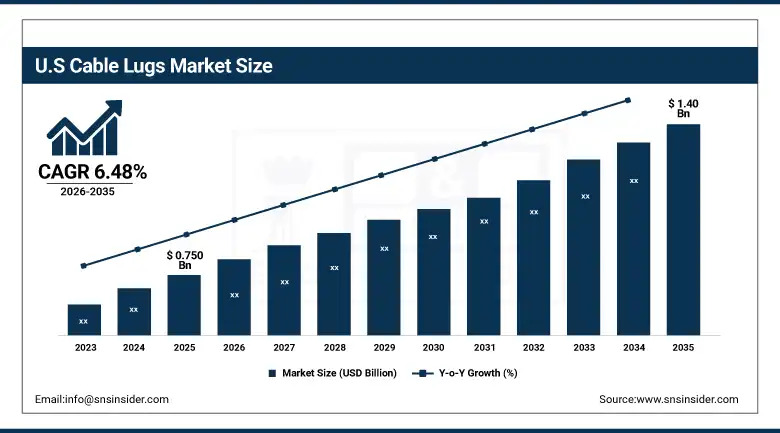

The U.S. Cable Lugs Market Outlook

The U.S. Cable Lugs Market was valued at USD 0.750 Billion in 2025 and is expected to reach USD 1.40 Billion by 2035, growing at a CAGR of 6.48%.

The United States dominates the national cable lugs market in North America, buoyed by the scale of its electrical infrastructure investment programs, the extensive renewal activity across its transmission and distribution grid and the broad base of industrial manufacturing, construction and energy sector activity, which combine to create a steady demand for cable connectivity products. U.S. federal infrastructure investment programs (grid modernization, clean energy integration, broadband network expansion) collectively have delivered unprecedented levels of capital to the electrical infrastructure sector and supported high levels of cable lug consumption in new installation and system upgrade scenarios.

More than 70% of EV charging station deployments utilize copper-based cable lugs due to their superior conductivity and performance under high-current operating conditions. More than 50,000 public EV charging locations across the U.S. require high-current cable termination systems, creating a growing market for specialized cable lug solutions designed for fast-charging applications.

Cable Lugs Market Segment Analysis

-

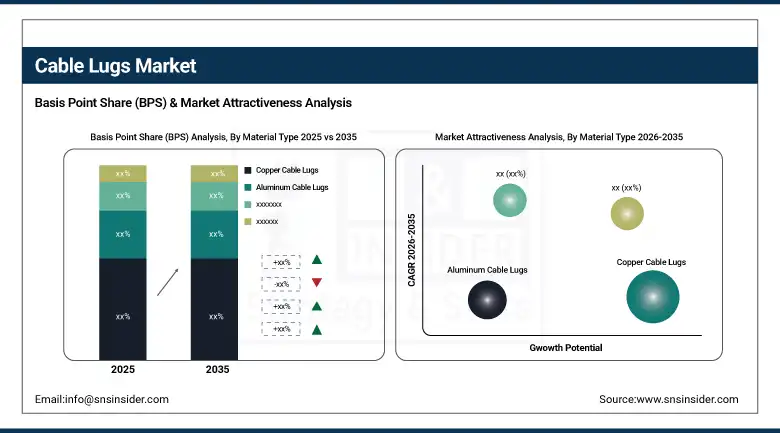

By Material Type, copper cable lugs dominated the market with 54.09% share in 2025, while bimetallic cable lugs are the fastest growing material segment with the highest CAGR of 7.84% from 2026 to 2035.

-

By Product Type, compression cable lugs dominated the market with 31.46% share in 2025, while mechanical cable lugs are the fastest growing product type with the highest CAGR of 7.74% from 2026 to 2035.

-

By Voltage Type, low voltage cable lugs dominated the market with 46.15% share in 2025, while high voltage cable lugs are the fastest growing voltage segment with the highest CAGR of 7.17% from 2026 to 2035.

-

By End-Use Industry, power & utilities dominated the market with 35.04% share in 2025, while automotive & transportation is the fastest growing end-use segment with the highest CAGR of 8.01% from 2026 to 2035.

By Material Type, copper cable lugs dominate the cable lugs market, while bimetallic cable lugs are the fastest-growing segment.

Copper cable lugs accounted for the largest market share in 2025, with a share of around 54.09% of total revenue. High electrical conductivity of copper, its long-standing use in power distribution, industrial and commercial electrical installations, and the availability of copper conductor cables are all factors that support a strong demand for compatible copper lug termination products. Copper cable lugs are the preferred specification for installations across the globe in the utility, industrial and construction sectors due to their excellent corrosion resistance, high current-carrying capacity, easy soldering and crimping and compliance with global electrical standards.

The segment of bimetallic cable lugs is expected to grow at the highest CAGR of 7.84% during the forecast period of 2026-2035 due to the rising deployment of aluminum conductor cables in power distribution networks, renewable energy installations and industrial facilities where the weight and cost benefits of aluminum conductors are becoming more attractive as compared to copper alternatives. The global proliferation of mixed-metal electrical systems through grid modernization and integration of renewable energy is propelling the adoption of bimetallic cable lugs in key markets as a vital component for reliable aluminum-to-copper connections at equipment terminals, busbars and switchgear interfaces.

By Product Type, compression cable lugs dominate the cable lugs market, while mechanical cable lugs are the fastest-growing segment.

The compression cable lugs segment accounted for the highest revenue share of 31.46% in 2025, owing to their superior mechanical and electrical performance characteristics that make them the preferred specification for high-reliability applications such as power utility infrastructure, industrial motor connections and switchgear installations. Compression lugs are the standard specification for all applications where the connection integrity is critical to system reliability and safety. The compression termination method creates a gas-tight, low resistance connection that resists oxidation, vibration loosening and thermal cycling. The widespread availability of hydraulic and battery-powered compression tools has also made field installation easier in a wide variety of project settings.

The mechanical cable lugs segment is expected to register the fastest CAGR of 7.74% during 2026-2035, owing to the expanding field service applications, where tool-free or minimal-tool installation is valued, increasing adoption in data center, telecommunications and building services applications, where flexibility and ease of re-termination are operationally important, and growing preference for mechanical lugs in retrofit and upgrade projects, where access constraints make hydraulic compress The category is also supporting above average growth driven by the growing installed base of mechanical lug applications in emerging markets where availability of specialized tools is limited.

By Voltage Type, low voltage cable lugs dominate the cable lugs market, while high voltage cable lugs are the fastest-growing segment.

The low voltage cable lugs segment held the maximum share of the market in 2025 with 46.15% and is anticipated to remain dominant throughout the forecast period due to the omnipresent existence of low voltage electrical systems across residential, commercial, industrial, and infrastructure applications, constituting the widest and volumetrically significant segment of the global electrical cable installation base. The huge volume of construction, renovation and industrial facility activity that requires low voltage cable termination means that the demand for standard-specification low voltage lug products is consistently high volume and across all geographies and end-use sectors world-wide.

The high voltage cable lugs segment is expected to register a rapid CAGR of 7.17% during the forecast period of 2026-2035 driven by the increasing investments in high-voltage transmission infrastructure, HVDC interconnection projects, offshore wind farm cable systems, and grid expansion programs in the fast-electrifying emerging economies. The technical complexity and higher unit value of high voltage cable lug products, together with the capital intensity of the infrastructure projects in which they are deployed, support above-average revenue growth relative to the broader market expansion rate through the forecast period.

By End-Use Industry, power & utilities dominates the cable lugs market, while automotive & transportation is the fastest-growing segment.

The power & utilities segment held the largest share of the cable lugs market with a revenue share of 35.04% in 2025 due to the huge size of the global electricity generation, transmission, and distribution infrastructure, which requires the highest volume of cable termination products from any single end-use segment. Power utility infrastructure at all voltage levels from low-voltage secondary distribution to high-voltage transmission requires reliable cable lug products from generating stations to substations to distribution networks. This diversified demand includes the full spectrum of cable lug product categories and high volumes for new installation as well as ongoing maintenance and replacement activities.

Automotive & transportation segment is projected to witness the fastest CAGR of 8.01% during the forecast period of 2026-2035 due to the electrification of vehicle propulsion systems, the rapid expansion of EV charging infrastructure globally, and the increasing electrical complexity of modern vehicles that requires greater numbers of high-quality cable termination components per unit. The growth of battery electric vehicle production, hybrid electric systems, and the extensive charging network infrastructure deployment programs of major economies are all driving unprecedented demand growth in the automotive-grade and charging infrastructure cable lug product categories.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.54% |

|

Asia Pacific |

China |

41.89% |

|

Europe |

Germany |

29.33% |

|

Middle East & Africa |

UAE |

35.06% |

|

Latin America |

Brazil |

43.25% |

North America Cable Lugs Market Insights

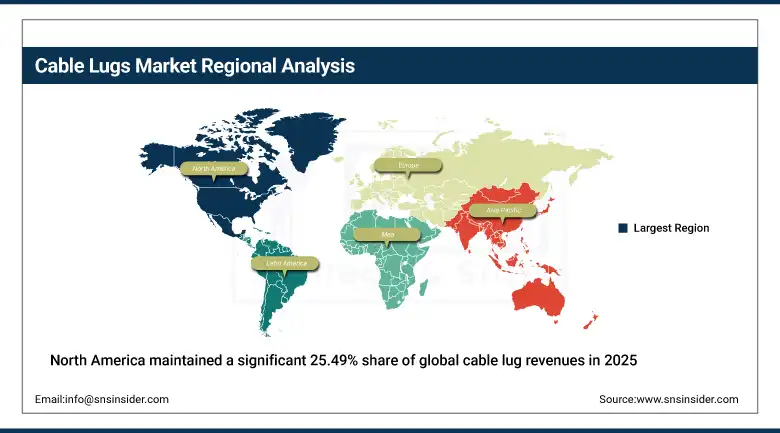

North America maintained a significant 25.49% share of global cable lug revenues in 2025, with the United States accounting for 84.54% of regional revenues. The North American market is characterized by ongoing infrastructure renewal activity, the scale of industrial manufacturing facilities that need electrical system maintenance and upgrade, and the growing installation of clean energy infrastructure that requires large amounts of high-quality cable termination products. Provisions in the U.S. Infrastructure Investment and Jobs Act and Inflation Reduction Act providing support for clean energy deployment have directed large sums toward electrical infrastructure projects, which are fueling above-average growth in cable lug demand compared to historic consumption trends.

Canada provides complementary demand through its resource extraction sector electrical requirements, expanding renewable energy capacity including hydropower and wind, and increasing industrial manufacturing activity. The Canadian market's geographic concentration in resource-rich provinces creates specialized demand patterns for rugged, environmentally resistant cable lug products suited to the demanding installation environments of mining, oil sands, and heavy industrial applications.

The region operates more than 8 million miles of electricity transmission and distribution infrastructure, creating sustained demand for cable lugs in utility maintenance and expansion projects. Over 65% of grid modernization projects across the U.S. and Canada utilize advanced compression and bimetallic cable lug solutions. More than 70% of public EV fast-charging installations employ high-current copper cable lugs for reliable power transfer.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Cable Lugs Market Insights

The European cable lugs benefits from the region’s large industrial manufacturing base, the strong building renovation programs driven by EU energy efficiency directives, and the large-scale renewable energy infrastructure investment under the Repower EU framework and national clean energy transition programs. Germany is the European revenue leader, thanks to being the region’s largest manufacturing economy, and hosting a significant amount of electrical equipment manufacturing activity. German producers’ engineering and export-oriented cable lug manufacturing competencies complement domestic industrial demand, supplying both regional and global markets. Significant demand is driven by solar energy deployment programmers and by building construction and renovation activities in Southern Europe, especially in Italy, Spain and France.

Europe's renewable energy investments under the REPowerEU plan target over 600 GW of installed renewable capacity by 2030, creating a sustained multi-year pipeline of cable accessory and termination product demand that is expected to support above-average cable lug market growth across the continent through the forecast period. Nearly 55% of industrial electrical upgrade projects incorporate premium compression cable lugs to improve operational reliability.

Asia Pacific Cable Lugs Market Insights

Asia Pacific dominated the global cable lugs market in 2025, holding 36.15% of global revenues, representing the largest and fastest-growing regional market with a CAGR of 7.10% through 2035. China has the largest national share in the region, due to the scale of ongoing power grid expansion programs, the manufacturing intensity of its industrial base, and the magnitude of infrastructure construction activity that combined drive the highest absolute volume of cable lug consumption of any single country in the world. The Chinese government’s ongoing investment in ultra-high-voltage transmission infrastructure, expansion of renewable energy capacity and development of industrial parks sustains multi-year demand growth at volumes that make China alone the single most influential market driver for global cable lug demand.

Over 40% of new renewable energy installations globally are concentrated in Asia-Pacific, generating significant demand for power interconnection products. Industrial and manufacturing facilities represent nearly 35% of cable lug consumption across the region. More than 75% of new urban electrification projects utilize compression-type cable lugs for distribution network applications.

MEA & Latin America Cable Lugs Market Insights

In 2025, Middle East & Africa and Latin America together accounted for about 13% of the global total cable lug revenue, both regions witnessing above-average growth trends owing to investment in infrastructure development, power network expansion initiatives, and growing industrial activity of their fast-growing economies. The UAE ranks number one in Middle East & Africa revenues, due to the scale of construction activity, the sophistication of its commercial and industrial electrical infrastructure, and as a regional hub for distribution of cable products throughout the wider Gulf Cooperation Council market.

Brazil leads the Latin American cable lug market with its large industrial base, constant investment in power infrastructure and a substantial construction sector. Mexico’s export-driven manufacturing economy, with its large automotive and electronics manufacturing clusters, provides a large demand for industrial cable lugs, complementing Brazil’s utility and construction-oriented consumption pattern. The region's market expansion is adding a growing demand layer for high-quality cable terminations due to the region’s renewable energy buildout, particularly in solar and wind capacity.

Over 50% of newly commissioned substations utilize high-voltage cable lug systems designed for harsh environmental conditions. Industrial diversification programs and electrification projects are driving annual growth in cable lug installations across several African economies. More than 60% of regional cable lug demand originates from utility transmission and distribution projects.

Market Dynamics

Growth Drivers: Power infrastructure investment and renewable energy expansion

The global acceleration of power infrastructure investment, including grid expansion in emerging economies, grid modernization in developed markets, and the integration of renewable energy generation at unprecedented scale, represents the primary structural growth driver for the cable lugs market through the forecast period. Every increment of generating capacity, transmission line, substation, and distribution network installation creates demand for cable lug products at connection points throughout the power system, and the global magnitude of power infrastructure investment is at multi-decade highs in response to the energy transition imperative, electrification of transportation and heating, and electricity demand growth from data center and industrial expansion.

The rise of smart manufacturing and Industry 4.0 is increasing demand for high-reliability cable lugs as automated production systems require more robust and failure-resistant electrical connections.

Restraints: Raw material price volatility and counterfeit product competition

Cable lugs market is facing meaningful headwinds due to the continued volatility of copper and aluminum commodity prices that are the primary cost inputs into the manufacturing of cable lugs, and have a direct impact on product pricing, margin stability and cost competitiveness of cable lug procurement vis-à-vis total electrical project budgets. Global macroeconomic conditions, mining supply dynamics and a competing demand from the electric vehicle and renewable energy sectors lead to copper price volatility and procurement uncertainty for cable lug manufacturers and their customers in the construction, utility and industrial sectors that buy cable lugs as part of larger electrical system packages.

Opportunities: EV charging infrastructure and smart grid deployment

The global buildout of electric vehicle charging infrastructure represents one of the most important near-term market expansion opportunities for cable lug manufacturers. The high current requirements of fast and ultra-fast charging systems create demand for premium specification, high current rated cable lug products, which have technical requirements and unit values considerably higher than standard electrical installation applications. The scale of EV charging network deployment programs across North America, Europe and China, along with ongoing development of megawatt scale charging systems for commercial vehicles and freight transport, is creating a sustained high growth demand segment that is expected to contribute meaningfully to cable lug market volume and value expansion through the forecast period.

Grid modernization and resilience investment programs being executed by utilities across major economies to deploy smart grids are driving demand for cable lug products within substation automation, distributed energy resource integration and transmission monitoring applications, where a combination of new installation and system upgrade activity is driving project-driven demand growth. The growing use of battery energy storage systems at utility, commercial and industrial scale is another demand driver for specialized cable lug products designed for the high-current, high-cycling battery connection environment.

Recent Developments:

-

2026: Panduit Corporation introduced its SmartZone cable management and termination system incorporating enhanced mechanical cable lugs with integrated installation verification features, targeting data center and critical infrastructure applications where connection quality assurance is operationally essential.

-

2026: Klauke GmbH, a leading European cable lug manufacturer, launched a new generation of insulated cable lugs with integrated color-coded cross-section identification for low and medium voltage distribution panel applications, improving installation accuracy and compliance in commercial building electrical systems.

-

2025: TE Connectivity Ltd. expanded its COPALUM connector series with enhanced bimetallic cable lug variants for aluminum-to-copper connections, targeting utility-scale solar and wind interconnection applications requiring certified transition connections at high current ratings.

-

2025: ABB Ltd. launched an extended range of compression cable lugs for HVDC transmission applications under its Installation Products division, designed to meet the demanding electrical and mechanical performance requirements of high-voltage direct current grid interconnection infrastructure.

Cable Lugs Market Key Players are:

-

TE Connectivity Ltd.

-

ABB Ltd.

-

Schneider Electric SE

-

Panduit Corporation

-

Eaton Corporation plc

-

Hubbell Incorporated

-

Thomas & Betts Corporation (ABB Installation Products)

-

Weidmüller Interface GmbH & Co. KG

-

Klauke GmbH

-

Cembre S.p.A.

-

3M Company

-

Legrand SA

-

HellermannTyton Group PLC

-

Phoenix Contact GmbH & Co. KG

-

LAPP Group

-

Siemens AG

-

Mencom Corporation

-

K.S. Terminals Inc.

-

MECATRACTION SAS

-

Jainson Cables India Pvt. Ltd.

Cable Lugs Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 3.48 Billion |

| Market Size by 2035 | USD 6.60 Billion |

| CAGR | CAGR of 6.68% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Material Type (Copper Cable Lugs, Aluminum Cable Lugs, Bimetallic Cable Lugs, Others) • By Product Type (Compression Cable Lugs, Ring/Tubular Cable Lugs, Pin Cable Lugs, Fork/Spade Cable Lugs, Blade Cable Lugs, Mechanical Cable Lugs) • By Voltage Type (Low Voltage, Medium Voltage, High Voltage) • By End-Use Industry (Power & Utilities, Industrial Manufacturing, Construction & Infrastructure, Oil & Gas, Automotive & Transportation, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | TE Connectivity Ltd., ABB Ltd., Schneider Electric SE, Panduit Corporation, Eaton Corporation plc, Hubbell Incorporated, Thomas & Betts Corporation (ABB Installation Products), Weidmüller Interface GmbH & Co. KG, Klauke GmbH, Cembre S.p.A., 3M Company, Legrand SA, HellermannTyton Group PLC, Phoenix Contact GmbH & Co. KG, LAPP Group, Siemens AG, Mencom Corporation, K.S. Terminals Inc., MECATRACTION SAS, Jainson Cables India Pvt. Ltd. |

Frequently Asked Questions

The cable lugs market is expected to grow at a CAGR of 6.68% from 2026 to 2035.

The cable lugs market was valued at USD 3.48 Billion in 2025.

The primary growth factors include the sustained global expansion of power transmission and distribution infrastructure investment, accelerating renewable energy installations requiring extensive cable termination products, that collectively generate structural demand growth across the full range of cable lug product categories.

Bimetallic Cable Lugs is the fastest-growing material type in the cable lugs market, with a CAGR of 7.84% from 2026 to 2035.

Asia Pacific dominated the cable lugs market in 2025, holding 36.15% of global revenues.

Get in Touch