LAN Cable Market Size & Key Insights:

The LAN Cable Market Size was valued at USD 14.08 Billion in 2023 and is expected to reach USD 44.41 Billion by 2032 and grow at a CAGR of 13.63% over the forecast period 2024-2032.

The LAN (Local Area Network) Cable Market is undergoing transformative growth, which is being driven by the increasing need for high-speed and reliable network connectivity across residential, commercial, and industrial sectors. Global government policies and initiatives have taken up significant roles in terms of further boosting the demand in 2023 and 2024. For example, Europe's "Digital Decade" program focuses on full digital transformation, while India's "Digital India" initiative is focused on strengthening broadband infrastructure.

Get more information on LAN Cable Market - Request Sample Report

For instance, India is preparing for a significant advancement in digital connectivity with the introduction of three new subsea cable projects. In August 2024, reports indicated that projects—2Africa Pearls, India-Asia-Express (IAX), and India-Europe-Express (IEX)—are anticipated to increase India’s internet capacity fourfold, greatly enhancing the speed and dependability of its digital connectivity. Similarly, in the United States, a good amount of investment has gone into legacy networks upgradation as well as to promote advanced connectivity solutions in their infrastructure development agenda. These programs have boosted high-performance LAN cables deployment in the urban and industrial centers.

Technology is also remodeling the LAN cable market landscape. Innovations such as Cat 7 and Cat 8 cables, which provide ultra-fast data transfer speeds and minimal interference, gained significant traction in 2024 and are set to expand further in 2025. The growing adoption of IoT devices, smart homes, and industrial automation systems necessitates robust and efficient LAN cables to handle complex network requirements. Other innovations brought to the table in 2023 were environmentally friendly LAN cables, driven by the trend towards green and consumer-friendly products across the world.

The opportunities ahead for the LAN cable market are limitless, as is the promise that a variety of emerging trends bring. Rising dependency on cloud computing and other forms of digital services has caused data centers to increase dramatically and have become very popular; such infrastructure requires more complex LAN cables. Other major growth drivers are the deployment of 5G networks and smart city projects in countries across the globe. Over 75% of the global organizations will implement hybrid work models by 2024, meaning more dependability in remote working network solutions will drive demand for LAN cables.

Government and industry sources show data on the significant role LAN cables play in modernizing digital ecosystems. Continued investment in the upgrade of digital infrastructure and advances in cable technology mean that the LAN cable market is here to stay, an integral part of global connectivity solutions that drives innovation and economic development.

LAN Cable Market Dynamics

Key Drivers:

-

Expansion of Data Centers and Increasing Need for High-Performance LAN Cables in Hybrid Cloud Age

Data centers are very crucial in the support of global internet and cloud services. The data center deployment is expected to increase by 25% by 2024, with exponential growth in the generation, storage, and processing of data. New data centers are being established, and the private and government sectors are contributing significantly, particularly from the U.S., India, and China. LAN cables are very crucial for the interconnection of servers and for fast, low-latency data transfer.

As more than 80% of the enterprises are likely to shift towards hybrid cloud solutions by 2024, demand for high-performance LAN cables like Cat 6 and Cat 7 is going to increase dramatically. These cables ensure the required bandwidth and reliability needed for handling heavy loads of data and, thus, are a significant part of the modern data center infrastructure.

-

Increasing Need for LAN Cables Fueled by IoT Development and Expansion of Smart Home Technologies

There is an ever-increasing level of proliferation with IoT and smart home devices as it continues to grow worldwide; the estimation reached 35% in 2023. At the same time, there would be an exceeding number of interconnected IoT devices - more than 32 billion-in 2030 worldwide. They strictly depend on LAN cables for proper and efficient communication networking.

Fast developing smart home technology, particularly among North American and European customers, has boosted their demand for such network infrastructures. LAN cables, especially Cat 7 and Cat 8, are necessary for providing the gigabit speeds with minimal interference to support these applications. Governmental initiatives that enhance digital transformation are also increasing through subsidies on smart devices in places like Germany and the U.S. Therefore, the demand for LAN cables also increases.

Restrain:

-

The cost of installing and maintaining LAN cable networks is still a major challenge for the market.

High installation and maintenance costs have hindered the adoption of LAN cables in some regions, especially in developing economies. For example, installing advanced LAN cable networks such as Cat 7 or Cat 8 is 40% more expensive than standard options. These costs include purchasing high-grade materials, specialized labor for installation, and maintenance. Small and medium-sized enterprises (SMEs), which constitute 70% of businesses in emerging markets, usually find these costs too expensive. In addition, the cost of upgrading legacy systems to support newer LAN cables adds to the expense.

Government subsidies and tax benefits in North America and Europe have partly compensated for these costs, but other regions are limited by such incentives. In these cost-sensitive markets, the business continues to use less advanced alternatives, and the modern LAN cable is not used on a mass scale. This is the main reason why these cost-related issues must be overcome in order to realize the full potential of the LAN cable market.

Local Area Network Cable Market Segment Analysis

By Application

In 2023, the Industrial Use segment dominated the LAN Cable Market, accounting for 48% of the market share. This is largely due to increased use of LAN cables in manufacturing units, logistics stations, and similar industrial establishments needing high-speed data transfer and effective network connectivity. The incorporation of automation and robots in industries escalated the demand for advanced LAN cables as well.

During the forecast period of 2024-2032, the Industrial Use segment is expected to grow at the fastest CAGR of 13.78%. It is driven by the emergent Industry 4.0 and smart factories that require high-bandwidth LAN cables for interconnected machines and real-time data analytics. Industry initiatives such as Germany's "Industry 4.0" program also are expected to boost further this segment. The remaining applications, which comprise commercial and residential uses, maintain a steady level of growth with the rising penetration of IoT devices and smart home technologies.

By Type

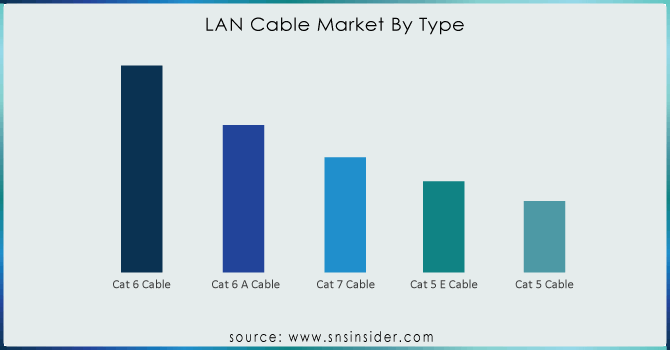

In 2023, Cat 6 cables dominated the LAN Cable Market. This type of cable was used in 33% of the market share because of its widespread application in commercial and residential areas. Cat 6 cables are superior in performance for gigabit Ethernet, which makes them applicable to many applications where reliable connectivity is needed.

The Cat 7 cable segment is expected to grow at the fastest CAGR of 14.40% during the forecast period of 2024-2032. Cat 7 cables offer better performance, including higher bandwidth and reduced interference, making them ideal for modern data centers and industrial networks. Increasing high-speed network deployment and a shift towards 10 Gbps Ethernet standards are driving demand for Cat 7 cables. In addition, the advancement of technology and growth in future-proofed networking infrastructure are definitely going to add considerable value to the market segment.

LAN (Local Area Network) Cable Market Regional Overview

North America led the LAN Cable Market in 2023, with 36% of the market share. This can be attributed to the high penetration of advanced networking solutions in both industries and residential sectors. In addition, huge investments in data centers and supportive government policies toward digital infrastructure have increased the demand for LAN cables in the U.S. and Canada.

Europe is expected to lead the market in terms of CAGR at 13.95% during the forecast period of 2024-2032. This is due to rising investments in smart city projects and the adoption of Industry 4.0 technologies. Germany, France, and the U.K. are leading the way in digital infrastructure upgradation, which is a lucrative opportunity for LAN cable manufacturers.

Need any customization research on LAN Cable Market - Enquiry Now

Key Players

Some of the Major Players in the LAN Cable Market Are

-

Belden Inc. (Cat 6 Cables, Cat 5e Cables)

-

Nexans (Cat 7 Cables, Cat 6A Cables)

-

Prysmian Group (Fiber Optic Cables, Cat 6 Cables)

-

Leviton Manufacturing Co., Inc. (Patch Cords, Ethernet Cables)

-

CommScope (Coaxial Cables, Fiber Patch Panels)

-

Schneider Electric (Cat 6A Cables, Patch Panels)

-

Panduit (Copper Cables, Fiber Optic Cables)

-

Siemon (High-Speed Patch Cords, Cat 7 Cables)

-

Superior Essex (Cat 5e Cables, Coaxial Cables)

-

TE Connectivity (RJ45 Connectors, Cat 6 Cables)

-

General Cable (Ethernet Cables, Fiber Optic Cables)

-

LS Cable & System (LAN Cables, Fiber Optic Cables)

-

Molex (Patch Cords, Cat 6A Cables)

-

Corning Incorporated (Fiber Optic Solutions, Connectors)

-

Hitachi Cable America (Cat 6A Cables, Fiber Optic Cables)

-

Allied Wire & Cable (Bulk LAN Cables, Patch Cords)

-

AMP Netconnect (Copper LAN Cables, Fiber Patch Cords)

-

Draka Communications (Cat 6 Cables, Fiber Optic Cables)

-

3M (Fiber Connectors, Cable Assemblies)

-

Fujikura (Fiber Cables, Connectors)

Major Suppliers (Components, Technologies)

-

Dow Chemical (Insulation Materials, Conductors)

-

BASF SE (Polymer Materials, Additives)

-

DuPont (Flame Retardants, Jacketing Materials)

-

Borealis AG (Polyethylene Compounds, Cable Insulation)

-

SABIC (Polypropylene, Polyethylene)

-

Arkema (Specialty Polymers, High-Performance Compounds)

-

Covestro (Polyurethane, Advanced Resins)

-

ExxonMobil (High-Density Polyethylene, Cable Fillers)

-

Solvay (Polyvinyl Chloride, Advanced Polymers)

-

LG Chem (Plasticizers, PVC Compounds)

Major Clients

-

Microsoft

-

Amazon Web Services

-

AT&T

-

Google

-

Verizon

-

Cisco Systems

-

IBM

-

Facebook (Meta)

-

Huawei

-

Siemens

Recent Trends

-

August 2024: Prysmian, a leading global company in the energy and telecommunications cable systems sector, reports the successful conclusion of sea trial assessments for the ultra-deep installation of a 500 kV HVDC MI1 cable at a depth of 2,150 meters. This represents a record-setting installation in the LAN Cable Market, being the first instance of an HVDC cable being placed at such a depth, establishing new standards for the market.

-

July 2024: To progress with its strategy to reduce its substantial debt burden, CommScope has finalized an agreement to sell its outdoor wireless networks (OWN) division and its distributed antenna systems (DAS) operations to Amphenol Corp. for $2.1 billion.

| Report Attributes | Details |

|---|---|

|

Market Size in 2023 |

USD 14.08 Billion |

|

Market Size by 2032 |

USD 44.41 Billion |

|

CAGR |

CAGR of 13.63% From 2024 to 2032 |

|

Base Year |

2023 |

|

Forecast Period |

2024-2032 |

|

Historical Data |

2020-2022 |

|

Report Scope & Coverage |

Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

|

Key Segments |

• By Type (Cat 7 Cable, Cat 6 Cable, Cat 6 A Cable, Cat 5 Cable, Cat 5 E Cable) |

|

Regional Analysis/Coverage |

North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

|

Company Profiles |

Belden Inc., Nexans, Prysmian Group, Leviton Manufacturing Co., Inc., CommScope, Schneider Electric, Panduit, Siemon, Superior Essex, TE Connectivity, General Cable, LS Cable & System, Molex, Corning Incorporated, Hitachi Cable America, Allied Wire & Cable, AMP Netconnect, Draka Communications, 3M, Fujikura. |

|

Key Drivers |

• Expansion of Data Centers and Increasing Need for High-Performance LAN Cables in Hybrid Cloud Age. |

|

Restraints |

• The cost of installing and maintaining LAN cable networks is still a major challenge for the market. |

Frequently Asked Questions

Ans: North America dominated the LAN Cable Market in 2023.

Ans: The Cat 6 cables segment dominated the LAN Cable Market.

Ans: The major growth factors of the LAN Cable Market are Increased Deployment of Data Centers Worldwide and Increasing Adoption of IoT and Smart Home Devices.

Ans: LAN Cable Market size was USD 14.08 Billion in 2023 and is expected to Reach USD 44.41 Billion by 2032.

Ans: The LAN Cable Market is expected to grow at a CAGR of 13.63% during 2024-2032.

Get in Touch