Cannabis Cultivation Market Report Scope & Overview:

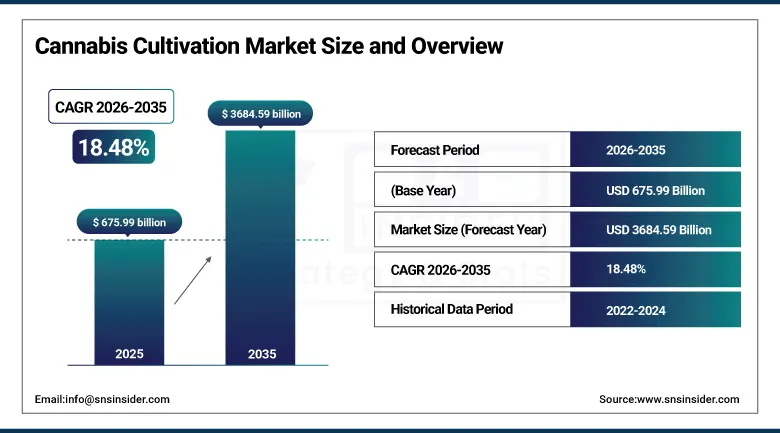

The Cannabis Cultivation Market was valued at USD 675.99 Billion in 2025 and is expected to reach USD 3,684.59 Billion by 2035, growing at a CAGR of 18.48% from 2026–2035.

The cannabis cultivation industry is witnessing a transition in terms of its life cycle stages due to globalization. In the wake of legalization of cannabis in North America, Europe, and Asia Pacific countries, cannabis becomes something different as it evolves from being an illicit substance to becoming an all-round agricultural, medicinal, and health product. The cannabis industry is propelled by the use of cannabis growth programs and systems within the retail and medicinal segments of the business.

Germany’s adult-use legalization in April 2024 opened one of Europe’s largest consumer markets. Thailand became the first Asian country to decriminalize cannabis cultivation in 2022, setting a precedent for regional reform. U.S. federal rescheduling discussions are advancing, which could unlock interstate commerce and institutional banking access for cultivators.

Market Size and Forecast

- Market Size in 2026E: USD 800.94 Billion

- Market Size by 2035: USD 3,684.59 Billion

- CAGR: 18.48% from 2026 to 2035

- Fastest Growing Region: Asia Pacific

- Largest Region: North America

To Get more information on Cannabis Cultivation Market - Request Free Sample Report

Cannabis Cultivation Market Trends

- The rise in precision agriculture technologies including IoT sensors, artificial intelligence-based crop monitoring techniques, and climate control systems will improve yield uniformity and reduce the cost of production per gram.

- Regional legalization in Europe, Asia-Pacific, and Latin America is resulting in an increase in the number of cultivation facilities along with investments made by institutions in the industry.

- The rise in the demand for pharmaceutical-grade cannabis with GMP certification will force cannabis producers to come up with standardized practices.

- The shift towards organic and terpene rich cannabis among consumers has generated premium product categories where wholesalers can demand higher prices.

- The use of alternative energy sources such as solar and geothermal energy in cultivation facilities will reduce operational costs.

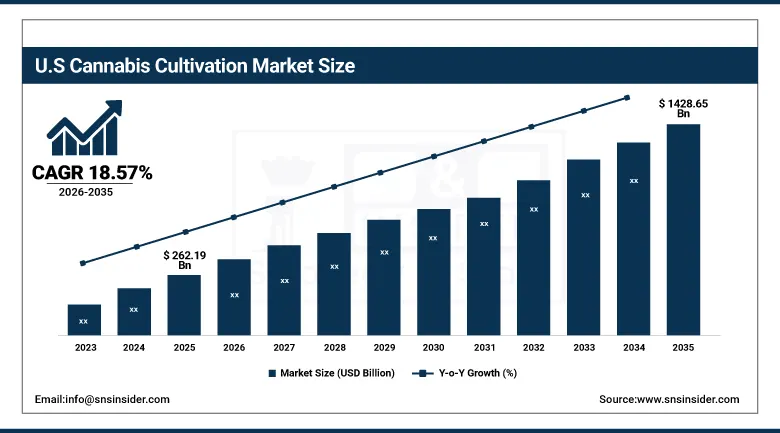

The U.S. Cannabis Cultivation Market Outlook

The U.S. Cannabis Cultivation Market was valued at approximately USD 262.19 Billion in 2025 and is expected to reach approximately USD 1,428.65 Billion by 2035, growing at a CAGR of 18.57%.

The United States is the world’s largest cannabis cultivation market. State-level adult-use and medical cannabis legalization programmes have created a mature licensed producer and dispensary ecosystem that now spans over 40 jurisdictions. The diversity of cultivation environments across U.S. states, from California’s outdoor sun-grown farms to Michigan’s large-scale indoor operations and Colorado’s greenhouse facilities, supports a highly varied commercial landscape with distinct cost structures and consumer positioning.

Canopy Growth’s February 2025 launch of its premium craft cannabis brand under a new retail partnership demonstrates the commercial tension in the U.S. market between mass-production scale economics and the craft quality premium that a growing consumer segment is willing to pay for. Both strategies have distinct and sustainable commercial futures in a market of the U.S.’s scale and consumer sophistication.

Cannabis Cultivation Market Segment Analysis

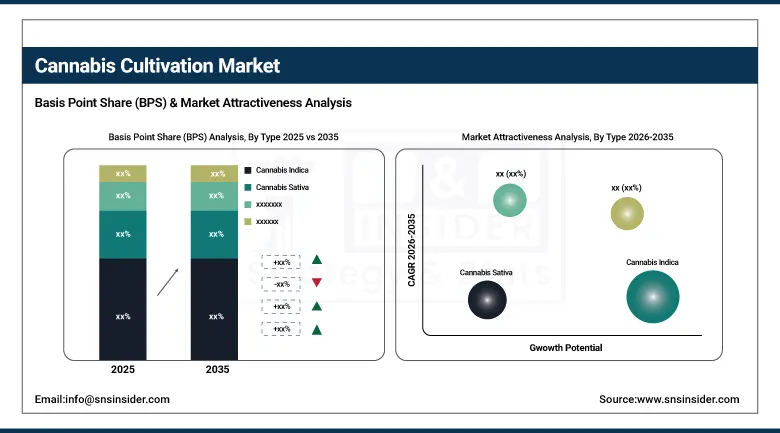

- By Type, Cannabis Indica held the largest share of approximately 45.62% in 2025, driven by strong consumer demand for its relaxation and therapeutic properties across both medical and recreational segments; Cannabis Sativa is expected to register the fastest CAGR of 19.23% during 2026–2035.

- By Biomass, Marijuana dominated the market with approximately 62.47% share in 2025 through its established recreational and medical consumer demand across legalized jurisdictions; Hemp is expected to register the fastest growth at a CAGR of 19.85%.

- By Technology, Indoor Cultivation accounted for the leading share of approximately 51.38% in 2025, driven by its ability to deliver consistent year-round harvests, precise cannabinoid profile control, and pharmaceutical-grade product quality requirements; Indoor Cultivation is also the fastest-growing technology at a CAGR of approximately 18.94%.

- By Cultivation Method, Soil-Based Cultivation contributed the largest revenue share of approximately 43.71% in 2025 through strong cultivator preference for organic growing methods, complex terpene development, and lower capital expenditure relative to hydroponic and aeroponic systems; Hydroponics is projected to grow at the highest CAGR of approximately 20.12%.

By Type, cannabis indica dominates, cannabis sativa grows fastest

Cannabis Indica maintained its status as the leading type with about 45.62% of cannabis production market shares in 2025. The type's dominance is attributed to consumer familiarity, wide scope of medical applications ranging from pain management to anxiety relief and sleeping disorders, established supply chain of commercially successful varieties that feature consistent growth patterns, as well as operational convenience associated with shorter flowering periods and compact growth of the plants themselves.

Cannabis Sativa remains the fastest growing type at CAGR of 19.23% until 2035. Growing consumer demand for Sativa's energizing effect and use of the type in various daytime recreational applications and wellness products contributes to its fast growth rate. Sativa's dominance in CBD hemp crops is also worth noting. With expanding global markets for CBD-containing products – from food and beverages to cosmetics and medicine – cultivars of Sativa are becoming a preferred choice when it comes to large-scale CBD hemp farming due to their favorable cannabinoid ratio. Regulatory allowances for Sativa's cultivation in new areas of APAC and LATAM regions will further fuel Sativa cultivation expansion without legal hurdles.

By Biomass, marijuana dominates, hemp grows fastest

Marijuana continued to maintain its lead in biomass production share with an estimate of about 62.47% of the cannabis growth industry in 2025. The leading market position of marijuana is attributed to the maturity of the commercial markets for recreational and medicinal use of marijuana, which together account for the largest revenue generation segment of the market. The cultivators of marijuana operate within well-regulated production and dispensing mechanisms, which ensure reliable commercial interaction between producers, processors, and retailers.

Hemp is the fastest-growing biomass segment at a CAGR of 19.85% through 2035. The growth reflects the extraordinary breadth of hemp’s commercial applications. CBD extraction for nutraceutical, cosmetic, and pharmaceutical products represents the largest current value driver. Industrial applications including hemp fibre for textile and composite material manufacturing, hemp seed protein for food products, and hemp hurds for construction materials are all growing commercially. The regulatory pathway for hemp cultivation is substantially less restrictive than marijuana in most jurisdictions, enabling wider geographic market development in Asia Pacific, Latin America, and sub-Saharan Africa where marijuana cultivation remains prohibited.

By Technology, indoor cultivation dominates and grows fastest

Indoor cultivation was the leading technological cultivation process in 2025, comprising around 51.38% of the cannabis cultivation market. This process offers the best environmental control among all other methods. Factors such as temperature, moisture levels, CO2 concentration, light quality, and irrigation timing can all be optimized to maximize the amount of cannabinoids in the crop. This is very important because the value of pharmaceutical cannabis and high-end retail cannabis is determined by the level of cannabinoids and terpenes contained in the product.

Indoor cultivation is simultaneously the fastest-growing technology at a CAGR of approximately 18.94% through 2035. This dual dominance reflects the compounding commercial advantages of ongoing technology improvement. LED horticultural lighting efficiency improvements are reducing electricity costs by 20 to 40% per crop cycle compared to high-pressure sodium systems. AI-powered crop management platforms are optimizing growing conditions in real time. Modular grow room designs are reducing capital expenditure and enabling faster facility commissioning. Each improvement cycle strengthens indoor cultivation’s economics relative to competing methods.

By Cultivation Method, soil-based dominates, hydroponics grows fastest

Soil-based growing maintained the leading cultivation method position with approximately 43.71% share of the cannabis growing market in 2025 due to its numerous advantages for cultivational and commercial purposes. It should be noted that the use of the soil allows developing highly diverse terpenoid and secondary metabolite expression profiles that cannot be achieved using less complicated nutrient solutions used in hydroponics or aeroponics at an equal level. It is especially important to mention the high economic value of these properties in the craft cannabis sector since sophisticated customers seek out products with unique aroma and flavor.

The hydroponics growing method shows the fastest growth rate, with a compound annual growth rate (CAGR) reaching approximately 20.12% until 2035. This growth indicates the tendency to focus more on yield optimization, water savings, and growing speed among the licensed producers of cannabis. Hydroponic technology can provide a 20% to 30% higher biomass yield per square foot in comparison to soil cultivating owing to direct nutrition supply to the plant root zone as well as the absence of pathogens. Water saving capacity is increased.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

83.4% |

|

Europe |

Germany |

24.3% |

|

Asia Pacific |

Thailand |

28.6% |

|

Middle East & Africa |

South Africa |

31.2% |

|

Latin America |

Colombia |

38.7% |

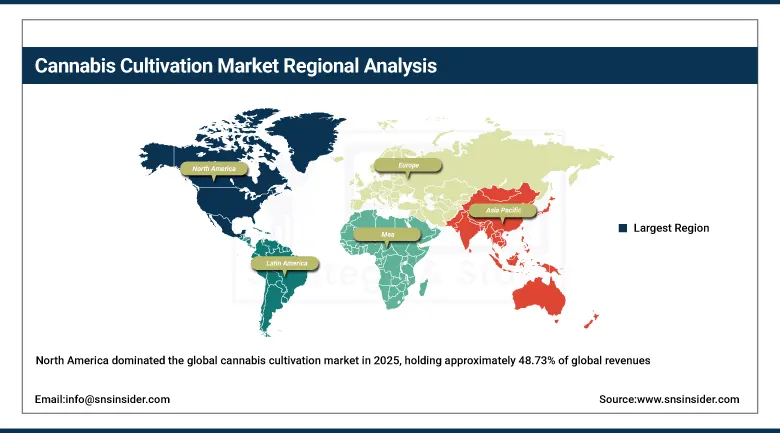

North America Cannabis Cultivation Market Insights

North America dominated the global cannabis cultivation market in 2025, holding approximately 48.73% of global revenues. The United States, representing approximately 83.4% of North American revenues, is the world’s largest cannabis cultivation market by significant margin. Canada’s federally regulated adult-use cannabis framework continues to support one of the world’s most mature licensed producer ecosystems. Canadian producers including Aurora Cannabis and Tilray Brands operate at commercial scale with GMP certification infrastructure that supports both domestic sales and international medical cannabis exports.

The U.S. market’s extraordinary scale reflects the commercial depth of 40+ state-level regulated markets whose collective consumer demand, retail dispensary density, and cultivator licensing programmes have created an agricultural sector of national economic significance. Multi-state operators are consolidating cultivation capacity to achieve cost efficiencies. Craft cultivators are differentiating on quality and consumer experience. Both strategies are commercially viable in a market of the U.S.’s scale and maturity.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Cannabis Cultivation Market Insights

Europe is an increasingly commercially significant cannabis cultivation market, driven by the progressive expansion of medical cannabis programmes across Germany, the United Kingdom, the Netherlands, Poland, and Scandinavian markets, and the landmark shift created by Germany’s adult-use legalization in April 2024. Germany accounts for approximately 24.3% of European cannabis cultivation revenues through its status as the EU’s largest medical cannabis consumer market and the first major EU economy to legalize adult-use cannabis.

The European cannabis cultivation market is characterized by strong demand for GMP-certified pharmaceutical-grade product. Domestic European cultivation capacity remains limited. The majority of medical cannabis consumed in Europe is currently imported from licensed producers in Canada, Portugal, Colombia, and Israel. This is creating significant commercial opportunity for European-licensed cultivation facilities able to operate at pharmaceutical quality standards within the EU regulatory framework.

Aurora Cannabis’ expansion of its Aurora Nordic 2 facility in Denmark adding 200,000 square feet of EU-GMP certified capacity in January 2025 illustrates the strategic investment that major producers are making to capture European medical market demand from within the EU rather than from export markets subject to import restrictions and regulatory uncertainty.

Asia Pacific Cannabis Cultivation Market Insights

Asia Pacific is the fastest-growing regional cannabis cultivation market at a CAGR of approximately 22.17% through 2035. Thailand became the first Asian country to decriminalize cannabis cultivation in 2022 and has since developed a regulated medical and wellness cannabis industry whose cultivation infrastructure is expanding rapidly. Australia’s well-developed medical cannabis licensing programme has created a significant domestic cultivation sector serving both local patient demand and export markets. South Korea, Japan, and India are at earlier stages of regulatory development but represent enormous potential markets given their population scale.

Thailand accounts for approximately 28.6% of Asia Pacific revenues, reflecting its first-mover advantage in the region as both a cultivator and regional export hub for medical cannabis products targeting the ASEAN market. Australia’s regulatory rigour and geographic isolation from major production markets have supported the development of a premium quality domestic industry whose GMP certification standards and export-oriented production capability position it as a significant supplier to Japanese and other future Asia Pacific medical markets as regional legalization progresses.

MEA & Latin America Cannabis Cultivation Market Insights

Middle East and Africa and Latin America are growing cannabis cultivation markets where regulatory reform is creating structured commercial opportunity for both domestic consumption and export. South Africa leads MEA revenues at approximately 31.2% of the regional total after the Constitutional Court’s ruling decriminalizing private cannabis use and cultivation. South Africa’s Mediterranean climate and low labour costs create compelling production economics for licensed outdoor cultivation targeting both domestic and European export markets.

Colombia leads Latin American cannabis cultivation revenues at approximately 38.7% of the regional total. Colombia’s combination of equatorial growing conditions enabling year-round outdoor cultivation, low production costs, established licensed export infrastructure, and a regulatory framework specifically designed to develop cannabis as an agricultural export commodity make it the most commercially advanced cannabis cultivation market in Latin America. Colombian exporters including Khiron Life Sciences, Clever Leaves, and PharmaCielo are actively supplying European medical cannabis markets where their cost-competitive GMP-certified product is meeting strong import demand.

Market Dynamics

Growth Drivers: Expanding legalization creating new legal cultivation markets, rising medical cannabis demand driving pharmaceutical-grade production investment

The primary structural growth driver for the cannabis cultivation market is the expanding legalization and regulatory reform wave that is progressively transforming cannabis from illicit agricultural activity into a licensed commercial sector across the world’s most significant economies. Each new jurisdiction that establishes a legal cultivation framework adds both a domestic consumer market and a potential export market to the global commercial ecosystem.

Medical cannabis demand is growing independently of recreational legalization. The evidence base for cannabis-based therapeutic applications is expanding across pain management, epilepsy, anxiety, and palliative care. This is compelling healthcare systems and reimbursement frameworks in Germany, the UK, and Australia to broaden patient access, which in turn drives licensed cultivation capacity expansion to serve prescription demand that is growing faster than existing supply can satisfy.

Precision cultivation technology is simultaneously improving the market’s economics. AI-powered growing platforms, LED efficiency improvements, and automated environmental control systems are reducing per-gram energy and labor costs consistently across harvest cycles. This improvement makes regulated legal cannabis increasingly competitive with illicit market pricing, supporting legal market penetration of consumer demand.

Restraints: Regulatory fragmentation creating compliance costs across jurisdictions, banking and financial services restrictions on cannabis businesses in the U.S.

One key limitation facing the growth of cannabis production companies is the existence of fragmented regulations within the state, national, and international legal systems. Cannabis producers in America operating in multiple jurisdictions are required to adhere to entirely different sets of rules regarding licensing, product testing, packaging, and reporting in each region. These additional costs make it difficult for small-scale producers and hinder their ability to operate across state borders.

The limited access to banking and financing facilities in the cannabis industry limits cannabis growers’ access to finance compared to farmers in traditional industries. The growers have no option other than to conduct business in cash, limiting their security and operational capabilities. Rescheduling of the cannabis plant by federal authorities would alleviate some limitations, while full banking access might require further legislation.

Price compression is a growing commercial challenge in mature regulated markets. As cultivation capacity has expanded in California, Oregon, and Colorado, wholesale cannabis prices have declined significantly from early-market highs. Cultivators in oversupplied markets face margin pressure that is consolidating the industry toward the most cost-efficient large-scale operators at the expense of smaller craft producers who cannot achieve comparable cost structures.

Opportunities: Cannabis export market development from low-cost producing nations to European medical markets

The international medical cannabis export market represents one of the most commercially significant opportunities for licensed cultivators in Colombia, Portugal, Thailand, South Africa, and Australia. European medical cannabis import demand is growing faster than domestic EU cultivation capacity can currently serve. Cultivators in low-cost production markets with GMP-certified facilities and established export infrastructure are positioned to capture significant long-term supply contracts with European pharmaceutical distributors and medical cannabis operators.

Hemp-derived CBD product market expansion across food, beverage, nutraceutical, and cosmetic applications is creating growing demand for pharmaceutical-grade hemp biomass whose consistent cannabinoid profiles and contaminant-free cultivation credentials support premium pricing above commodity hemp market rates. This opportunity is particularly commercially significant for cultivators willing to invest in the testing, documentation, and quality assurance infrastructure that premium CBD product brands require from their biomass suppliers.

Recent Developments:

- 2025: Aurora Cannabis completed the expansion of its Aurora Nordic 2 greenhouse facility in Denmark in January 2025, adding 200,000 square feet of EU-GMP certified cultivation capacity dedicated to supplying growing medical cannabis demand across German, UK, and Scandinavian markets, strengthening Aurora’s position as Europe’s leading licensed producer.

- 2025: Canopy Growth launched a new premium craft cannabis brand in February 2025 under a retail partnership targeting the growing consumer segment demanding small-batch, terpene-rich products, repositioning a portion of its Canadian cultivation capacity toward the premium craft segment whose wholesale pricing exceeds commodity indoor flower.

- 2025: Tilray Brands expanded its European medical cannabis distribution network by securing new pharmacy distribution agreements in Poland and Czech Republic, requiring incremental GMP-certified cultivation capacity from its Portuguese and German production facilities to serve growing patient demand in newly accessible European markets.

Cannabis Cultivation Market Key Players are:

- Curaleaf Holdings Inc.

- Trulieve Cannabis Corp.

- Green Thumb Industries Inc.

- Cresco Labs Inc.

- Aurora Cannabis Inc.

- Tilray Brands Inc.

- Canopy Growth Corporation

- Cronos Group Inc.

- Organigram Holdings Inc.

- Verano Holdings Corp.

- Acreage Holdings

- TerrAscend Corp.

- STIIIZY Inc.

- Khiron Life Sciences Corp.

- PharmaCielo Ltd.

- Clever Leaves International Inc.

- Harvest Health & Recreation Inc.

- iAnthus Capital Holdings

- Columbia Care Inc.

- 4Front Ventures Corp.

Cannabis Cultivation Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 675.99 Billion |

| Market Size by 2035 | USD 3,684.59 Billion |

| CAGR | CAGR of 18.48% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Type (Cannabis Indica, Cannabis Sativa, Cannabis Ruderalis) •By Biomass (Marijuana, Hemp) •By Technology (Indoor Cultivation, Outdoor Cultivation, Greenhouse Cultivation) •By Cultivation Method (Soil-Based, Hydroponics, Aeroponics, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Curaleaf Holdings Inc., Trulieve Cannabis Corp., Green Thumb Industries Inc., Cresco Labs Inc., Aurora Cannabis Inc., Tilray Brands Inc., Canopy Growth Corporation, Cronos Group Inc., Organigram Holdings Inc., Verano Holdings Corp., Acreage Holdings, TerrAscend Corp., STIIIZY Inc., Khiron Life Sciences Corp., PharmaCielo Ltd., Clever Leaves International Inc., Harvest Health & Recreation Inc., iAnthus Capital Holdings, Columbia Care Inc., and 4Front Ventures Corp. |

Get in Touch