Chemical Recycling Market Report Scope & Overview:

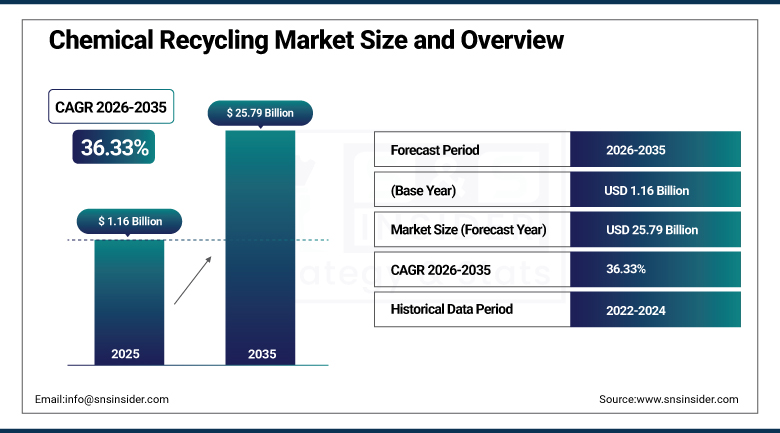

The Chemical Recycling Market was valued at approximately USD 1.16 billion in 2025 and is expected to reach around USD 25.79 billion by 2035, growing at a CAGR of 36.33% from 2026–2035.

The chemical recycling market is witnessing strong growth in the global market owing to increasing plastic waste generation and strict environmental regulations. Rising demand for circular economy solutions is supporting market expansion. Growing adoption of advanced recycling technologies is accelerating industry development. Manufacturers are focusing on converting difficult-to-recycle plastics into valuable feedstock. Expanding applications in packaging, automotive, and industrial sectors are creating new opportunities. Technological advancements in pyrolysis and depolymerization processes are improving efficiency. Increasing investments in sustainable waste management infrastructure are further accelerating market adoption.

As per the OECD & Global Plastics Outlook and UN Environment Programme 2025 plastics circularity indicators, only 9% of total plastic waste generated around the globe gets recycled, and chemical recycling is seen as a complimentary approach to a circular economy strategy in nations.

According to the European Commission 2025 waste framework directives, it is necessary for the member countries to reach the 55% of municipal waste recycling goals, which will promote the use of advanced recycling processes. In addition, the UNEP claims that around 400 million tonnes of plastic waste is produced each year worldwide, and less than 20% is recycled.

Market Size and Forecast:

-

Market Size 2026E: USD 1.59 billion

-

Market Size 2035: USD 25.79 billion

-

CAGR (2026 - 2035): 36.33%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Chemical Recycling Market- Request Free Sample Report

Chemical Recycling Market Trends:

-

Rapid increase in global plastic waste generation is accelerating adoption of chemical recycling technologies across packaging automotive and consumer goods sectors.

-

Governments worldwide are enforcing strict regulations and bans on landfill disposal of plastics promoting circular economy-based recycling systems globally.

-

Rising corporate sustainability commitments and net zero targets are encouraging investment in advanced chemical recycling infrastructure and technologies worldwide.

-

Expanding use of depolymerization technology is enabling high purity monomer recovery improving demand for virgin like recycled plastic materials.

-

Enzymatic recycling innovations are gaining traction for selective polymer breakdown enabling efficient closed loop recycling of PET and polyester waste streams.

-

Increasing R&D investments and partnerships are improving scalability and cost efficiency of chemical recycling processes across global industrial applications.

U.S. Chemical Recycling Market Outlook:

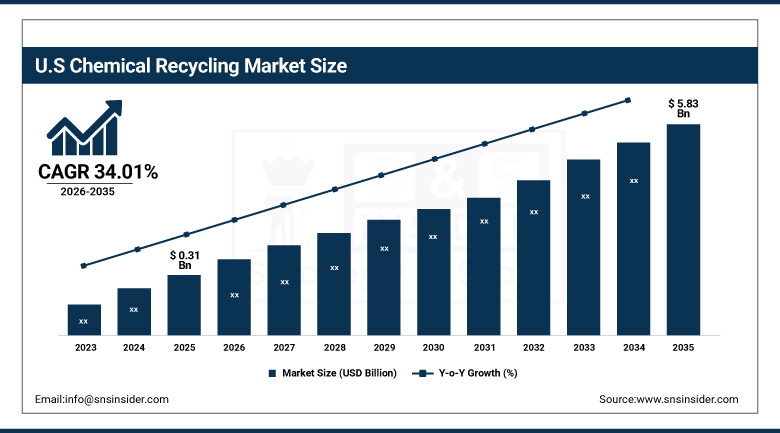

The U.S. Chemical Recycling Market was valued at approximately USD 0.31 billion in 2025 and is expected to reach around USD 5.83 billion by 2035, growing at a CAGR of 34.01% from 2026–2035.

The U.S. chemical recycling market is experiencing steady growth as a result of the rising amount of plastic waste generated and stringent environmental laws. The high rate of adoption of advanced chemical recycling technologies in the petrochemical industry is facilitating the growth of the market. High demand for circular economic models in the packaging and automotive industry is also fostering the growth of the market. Increasing investments in the establishment of pyrolysis and depolymerization facilities are also boosting the development of the market.

In accordance with the US EPA Sustainable Materials Management Program and 2025 National Recycling Strategy, about 35.7 million tons of plastic waste is produced annually by the United States. In addition, the rate of mechanical recycling of post-consumer plastics remains under 10%.

According to the Plastics Innovation Challenge by the United States Department of Energy, federally sponsored research projects will lead to up to 50% reduction in the leakage of plastic waste due to chemical recycling technology, which includes methods like depolymerization and pyrolysis. According to lifecycle assessments by the EPA, chemical recycling can also help in attaining up to 70-80% efficiency in feedstock recovery.

Chemical Recycling Market Segment Analysis:

-

By Type, PET (polyethylene terephthalate) dominated the market with 31.74% share in 2025; while polyurethane waste is the fastest growing segment with CAGR of 43.80% during 2026 to 2035.

-

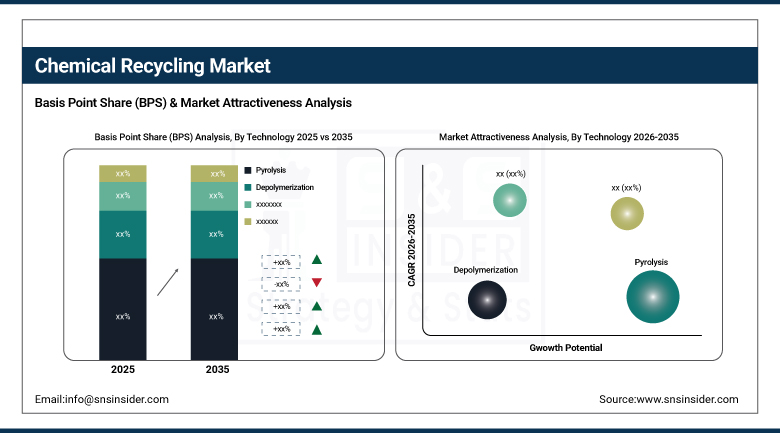

By Technology, pyrolysis dominated the market with 38.10% share in 2025; while depolymerization are the fastest growing segment with CAGR of 44.45% during 2026 to 2035.

-

By End-Use Industry, packaging dominated the market with 44.68% share in 2025; while automotive are the fastest growing segment with CAGR of 41.64% during 2026 to 2035.

By Type, PET (polyethylene terephthalate) dominated the chemical recycling market, while polyurethane waste is the fastest growing segment.

PET (Polyethylene Terephthalate) held the dominated revenue share in the chemical recycling market in 2025, owing to wide-ranging utilization in the production of beverage bottles and food packaging products. The high collection rate along with an efficient recycling channel ensures the large-scale processibility of PET. In addition to that, consistent demand from the packaging industry and textile industry guarantees constant supply of raw material. Also, well-developed depolymerization technologies for PET help to recover the raw material efficiently.

Polyurethane waste segment is expected to grow at the fastest CAGR from 2026 to 2035 due to increasing use in automotive seating, construction insulation, and industrial applications. Growing environmental concerns regarding landfill accumulation of polyurethane materials are driving adoption of advanced recycling solutions. Chemical recycling enables recovery of valuable polyols and raw materials from complex polyurethane waste streams. Rising investment in circular economy initiatives and technological advancements in chemical breakdown processes are further accelerating segment growth globally.

By Technology, pyrolysis dominated the chemical recycling market, while depolymerization are the fastest growing segment.

The Pyrolysis Segment held the dominated revenue share in the chemical recycling market in 2025. It is popular because of its capability to manage plastic wastes that have been contaminated and mixed. This technology converts plastic wastes to fuel and feedstock. Its scalability and suitability to large scale industrial applications ensure high demand. Continued innovations in technology and availability of the infrastructure are also contributing towards making it a dominant segment in the global chemical recycling system.

The Depolymerization Segment is anticipated to witness the fastest CAGR from 2026–2035 because of growing requirement for pure recycled polymers. It converts the plastic waste into the initial monomers. It offers an option for closed loop recycling. The rising demand from the packaging and textiles industry is propelling its adoption. The push for circular economy from the regulators and investments in advanced recycling facilities are aiding its growth.

By End-Use Industry, packaging dominated the chemical recycling market, while automotive are the fastest growing segment.

Packaging sector accounted for the dominated revenue share in the chemical recycling market in 2025 due to huge amount of plastic packaging waste generated in food & beverages and consumer goods sectors. Pressure from the government regarding single-use plastics is resulting in increased adoption of chemical recycling processes. The high demand for recycled feedstocks in packaging application will continue to drive the growth of this sector in the global chemical recycling market.

The Automotive sector is anticipated to be the fastest growing sector at a CAGR from 2026 to 2035 owing to the growing need for sustainable and lightweight materials for vehicles. Manufacturers are focusing on cutting down carbon emissions and enhancing fuel efficiency using recycled polymers. Recycling chemicals allow manufacturers to recover high-quality materials for use in the automobile sector.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025(%) |

|---|---|---|

|

North America |

United States |

78.35% |

|

Europe |

Germany |

28.60% |

|

Asia Pacific |

China |

44.20% |

|

Middle East & Africa |

UAE |

18.40% |

|

Latin America |

Brazil |

47.10% |

North America Chemical Recycling Market Insights.

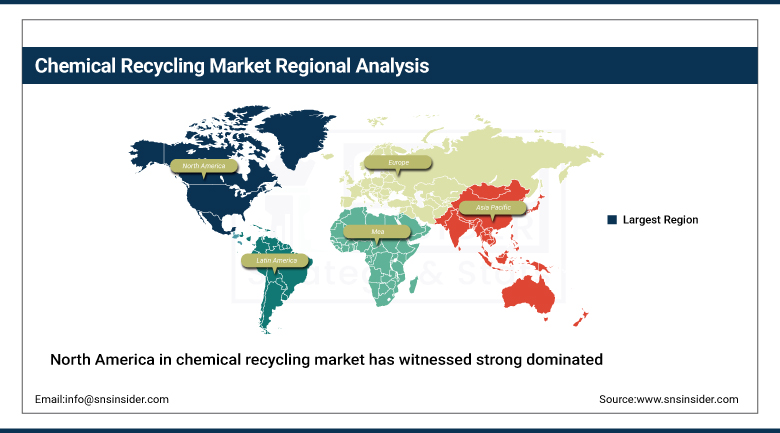

North America in chemical recycling market has witnessed strong dominance with a market share of about 34.25% in 2025 due to advanced petrochemical infrastructure and strong waste management systems. The region benefits from high adoption of circular economy initiatives across packaging, automotive, and industrial sectors. Increasing investments in pyrolysis and depolymerization facilities are driving market expansion. Strong regulatory support for plastic waste reduction is further accelerating growth across the United States and Canada. Continuous innovation in recycling technologies is strengthening regional leadership in chemical recycling market development.

According to the U.S. Environmental Protection Agency & Sustainable Materials Management Program and Environment and Climate Change Canada plastics, North America generated approximately 35 million metric tons of plastic waste annually, with recycling rates remaining below 10% for plastic streams in recent federal waste assessments.

As per OECD Global Plastics Outlook 2025 indicators, chemical recycling technologies in OECD Americas account for a small but growing share of plastic recovery capacity, with pilot and demonstration-scale facilities representing over 60% of operational chemical recycling infrastructure in the region, reflecting early-stage industrial adoption under circular economy policies.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Chemical Recycling Market Insights.

Europe chemical recycling market is characterized by strong growth in 2025 owing to strict environmental regulations and circular economy policies. The major countries contributing include Germany, France, United Kingdom, and Netherlands. Rising demand for sustainable packaging and industrial recycled feedstock is fueling market growth. Increasing adoption of depolymerization and solvolysis technologies is further accelerating market development. Strong focus on reducing landfill dependency is supporting large scale adoption across industries. Regulatory mandates under European sustainability frameworks are driving consistent expansion in chemical recycling infrastructure.

According to the European Environment Agency and Eurostat waste statistics 2025, the European Union generated approximately 225 million tonnes of plastic waste annually, with recycling rates averaging about 32% across member states.

As per the updates in the Circular Economy Action Plan, EU legislation requires that all packaging should be made in such a way that it becomes recyclable economically by 2030, having a target for recycled content of 30% for plastic packaging.

Asia Pacific Chemical Recycling Market Insights.

Asia Pacific is positioned to register the fastest CAGR growth in the chemical recycling market during the forecast period, with an estimated growth rate of 39.24%. Rapid industrialization and rising plastic consumption are driving strong demand across China, India, Japan, South Korea, and Southeast Asia. Expanding packaging and automotive industries are significantly boosting adoption of chemical recycling technologies. Increasing investments in large scale recycling plants and government sustainability initiatives are accelerating regional growth. Strong demand for cost effective waste management solutions supports long term market expansion.

According to UN Environment Program and OECD Global Plastic Outlook 2025, Asia Pacific generates around 51% of global plastic waste, where the recycling rate varies between different economies. While the recycling rate is lower than 10% in some developing nations, it is higher than 30% in advanced nations like Japan and South Korea.

According to World Bank’s plastic waste baseline and national policies of circular economy in China, Japan, and South Korea, chemical recycling is becoming part of the strategy in the plastic waste management pilots of the region, which are now more than 20%.

Middle East & Africa and Latin America Chemical Recycling Market Insights.

The Middle East & Africa along with Latin America regions are experiencing steady growth due to increasing industrialization and rising investments in waste management infrastructure. Key contributing countries include Brazil, Mexico, UAE, Saudi Arabia, and South Africa. Growing demand for sustainable packaging and automotive materials is supporting market expansion. Rising focus on circular economy development is further driving adoption of chemical recycling technologies. Limited but growing infrastructure is creating new opportunities for market players across these emerging regions.

According to the World Bank “Waste Management in the Middle East and North Africa” 2026 report and OECD Global Plastics Outlook, the Middle East & North Africa region recycles less than 10% of municipal solid waste, while more than 66% is mismanaged and the region generates over 155 million tons of waste annually. As per OECD 2025 plastics indicators, Latin America achieves an estimated plastics recycling rate of around 12%, while up to 56% of waste in comparable developing economies remains improperly managed.

Market Dynamics:

Growth Drivers: Rising plastic waste generation and increasing regulatory pressure driving adoption of circular recycling systems globally

With rising plastic consumption in global packaging, automotive, and consumer goods industries, the volume of plastic waste has greatly increased. It is now common for governments around the world to introduce stringent measures with an aim of reducing landfill use. With chemical recycling, plastics that cannot be recycled can be converted to valuable raw material, thus fostering sustainability. There has been more investment in advanced recycling technologies because of the growing corporate commitment to carbon neutrality.

As stated by the United Nations Environment Programme & Global Plastics Outlook 2025, the total annual global generation of plastic waste has come down to around 353 million tons of which only 9% is getting successfully recycled while the rest goes into landfills, is incinerated, or is mishandled. As per the OECD Global Plastics Outlook policy indicators, 175 nations have brought out policies aimed at tackling single-use plastics, and over 60% of member countries of OECD have set up an extended producer responsibility system.

Restraints: Limited feedstock quality consistency and insufficient collection infrastructure restricting efficient recycling output performance

The inconsistency in quality of the plastic waste feedstock, through contamination and the mix of different streams of materials, decreases the efficiency of chemical recycling techniques. The absence of adequate systems of collecting and segregating in some developing areas makes it difficult to access raw material. Inefficiency in yield production and high costs of processing are thus witnessed. There are technological adjustments that need to be developed to overcome these challenges.

Opportunities:Advancements in depolymerization and enzymatic recycling technologies enabling high purity material recovery and new revenue streams

Innovation in modern recycling techniques including depolymerization and enzyme-based methods is bringing about the possibility of obtaining pure monomers. This innovation allows for closed-loop recycling of PET and other polymers to obtain materials that resemble virgin materials. There is an increase in investment in research and development making the process more efficient and scalable. The growing need for sustainable materials by the packaging and textile industry is encouraging the commercial application of this technology.

As per the European Environment Agency & circular economy monitoring framework, over 60% of EU plastic waste is still directed to energy recovery or disposal rather than material recovery. OECD policy tracking also shows that enzymatic and depolymerization-based chemical recycling technologies are included in fewer than 15% of active national plastic waste strategies, indicating early-stage adoption despite increasing policy support.

Recent Developments:

-

2026: Loop Industries selected BASF Industriepark Lausitz in Germany for its Infinite Loop Europe facility, advancing 70,000 tpa PET recycling project under licensing model.

-

2025: ExxonMobil paused €100 million European chemical recycling investments in Rotterdam and Antwerp due to evolving EU regulatory framework concerns impacting project viability.

-

2025: Eastman Chemical Company progressed polyester renewal facility operations using methanolysis technology to recycle hard-to-recycle plastic waste streams.

-

2024: Plastic Energy expanded pyrolysis-based chemical recycling facilities in Spain producing TACOIL feedstock for new plastic manufacturing

Chemical Recycling Market Key Players are:

-

Loop Industries

-

Agilyx

-

Plastic Energy

-

Brightmark

-

Carbios

-

PureCycle Technologies

-

Mura Technology

-

Licella Holdings

-

Eastman Chemical Company

-

BASF SE

-

Dow Inc.

-

ExxonMobil

-

Shell plc

-

TotalEnergies SE

-

LyondellBasell Industries

-

Indorama Ventures

-

Covestro AG

-

OMV AG

-

Neste Oyj

-

Veolia Environnement

Chemical Recycling Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 1.16 Billion |

| Market Size by 2035 | USD 25.79 Billion |

| CAGR | CAGR of 36.33% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (PET (Polyethylene Terephthalate), PE (Polyethylene), PP (Polypropylene), PS (Polystyrene), PVC (Polyvinyl Chloride), Mixed Plastic Waste, Multilayer Plastics, Polyurethane Waste) • By Technology (Pyrolysis, Gasification, Depolymerization, Solvolysis, Enzymatic Recycling, Catalytic Cracking, Hydrothermal Processing) • By End-Use Industry (Packaging, Automotive, Construction, Textile, Electrical & Electronics, Industrial Manufacturing, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Loop Industries, Agilyx, Plastic Energy, Brightmark, Carbios, PureCycle Technologies, Mura Technology, Licella Holdings, Eastman Chemical Company, BASF SE, Dow Inc., ExxonMobil, Shell plc, TotalEnergies SE, LyondellBasell Industries, Indorama Ventures, Covestro AG, OMV AG, Neste Oyj, Veolia Environnement |

Frequently Asked Questions

The chemical recycling market is expected to grow at a CAGR of 36.33% from 2026 to 2035.

The chemical recycling market was valued at approximately USD 1.16 billion in 2025.

The major growth factors include rising plastic waste, strict regulations, circular economy adoption, sustainable packaging demand, and advancements in pyrolysis, depolymerization, and enzymatic recycling improving recovery efficiency and scalability.

The pyrolysis segment dominated the market in 2025 due to processing mixed plastics efficiently and producing valuable fuel and feedstock.

North America dominated the chemical recycling market in 2025 due to strong petrochemical infrastructure, circular economy investment, and advanced recycling systems.

Get in Touch