Clinical Nutrition Market Report Scope & Overview:

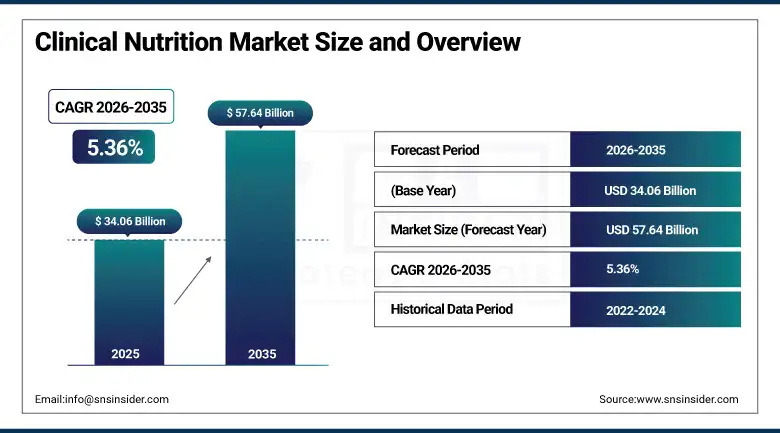

The Clinical Nutrition Market was valued at USD 34.06 Billion in 2025 and is expected to reach USD 57.64 Billion by 2035, growing at a CAGR of 5.36% from 2026–2035.

The global clinical nutrition market is experiencing robust growth driven by the rising prevalence of chronic diseases, increasing hospitalization rates among the ageing population, and growing awareness of nutritional therapy’s role in clinical outcome improvement. Clinical nutrition encompasses medically formulated products designed to supplement or replace normal food intake in patients who cannot meet their nutritional needs through conventional diet alone, spanning enteral formulas delivered via feeding tube, parenteral nutrition administered intravenously, oral nutritional supplements, and infant nutrition products for premature and medically compromised neonates. Market growth is driven by the ageing global population’s increased malnutrition risk, growing cancer patient population, and the healthcare system’s evidence-based recognition that nutritional intervention reduces complication rates.

In 2024, Abbott Nutrition launched its Ensure Plant-Based Protein nutritional supplement with 20 grams of plant-derived protein per serving, targeting the growing patient population seeking plant-based clinical nutrition alternatives to conventional dairy-derived protein oral nutritional supplements. The product launch reflects the clinical nutrition market’s adaptation to patient dietary preference diversity whose vegan and plant-based positioning creates premium specification opportunity in the oral supplementation segment.

Clinical Nutrition Market Size and Forecast

-

Market Size in 2026E: USD 35.89 Billion

-

Market Size by 2035: USD 57.64 Billion

-

CAGR: 5.36% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Clinical Nutrition Market - Request Free Sample Report

Clinical Nutrition Market Trends

-

Home enteral nutrition adoption is increasing as post-discharge nutritional support shifts from hospitals to homecare settings globally.

-

Disease-specific nutrition formulas are expanding for cancer, sarcopenia, and organ-related conditions, supporting improved patient outcomes.

-

Prebiotic and probiotic integration in clinical nutrition products is enhancing gut health, immunity, and post-operative recovery support.

AI-powered nutrition assessment tools are enabling personalized nutritional prescriptions based on individual patient requirements and health conditions.

-

Sustainable and clean-label clinical nutrition products are gaining demand due to environmentally conscious healthcare procurement policies.

The U.S. Clinical Nutrition Market Outlook

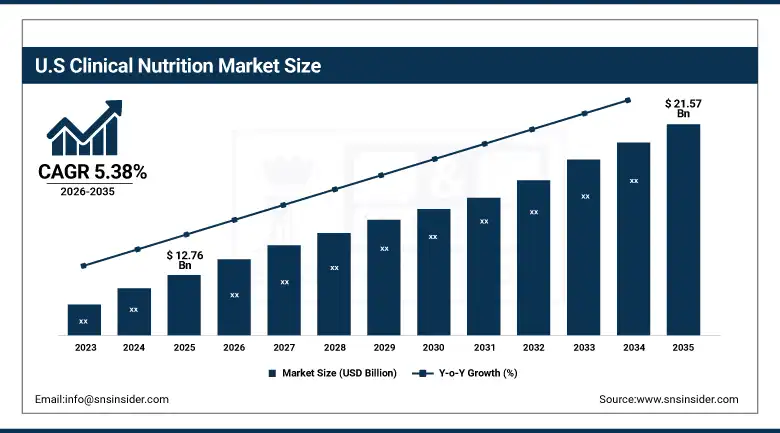

The U.S. Clinical Nutrition Market was valued at approximately USD 12.76 Billion in 2025 and is expected to reach approximately USD 21.57 Billion by 2035, growing at a CAGR of approximately 5.38%.

The U.S. is the most commercially sophisticated clinical nutrition market within North America’s dominant revenue position. Abbott Nutrition, Nestlé Health Science, Fresenius Kabi, Baxter International, and B. Braun Melsungen collectively define the domestic clinical nutrition commercial landscape. CMS reimbursement for enteral and parenteral nutrition under Medicare Part B creates structured government-funded procurement that sustains above-average institutional clinical nutrition investment. The growing cancer patient population’s oncology nutrition support requirement, the ICU’s nutritional intervention protocol adoption, and the ageing population’s malnutrition risk collectively sustain above-average U.S. clinical nutrition market engagement.

In 2025, Nestle Health Science launched its Impact Oral Supplement formula update with enhanced immunonutrition components including arginine, omega-3 fatty acids, and RNA nucleotides targeting pre- and post-operative surgical patient nutrition support whose clinical evidence for complication rate reduction creates structured hospital formulary procurement motivation.

Clinical Nutrition Market Segment Analysis

-

By Product Type, the oral clinical nutrition products segment dominated the market with approximately 38% share in 2025, while the enteral feeding formulas segment is the fastest growing.

-

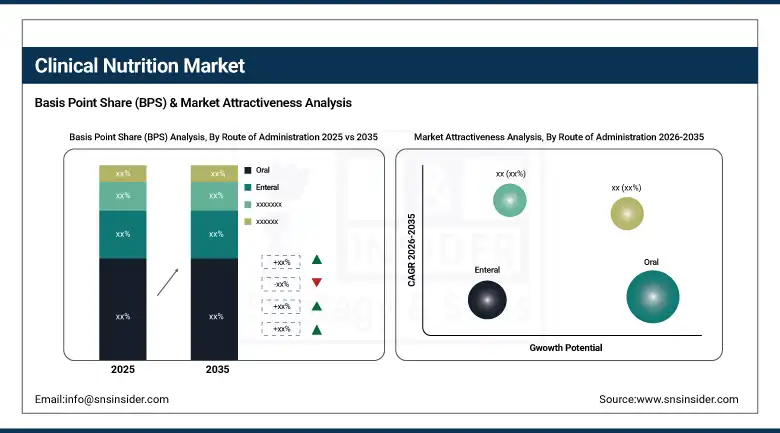

By Route of Administration, the oral route dominated the market with approximately 52% share in 2025, while the enteral route is the fastest growing.

-

By Application, the malnutrition/nutritional deficiency segment dominated the market with approximately 34% share in 2025, while the cancer care segment is the fastest growing.

-

By Distribution Channel, hospital pharmacies dominated the market with approximately 44% share in 2025, while the online pharmacies segment is the fastest growing.

By Route, oral dominates, enteral grows fastest

Oral route retained the dominant administration position with approximately 52% of the market in 2025. The oral supplement’s patient acceptance advantage, compliance benefit relative to tube feeding, and accessibility across both institutional and community settings create the broadest clinical nutrition application footprint. Each hospital malnutrition protocol that initiates oral nutritional supplementation before tube feeding creates oral route procurement whose aggregate across hospital admission volume sustains the route’s dominant commercial position. The community dietitian’s prescribing of oral supplements for malnourished elderly, cancer, and chronic disease outpatients creates retail pharmacy and online channel oral supplement procurement that compounds with hospital-initiated supplementation.

Enteral route is the fastest-growing because dysphagia’s progressive prevalence with advancing age and neurological disorder incidence growth creates structured tube feeding procurement that compounds with the ageing population’s nursing home and homecare residential growth. Each stroke patient, Parkinson’s disease patient, and head and neck cancer patient whose swallowing impairment creates tube feeding dependence creates long-duration enteral formula procurement whose recurring weekly supply creates above-average commercial lifetime value per patient.

By Application, malnutrition dominates, cancer care grows fastest

Malnutrition and nutritional deficiency retained the dominant application position with approximately 34% of the market in 2025. Hospital malnutrition’s documented 20-50% prevalence among acute care inpatients across major healthcare systems creates the most commercially concentrated institutional clinical nutrition procurement motivation. Each hospitalized patient whose nutritional screening identifies malnutrition risk creates clinical nutrition product prescription whose aggregate across hospital admissions creates consistent enteral and oral supplement procurement. The healthcare system’s growing recognition that nutritional intervention reduces complication rates, antibiotic use, and length of stay creates institutional investment motivation that sustains malnutrition’s dominant application position.

Cancer care is the fastest-growing application because the growing global cancer incidence, cancer cachexia’s 80% prevalence in advanced cancer patients whose muscle wasting creates treatment interruption and mortality risk, and the oncology nutrition support programme’s clinical outcome improvement evidence create structured growing procurement. Each new oncology nutrition support protocol that specifies cancer-specific clinical nutrition formula creates above-standard oral supplement procurement whose immunonutrition and omega-3 enriched formulations create premium pricing justification above commodity nutrition supplement alternatives.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Clinical Nutrition Market Insights

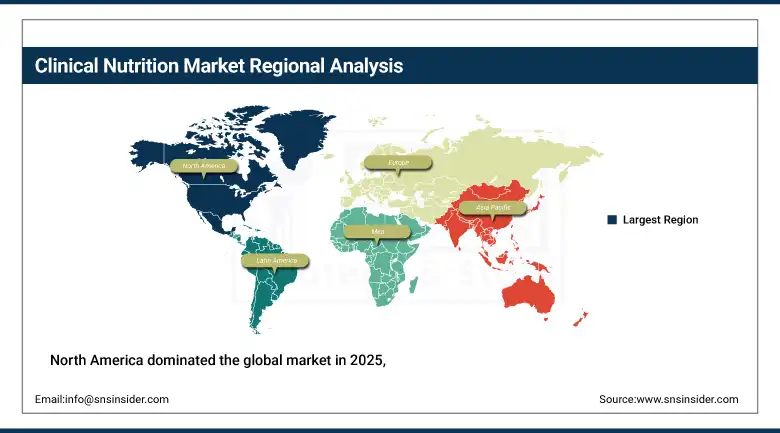

North America dominated the global market in 2025, driven by the most advanced clinical nutrition protocol implementation, CMS reimbursement for enteral and parenteral nutrition, and the commercial presence of Abbott Nutrition, Nestlé Health Science, Fresenius Kabi, and Baxter. The United States accounts for approximately 87.4% of North American revenues through its large hospital sector’s institutional procurement and the growing homecare nutrition market.

Canada contributes approximately 12.6% of North American revenues through its provincial healthcare system’s clinical nutrition reimbursement, the hospital sector’s malnutrition screening protocol, and the growing oncology nutrition support investment.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Clinical Nutrition Market Insights

Europe is a sophisticated clinical nutrition market where ESPEN clinical nutrition guidelines create evidence-based protocol standardization, Fresenius Kabi’s German headquarters and Nestlé Health Science’s Swiss base create supply leadership, and national health system reimbursement creates structured procurement. Germany accounts for approximately 22.3% of European revenues through Fresenius Kabi’s domestic operations, the hospital sector’s nutritional support protocol, and the ageing population’s community nutrition supplement demand.

The United Kingdom, France, and the Netherlands are significant secondary markets where NHS dietitian referral prescribing, national healthcare reimbursement, and ESPEN guideline adoption create consistent clinical nutrition procurement.

Asia Pacific Clinical Nutrition Market Insights

Asia Pacific is the fastest-growing regional market, driven by China’s growing hospital clinical nutrition programme, India’s expanding healthcare infrastructure creating first-time enteral nutrition adoption, Japan’s ageing population’s homecare nutrition demand, and South Korea’s oncology nutrition support investment. China accounts for approximately 44.8% of Asia Pacific revenues through its large hospital sector’s growing nutrition support programme and the domestic pharmaceutical clinical nutrition manufacturer development.

India represents the most commercially dynamic emerging market within Asia Pacific where the growing private hospital network’s clinical nutrition procurement, the expanding cancer treatment infrastructure’s oncology nutrition investment, and the ageing population’s malnutrition awareness create above-average market development.

MEA & Latin America Clinical Nutrition Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through its advanced hospital sector’s clinical nutrition formulary investment, the oncology center’s cancer nutrition support programme, and Vision 2030’s healthcare quality improvement creating above-average institutional clinical nutrition procurement. Brazil leads Latin American revenues at approximately 44.2% through its large hospital network’s clinical nutrition investment, the oncology treatment infrastructure’s nutritional support, and the growing homecare nutrition market. UAE’s premium hospital sector and South Africa’s growing oncology nutrition programme collectively sustain regional market development through 2035.

Market Dynamics

Growth Drivers: Ageing population malnutrition risk and cancer patient nutrition support creating structured procurement

The ageing global population’s accelerating malnutrition risk is the clinical nutrition market’s most commercially certain structural growth driver. Each demographic cohort entering the above-65 age group creates above-average clinical nutrition procurement motivation from the documented 20-30% malnutrition prevalence among older hospitalized patients and the 15-20% prevalence among community-dwelling elderly. Hospital malnutrition screening protocol adoption by ESPEN, ASPEN, and national clinical dietetics guidelines creates systematic institutional clinical nutrition prescription whose adherence creates consistent product procurement from identified at-risk patient populations.

The growing global cancer patient population’s oncology nutrition support requirement creates above-average clinical nutrition procurement from cancer center formulary investment, chemotherapy-associated nutritional support prescribing, and cancer cachexia management’s disease-specific formula specification. Each new oncology center establishment and each cancer incidence increase creates structured clinical nutrition procurement whose aggregate compounds with global cancer prevalence growth.

Restraints: High cost of specialty clinical nutrition products and reimbursement variability

Specialty clinical nutrition products’ above-commodity cost creates procurement barriers in healthcare systems whose formulary management prioritizes cost-effective standard supplement alternatives over premium disease-specific formulations. Each health system whose formulary committee evaluates premium immunonutrition or oncology-specific formula specification requires clinical outcome evidence demonstrating cost-effectiveness that sustains above-standard product pricing.

Reimbursement policy variability across national healthcare systems creates market access complexity whose formulary inclusion requirement and reimbursement negotiation timelines moderate the pace of new clinical nutrition product commercial adoption across diverse national market regulatory environments.

Opportunities: Homecare nutrition expansion and oncology-specific formula development

Homecare enteral nutrition programme expansion represents the most commercially dynamic near-term market development whose transition from hospital-based to home-based tube feeding administration creates growing homecare channel clinical nutrition procurement. Each patient whose hospital discharge with ongoing tube feeding requirement creates homecare enteral formula subscription procurement whose recurring supply model sustains above-transactional commercial relationships.

Oncology-specific clinical nutrition formula development represents the most commercially premium product innovation opportunity whose cancer cachexia management evidence and immunonutrition clinical outcome data create formulary inclusion justification that sustains premium pricing above standard oral supplement alternatives in hospital oncology formulary procurement.

Recent Developments:

-

2026: Danone Nutricia expanded its Advanced Medical Nutrition platform with specialized oral and enteral nutrition solutions focused on oncology, frailty, and malnutrition management, supporting personalized clinical nutrition interventions.

-

2025: Nestle Health Science expanded its medical nutrition portfolio through new disease-specific nutritional formulations targeting oncology, gastrointestinal disorders, and healthy aging applications, strengthening its clinical nutrition presence across hospital and homecare settings.

-

2025: Abbott Nutrition enhanced its therapeutic nutrition product range with advanced high-protein and condition-specific formulations designed to support recovery, muscle preservation, and nutritional management in chronic disease patients.

-

2025: Kate Farms introduced expanded plant-based medical nutrition offerings with improved organic, allergen-free formulations designed for tube feeding and oral nutritional support in pediatric and adult patient populations.

Clinical Nutrition Market Key Players are:

-

Abbott Laboratories (Abbott Nutrition)

-

Nestlé Health Science SA

-

Fresenius Kabi AG

-

Baxter International Inc.

-

B. Braun Melsungen AG

-

Danone SA (Nutricia)

-

Kate Farms

-

Mead Johnson Nutrition (Reckitt)

-

Hormel Health Labs

-

Ajinomoto Co. Inc.

-

Medtrition Inc

-

Global Health Products Inc.

-

Targeted Medical Pharma Inc.

-

Nutricia Advanced Medical Nutrition

-

ICU Medical Inc.

-

Vitalibis GmbH

-

Perrigo Company plc

-

Biosearch Life (Kerry Group)

-

Nualtra Ltd.

-

Victus, Inc.

Clinical Nutrition Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 34.06 Billion |

| Market Size by 2035 | USD 57.64 Billion |

| CAGR | CAGR of 5.36% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Oral Clinical Nutrition Products, Enteral Feeding Formulas, Parenteral Nutrition Components, Infant Nutrition Products, Total Parenteral Nutrition (TPN) Solutions) • By Route of Administration (Oral, Enteral, Parenteral) • By Application (Malnutrition/Nutritional Deficiency, Cancer Care, Chronic Kidney Diseases, Diabetes Management, Neurological Disorders, Gastrointestinal Disorders, Dysphagia, Others) • By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, Homecare & Specialty Clinics, Institutional Sales) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Abbott Laboratories (Abbott Nutrition), Nestlé Health Science SA, Fresenius Kabi AG, Baxter International Inc., B. Braun Melsungen AG, Danone SA (Nutricia), Kate Farms, Mead Johnson Nutrition (Reckitt), Hormel Health Labs, Ajinomoto Co. Inc., Medtrition Inc., Global Health Products Inc., Targeted Medical Pharma Inc., Nutricia Advanced Medical Nutrition, ICU Medical Inc., Vitalibis GmbH, Perrigo Company plc, Biosearch Life (Kerry Group), Nualtra Ltd., Victus, Inc. |

Frequently Asked Questions

The Clinical Nutrition Market is expected to grow at a CAGR of 5.36% from 2026 to 2035.

The Clinical Nutrition Market was valued at USD 34.06 Billion in 2025.

Ageing global population’s rising malnutrition risk creating systematic hospital screening and clinical nutrition prescription.

Malnutrition/Nutritional Deficiency dominated the market with approximately 34% share in 2025.

North America dominated the Clinical Nutrition Market in 2025.

Get in Touch