In Situ Hybridization Market Report Scope & Overview:

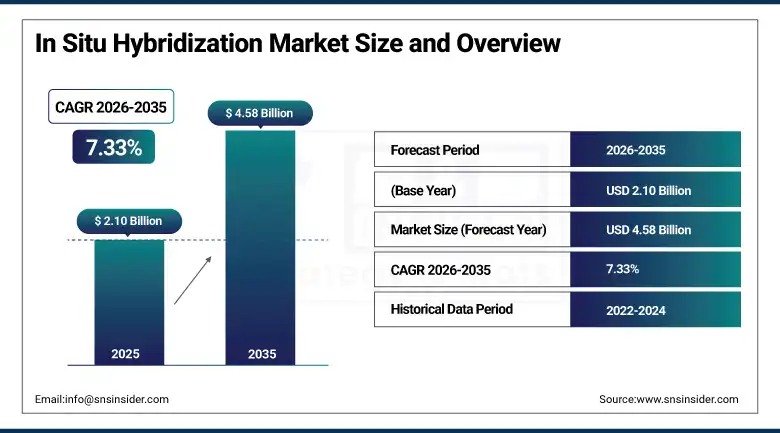

The In Situ Hybridization Market was valued at USD 2.10 Billion in 2025 and is expected to reach USD 4.58 Billion by 2035, growing at a CAGR of 7.33% from 2026–2035.

The global in situ hybridization market is witnessing steady and widespread commercial growth. In situ hybridization is a biological process wherein labelled probes are used for identifying particular sequences in DNA/RNA molecules. Such a technique assists in detecting genetic alterations and also proves to be essential in the diagnosis of different cancers. The rising incidences of cancer and genetic problems have made there be a great need for molecular diagnostics; recent improvements in FISH and CISH have made them more accurate and sensitive. The use of in situ hybridization automated systems as well as artificial intelligence image recognition software is becoming more common.

In 2024, Leica Biosystems launched its BOND-PRIME automated multiplex ISH system with enhanced multi-probe detection capability for simultaneous visualization of up to four RNA targets in a single tissue section. The multiplex ISH capability enables spatial transcriptomics-adjacent applications in pathology tissue sections. The launch reflects the commercial direction of ISH system development toward multiplexing capability whose simultaneous multi-target detection creates new research and companion diagnostic applications.

Market Size and Forecast

-

Market Size in 2026E: USD 2.25 Billion

-

Market Size by 2035: USD 4.58 Billion

-

CAGR: 7.33% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On In Situ Hybridization Market - Request Free Sample Report

In Situ Hybridization Market Trends

-

Multiplex ISH enables simultaneous target detection, expanding spatial gene expression and transcriptomics applications

-

Automated hybridization platforms reduce turnaround time and variability across high-throughput diagnostic laboratories globally

-

RNA-scope and advanced RNA ISH improve RNA localization diagnostics in tumor microenvironment and oncology research

-

Companion diagnostic ISH tests grow with FDA-approved targeted cancer therapies requiring patient selection biomarkers

-

Digital pathology integration enables AI-based ISH image analysis improving accuracy, quantification, and consistency across labs.

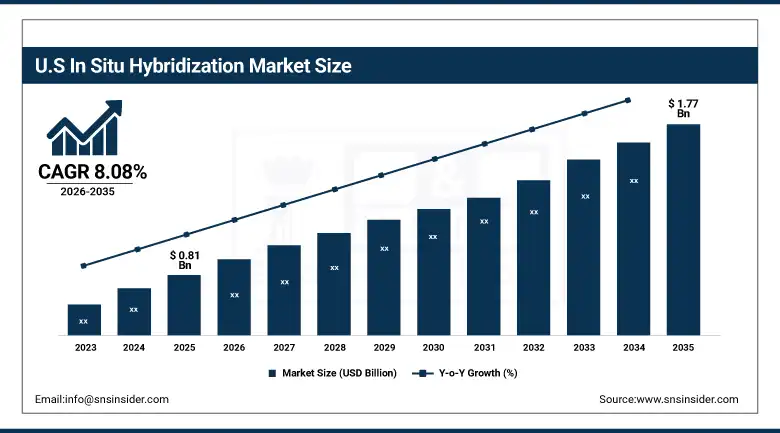

The U.S. In Situ Hybridization Market Outlook

The U.S. In situ hybridization market was valued at approximately USD 0.81 Billion in 2025 and is expected to reach approximately USD 1.77 Billion by 2035, growing at a CAGR of approximately 8.08%.

The U.S. is the most commercially sophisticated ISH market within North America's dominant revenue position. Agilent Technologies, Thermo Fisher Scientific, Abbott Molecular, Leica Biosystems, and Bio-Rad Laboratories' U.S. operations collectively define the commercial ISH landscape. The high incidence of cancer and genetic diseases in the U.S. and Canada creates above-average cytogenetics, oncology, and infectious disease ISH testing demand. FDA companion diagnostic approvals for HER2 FISH testing in breast cancer, ALK FISH testing in lung cancer, and PD-L1 expression by RNAscope create structured clinical ISH procurement whose volumes scale with the corresponding targeted therapy prescription rates.

In 2024, Agilent Technologies enhanced its FISH probe portfolio with a series of validated probes for rare chromosomal abnormalities in hematological malignancies to meet the increasing need for accurate cytogenetic evaluation of lymphoma, leukemia, and myeloma sub-types where the treatment of the disease necessitates identification of chromosomal abnormalities. This is because of the market realization that there is an increasing need for molecular cytogenetic characterization in hematological oncology, which leads to premium ISH probe purchases generating profits above the market rate.

In Situ Hybridization Market Segment Analysis

-

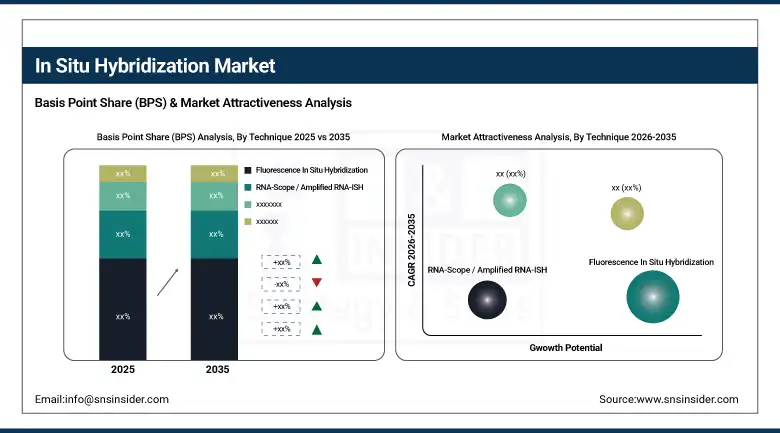

By Technique, the fluorescence in situ hybridization (FISH) segment dominated the market with 54.25% share in 2025, while the chromogenic in situ hybridization (CISH) segment is the fastest growing with a CAGR of 7.71%.

-

By Probe Type, the DNA probes segment dominated the market with 58.41% share in 2025, while the RNA probes segment is the fastest growing.

-

By Application, the cancer diagnostics & research segment dominated the market with approximately 42% share in 2025, while the infectious diseases segment is the fastest growing.

-

By End User, the research institutes & academic centers segment dominated the market with approximately 38% share in 2025, while the hospitals & diagnostic laboratories segment is the fastest growing.

By Technique, FISH dominates, CISH grows fastest

FISH retained the dominant technique position with 54.25% of the market in 2025. FISH's commercial primacy reflects its position as the gold-standard molecular cytogenetic technique whose fluorescence-labelled probe detection of chromosomal copy number changes, structural rearrangements, and gene amplifications creates diagnostic information that conventional karyotyping and immunohistochemistry cannot provide with equivalent sensitivity. Each breast cancer patient requiring HER2 gene amplification assessment before trastuzumab therapy, each lung cancer patient requiring ALK gene rearrangement before crizotinib prescription, and each hematological malignancy patient requiring cytogenetic characterization creates FISH testing procurement that compounds with cancer incidence and targeted therapy prescription growth.

CISH is the fastest-growing technique at 7.71% CAGR because its brightfield microscope compatibility, which eliminates the specialized fluorescence microscopy infrastructure that FISH requires, creates accessibility in resource-constrained pathology laboratories whose standard light microscope infrastructure accommodates CISH without capital equipment investment. Each resource-constrained laboratory in emerging market healthcare systems that adopts CISH instead of FISH for HER2 testing creates procurement that compounds with oncology diagnostic infrastructure expansion in developing countries.

By Application, cancer dominates, infectious diseases grow fastest

Cancer diagnostics and research retained the dominant application position with approximately 42% of the market in 2025. The extraordinary commercial scale of global oncology diagnostic testing, combined with the regulatory requirement for ISH-based companion diagnostics in targeted cancer therapy patient selection, creates the most commercially concentrated and largest aggregate ISH procurement category. Each new targeted cancer therapy approval whose companion diagnostic specifically requires ISH-based gene alteration testing creates a new defined procurement category whose volume scales with the therapy's prescription adoption.

Infectious diseases is the fastest-growing application because ISH's ability to detect viral and bacterial nucleic acid in tissue sections with spatial resolution creates diagnostic and research applications that culture-based and PCR alternatives cannot provide with equivalent histological context. HPV ISH for cervical cancer precursor lesion characterization, CMV ISH for transplant patient surveillance, and SARS-CoV-2 tissue tropism research collectively represent infectious disease ISH applications whose adoption creates procurement growth that compounds with infectious disease diagnostic programme expansion in both clinical and public health settings.

By End User, research institutes dominate, hospitals grow fastest

Research institutes and academic centers retained the dominant end-user position with approximately 38% of the market in 2025. NIH, MRC, DFG, and national research council funding creates the institutional procurement environment whose grant-funded equipment and reagent purchases sustain above-average academic ISH demand across research programme cycles. Each new research publication demonstrating ISH's application in a new biological context creates methodological awareness that sustains research community procurement.

Hospitals and diagnostic laboratories are the fastest-growing end user because the clinical ISH testing volume's expansion driven by companion diagnostic mandates, precision oncology adoption, and the progressive integration of molecular cytogenetics into routine pathology workflow creates above-average procurement growth in clinical settings. The progressive standardization of ISH in clinical pathology guidelines creates systematic adoption across healthcare systems whose combined implementation creates commercial growth that compounds with oncology patient volume increase.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America In Situ Hybridization Market Insights

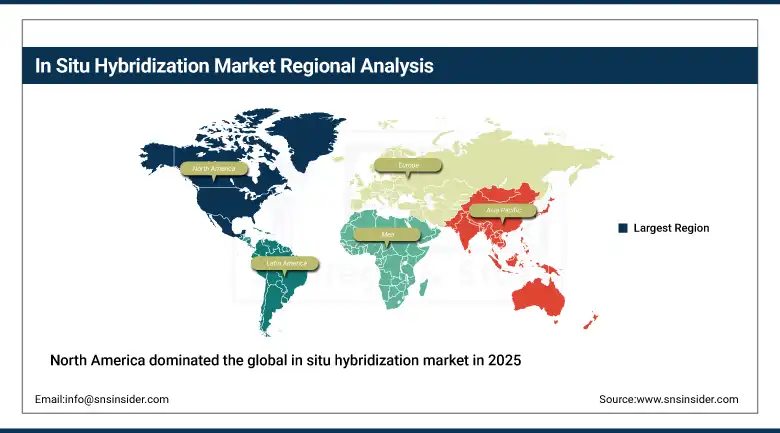

North America dominated the global in situ hybridization market in 2025 as the most commercially advanced molecular diagnostics market. The United States accounts for approximately 87.4% of North American revenues through Agilent Technologies, Abbott Molecular, Leica Biosystems, Thermo Fisher Scientific, and Bio-Rad Laboratories' commercial operations whose combined portfolio defines the ISH technology standard. The high incidence of cancer, FDA companion diagnostic approvals requiring ISH testing, and NIH research funding sustaining academic ISH procurement collectively create the most commercially concentrated ISH demand of any national market.

Canada contributes approximately 12.6% of North American revenues through its cancer centre network's FISH testing infrastructure, university research community's ISH procurement, and the public health system's molecular cytogenetics laboratory investment.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe In Situ Hybridization Market Insights

Europe is a technically sophisticated ISH market where Leica Biosystems' European commercial operations, the EMA's companion diagnostic regulatory framework, and the pharmaceutical industry's clinical trial ISH biomarker assessment create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its advanced pathology laboratory infrastructure, the pharmaceutical industry's ISH biomarker investment, and the research institute network's genomic and developmental biology ISH programme.

The United Kingdom, France, and the Netherlands are significant secondary markets where national cancer research programmes, NHS and equivalent healthcare system pathology laboratory investment, and the European Bioinformatics Institute's genomic research infrastructure create consistent ISH procurement.

Asia Pacific In Situ Hybridization Market Insights

Asia Pacific is the fastest-growing regional ISH market at 8.43% CAGR, driven by growing healthcare investments in China and India, rising incidence of genetic diseases and cancer requiring molecular diagnostics, and government initiatives promoting advanced diagnostic technology adoption. China accounts for approximately 44.8% of Asia Pacific revenues through its expanding hospital molecular pathology laboratory network, the government's precision medicine initiative, and the growing pharmaceutical industry's ISH biomarker research investment.

India's rapidly expanding oncology infrastructure, Japan's advanced pharmaceutical industry's ISH-based companion diagnostic development, and South Korea's sophisticated clinical molecular genetics laboratories create significant secondary markets whose combined procurement reinforces Asia Pacific's fastest-growing regional status.

MEA & Latin America In Situ Hybridization Market Insights

Saudi Arabia leads MEA revenues at approximately 31.2% through its advanced oncology center network, King Faisal Specialist Hospital and Research Centre's molecular pathology investment, and Vision 2030's healthcare infrastructure development creating ISH technology adoption. Brazil leads Latin American revenues at approximately 44.2% through its large cancer center network, university biomedical research community, and the growing pharmaceutical clinical trial sector's ISH biomarker assessment requirement.

UAE's advanced hospital infrastructure and South Africa's academic molecular pathology community create significant MEA secondary markets whose ISH procurement reflects growing molecular diagnostics adoption across both countries' healthcare systems.

Market Dynamics

Growth Drivers: Cancer incidence requiring companion diagnostic ISH testing and technological advancement expanding application breadth

Rising global cancer incidence is the ISH market's most commercially certain structural growth driver. The WHO's projection that cancer incidence will increase 77% by 2050 creates a continuously expanding diagnostic testing volume whose ISH component grows with the progressive adoption of companion diagnostic testing requirements for targeted cancer therapies. Each new FDA approval for a targeted cancer therapy whose companion diagnostic requires ISH-based gene alteration testing creates a new defined procurement category whose commercial scale reflects the approved indication's patient population size.

Technological advancement in ISH sensitivity, multiplexing capability, and automation is simultaneously creating new clinical and research applications that expand the addressable market. Automated multiplex ISH systems' ability to simultaneously detect up to four RNA or DNA targets in a single section creates spatial gene expression profiling capability whose research value creates institutional procurement motivation beyond conventional single-target diagnostic ISH.

Restraints: High cost of FISH-based testing and technical complexity requiring trained personnel

FISH testing's cost, typically USD 150-400 per test in laboratory settings, creates patient access barriers in healthcare systems whose reimbursement frameworks limit specialized molecular testing adoption. The capital investment in fluorescence microscopy, image analysis software, and automated hybridization systems creates additional procurement barriers for smaller pathology laboratories whose patient volumes do not justify the capital cost.

Technical complexity requiring trained laboratory scientists whose ISH probe hybridization, wash protocol management, and signal interpretation expertise creates staffing constraints in resource-limited healthcare environments.

Opportunities: Spatial transcriptomics ISH applications and emerging market clinical laboratory expansion

Spatial transcriptomics ISH represents the most commercially exciting growth frontier whose combined spatial resolution and quantitative RNA expression capability creates research tool demand that conventional ISH and next-generation sequencing individually cannot serve. Each new spatial transcriptomics study that employs multiplex RNAscope or seqFISH to characterize tumor microenvironments, neuronal cell type distributions, or embryonic tissue organisations creates ISH probe and instrument procurement whose compound growth with the spatial transcriptomics field's commercial momentum sustains above-average market segment growth.

Emerging market clinical laboratory expansion in China, India, Southeast Asia, and Latin America represents the most commercially significant volume growth opportunity whose first-time ISH adoption creates net new procurement beyond the established market's replacement and upgrade cycle. Each new oncology hospital or cancer center that establishes FISH testing capability creates structured procurement whose aggregate across the developing world's extraordinary healthcare infrastructure investment compounds with each country's rising cancer diagnostic capacity.

Recent Developments:

-

2026: Spatial transcriptomics integration with ISH accelerated via AI-driven pathology models improving gene expression analysis and molecular tissue mapping accuracy.

-

2025: Roche advanced VENTANA companion diagnostics with AI-powered digital pathology ISH assays enabling improved cancer biomarker detection and patient stratification.

-

2025: Bio-Techne expanded RNAscope ISH probe portfolio to over 70,000 probes, strengthening spatial transcriptomics and high-sensitivity RNA detection capabilities.

In Situ Hybridization Market key players are:

-

Agilent Technologies Inc.

-

Thermo Fisher Scientific Inc.

-

Abbott Molecular Inc.

-

Leica Biosystems Nussloch GmbH

-

F. Hoffmann-La Roche Ltd.

-

Bio-Rad Laboratories Inc.

-

PerkinElmer Inc.

-

Merck KGaA (Sigma-Aldrich)

-

Oxford Gene Technology IP Ltd.

-

Advanced Cell Diagnostics (Bio-Techne)

-

Biocare Medical LLC

-

NeoGenomics Laboratories

-

BioView Ltd.

-

Danaher Corporation

-

Empire Genomics LLC

-

MetaSystems GmbH

-

Applied Spectral Imaging

-

10x Genomics

-

Sysmex Corporation

-

NanoString Technologies

In Situ Hybridization Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.10 Billion |

| Market Size by 2035 | USD 4.58 Billion |

| CAGR | CAGR of 7.33% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Technique (Fluorescence In Situ Hybridization/FISH, Chromogenic In Situ Hybridization/CISH, RNA-Scope/Amplified RNA-ISH, Single Molecule FISH, Others) • By Probe Type (DNA Probes, RNA Probes) • By Application (Cancer Diagnostics & Research, Genetic & Chromosomal Disorders, Infectious Diseases, Neuroscience & Developmental Biology, Others) • By End User (Research Institutes & Academic Centers, Hospitals & Diagnostic Laboratories, Pharmaceutical & Biotechnology Companies, Contract Research Organizations) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Agilent Technologies Inc., Thermo Fisher Scientific Inc., Abbott Molecular Inc., Leica Biosystems Nussloch GmbH, F. Hoffmann-La Roche Ltd., Bio-Rad Laboratories Inc., PerkinElmer Inc., Merck KGaA (Sigma-Aldrich), Oxford Gene Technology IP Ltd., Advanced Cell Diagnostics (Bio-Techne), Biocare Medical LLC, NeoGenomics Laboratories, BioView Ltd., Danaher Corporation, Empire Genomics LLC, MetaSystems GmbH, Applied Spectral Imaging, 10x Genomics, Sysmex Corporation, NanoString Technologies |

Frequently Asked Questions

The In Situ Hybridization Market is expected to grow at a CAGR of 7.33% from 2026 to 2035.

The In Situ Hybridization Market was valued at USD 2.10 Billion in 2025.

Growing prevalence of cancer requiring companion diagnostic ISH testing for targeted therapy patient selection.

FISH dominated the In Situ Hybridization Market with 54.25% share in 2025.

North America dominated the In Situ Hybridization Market in 2025.

Get in Touch