Clinical Risk Grouping Solutions Market Report Scope & Overview:

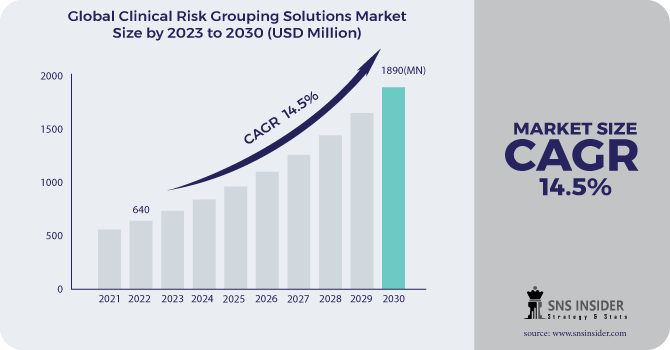

The Clinical Risk Grouping Solutions Market Size was valued at USD 640 million in 2022, and is expected to reach USD 1890 million by 2030, and grow at a CAGR of 14.5% over the forecast period 2023-2030.

The market for clinical risk grouping software is being driven by growing consumer awareness of risk management and the adoption of big data solutions. Significant growth prospects for market players are also presented by the mounting paperwork that causes physician fatigue and the growing emphasis on AI & machine learning.

Get more information on Clinical Risk Grouping Solutions Market Market - Request Sample Report

The Clinical Risk Grouping (CRG) solutions are a well-known method for classifying and grouping people using inpatient and outpatient diagnosis and procedure codes, drug records, demographic information, and functional health status in order to place each person in a particular risk group for future healthcare projections. A software called CRG uses expert clinical logic to divide each patient into a certain risk group. It is a particular mechanism for categorizing people based on data and supported by clinical evidence. It uses a wide range of data, including patient histories, records, administrative data, and other data to identify individuals from different age groups, adults, including children, and elderly people.

CRGs are largely used to assess the prevalence of chronic or congenital diseases, adjust prices and capitations for risk, profile physician practice patterns, profile novel illness patterns and occurrences, and many more purposes. All populations can benefit from CRG's patient-centric approach, which focuses on the overall burden of diseases rather than just one illness. In order to monitor possibly avoidable incidents and predict future healthcare use, they are also employed.

MARKET DYNAMICS

DRIVERS

-

Growth in the Use of Big Data Solutions

-

Benefits of Risk Management Solutions

RESTRAINTS

-

Insufficient infrastructure

-

Privacy Breach in the Private Cloud: Issues

-

Exorbitant Price for Clinical Solutions

OPPORTUNITIES

-

Increasing Doctor Burnout as a Result of Documentation Requirements

-

The importance of AI and machine learning is rising

CHALLENGES

-

Lack of Experienced Healthcare IT Professionals

-

Privacy Issues Associated with Patient Data

IMPACT OF COVID-19

Healthcare organisations are already formulating new strategies to deal with the increasing COVID-19 patient population, from locating speedy diagnostic tools to procuring enough PPE kits for staff.

The financing for chondroitin sulfate-related R&D activities has been cut due to the medical community's shift toward treating COVID-19, and as a result, this sector must deal with neglect, which has a detrimental effect on clinical risks. market for grouping solutions

However, CRGs could be crucial during this COVID-19 pandemic since they would aid healthcare administrators, professionals, and physicians in categorizing individuals into particular categories utilizing patient data.

Governments want to deploy CRGs in COVID-19-related healthcare services to annoy healthcare providers and boost efficiency.

By Product Type

Clinical risk grouping solutions come in three different product categories: scorecard & visualization tools, dashboard analytics, and risk reporting. Due to its capacity to estimate payment processes precisely and project per-patient risk, the scorecard & visualization tools segment commanded the greatest part of the market. During the projected period, the segment's growth is anticipated to be aided by the growing demand to lower healthcare expenses through these two channels.

By Deployment Model

Due to the highest level of security for sensitive data and suitability for highly sensitive clinical risk grouping data, private cloud accounted for the largest proportion of the clinical risk grouping software market in 2018. To prevent any violation of data privacy that can have legal repercussions, this data must be stored securely. Nevertheless, it is anticipated that the public cloud category would develop at the highest CAGR and the fastest rate. Due to the low cost of public cloud systems in comparison to alternative deployment options and the large number of public cloud providers, this market is expanding.

By End User

End-users of clinical risk grouping solutions include hospitals, payers, ambulatory care facilities, long-term care facilities, and others; hospitals held the biggest market share of these solutions. The expansion of this market is being driven by the expanding use of big data solutions in healthcare facilities (such as hospitals and clinics), the increasing attention that caregivers are giving to risk management, and the expanding use of AI and machine learning in the healthcare sector.

KEY MARKET SEGMENTS:

By Product Type

-

Scorecard & Visualization Tools

-

Dashboard Analytics

-

Risk Reporting

By Deployment Model

-

Private Cloud

-

Public Cloud

-

Hybrid Cloud

By End User

-

Hospitals

-

Payers

-

Ambulatory Care Centers

-

Long- Term Care Centers

.png)

Need any customization research on Clinical Risk Grouping Solutions Market Market - Enquiry Now

REGIONAL ANALYSIS

With the greatest market share among the geographical categories, North America is predicted to experience considerable market expansion. The dominance is caused by elements like the rise in the prevalence of chronic diseases worldwide and the increasing adoption of technology in the area, which has led to an increase in demand for novel treatment methods that are driving the market in the United States. The presence of a well-developed infrastructure, the presence of major industry and government initiatives to induce clinical data management solutions in the healthcare settings, the sharp increase in healthcare spending and high pressure to achieve better health outcomes at lower costs, as well as the availability of these factors will all contribute to the market's growth in the near future.

REGIONAL COVERAGE:

-

North America

-

USA

-

Canada

-

Mexico

-

-

Europe

-

Germany

-

UK

-

France

-

Italy

-

Spain

-

The Netherlands

-

Rest of Europe

-

-

Asia-Pacific

-

Japan

-

south Korea

-

China

-

India

-

Australia

-

Rest of Asia-Pacific

-

-

The Middle East & Africa

-

Israel

-

UAE

-

South Africa

-

Rest of Middle East & Africa

-

-

Latin America

-

Brazil

-

Argentina

-

Rest of Latin America

-

KEY PLAYERS:

Some of the major key players of Clinical Risk Grouping Solutions Market are as follows: 3M Corporation, Dynamic Healthcare Systems, Cerner Corporation, Optum Inc., Conduent Inc., Health Catalyst, Johns Hopkins University, Nuance Communications, HBI Solutions, PeraHealth, Lightbeam Health Solutions and Other Players.

Dynamic Healthcare Systems-Company Financial Analysis

| Report Attributes | Details |

|---|---|

| Market Size in 2022 | US$ 640 Million |

| Market Size by 2030 | US$ 1890 Million |

| CAGR | CAGR of 14.5% From 2023 to 2030 |

| Base Year | 2022 |

| Forecast Period | 2023-2030 |

| Historical Data | 2020-2021 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Scorecard & Visualization Tools, Dashboard Analytics, Risk Reporting) • By Deployment Model (Private Cloud, Public Cloud, Hybrid Cloud) • By End User (Hospitals, Payers, Ambulatory Care Centers, Long- Term Care Centers) |

| Regional Analysis/Coverage | North America (USA, Canada, Mexico), Europe (Germany, UK, France, Italy, Spain, Netherlands, Rest of Europe), Asia-Pacific (Japan, South Korea, China, India, Australia, Rest of Asia-Pacific), The Middle East & Africa (Israel, UAE, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | 3M Corporation, Dynamic Healthcare Systems, Cerner Corporation, Optum Inc., Conduent Inc., Health Catalyst, Johns Hopkins University, Nuance Communications, HBI Solutions, PeraHealth, Lightbeam Health Solutions. |

| DRIVERS | • Growth in the Use of Big Data Solutions • Benefits of Risk Management Solutions |

| RESTRAINTS | • Insufficient infrastructure • Privacy Breach in the Private Cloud: Issues • Exorbitant Price for Clinical Solutions |

Frequently Asked Questions

Due to its capacity to estimate payment processes precisely and project per-patient risk, the scorecard & visualization tools segment commanded the greatest part of the market.

With the greatest market share among the geographical categories, North America is predicted to experience considerable market expansion.

Clinical Risk Grouping Solutions Market is divided into three segments By Product Type, By Deployment Model, and By End User

Insufficient infrastructure, Exorbitant Price for Clinical Solutions are the restraints of Clinical Risk Grouping Solutions Market.

Ans: The Clinical Risk Grouping Solutions market size was valued at US$ 640Mn in 2022.

Get in Touch