Cloud Service Brokerage Market Report Scope & Overview:

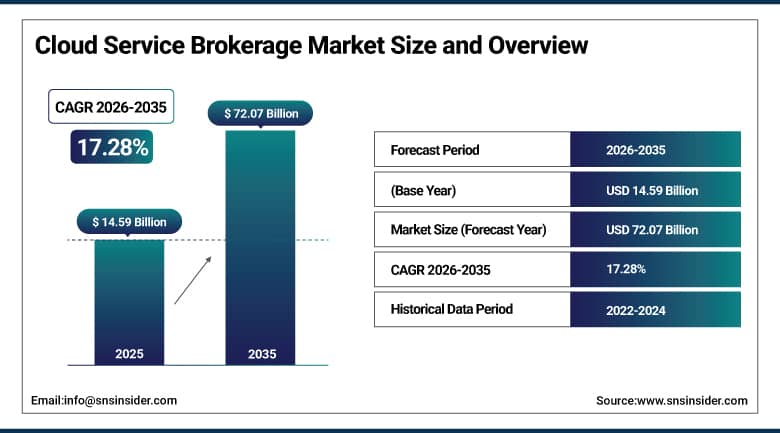

The Cloud Service Brokerage Market size was USD 14.59 Billion in 2025 and is expected to reach USD 72.07 Billion by 2035, growing at a CAGR of 17.28% from 2026–2035.

The field of Cloud Service Brokerage is developing very fast as organizations require efficient solutions for managing their clouds. Factors contributing to market development include greater cloud infrastructures investments, cost-reduction solutions, and the demand for automatic service provision. The matters of compliance and security continue to be among the most important factors influencing the demand for governance policies. Automation and artificial intelligence integration make service orchestration simpler, and improved migration technologies increase the speed of deployment. As enterprises are paying more attention to scalability and flexibility, CSB solutions become more relevant.

Cloud Service Brokerage Market Size and Forecast

-

Market Size in 2026E: USD 17.11 Billion

-

Market Size by 2035: USD 72.07 Billion

-

CAGR: 17.28% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Cloud Service Brokerage Market - Request Free Sample Report

Cloud Service Brokerage Market Trends

-

AI-powered cloud management platforms are enabling predictive cost optimization and automated resource right-sizing.

-

Hybrid cloud brokerage is gaining adoption as enterprises balance public cloud scalability with on-premise security.

-

FinOps disciplines are creating new demand for brokerage platforms with real-time cost visibility and governance tools.

-

Security and compliance brokerage capabilities are becoming table-stakes as regulatory scrutiny of cloud data intensifies.

-

Multi-cloud data sovereignty tools are expanding brokerage demand in markets with strict data residency requirements.

-

SME adoption of external cloud brokerage services is accelerating as managed service models lower IT complexity barriers.

The U.S. Cloud Service Brokerage Market Outlook

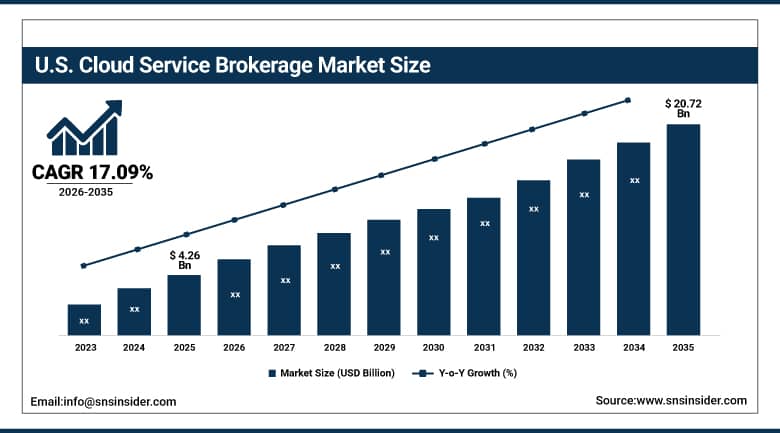

The U.S. Cloud Service Brokerage Market was valued at approximately USD 4.26 Billion in 2025. It is expected to reach approximately USD 20.72 Billion by 2035, growing at a CAGR of approximately 17.09%.

Expansion of the market in the U.S. is driven by increased adoption of multi-cloud approach among businesses due to their desire for reduced costs, scalability, and easy service integration. Investments in cloud infrastructure and the need for automated cloud management drive market growth. The challenges of strict compliance to regulations and cybersecurity concerns push businesses towards CSB solutions focused on governance. Combination of AI automation along with better migration and deployment capabilities will further support market expansion. Leading players in the space such as AWS, IBM, Accenture, and Flexera, who are based in the U.S., consistently maintain market dominance.

At VMware Explore 2024 Barcelona, Broadcom introduced expanded VMware Cloud Foundation services, enhancing AI-driven applications, cybersecurity, and sovereign cloud adoption. New features include Tanzu Data Services for better data management and VMware Live Recovery for cyber resilience.

Cloud Service Brokerage Market Segment Analysis

-

By Platform, the Internal Brokerage Enablement segment dominated the cloud service brokerage market with approximately 55% share in 2025. The External Brokerage Enablement segment is expected to grow fastest, at a CAGR of 18.16% through the forecast period.

-

By Enterprise Size, the Large Enterprises segment dominated the cloud service brokerage market with approximately 69% share in 2025. The SMEs segment is expected to grow fastest, at a CAGR of 18.93% through the forecast period.

-

By End-use, the IT and Telecom segment dominated the cloud service brokerage market with approximately 28% share in 2025. The Energy and Utilities segment is expected to grow fastest, at a CAGR of 22.38% through the forecast period.

-

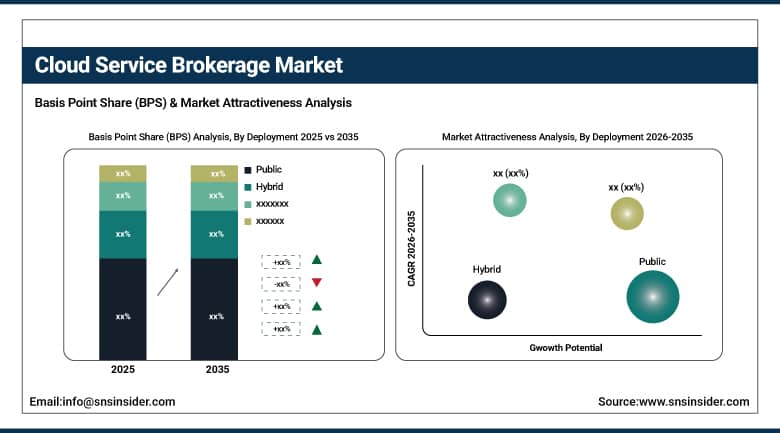

By Deployment, the Public Cloud segment dominated the cloud service brokerage market with approximately 48% share in 2025. The Hybrid Cloud segment is expected to grow fastest, at a CAGR of 19.39% through the forecast period.

-

By Service, the Integration and Support segment dominated the cloud service brokerage market with approximately 24% share in 2025. The Security and Compliance segment is expected to grow fastest, at a CAGR of 19.06% through the forecast period.

By Deployment, Public dominates, Hybrid grows fastest

the Public Cloud segment dominated the Cloud Service Brokerage Market, accounting for approximately 48% of the revenue share in 2025. The segment's leadership is driven by the widespread adoption of public cloud platforms due to their cost efficiency, scalability, rapid deployment capabilities, and lower infrastructure maintenance requirements. Enterprises increasingly rely on public cloud brokerage solutions to simplify multi-cloud management, optimize cloud spending, and streamline service integration while supporting digital transformation initiatives.

The Hybrid Cloud segment is projected to register the fastest CAGR of 19.39% during the forecast period. Growth is fueled by rising enterprise demand for flexible cloud architectures that combine the scalability of public clouds with the security and compliance advantages of private cloud environments. Organizations across regulated industries are increasingly adopting hybrid cloud brokerage solutions to manage complex workloads, ensure data sovereignty, improve operational resilience, and enable seamless workload portability across diverse cloud infrastructures.

By Platform, internal brokerage dominates, external grows fastest

The Internal Brokerage Enablement segment will be dominant in the year 2025 and would account for a revenue share of approximately 55%. The reason behind the rise in adoption of the internal broker enablement strategy is that firms want to manage the cloud resources internally to ensure better control, security, and compliance of the cloud resources. Firms use internal broker solutions to make things easy, get more out of cloud spending and manage hybrid and multi-cloud without involving any other party. Larger firms, particularly in the fields where compliance is required like finance and healthcare, use internal broker enablement to manage the clouds in an effective manner without losing data sovereignty and efficiency.

The External Brokerage Enablement segment is forecasted to witness the fastest growth in terms of CAGR of 18.16%. This is because firms adopt external broker solutions in order to reduce complexities of IT, save cost, and gain multi-cloud expertise. The small-medium enterprises particularly benefit from the external brokerage service providers as they offer managed services, automated provisioning and vendor agnostic cloud management capabilities.

By Enterprise Size, large enterprises dominate, SMEs grow fastest

The Large Enterprises Segment was on top in 2025 as it accounted for almost 69% of the revenue. The reason behind this can be attributed to their complex IT infrastructure, multi-cloud usage, and the requirement for efficient cloud governance and cost optimization. Security, compliance, and optimal multi-cloud provider integration are valued by large enterprises which require the services of brokers for cloud optimization. These organizations spend heavily in custom-built brokerage solutions for the optimization of processes and compliance with stringent regulatory requirements.

Small and Medium Enterprises will witness the highest growth CAGR of 18.93% during the forecast period owing to increased adoption of cloud solutions and cost-effective IT management solutions. Third-party cloud brokerage services are used by Small and Medium Enterprises to reduce complexity, reduce cloud costs, and leverage multi-cloud capabilities without investing in a huge IT workforce. Increasing demands of managed services and cloud integration are forcing these organizations to adopt brokerage solutions in order to scale up.

By End-use, IT & Telecom dominates, Energy & Utilities grows fastest

IT and Telecom was dominant in 2025, accounting for about 28% of the total revenue in the market. This trend is driven by the high reliance of the industry on cloud infrastructures, extensive use of multiple clouds and orchestration of services. The IT and telecommunication companies need cloud brokering capabilities to help them in orchestrating hybrid cloud environment, optimizing network, and utilizing scalability. The growing demand for 5G networks, edge computing and data-based application solutions has also increased the requirement for cloud brokering services. BFSI and Healthcare sectors also make a significant contribution towards end-user demands.

The Energy and Utilities sector is predicted to have the highest growth rate or CAGR of 22.38%. The increasing adoption of smart grid systems, IoT based energy management and predictive analysis makes the necessity of cloud service brokering essential for easier integration and optimization of costs. Cloud brokering can facilitate real-time monitoring, efficient operation, and security due to increasing investments in renewable energy sources.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

82.5% |

|

Europe |

Germany |

24.6% |

|

Asia Pacific |

China |

40.6% |

|

Middle East & Africa |

UAE |

22.8% |

|

Latin America |

Brazil |

43.8% |

North America Cloud Service Brokerage Market Insights

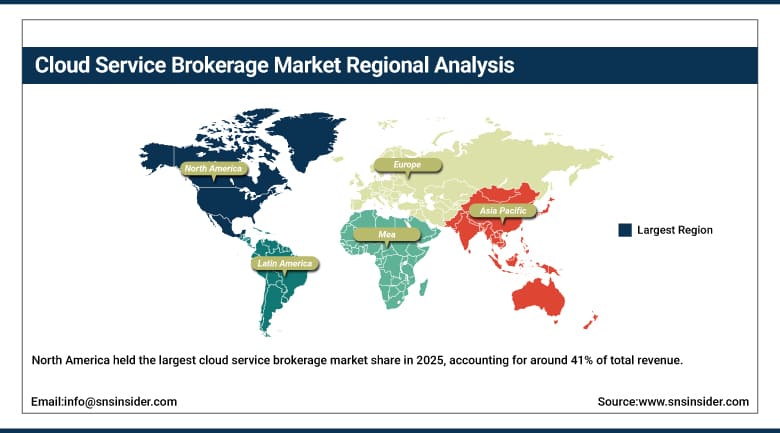

North America held the largest cloud service brokerage market share in 2025, accounting for around 41% of total revenue. The reason behind this includes widespread adoption of cloud in the region, availability of major cloud service providers in the region, and advanced IT infrastructure in the region. Enterprises from different sectors leverage cloud brokerage services to manage their multi-cloud environment, enhance security, and reduce costs. Additionally, increasing need for digital transformation and strict compliance with regulations have increased the market growth. Increasing investment in artificial intelligence (AI)-based cloud services and hybrid cloud services has also contributed to the market leadership of this region.

In North America, the US holds the major share of around 82.5%. Strong enterprise digital transformation investments and availability of major brokerage platform vendors continue to drive the domestic demand in the region.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Cloud Service Brokerage Market Insights

Europe presents an important market for the Cloud Service Brokerage, which is driven by investments in digital transformation and stringent data sovereignty laws. Germany holds the leading position in this market region, thanks to the development of industrial IT and financial clouds. The demands of France and the United Kingdom also help this market, thanks to their enterprise clouds and regulations.

The contribution of Germany to the revenue of Europe makes up approximately 24.6%. The requirements for GDPR compliance continue to make companies turn towards managed multi-cloud solutions, which can be provided by CSBs.

Asia Pacific Cloud Service Brokerage Market Insights

The Asia Pacific region is projected to grow at a CAGR of 19.65% between 2026–2035. Rapid cloud adoption rates, development of digital economy, and increase in demand for cost-effective IT solutions propel the market’s growth. Enterprises are moving towards multi-cloud solutions, leading to an increase in demand for brokerage services, as these services enable better cloud management and security solutions. Favorable government policies towards cloud infrastructures, investments in AI and automation, and increased cloud adoption by SMEs will further boost market growth.

China represents about 40.6% share of the Asia Pacific revenue. The region’s cloud adoption rates are being supported by Alibaba Cloud, Tencent Cloud, and governmental cloud initiatives. As digital transformation continues to progress in the region, the trend is expected to continue in the future.

MEA & Latin America Cloud Service Brokerage Market Insights

The UAE dominates MEA revenues with around 22.8% share. Digitization of enterprises and increasing cloud expenditure contribute to that. Vision 2030 digital transformation programs in Saudi Arabia help the country build infrastructure for cloud and digital economy growth.

Brazil is a market leader of Latin American revenue with around 43.8%. Increasing digitalization of enterprises and growing cloud adoption boost regional demand. Demand comes secondarily from Mexico and Argentina due to their enterprise technology market development.

Market Dynamics

Growth Drivers: Growing need for CSB solutions to manage multi-cloud complexity

The broad usage of multi-cloud has resulted in the emergence of major difficulties in managing diverse cloud environments. Different cloud providers are used by businesses to gain flexibility, performance, and reduce costs; however, such approaches result in integration difficulties, load balancing difficulties, and governance issues. Cloud Service Brokerage tools solve these issues offering such features as centralization, automation, and optimization. Companies seek for brokerage services to automate their processes, reduce costs, and reach maximum ROI.

As companies' cloud systems become more complex, there is a growing need for brokerage solutions to integrate cloud assets, provide visibility, and make better decisions. Transition to working from home and cloud-native development is an additional driver of the importance of CSB platforms. With the continuous digital transformation, this driver will stay relevant during the forecast period.

Restraints: Security risks and compliance challenges limiting adoption

Organizations processing highly confidential information are facing significant difficulties in using cloud service brokerage firms as third parties. Breach of data, misuse, and cyberattacks create doubts about using cloud service brokers as the key service provider for performing core organizational functions. Compliance issues raised by regulatory guidelines are stringent, and organizations have to ensure data protection in multiple cloud environments.

In case of a brokered system, it is difficult to ensure visibility and control of security policies. Not complying with regulations may lead to legal issues, fines, and reputation losses. Organizations working with very confidential data in health care and finance sectors are particularly cautious while using brokerage services.

Opportunities: AI and automation transforming cloud brokerage with intelligent management

Integration of AI and Automation has changed cloud service brokering in the aspect of efficient operation and effective decision-making processes. AI-supported services provide real-time monitoring, analysis, and automatic resource allocation; thus, making multi-cloud management less complicated. Self-service capabilities of enterprises make provisioning, scaling, and optimization easy and do not require any human participation.

Intelligent automation makes it cost-efficient to identify underutilized resources and optimize processes. AI-enabled security mechanisms help in compliance because of the anomaly detection and potential threats prevention. With more and more enterprises adopting cloud technology, there will be an increasing demand for brokerage solutions that include AI.

Challenges: Vendor lock-in risks limiting multi-cloud flexibility

Organizations implementing cloud services brokerage models stand the danger of vendor lock-in, which locks them out from switching vendors or cloud service strategies. Most of the cloud brokerages tend to favor certain vendors and switching between clouds gets difficult. Such dependency may lead to increased costs, decreased bargaining power, and difficulties in exploiting state-of-the-art cloud offerings.

Organizations that are seeking cloud liberty do not want to become a part of the vendor ecosystem due to proprietary integration. Businesses that seek multi-cloud flexibility do not want to get locked up in a system that is not interoperable. To overcome these concerns, businesses need to have brokerage tools that support open standards and multiple cloud services.

Recent Developments:

-

2024: At VMware Explore 2024 Barcelona, Broadcom introduced expanded VMware Cloud Foundation services, enhancing AI-driven applications, cybersecurity, and sovereign cloud adoption, with Tanzu Data Services and VMware Live Recovery.

-

2025: Arrow Electronics introduced new updates to its ArrowSphere cloud platform, adding GreenOps, FinOps, and SecOps dashboards to improve sustainability, cost optimization, and security for channel partners.

-

2024: IBM enhanced its IBM Cloud Pak for Integration with AI-powered orchestration capabilities, enabling enterprises to automate multi-cloud service management and reduce operational complexity across hybrid environments.

Cloud Service Brokerage Market Key Players are:

-

Accenture

-

IBM

-

Broadcom

-

Arrow Electronics

-

Fujitsu

-

DXC Technology

-

Wipro

-

Eviden

-

Amazon Web Services (AWS)

-

Infosys

-

NTT Data

-

Tata Consultancy Services (TCS)

-

Tech Mahindra

-

BMC Software

-

Flexera

-

Jamcracker

-

Cloudmore

-

OpenText

-

Capgemini

-

Oracle

Cloud Service Brokerage Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 14.59 Billion |

| Market Size by 2035 | USD 72.07 Billion |

| CAGR | CAGR of 17.28% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Service (Integration and Support, Automation and Orchestration, Billing and Provisioning, Migration and Customization, Security and Compliance, Others) • By Platform (Internal Brokerage Enablement, External Brokerage Enablement) • By Deployment (Private, Public, Hybrid) • By Enterprise Size (Large Enterprises, Small and Medium-sized Enterprises) • By End-use (IT and Telecom, BFSI, Government and Public Sector, Healthcare, Consumer Goods and Retail, Manufacturing, Energy and Utilities, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Accenture, IBM, Broadcom, Arrow Electronics, Fujitsu, DXC Technology, Wipro, Eviden, Amazon Web Services (AWS), Infosys, NTT Data, Tata Consultancy Services (TCS), Tech Mahindra, BMC Software, Flexera, Jamcracker, Cloudmore, OpenText, Capgemini, and Oracle. |

Frequently Asked Questions

North America dominated the Cloud Service Brokerage Market with approximately 41% revenue share in 2025. Asia Pacific is the fastest-growing region at an estimated CAGR of 19.65%.

Growing multi-cloud strategy adoption, AI-powered automation integration, and enterprise demand for centralized cloud governance are the primary growth factors.

The Cloud Service Brokerage Market was valued at USD 14.59 Billion in 2025.

The Cloud Service Brokerage Market is expected to grow at a CAGR of 17.28% from 2026 to 2035.

The Internal Brokerage Enablement segment dominated with approximately 55% share in 2025. External Brokerage Enablement is expected to grow fastest at a CAGR of 18.16%.

Get in Touch