Coil Coatings Market Report Scope & Overview:

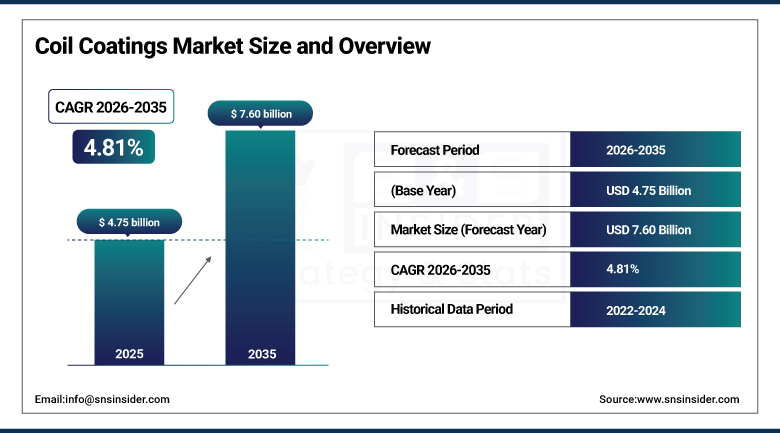

The Coil Coatings Market was valued at USD 4.75 billion in 2025 and is expected to reach USD 7.60 billion by 2035, growing at a CAGR of 4.81% from 2026–2035.

The global coil coatings market is expanding steadily, underpinned by the construction industry’s enduring preference for pre-finished metal surfaces that deliver long-term aesthetic durability, corrosion resistance, and installation efficiency within a single factory-applied system that eliminates on-site painting and substantially lowers building lifecycle maintenance costs. Coil coating is the continuous industrial process of applying organic protective and decorative coatings to metal coils of steel and aluminium on automated high-speed lines before the metal is formed, slit, or fabricated into finished components. The process delivers fundamental efficiency advantages over post-fabrication painting, including precise film thickness control, managed solvent emissions through fully enclosed oven cure systems, near-zero coating waste, and the capacity to apply multiple coating layers in one production pass, making it both economically and environmentally superior across high-volume manufacturing contexts. The market’s growth is principally driven by the global construction boom across residential, commercial, and industrial sectors that is generating sustained demand for pre-painted metal roofing panels, wall cladding, curtain wall infill panels, and structural components whose performance, colour retention, and weather resistance requirements are most reliably achieved through the controlled factory coil coating process. The appliance manufacturing industry represents the second largest demand driver, as the global production of washing machines, refrigerators, dishwashers, air conditioning units, and cooking appliances requires consistently finished steel and aluminium sheet surfaces whose cosmetic quality, scratch resistance, and chemical compatibility with cleaning agents are best achieved through carefully formulated and factory-applied coil coating systems.

The shift across Europe and North America toward low-VOC waterborne and high-solids coil coating formulations, driven by tightening industrial emissions regulations and voluntary sustainability commitments from leading coil coaters and metal product manufacturers, is creating both a product reformulation investment cycle for coating suppliers and a competitive differentiation opportunity for coating companies whose waterborne polyester and PVDF systems can match the performance of solvent-borne incumbents while satisfying the most demanding environmental compliance requirements.

Market Size and Forecast

-

Market size in 2026E: USD 4.98 Billion

-

Market size by 2035: USD 7.60Billion

-

CAGR (2026 to 2035): 4.81%

-

Fastest growing region: Asia Pacific

-

Largest region: Asia Pacific

To Get more information on Coil Coatings Market - Request Free Sample Report

Coil Coatings Market Trends

-

Accelerating transition across the industry toward waterborne and high-solids coil coating formulations that reduce volatile organic compound emissions, meet progressively tightening European Industrial Emissions Directive and U.S. EPA solvent emission standards.

-

Growing adoption of PVDF-based fluoropolymer coil coating systems in premium architectural applications including high-rise façade cladding, roofing membranes, and architectural soffit panels.

-

Rising deployment of UV and electron beam curable coil coating technology, exemplified by PPG Industries’ May 2025 launch of the DuraNEXT energy-curable coil coating line.

-

Expanding application of solar reflective and cool-roof coil coating systems that incorporate infrared-reflective pigments, high solar reflectance index values, and low thermal emittance properties into standard coil-coated metal roofing and wall panel products.

-

Growing interest in antimicrobial and functional coil coating formulations that incorporate silver-based biocidal agents, photocatalytic titanium dioxide particles, or engineered surface micro-textures that reduce microbial colonisation on coated metal surfaces in healthcare, food processing, and transportation applications.

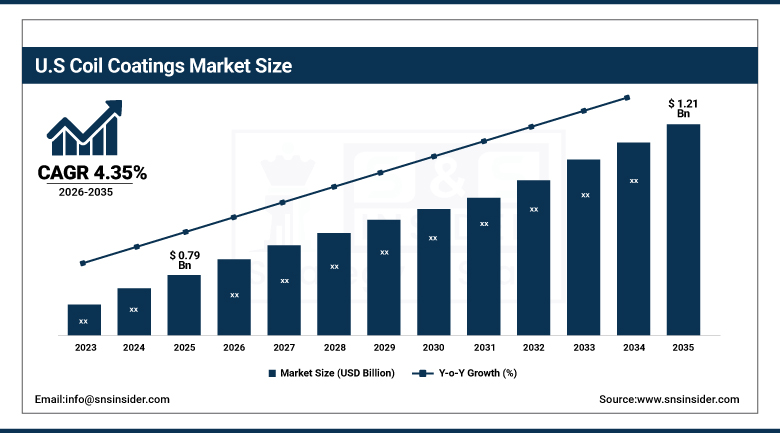

The U.S. coil coatings market outlook

The U.S. coil coatings market was valued at USD 0.79 billion in 2025 and is expected to reach USD 1.21 billion by 2035, growing at a CAGR of 4.35% from 2026–2035.

The United States coil coatings market is characterised by strong institutional demand from the commercial construction sector, where metal building systems manufacturers, standing seam roofing producers, and architectural cladding fabricators collectively account for the largest component of annual coil coating volume consumed domestically. The country’s appliance sector generates the second most significant demand stream, with major manufacturers including Whirlpool, GE Appliances, and LG’s U.S. operations. The Inflation Reduction Act’s investment tax credits for solar energy installations are creating an incremental coil coating demand opportunity in the solar racking, mounting hardware, and building-integrated photovoltaic panel framing segment, as the aluminium extrusion and sheet metal components that solar energy infrastructure requires are increasingly specified with factory-applied coil coating finishes that deliver the corrosion resistance and long service life that 25-year solar system warranties demand.

Sherwin-Williams’ March 2025 acquisition of Shingels, S.A., a Barcelona-based aluminium coil coating specialist, reflects the strategic importance that leading North American coatings companies are placing on the European coil coating market and the technical expertise in aluminium substrate coil coating that positions Sherwin-Williams to serve both European and North American aluminium coil coating demand with enhanced product development and formulation capabilities that the acquisition’s specialist technical team contributes to the combined business.

Coil Coatings Market Segment Analysis

-

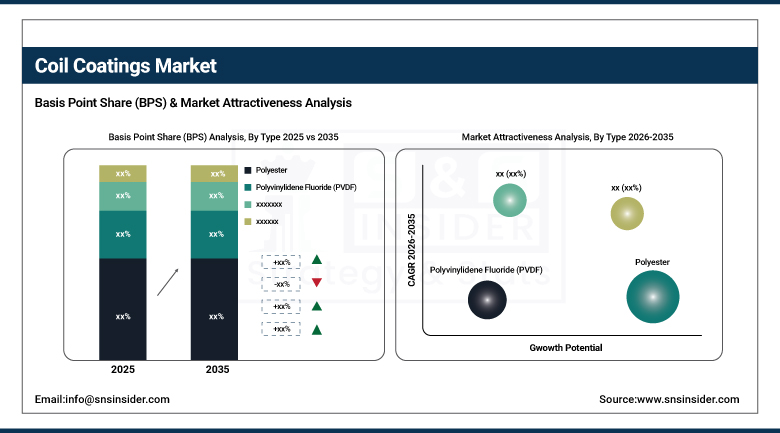

By resin type, polyester dominated the coil coatings market with approximately 48.50% revenue share in 2025; PVDF is the fastest-growing resin segment at a CAGR of approximately 5.80% through the forecast period.

-

By application substrate, steel dominated the coil coatings market with approximately 70% share in 2025; aluminium is the fastest-growing substrate segment.

-

By coating technology, liquid coatings dominated the coil coatings market with approximately 61% share in 2025; powder coatings are the fastest-growing technology segment.

-

By end use, building & construction dominated the coil coatings market with approximately 56.90% revenue share in 2025; automotive is the fastest-growing end use segment at a CAGR of approximately 5.50%.

By Type, polyester dominates resin, PVDF grows fastest

Polyester retained the dominant resin type position with approximately 48.50% of the coil coatings market in 2025, a dominance grounded in its unmatched commercial versatility across the broadest possible range of substrate types, end use applications, coating line configurations, and price points that no other coil coating resin technology can simultaneously serve with equivalent cost efficiency and technical performance. Standard polyester coil coatings deliver the weather resistance, forming flexibility, and colour stability performance that commercial roofing, wall cladding, and appliance applications require as standard specification, while modified polyester chemistries including high-durability polyester and siliconized modified polyester extend the resin family’s performance envelope into applications requiring enhanced UV resistance and gloss retention without reaching the cost level of fluoropolymer alternatives.

PVDF is the fastest-growing resin segment at approximately 5.80% CAGR, driven by its growing adoption in premium architectural facades, roofing systems, and cladding panels across high-rise commercial and institutional construction where its superior colour retention, chalk resistance, and chemical stability over multi-decade service life justify the significant price premium relative to polyester systems through reduced maintenance, recoating, and aesthetic degradation costs over building operational lifetimes measured in 30 to 50 years.

By Application Substrate, steel dominates, aluminium grows fastest

Steel retained the dominant application position with approximately 70% of the coil coatings market in 2025, a reflection of the metal’s enduring status as the primary structural and sheet metal substrate across the construction, appliance, and general industrial sectors that collectively generate the largest volumes of pre-painted metal product demand globally. Hot-dipped galvanised and galvalume steel coils remain the workhorse substrates of the global coil coating industry, providing the combination of structural strength, formability, corrosion protection from the zinc and aluminium-zinc alloy coatings, and excellent coil coating adhesion that standard commercial roofing, wall panel, and metal building system fabrication requires at the cost efficiency that mass residential and commercial construction markets demand.

Aluminium is the fastest-growing substrate at a CAGR driven by progressive adoption in lightweight architectural facade systems, premium appliance exterior surfaces, and electric vehicle body panel applications where aluminium’s natural corrosion resistance, weight advantage over steel, and premium aesthetic appeal are creating incremental coil coating volume across the industry’s highest-value and most technically demanding market segments.

By Technology, liquid coatings dominate, powder coatings grow fastest

Liquid coatings retained the dominant technology position with approximately 61% of the coil coatings market in 2025, anchored by the technology’s long-established integration into the high-speed continuous coil coating production process whose line speeds, multi-layer coating capabilities, and substrate flexibility are optimised for liquid coating application in ways that require substantial capital reinvestment to reconfigure for powder coating delivery. The liquid coatings segment encompasses the full spectrum of solvent-borne, waterborne, and high-solids formulation chemistries across polyester, PVDF, PU, and SMP resin types that together constitute the comprehensive coil coating product portfolio that building, appliance, and industrial customers specify across the global market.

Powder coatings are the fastest-growing technology segment, propelled by zero-VOC emission profiles that satisfy the most demanding industrial air quality regulations, improving formability performance on complex profiles, and the growing construction preference for thicker, more textured surface finishes that differentiate premium architectural metal products in a competitive specification environment.

By End Use, building & construction dominates, automotive grows fastest

Building and construction retained the dominant end use position with approximately 56.90% of the coil coatings market in 2025, reflecting the global construction industry’s structural dependence on pre-painted metal materials whose combination of aesthetic variety, weather protection, low maintenance, and rapid installation enables the design ambition and construction programme efficiency that modern commercial and residential building projects require. The segment’s dominance is sustained by the breadth of coil-coated metal application within buildings, spanning standing seam and trapezoidal profile metal roofing through horizontal and vertical wall cladding, rainscreen panel systems, column cladding, soffit panels, guttering, and fascia to the interior metal ceiling tile, suspended ceiling grid, and partition systems that complete the architectural metal package of a fully finished building.

Automotive is the fastest-growing end use at approximately 5.50% CAGR, as electric vehicle platforms’ extensive aluminium body panel content, battery enclosure fabrication from pre-coated aluminium sheet, and structural lightweight component production are creating new coil coating demand streams in vehicle manufacturing that grow proportionally with EV production volume expansion across China, Europe, and North America.

Regional analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

61.7% |

|

Middle East & Africa |

Saudi Arabia |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Coil Coatings Market Insights

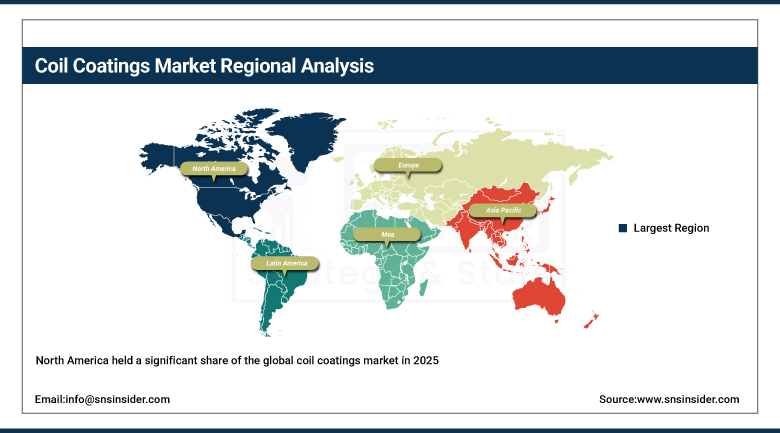

North America held a significant share of the global coil coatings market in 2025, with the United States accounting for approximately 87.4% of North American revenues, underpinned by the country’s large commercial metal building industry, active appliance manufacturing sector, and progressive energy efficiency building code requirements that are driving specification upgrades to higher-performance coil coating systems across new construction and renovation projects. The U.S. market benefits from a dense domestic distribution network of steel service centres and coil coating contract processors whose geographic reach enables just-in-time pre-painted metal supply to fabricators and building product manufacturers across all major construction activity centres. Canada contributes approximately 12.6% of North American coil coatings revenues through its metal building system manufacturing industry in Ontario and Alberta and residential metal roofing adoption that is growing as homeowners in high-snowfall markets choose steel over asphalt shingles for longevity and thermal performance reasons.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Coil Coatings Market Insights

Europe is the global coil coatings market’s most technically sophisticated regional market, characterised by the world’s highest penetration of premium PVDF fluoropolymer coating systems in architectural applications, the most demanding industrial emissions compliance environment that is accelerating the transition to waterborne and energy-curable formulations, and the presence of global coil coating innovation leaders including Beckers Group, AkzoNobel Coil Coatings, and Axalta whose European R&D centres are defining next-generation sustainable coating technology. Germany accounts for approximately 22.3% of European coil coatings revenues as the region’s largest national market, anchored by its major steel and aluminium processing industry, dominant metal building product manufacturing sector, and the appliance manufacturing operations of Bosch-Siemens, Miele, and Liebherr that generate significant coil-coated steel and aluminium sheet demand from domestic and international supply chains. The EU’s tightening industrial VOC emission regulations and the European Green Deal’s broader sustainability agenda are simultaneously creating compliance investment requirements for existing solvent-borne coil coating lines and competitive opportunities for waterborne and UV-curable coating system suppliers whose products align with the regulatory direction of travel.

Asia Pacific Coil Coatings Market Insights

Asia Pacific dominated the global coil coatings market in 2025 with approximately 44% of global revenues, a dominance driven by China’s extraordinary steel and aluminium production and processing scale, the region’s massive residential and commercial construction pipeline, Japan’s and South Korea’s technologically sophisticated coil coating and metal product manufacturing industries, and India’s rapidly expanding construction, appliance, and solar energy sectors that are generating the fastest-growing coil coating demand increment in the global market. China accounts for approximately 61.7% of Asia Pacific coil coatings revenues and represents the single largest national coil coating market globally, with domestic steel mills and coil coating lines supplying pre-painted steel for the country’s enormous residential apartment construction programme, the world’s largest solar panel racking and mounting hardware industry, and a rapidly growing domestic appliance and air conditioning manufacturing sector whose output serves both domestic and export markets. India represents the most significant medium-term growth opportunity in Asia Pacific, as the government’s infrastructure development agenda, affordable housing programme, and Production-Linked Incentive scheme for white goods manufacturing are collectively creating sustained demand growth for coil-coated pre-finished metal products across construction, appliance, and solar energy application categories.

Latin America And MEA Coil Coatings Market Insights

Latin America and the Middle East and Africa are growing coil coatings markets where rapid urbanisation, active construction investment, and expanding industrial manufacturing activity are creating sustained demand for pre-painted metal building products and finished metal components across residential, commercial, and industrial end use categories. Brazil accounts for approximately 44.2% of Latin American coil coatings revenues through its large domestic steel processing industry, active residential and commercial construction sector in São Paulo, Rio de Janeiro, and expanding secondary cities, and a growing domestic appliance manufacturing base that sources pre-coated steel sheet from domestic flat steel producers and international coil coating suppliers serving the Brazilian market through local service centre distribution. Saudi Arabia leads Middle East and Africa coil coatings revenues at approximately 38.4% of the regional total, driven by Vision 2030’s giga-project construction programme requiring enormous volumes of pre-painted steel and aluminium cladding, roofing, and structural components across NEOM, Qiddiya, Diriyah Gate, and the Kingdom’s numerous associated infrastructure and hospitality construction projects that together constitute one of the world’s most concentrated premium coil coating demand opportunities.

Market Dynamics

Growth drivers: Global construction activity sustaining building & construction coil coating demand, appliance manufacturing growth driving pre-painted steel consumption

The primary structural growth drivers for the coil coatings market are the global construction industry’s sustained and broadly based expansion across emerging and established markets that is generating large and consistent volumes of demand for pre-painted metal roofing, wall cladding, and structural building product applications whose performance, aesthetic, and efficiency requirements are best served by the factory-applied coil coating process. The world’s rapidly expanding middle class in Asia Pacific, Africa, and Latin America is simultaneously creating appliance demand growth, as rising household incomes enable first-time purchases of refrigerators, washing machines, air conditioners, and cooking appliances whose manufactured exteriors rely on coil-coated steel and aluminium sheet for the cosmetic quality and corrosion resistance that consumer durability expectations and retail display requirements demand at commercial scale. The renewable energy sector’s extraordinary growth, particularly in solar photovoltaic infrastructure, is creating an incremental coil coating demand stream through the aluminium racking, mounting hardware, and integrated metal roofing systems that large-scale solar installations require in quantities that are growing proportionally with the global solar capacity addition programme that net-zero carbon commitments across more than 130 countries are sustaining across the forecast period.

Restraints: Raw material cost volatility affecting coating formulation margins, fluctuating steel and aluminium production cycles creating substrate availability uncertainty

A significant restraint on the coil coatings market is the raw material cost volatility that affects the primary chemical inputs of coating formulation, spanning titanium dioxide pigments, polyester and PVDF resin feedstocks, crosslinking agents, and solvent or coalescent components whose pricing cycles are driven by energy market fluctuations, petrochemical feedstock availability, and global logistics cost variability that compress coating supplier margins and complicate long-term contract pricing commitments to coating line operators and fabricated metal product manufacturers. The steel and aluminium production cycle’s inherent volatility, where blast furnace and smelter output adjustments in response to commodity market conditions create periodic substrate availability constraints and price spikes that ripple through the coil coating supply chain to affect finished product costs for building product fabricators and appliance manufacturers, represents a structural supply chain risk that coating suppliers and their customers manage through inventory strategies and multi-supplier sourcing relationships but cannot entirely eliminate across the commodity price cycles that characterise the global metals industry.

Opportunities: Electric vehicle aluminium body panel coil coating creating premium growth segment

The electric vehicle industry’s progressive transition to aluminium-intensive body structures, battery enclosure systems, and lightweight structural components is creating a premium coil coating demand opportunity whose technical requirements in terms of adhesion to aluminium substrates, electrocoat compatibility for automotive OEM paint lines, formability without cracking or delamination through complex press forming operations, and surface quality consistency to automotive Class A finish standards are substantially more demanding and higher-value than the standard coil coating specifications that dominate building and appliance applications. The PFAS-free fluoropolymer opportunity, where regulatory pressure on per- and polyfluoroalkyl substances is driving the architectural coatings industry to develop alternative fluoropolymer and high-performance polyester systems that deliver PVDF-equivalent durability without PFAS environmental persistence concerns, represents a significant product development investment cycle that coating companies with strong resin chemistry capabilities are investing in ahead of anticipated regulatory mandates across European and North American markets.

Recent developments:

-

2025: PPG Industries launched the DuraNEXT line of energy-curable coil coatings in May 2025, comprising UV and electron beam-curable backers, primers, basecoats, and clearcoats that cure instantly at ambient temperature without thermal ovens or solvents.

-

2025: Sherwin-Williams acquired Shingels, S.A. in March 2025, a Barcelona-based paints and coatings manufacturer specialising in aluminium coil coating and industrial applications across Europe, strengthening Sherwin-Williams’ European coil coating market position.

-

2025: AkzoNobel Coil Coatings continued the commercial rollout of its FIDURA versatile coil coating system, launched in August 2024 and targeted at the construction sector with a formulation designed to deliver the flexibility, adhesion consistency, and durability performance across diverse steel and aluminium substrates.

Coil Coatings Market Companies are:

-

AkzoNobel NV

-

PPG Industries Inc.

-

Beckers Group

-

Axalta Coating Systems LLC

-

The Sherwin-Williams Company

-

BASF SE

-

Nippon Paint Holdings Co., Ltd.

-

Kansai Paint Co., Ltd.

-

KCC Corporation

-

The Chemours Company

-

Henkel AG & Co. KGaA

-

Wacker Chemie AG

-

Valspar Corporation

-

Teknos Group

-

Tiger Coatings GmbH & Co. KG

-

Salchi Metalcoat

-

Yung Chi Paint & Varnish Manufacturing Co., Ltd.

-

JSW Paints

-

Jotun A/S

-

Hempel A/S

Coil Coatings Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.75 billion |

| Market Size by 2035 | USD 7.60 Billion |

| CAGR | CAGR of 4.81% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Resin Type (Polyester, Polyvinylidene Fluoride (PVDF), Polyurethane (PU), Silicone Modified Polyester (SMP), Plastisols, Others) • By Application (Steel, Aluminum) • By Coating Technology (Liquid Coatings, Powder Coatings) • By End Use (Building & Construction, Appliances, Automotive, Transportation, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | AkzoNobel NV, PPG Industries Inc., Beckers Group, Axalta Coating Systems LLC, The Sherwin-Williams Company, BASF SE, Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., KCC Corporation, The Chemours Company, Henkel AG & Co. KGaA, Wacker Chemie AG, Valspar Corporation, Teknos Group, Tiger Coatings GmbH & Co. KG, Salchi Metalcoat, Yung Chi Paint & Varnish Manufacturing Co., Ltd., JSW Paints, Jotun A/S, Hempel A/S |

Frequently Asked Questions

Asia Pacific dominated the coil coatings market in 2025, with China as the leading national market within the region.

Polyester dominated with approximately 48.50% revenue share in 2025.

The sustained global construction industry expansion generating large-scale demand for pre-painted metal roofing, wall cladding, and building product applications driving pre-coated steel and aluminium sheet consumption.

The coil coatings market was valued at USD 4.75 billion in 2025.

The coil coatings market is expected to grow at a CAGR of 4.81% from 2026 to 2035.

Get in Touch