Rainscreen Cladding Market Report Scope & Overview:

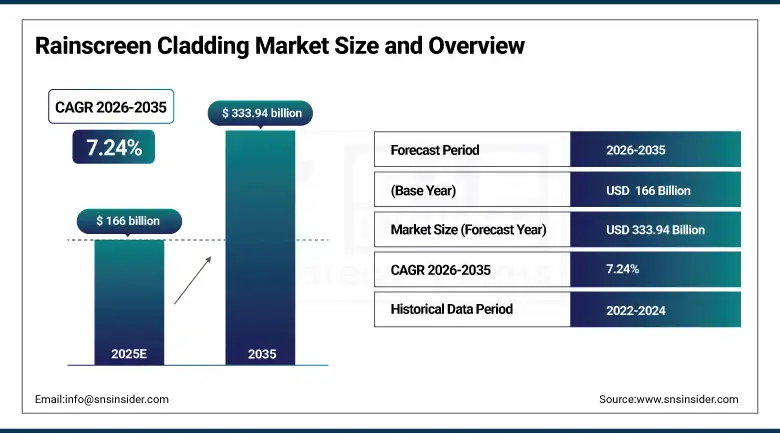

The Rainscreen Cladding Market size was valued at USD 166 billion in 2025 and is expected to reach USD 333.94 billion by 2035, growing at a CAGR of 7.24% over the forecast period of 2026-2035.

The global rainscreen cladding market trend is a growing demand for high-performance building envelope solutions such as ventilated facade systems, fiber cement cladding panels, and metal composite wall assemblies as the growth of the market is driven by increasing construction activity, government building energy codes, and rising need for weather-resistant and fire-safe exterior wall systems. This trend is also driven by a growing adoption of green building certifications and the growing focus on energy-efficient building design as developers and architects become more focused on reducing building lifecycle costs and are more willing to invest in durable exterior cladding systems, resulting in growth in the domestic and international market for new construction and renovation rainscreen cladding applications.

For instance, in March 2025, growing enforcement of fire safety regulations and rising commercial construction activity drove a 19% increase in rainscreen cladding installations for high-rise and institutional buildings across Europe, boosting demand for non-combustible facade systems and certified ventilated wall assemblies.

Rainscreen Cladding Market Size and Forecast:

-

Market Size in 2025: USD 166 billion

-

Market Size by 2035: USD 333.94 billion

-

CAGR: 7.24% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Rainscreen Cladding Market - Request Free Sample Report

Rainscreen Cladding Market Trends

-

Rainscreen cladding systems are being adopted because developers and building owners demand reliable protection from moisture, wind, and weathering along with reduced long-term maintenance costs for commercial and residential building exteriors.

-

Customized facade panel designs based on building type, climate zone, and project aesthetic requirements to improve the visual quality and weathertightness performance of building envelopes.

-

The development of lightweight composite panels, prefabricated facade modules, and digitally specified cladding systems to improve installation speed and reduce overall construction costs.

-

Fire-rated panel materials, non-combustible subframe systems, and third-party certified wall assemblies are all specified to ensure building safety regulation compliance and reduce risk of fire spread on external walls.

-

Increased demand for cloud-based product specification platforms, digital installation guides, and mobile-compatible cladding libraries to support faster procurement and improve on-site accuracy.

-

Collaboration between cladding manufacturers, facade engineering consultants, and main contractors to develop integrated rainscreen wall systems and improve standards of weathertightness and thermal performance.

-

Building safety regulators in the UK, EU, and North America promoting standards for fire resistance, combustibility classification, and external wall system testing to improve accountability and safety across the supply chain.

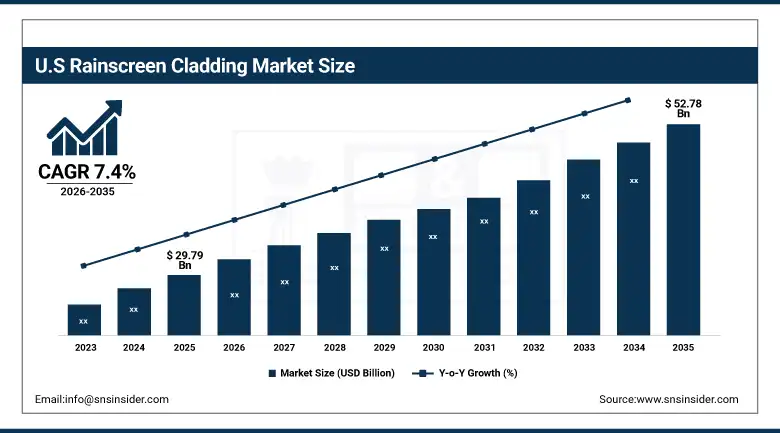

The U.S. Rainscreen Cladding Market was valued at USD 29.79 billion in 2025 and is expected to reach USD 52.78 billion by 2035, growing at a CAGR of 7.4% from 2026-2035. The United States represents the largest market for rainscreen cladding, primarily driven by the high volume of commercial and institutional construction activity, mandatory building energy performance codes, and well-developed construction materials supply infrastructure. Government and private sector investment in building retrofits, moderately high levels of green building certification adoption, and increased developer and contractor spending on facade performance help to drive growth in the market. Also, the U.S. is the largest regional market in the world, due to the regulatory support and swift adoption of fiber cement and metal composite rainscreen cladding systems across both new construction and renovation segments.

Rainscreen Cladding Market Growth Drivers:

-

Tightening Building Safety Regulations and Energy Efficiency Codes are Driving the Rainscreen Cladding Market Growth

Tightening building safety regulations and energy efficiency codes take the center stage as a growth driver for the rainscreen cladding market share, and are driven by the enforcement of fire resistance requirements, combustibility restrictions on external wall materials, and mandatory thermal performance standards across key construction markets. These requirements for building envelope improvement and occupant safety are driving the base of the market, the penetration of fiber cement and metal cladding product segments, and adding to the overall market share globally.

For instance, in January 2025, fire safety remediation programs in the United Kingdom contributed to a 24% increase in demand for non-combustible rainscreen cladding systems, as high-rise residential buildings began replacement of non-compliant external wall cladding under government-backed remediation funding schemes.

Rainscreen Cladding Market Restraints:

-

High Installation and Material Costs are Hampering the Rainscreen Cladding Market Growth

High installation and material costs of rainscreen cladding systems also restrict the rainscreen cladding market growth, as a large number of developers and building owners who recognize the performance benefits of ventilated facade systems remain deterred by the higher upfront cost of installation compared to conventional rendered or direct-fix wall cladding alternatives. This might lead to slower adoption rates, preference for lower-cost cladding products, and reduced investment in high-performance facade systems among cost-sensitive project types. As a result, market penetration is limited in the residential renovation segment and market growth is stunted in regions where construction budgets are constrained and awareness of long-term lifecycle cost savings is still limited.

Rainscreen Cladding Market Opportunities:

-

Growing Building Renovation and Energy Retrofit Activity Drives Future Growth Opportunities for the Rainscreen Cladding Market

The opportunity in growing building renovation and energy retrofit activity for the rainscreen cladding market is in the form of government-funded energy upgrade programs, fire safety remediation schemes, and owner-driven building improvement projects. These programs provide for improved building thermal performance, updated fire safety compliance, and extended building service life at the same time. Through increased specification of rainscreen systems as part of whole-building retrofit packages, growing government funding for energy efficiency improvements, and rising owner awareness of the dual performance and property value benefits of facade upgrades, particularly in regions with large volumes of aging commercial and residential buildings, these opportunities may improve adoption rates, reduce dependence on new construction cycles, and expand the market.

For instance, in February 2025, the European Commission’s Renovation Wave initiative reported that over 35 million buildings across EU member states were targeted for energy-efficiency upgrades by 2030, with rainscreen cladding systems identified as a preferred solution for improving building envelope performance in residential and institutional retrofit projects.

Rainscreen Cladding Market Segment Analysis

-

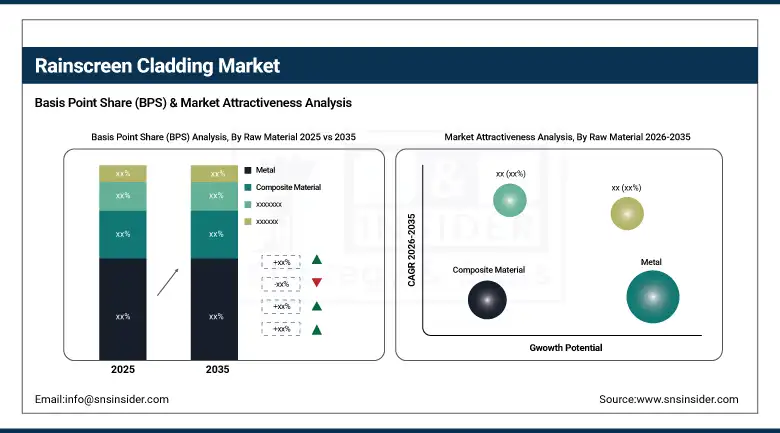

By raw material, metal held the largest share of around 36.42% in 2025, and the fiber cement segment is expected to register the highest growth with a CAGR of 8.12%.

-

By construction, new construction dominated the market with approximately 61.37% share in 2025, while the renovation segment is expected to register the highest growth with a CAGR of 8.54%.

-

By application, commercial accounted for the leading share of nearly 34.16% in 2025, and the institutional segment is expected to register the highest growth with a CAGR of 8.31%.

By Raw Material, Metal Leads the Market, While Fiber Cement Registers Fastest Growth

The metal segment accounted for the highest revenue share of approximately 36.42% in 2025, owing to its widespread use in commercial, institutional, and industrial construction projects due to its durability, design flexibility, and compatibility with a wide range of subframe systems. Emerging trends, including growing demand for lightweight facade materials and architect preference for clean metallic aesthetics in commercial building exteriors. In comparison, the fiber cement segment is anticipated to achieve the highest CAGR of nearly 8.12% during the 2026–2035 period, driven by the increasing demand from the residential and renovation segments, lower cost relative to composite and terracotta alternatives, and growing awareness of its fire resistance and weathering durability. Drivers include rising adoption among residential developers, the preference for fiber cement’s wide range of available textures, panel sizes, and surface finishes.

By Construction, New Construction Dominates, While Renovation Segment Shows Rapid Growth

By 2025, the new construction segment contributed the largest revenue share of 61.37% due to a sustained global pipeline of commercial, institutional, and residential building projects, particularly across Asia Pacific and the Middle East, and ongoing infrastructure investment in North America and Europe. Growing inclusion of rainscreen cladding in standard construction specifications for commercial and mixed-use developments and architect preference for performance-driven building envelopes from project inception are helping to anchor the segment’s position. The renovation segment is projected to grow at the highest CAGR of approximately 8.54% between 2026 and 2035 due to the growing need for building energy upgrades, fire safety remediation works, and owner-driven facade improvements across aging commercial and residential building stock. Some of the reasons include government-funded retrofitting programs across Europe and North America, growing recognition of renovation as a lower-carbon construction approach, and the energy cost savings delivered by improved external wall thermal performance.

By Application, Commercial Leads, While Institutional Segment Registers Fastest Growth

The commercial segment accounted for the largest share of the rainscreen cladding market with about 34.16%, owing to strong investment in office buildings, retail developments, hotels, and mixed-use urban projects where facade durability, weather performance, and architectural finish are primary specification requirements. Reasons driving the commercial segment include continued expansion of commercial real estate in Asia Pacific, ongoing office regeneration schemes across European cities, and steady growth of the U.S. commercial construction pipeline. In addition, the institutional segment is slated to grow at the fastest rate with a CAGR of around 8.31% throughout the forecast period of 2026–2035, as government investment in healthcare buildings, educational campuses, civic infrastructure, and public transport facilities increases globally. Increased focus on building fire safety compliance, long-term facade durability, and energy performance in publicly funded projects contribute to their adoption, while improved building safety ratings and reduced maintenance costs drive continued investment.

Rainscreen Cladding Market Regional Highlights:

North America Rainscreen Cladding Market Insights:

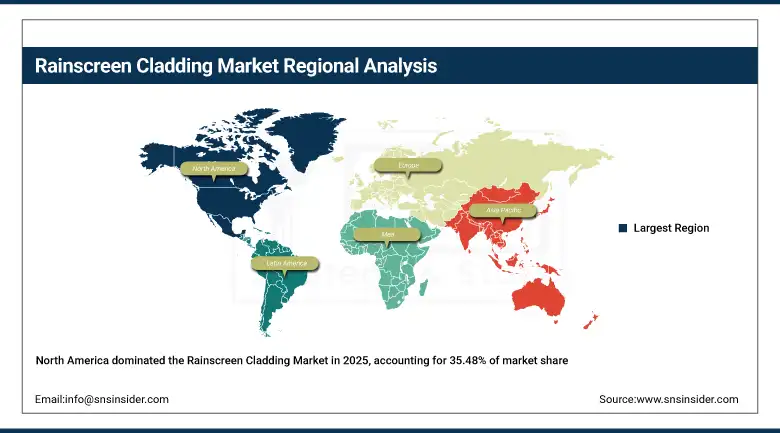

North America held the largest revenue share of over 35.48% in 2025 of the rainscreen cladding market due to an established construction industry, mandatory building energy performance codes, and strong commercial and institutional construction investment. Drivers include widespread use of fiber cement and composite rainscreen systems in both new construction and renovation projects, an improved construction supply chain network, growing awareness of the long-term performance advantages of ventilated facade systems stemming from increasing focus on energy efficiency and building sustainability. At the same time, various government infrastructure spending programs, building safety code updates, and enormous investments in commercial and public building construction from developers, healthcare operators, and educational institutions are anchoring rainscreen cladding products and systems in the market, and ensuring continued market revenue growth globally.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Rainscreen Cladding Market Insights:

Asia Pacific is the fastest-growing region in the rainscreen cladding market with a CAGR of 8.67%, as the awareness about modern building envelope systems, government infrastructure investment, and construction activity in developing nations is growing. Factors including rapid urbanization, a rising middle-class population with higher expectations for building quality, and growing uptake of international construction standards are stimulating the market growth. Government-backed smart city and healthcare infrastructure programs have been instrumental in increasing demand for high-performance cladding systems, especially in urban commercial and institutional buildings. Public-private partnerships and national construction programs also help in advancing building quality standards and adoption of modern facade systems. Increase in demand in Asia Pacific region owing to rising construction spending against historical levels and growing availability and affordability of locally manufactured rainscreen cladding systems.

Europe Rainscreen Cladding Market Insights:

The rainscreen cladding market in Europe is the second-dominating region after North America on account of an increase in the enforcement of fire safety regulations following the Grenfell Tower fire, mandatory energy performance standards under the EU Energy Performance of Buildings Directive, and increasing government support for building renovation and energy upgrade programs. Rising implementation of national building remediation schemes, advanced digital construction strategies, favorable government funding for energy efficiency improvements, and cross-border building safety directives are also contributing to the sustained growth of the market in leading European construction markets.

Latin America (LATAM) and Middle East & Africa (MEA) Rainscreen Cladding Market Insights:

In Latin America, and Middle East & Africa, the growing construction activity and increase in urbanization with rising government investment in public infrastructure support the rainscreen cladding market growth. The rising popularity of internationally certified cladding products at more accessible price points and improving architect and developer awareness of the performance benefits of ventilated facade systems, along with large-scale urban development programs, will aid building quality improvements and rainscreen system adoption. The increasing scale of commercial and institutional construction in Saudi Arabia, the UAE, and Brazil, and improving construction materials supply chains in these regions, are continuing to encourage market growth.

Rainscreen Cladding Market Competitive Landscape:

Kingspan Group plc (est. 1965) is a leading manufacturer of high-performance insulation and building envelope systems that focuses on rainscreen facade panels, insulated composite cladding, and ventilated wall assemblies for commercial, residential, and industrial construction markets. It uses its wide manufacturing network and specification relationships with architects and contractors to produce rainscreen cladding products that meet fire safety, thermal performance, and sustainability requirements.

-

In August 2025, Kingspan Group launched a new range of rainscreen cladding products developed to meet updated fire safety and environmental performance standards, targeting commercial new build and government-funded building retrofit programs across European and North American markets.

Rockwool International A/S (est. 1909) is a well-known global manufacturer of stone wool insulation and fire-resistant building products focused on non-combustible rainscreen cladding solutions and thermal wall systems for commercial, institutional, and residential construction. It invests in manufacturing capacity expansion and product development with the goal of meeting rising global demand for fire-safe, energy-efficient external wall systems across key construction markets.

-

In September 2025, expanded production capacity with investment in a new European manufacturing facility, increasing its ability to supply non-combustible cladding and insulation systems to growing fire safety remediation and new construction markets across the UK, Germany, and Scandinavia.

James Hardie Industries plc (est. 1888) is a world-leading fiber cement building products manufacturer that focuses on durable, low-maintenance, and fire-resistant rainscreen cladding panels, facade boards, and exterior wall systems for residential, commercial, and institutional construction. The company’s fiber cement cladding product range focuses on weatherproofing performance and design versatility, and features a strong presence in North American, Australian, and European construction markets owing to its established supply chain and installer network.

-

In February 2025, returned to the NAHB International Builders’ Show in Las Vegas, presenting an expanded range of fiber cement rainscreen cladding products and enhanced fire-resistant panel formats, reinforcing its commitment to innovation and sustainable facade solutions for the residential and commercial construction sectors.

Rainscreen Cladding Market Key Players:

-

Kingspan Group plc

-

Rockwool International A/S

-

James Hardie Industries plc

-

Sika AG

-

Trespa International B.V.

-

Etex Group SA

-

Cembrit Holding A/S

-

FunderMax GmbH

-

Saint-Gobain S.A.

-

SFS Holding AG

-

Sotech Optima

-

Alucobond (3A Composites GmbH)

-

Hunter Douglas N.V.

-

Nichiha Corporation

-

Everest Industries Limited

-

Carea Facade

-

Sto SE & Co. KGaA

-

Equitone (Eternit S.A.)

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 154.79 billion |

| Market Size by 2032 | USD 268.67 billion |

| CAGR | CAGR of 7.14% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Raw Material (Fiber Cement, Composite Material, Metal, High Pressure Laminates, Terracotta, Ceramic, Others) •By Construction (New Construction, Renovation) •By Application (Residential, Commercial, Offices, Institutional, Industrial) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Kingspan Group plc, Rockwool International A/S, Trespa International B.V., FunderMax GmbH, Compagnie de Saint-Gobain S.A., Sika AG, SFS Group AG, Alucobond (3A Composites), Hunter Douglas Architectural, and Sto Corp. |

Frequently Asked Questions

Strict regulations favor biodegradable coatings, boosting Rainscreen Cladding market share and reducing single-use plastics reliance.

Trends include prefabricated ventilated façade systems, lifecycle performance focus, and AI-based design tools for customization.

Raw materials include terracotta, metal, fiber cement, composites, high-pressure laminates, ceramics, and others.

Growth is fueled by net-zero policies, AI-powered design tools, and recycled, low-carbon facade cladding materials demand.

The rainscreen cladding market size was valued at USD 166 billion in 2025, reflecting steady global demand growth.

Get in Touch