Computer Assisted Coding Market Report Scope & Overview:

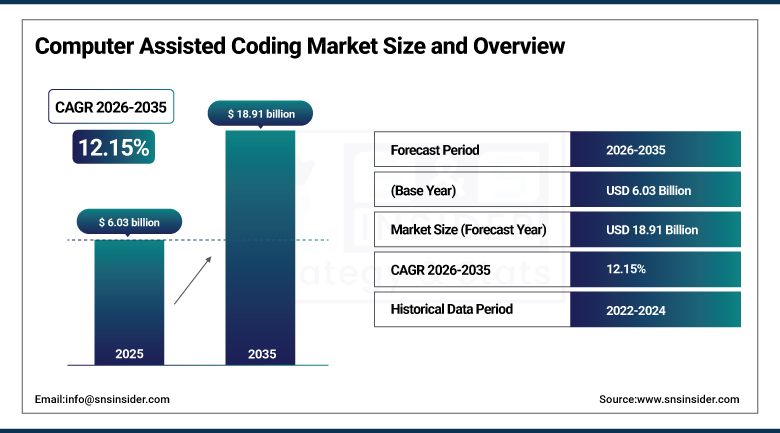

The Computer Assisted Coding Market was valued at USD 6.03 Billion in 2025 and is expected to reach USD 18.91 Billion by 2035, growing at a CAGR of 12.15% from 2026–2035.

The global computer assisted coding market is experiencing exceptional growth rates. Computer assisted coding (CAC) entails software programs that examine health care clinical documentation and automatically create medical codes with the help of natural language processing (NLP) and machine learning algorithms. Drivers of growth in this market include automation along with compliance-driven solutions that have proven to be significantly effective in terms of reduced error rates and improved accuracy of coding. Due to the increasing use of NLP and AI within CAC systems, these products enhance accuracy of coding, reduce chances for errors, increase efficiency of workflow and improve coding and compliance due to a growing trend of cloud-based CAC.

In January 2024, 3M Health Information Systems released an updated CAC software featuring enhanced machine learning algorithms for improved coding accuracy and better integration with electronic health record (EHR) systems. The updated platform’s EHR integration eliminates the manual chart pulling and dual-system entry, creating workflow efficiency improvement whose coder productivity measurement sustains institutional procurement motivation for premium integrated CAC solutions above standalone coding tools.

Market Size and Forecast

-

Market Size in 2026E: USD 6.76 Billion

-

Market Size by 2035: USD 18.91 Billion

-

CAGR: 12.15% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Computer Assisted Coding Market - Request Free Sample Report

Computer Assisted Coding Market Trends

-

Generative AI integration enables autonomous clinical documentation review, improving coding accuracy in complex multi-condition encounters significantly.

-

Real-time CAC during clinical documentation improves clinician engagement, reducing delays and increasing first-pass coding accuracy.

-

ICD-10 coding complexity with 70,000+ codes drives CAC adoption to reduce errors and improve compliance efficiency.

-

Remote coding workforce expansion increases demand for cloud-based CAC platforms with secure access and audit capabilities.

-

Value-based care reimbursement models drive CAC adoption for accurate HCC coding and improved revenue capture performance.

The U.S. Computer Assisted Coding Market Outlook

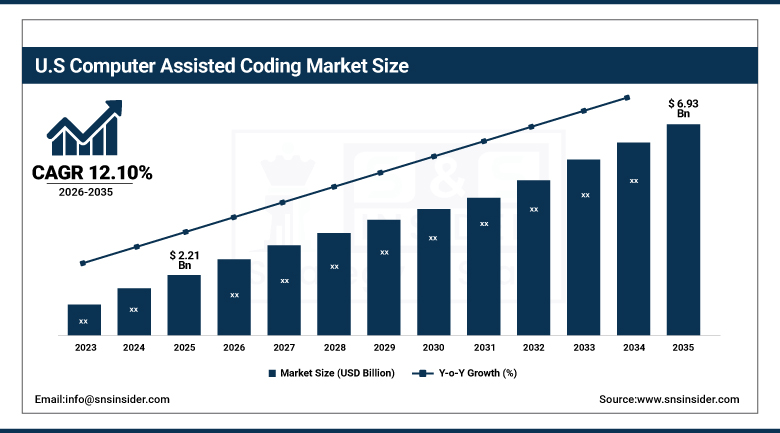

The U.S. computer assisted coding market was valued at approximately USD 2.21 Billion in 2025 and is expected to reach approximately USD 6.93 Billion by 2035, growing at a CAGR of approximately 12.10%.

The U.S. is the most commercially significant CAC market within North America’s dominant position. 3M Health Information Systems, Nuance Communications (Microsoft), Optum360, M*Modal, and Dolbey Systems collectively define the domestic CAC commercial landscape. The U.S. ICD-10-CM/PCS coding system’s complexity, CMS’ risk adjustment payment model’s HCC coding accuracy requirement, and HIPAA’s compliance standards create structured institutional procurement motivation. The extraordinary U.S. healthcare revenue cycle’s scale—whose annual medical billing transaction volume exceeds USD 3 trillion—creates the commercial foundation whose coding accuracy improvement creates measurable ROI that sustains CAC investment.

In March 2024, Optum360 launched a new CAC platform aimed at streamlining coding processes in outpatient settings, incorporating advanced natural language processing capabilities to enhance coding accuracy and efficiency across diverse clinical documentation. The outpatient focus addresses the historically underserved ambulatory coding market whose CPT/HCPCS complexity and high documentation volume create above-average CAC ROI from professional fee coding automation that supplements established inpatient DRG coding CAC deployment.

Computer Assisted Coding Market Segment Analysis

-

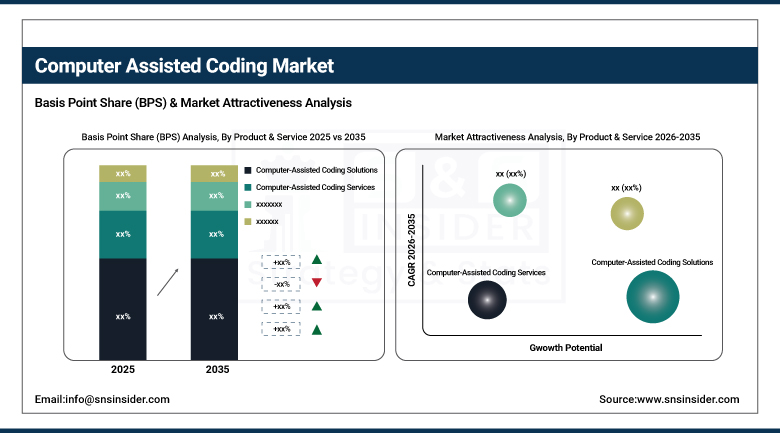

By Product & Service, the computer-assisted coding solutions segment dominated the computer assisted coding market in 2025, while the computer-assisted coding services segment is expected to be the fastest growing.

-

By Mode of Delivery, the cloud-based CAC segment dominated the computer assisted coding market with more than 48% share in 2025, while the web-based CAC segment is predicted to register the fastest CAGR during the forecast period.

-

By End User, the providers segment dominated the computer assisted coding market in 2025, while the payers segment is anticipated to register the fastest CAGR during the forecast period.

-

By Application, the inpatient coding segment dominated the computer assisted coding market with approximately 52% share in 2025, while the outpatient coding segment is the fastest growing.

By Product & Service, the computer-assisted solutions dominates, the computer-assisted services grow fastest

Computer-assisted coding solutions retained the dominant position in the market in 2025. CAC solution software’s commercial primacy reflects its foundational role as the primary commercial value in every CAC deployment whose NLP and machine learning capability creates the coding suggestion intelligence that generates measurable coder productivity improvement and error reduction ROI. Each hospital that deploys CAC software creates procurement whose per-facility license value reflects the coder count, coding volume, and system integration complexity. 3M’s 360 Encompass CAC, Nuance’s CAC Pro, Optum360’s CAC platform, and M*Modal’s Fluency for Coding collectively demonstrate the commercial ecosystem whose software capability creates institutional adoption motivation across inpatient, outpatient, and physician fee coding applications.

Computer-assisted coding services are the fastest-growing segment because increasing healthcare organization complexity creates growing demand for expert implementation, optimization, and ongoing support services whose technical depth creates above-software commercial relationships. Each CAC implementation whose EHR integration, workflow redesign, and coder training requirement creates services procurement that substantially exceeds the software license value in complex health system deployment contexts. The managed CAC service model, whose vendor-operated coding support combines technology and human expertise, creates recurring service revenue whose per-year commercial value sustains above-software growth.

By Mode of Delivery, cloud dominates, web-based grows fastest

Cloud-based CAC retained the dominant delivery mode position with more than 48% of the market in 2025. Cloud CAC’s commercial primacy reflects the healthcare industry’s progressive digital transformation’s shift from on-premise software to cloud-hosted SaaS platforms whose operational cost, update cadence, and scalability advantages create institutional specification preference. The cloud platform’s automatic code set update capability creates compliance currency assurance that sustains cloud specification preference in regulatory-sensitive healthcare billing. The remote coding workforce’s cloud access requirement creates institutional cloud CAC motivation that on-premise alternatives cannot serve with equivalent security and accessibility.

Web-based CAC is the fastest-growing delivery mode because its browser-accessible architecture eliminates client-side installation requirement, reducing IT deployment complexity for smaller practices and rural health systems whose limited IT infrastructure creates on-premise and even SaaS-managed deployment barriers. Each ambulatory practice, community hospital, and health system whose simplified deployment preference creates web-based specification creates adoption whose aggregate across the underserved outpatient and community healthcare market creates above-enterprise growth rate.

By End User, providers dominate, payers grow fastest

Providers retained the dominant end-user position in the computer assisted coding market in 2025. Hospital and health system’s inpatient coding programme, ambulatory coding department, and physician practice’s professional fee coding collectively create the most commercially concentrated CAC procurement category whose revenue cycle management investment sustains consistent demand. Each hospital system’s DRG-based inpatient reimbursement whose MS-DRG coding accuracy directly impacts case mix index and revenue creates CAC investment motivation whose financial return is measurable and auditable. The Joint Commission’s clinical documentation improvement programme’s integration with CAC creates institutional quality motivation that compounds with financial ROI.

Payers are the fastest-growing end user because insurance companies and health plan administrators’ growing adoption of CAC for claims processing automation, fraud and abuse detection, and risk adjustment accuracy creates structured commercial growth that compounds with value-based care reimbursement’s expansion. Each health plan that deploys CAC for claims review automation creates procurement whose processing volume at millions of annual claims creates commercial scale. The Medicare Advantage risk adjustment’s HCC coding accuracy audit creates payer motivation for CAC-assisted claims validation whose revenue protection value sustains premium system investment.

By Application, inpatient dominates, outpatient grows fastest

Inpatient coding retained the dominant application position with approximately 52% of the market in 2025. The inpatient coding application’s commercial primacy reflects the historical deployment priority where hospital DRG reimbursement’s per-case financial impact creates the most compelling single-application CAC ROI. Each hospital’s inpatient admission whose discharge coding creates DRG assignment affecting reimbursement by thousands of dollars creates motivation for CAC accuracy improvement whose error prevention value compounds with annual case volume. The inpatient coding workflow’s established CAC integration infrastructure creates commercial maturity that sustains consistent procurement as health system scale and case volume grow.

Outpatient coding is the fastest-growing application because the extraordinary ambulatory care volume’s CPT/HCPCS professional fee coding creates above-average per-coder productivity improvement motivation that historically underserved outpatient CAC deployment creates. Each outpatient encounter’s evaluation and management level assignment, procedure code selection, and diagnosis linkage creates coding complexity whose CAC assistance creates productivity improvement that sustains ROI beyond inpatient DRG alternatives. The outpatient setting’s higher encounter volume and shorter encounter documentation creates CAC processing throughput whose productivity improvement per coder creates financial motivation.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

North America Computer Assisted Coding Market Insights

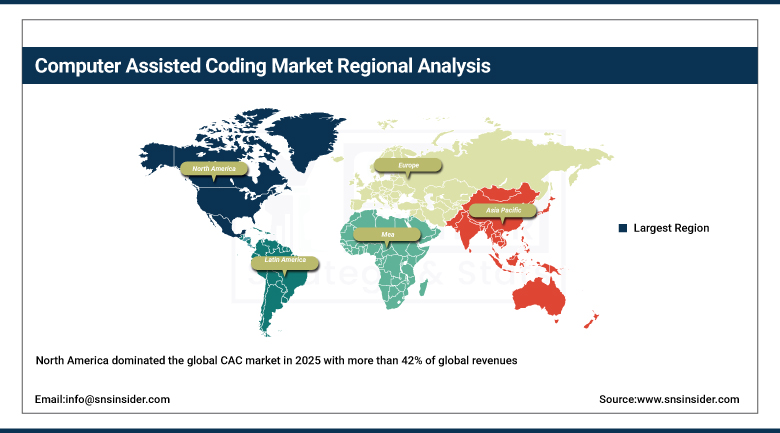

North America dominated the global CAC market in 2025 with more than 42% of global revenues. The United States accounts for approximately 87.4% of North American revenues through 3M Health Information Systems, Nuance Communications (Microsoft), Optum360, M*Modal, and Dolbey Systems’ commercial operations sustained by the U.S. healthcare system’s complexity and scale.

Canada contributes approximately 12.6% of North American revenues through its provincial health system’s ICD-10-CA coding adoption, the hospital sector’s revenue cycle management investment, and the growing CAC platform deployment in academic medical centers.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Computer Assisted Coding Market Insights

Europe is a technically sophisticated CAC market where ICD-10 national variants, DRG reimbursement system adoption, and hospital sector’s coding accuracy investment create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its G-DRG (German Diagnosis Related Groups) reimbursement system’s coding complexity and the hospital sector’s clinical documentation improvement investment.

France, the United Kingdom, and the Netherlands are significant secondary markets where national DRG systems, electronic health record adoption, and hospital revenue cycle modernization create consistent CAC procurement.

Asia Pacific Computer Assisted Coding Market Insights

Asia Pacific is the fastest-growing regional CAC market, driven by swift healthcare digitalization, increasing medical expenditure, and a growing preference for automated coding solutions. China accounts for approximately 44.8% of Asia Pacific revenues through its extraordinary hospital network expansion, the national health information system’s EHR adoption, and the growing revenue cycle management investment.

Japan’s advanced healthcare IT system, South Korea’s sophisticated hospital information system, and India’s rapidly growing private hospital sector’s revenue cycle investment create significant secondary markets whose combined procurement reinforces Asia Pacific’s fastest-growing regional status.

MEA & Latin America Computer Assisted Coding Market Insights

The MEA and Latin America Computer Assisted Coding (CAC) markets are witnessing steady growth driven by healthcare digital transformation and increasing coding complexity. In the Middle East & Africa, Saudi Arabia leads with approximately 31.2% revenue share, supported by Vision 2030 healthcare digitalization initiatives, nationwide EHR adoption, and rising investment in revenue cycle management systems.

In Latin America, Brazil dominates with around 44.2% share due to its extensive hospital network, growing demand for automated billing systems, and complexity of the TUSS coding framework. Expansion of private healthcare insurance and claims automation further strengthens CAC adoption across both regions.

Market Dynamics

Growth Drivers: AI and NLP technologies enhancing coding accuracy and ICD-10 complexity creating human error risk

AI and NLP technologies enhancing coding accuracy, reducing errors, and improving workflow efficiency in healthcare is the SNS Insider confirmed primary growth driver for the CAC market. Each new NLP model generation’s contextual clinical language understanding improvement creates coding suggestion quality whose accuracy performance creates coder productivity measurement that sustains institutional procurement motivation. The generative AI’s progressive integration with CAC creates autonomous documentation review capability whose large language model’s clinical narrative comprehension creates coding suggestion intelligence that rule-based alternatives cannot match in complex multi-condition encounter documentation.

ICD-10-CM/PCS coding system’s extraordinary complexity, whose 70,000+ code set creates human error risk in multi-condition encounter coding, creates systematic CAC motivation whose error prevention value compounds with the health system’s annual coding volume. Each ICD-10 code assignment error whose DRG impact creates reimbursement underpayment or compliance audit risk creates measurable financial motivation for CAC investment whose systematic code coverage prevents the high-consequence errors that human coder fatigue and knowledge gap create.

Restraints: Frequent coding regulation changes requiring continuous updates and EHR integration complexity

Frequent changes in medical coding regulations including annual ICD-10 code updates, CPT code additions and deletions, and CMS payment policy revisions require continuous CAC software database and algorithm updates whose development investment creates ongoing vendor cost that moderates system pricing competitiveness for smaller organisations. Each regulatory cycle’s coding update requirement creates vendor investment that sustains subscription model preference over perpetual license alternatives.

EHR integration complexity whose diverse health information system vendor landscape creates custom interface development requirement for each CAC deployment creates implementation timeline and cost that moderates adoption pace. Each EHR system’s proprietary documentation structure creates CAC integration project whose complexity creates implementation barrier that moderates smaller organization adoption below the technically available market.

Opportunities: Risk adjustment HCC coding automation and AI-powered autonomous coding

Medicare Advantage risk adjustment’s hierarchical condition category (HCC) coding completeness requirement creates premium CAC application whose annual revenue risk adjustment recalculation creates financial motivation for systematic HCC gap identification that manual coding audit cannot achieve at equivalent coverage. Each Medicare Advantage health plan whose risk score accuracy creates reimbursement impact motivates CAC investment whose revenue capture measurement sustains premium system specification.

AI-powered autonomous coding, whose advanced NLP capability creates fully automated code assignment from clinical documentation without human coder review for high-confidence encounters, represents the most commercially transformative CAC development whose per-encounter processing cost reduction creates economic disruption of the traditional human coding workflow.

Recent Developments:

-

2026: Nuance Communications (Microsoft) upgraded Dragon Medical One and CAC-enabled documentation tools in 2026 with generative AI clinical intelligence features, enabling real-time coding assistance and reducing administrative burden for clinicians.

-

2025: 3M Health Information Systems enhanced its 3M 360 Encompass System with advanced AI-driven natural language processing and improved ICD-10 coding automation, increasing coding accuracy and accelerating hospital revenue cycle workflows.

-

2025: Optum Inc. expanded Optum360 CAC capabilities by integrating generative AI-based clinical documentation understanding and real-time coding suggestions, improving first-pass claim accuracy across large healthcare provider networks.

Computer Assisted Coding Market Key Players are:

-

3M Health Information Systems (3M HIS)

-

Nuance Communications Inc. (Microsoft)

-

Optum Inc.

-

Verisk Health

-

Dolbey Systems Inc.

-

Zynx Health (Hearst Health)

-

Cerner Corporation (Oracle Health)

-

Epic Systems Corporation

-

Nthrive

-

Streamline Health Solutions Inc.

-

Artificial Medical Intelligence (AMI)

-

Iodine Software LLC

-

Aver Analytics

-

Vitalware (Strata Decision Technology)

-

Solarity (Solarity Healthcare)

-

Conifer Health Solutions

-

R1 RCM Inc.

-

Apixio Inc.

-

Coding Strategies Inc.

-

TrustHCS

Computer Assisted Coding Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 6.03 Billion |

| Market Size by 2035 | USD 18.91 Billion |

| CAGR | CAGR of 12.51% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product & Service (Computer-Assisted Coding Solutions/Software, Computer-Assisted Coding Services/Implementation & Support) • By Mode of Delivery (Cloud-Based CAC, Web-Based CAC, On-Premise CAC) • By Application (Inpatient Coding, Outpatient Coding, Physician/Professional Fee Coding) • By End User (Providers/Hospitals & Clinics, Payers/Insurance Companies & Health Plans, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | 3M Health Information Systems (3M HIS), Nuance Communications Inc. (Microsoft), Optum Inc., Verisk Health, Dolbey Systems Inc., Zynx Health (Hearst Health), Cerner Corporation (Oracle Health), Epic Systems Corporation, nThrive, Streamline Health Solutions Inc., Artificial Medical Intelligence (AMI), Iodine Software LLC, Aver Analytics, Vitalware (Strata Decision Technology), Solarity Healthcare, Conifer Health Solutions, R1 RCM Inc., Apixio Inc., Coding Strategies Inc., TrustHCS |

Frequently Asked Questions

The Computer Assisted Coding Market is expected to grow at a CAGR of 12.15% from 2026 to 2035.

The Computer Assisted Coding Market was valued at USD 6.03 Billion in 2025.

Computer-Assisted Coding Services is expected to be the fastest growing segment.

The Payers segment is anticipated to register the fastest CAGR.

Get in Touch