Online Dating Application Market Report Scope & Overview:

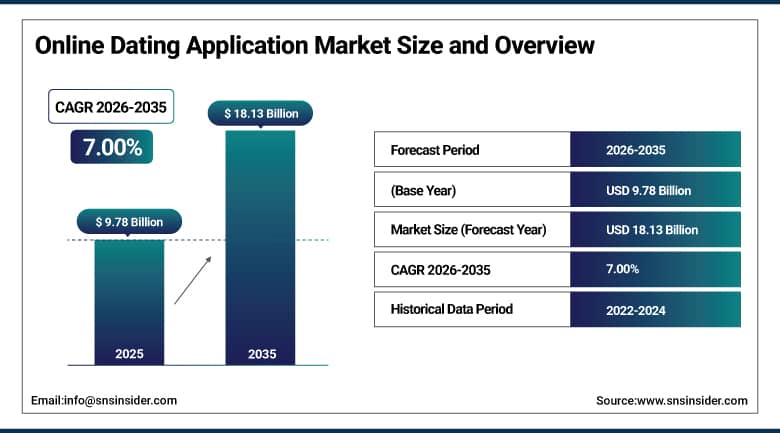

The Online Dating Application Market was valued at USD 9.78 Billion in 2025 and is expected to reach USD 18.13 Billion by 2035, growing at a CAGR of 7.00% from 2026 to 2035.

The report contains detailed insights regarding engagement factors, such as usage metrics, cultural and language preferences, algorithm effectiveness, psychographics and sentiment trends, safety and moderation statistics, unmatching and ghosting behavior. The market for online dating applications shows strong growth, caused by high level of smartphone penetration, changing social norms and AI-based matchmaking. Personalization using psychographics and sentiment analysis are among the main priorities of platforms, along with safety and cultural compatibility issues and moderation solutions. Increased engagement rates, multiple languages and algorithm effectiveness lead to high levels of customer satisfaction. Unmatching and ghosting behavior is also an important trend.

In 2024, Bumble Inc. expanded its safety verification features with enhanced photo verification and identity confirmation tools designed to reduce fake profile prevalence and increase user trust on the platform. The feature expansion addresses one of the most persistent commercial challenges facing dating application operators, where unverified user accounts and fraudulent profiles undermine platform credibility and discourage sustained engagement among users seeking genuine romantic connections through digital matchmaking services.

Market Size and Forecast

-

Market Size in 2026E: USD 10.46 Billion

-

Market Size by 2035: USD 18.13 Billion

-

CAGR: 7.00% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Online Dating Application Market - Request Free Sample Report

Online Dating Application Market Trends

-

Rising smartphone penetration and internet access globally are boosting user engagement on online dating platforms across all age groups, particularly in emerging economies where mobile data affordability continues to improve.

-

Increasing integration of artificial intelligence and machine learning technologies is revolutionizing matchmaking accuracy, with smart algorithms analyzing user behavior patterns, preferences, and usage to provide more precise matches and enhance user satisfaction.

-

Growing adoption of safety verification tools, including photo verification and identity confirmation features, is addressing user concerns about fake profiles and online scams that have historically damaged platform credibility.

-

Expansion of niche dating platforms catering to specific interests, communities, and demographic groups continues to fuel sustained market demand beyond mainstream general purpose dating applications.

-

Integration of voice and video AI features to simulate real conversations prior to in person meetings is improving user confidence and compatibility assessment before users commit to physical encounters.

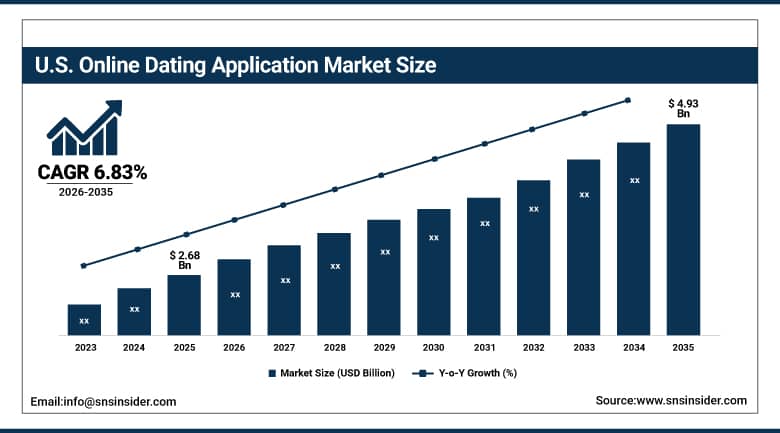

U.S. Online Dating Application Market Outlook

The U.S. Online Dating Application Market was valued at approximately USD 2.68 Billion in 2025 and is expected to reach approximately USD 4.93 Billion by 2035, growing at a CAGR of approximately 6.83%.

This market growth has been influenced by rising digital connectivity, changing attitudes of society towards virtual connections, and the trend towards mobile first interaction. The incorporation of algorithms driven by artificial intelligence for matching purposes has led to increased compatibility results, while security features, user authentication, and support for various genders have increased popularity. The U.S. market also has several other factors, including favorable cultural acceptance, high smartphone adoption, and growing popularity among Generation Z and millennials, with their preference for convenience and personalized experience in dating. Furthermore, the development of more niche platforms targeting particular segments contributes significantly to maintaining stable market demand.

Match Group released advanced AI enabled features of compatibility in all of its dating applications in 2023, which involved the analysis of behavioral patterns for the purposes of better matching recommendations. It shows that the company remains committed to differentiating itself from competitors through its algorithms, since better matchmaking outcomes help maintain user retention in the market characterized by low switching cost and high churn rate.

Online Dating Application Market Segment Analysis

-

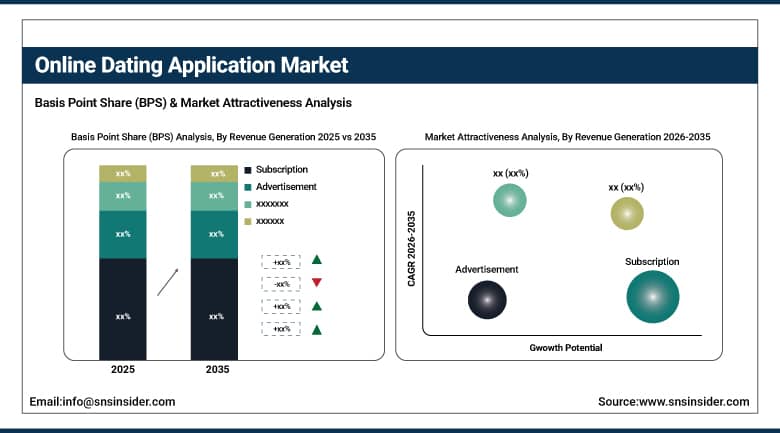

By Revenue Generation, the Subscription segment dominated the Online Dating Application Market with a 72% revenue share in 2025, and is forecasted to grow at the fastest CAGR of 8.07% through 2035.

-

By Age, the 18 to 25 Years segment dominated the Online Dating Application Market with the highest revenue share of about 40% in 2025, while older age segments continue to expand.

-

By Gender, the Male segment led the Online Dating Application Market with the highest revenue market share of nearly 64% in 2025, while the Female segment is anticipated to grow at the fastest CAGR of around 7.96%.

By Revenue Generation, subscription dominates and remains fastest growing

The subscription business model maintained its position as the leading business model, accounting for 72% of the online dating application market revenue in 2025. The dominance of the business model is supported by the desire of the consumers to have features like unlimited swipes, boosts, and premium matchmaking. The revenue from recurring payments is boosted by the incorporation of paywalls to access premium features, and tiered subscription models, with the consumers being more conscious about the returns on their investment of time for more effective and quality dates through the subscription model. Every business model of an online dating application offering premium matchmaking, unlimited interaction, and improved visibility for paid subscribers is a recurring revenue structure whose commercial certainty keeps the subscription business model dominant.

The subscription segment is also forecasted to grow at the fastest CAGR of 8.07 percent through 2035, sustaining its position as both the largest and fastest growing revenue generation category. Each new tiered subscription plan introduced by major platforms, whether offering basic, premium, or platinum membership levels, creates additional monetization granularity that captures varying willingness to pay across the user base. The advertisement segment continues to provide complementary revenue, particularly for free to use platforms whose business model relies on user volume and engagement metrics rather than direct subscription conversion.

By Age, 18 to 25 years dominates user engagement

The age group of 18 to 25 years accounted for the highest revenue share of around 40% in the online dating applications market in 2025 due to extensive use of smartphones, social media, and openness towards digitization. The younger generation is more aware of mobile-first interfaces and considers dating applications as a part of social interaction norms. This age group is characterized by high engagement rate and tends to use different platforms at the same time along with using dating applications as an integral part of their digital communication process. Every college student and young professional whose social world is becoming digital adds to the structured engagement process of this age group.

The 26 to 34 years and 35 to 50 years segments collectively represent substantial and growing user populations whose higher disposable income often translates into above average per user subscription spending despite lower overall engagement frequency relative to the youngest user cohort. Each older user whose career stability and financial capacity support premium subscription investment creates per capita revenue that partially offsets the lower volume engagement characteristic of these demographic segments, sustaining diversified age-based revenue contribution across the platform ecosystem.

By Gender, male dominates revenue, female grows fastest

The male category was dominant in the online dating app market, generating a revenue market share of almost 64% in 2025 owing to their higher level of activity and preference for paying for quality features. It is usually the case with men that they are more active in connecting with other people on dating websites, thus generating a higher rate of subscriptions and activity. Moreover, dating websites usually encourage likes and offer features that are preferred by male users who need high visibility, and such actions contribute towards higher revenue generation.

The female segment is anticipated to grow at the fastest CAGR of around 7.96% during the forecast period as a result of growing digital literacy, enhanced online security features, and societal norm changes. Women are increasingly engaging with online dating, supported by enhanced verification systems and women focused app interfaces. Apps that enable women to initiate conversations and take charge of interactions are promoting greater uptake and usage among women users in urban and semi urban regions, with safety focused product development creating particular appeal for this accelerating user segment.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

31.2% |

|

Latin America |

Brazil |

44.2% |

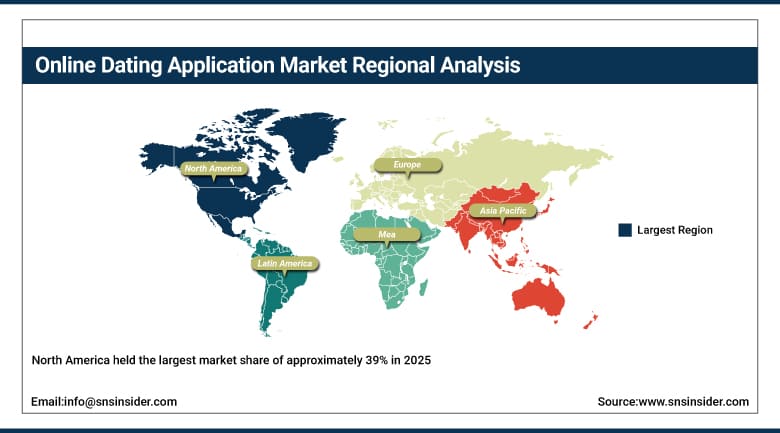

North America Online Dating Application Market Insights

North America held the largest market share of approximately 39% in 2025, as a result of the early adoption of online dating platforms and a high monetization of user base. It boasts excellent smartphone and internet penetration and cultural acceptance of meeting online. The good subscription revenues and steady uptake of premium features are powered by disposable income and a well developed user base on the ground in North America, keeping the region as the undeniable sector leader. The United States accounts for approximately 87.4% of North American revenues through Match Group, Bumble, and Grindr's commercial operations.

Canada contributes complementary North American revenue through its growing dating application user base and increasing smartphone penetration supporting consistent regional engagement across both subscription and advertisement revenue channels.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Online Dating Application Market Insights

Europe holds a significant market share supported by well developed countries such as Germany, the United Kingdom, and France whose strong presence of young population and online dating platforms sustains consistent regional demand. Germany accounts for approximately 22.3% of European revenues through its strong digital infrastructure and high smartphone penetration among the country's dating application user base.

The United Kingdom and France are significant secondary markets where higher gross domestic product, per capita income, and per capita spending on online dating platforms collectively result in a strong user base and increased adoption of online dating portals and applications across the region. Major global platforms maintain substantial commercial operations serving these established European markets.

Asia Pacific Online Dating Application Market Insights

The Asia Pacific region is expected to record the highest CAGR of around 8.78% from 2026 to 2035, due to swift digitalization, youth dominated population, and increasing willingness for online dating. The growth in the region is primarily driven by the large single population in the region and the growing purchasing power of consumers. China accounts for approximately 44.8% of Asia Pacific revenues through its extraordinary digital economy scale and growing acceptance of digital matchmaking among the country's young urban population.

India represents a particularly dynamic emerging market within Asia Pacific where growing trends of online dating coupled with changing lifestyles continue driving market growth in the region, with China and India together holding the majority share within Asia Pacific through their combined large population base and accelerating smartphone adoption.

MEA & Latin America Online Dating Application Market Insights

UAE is at the forefront of MEA revenues with the increasing use of technology and penetration of smartphones that help enhance the use of online dating application among its younger, wealthy and technologically advanced population. The developing digital economy and youthful demographic profile in Saudi Arabia make up for complementary demand in the region in the Gulf countries. Brazil is leading in revenues for Latin America with its large population base and the increasing use of digital dating applications among its urban population.

Market Dynamics

Growth Drivers: Rising smartphone penetration and AI driven matchmaking innovation

Growing smartphone penetration and greater internet accessibility are making a huge difference in the manner in which people interact, particularly in emerging economies. With increasing affordability of smartphones and mobile data plans becoming cheaper, more people are using digital platforms for romantic and social engagement. This extensive online presence has given rise to a huge user base, boosting app downloads and usage levels. Online dating applications use geolocation and AI algorithms, providing customized experiences that further draw users in. The convenience and anonymity provided by these platforms strongly appeal to millennials and Gen Z, who prefer digital first interactions.

As urban life gets more hectic, people look for fast and easy means of approaching potential partners, and these apps offer them readily. This rise in connectivity is increasingly becoming a driving force in market growth. Growing adoption of artificial intelligence and machine learning is revolutionizing user experience on online dating apps, generating significant market opportunities as AI inspects user behavior patterns, choices, and usage to provide more precise matches, enhancing success rates and user satisfaction across the platform ecosystem.

Restraints: Prevalence of fake profiles and online scams undermining trust

Spread of fake profiles, frauds, and scams in dating websites is diminishing user confidence and hampering market expansion. In most cases, users come across some form of deception, bots, or people with vested interests leading to detrimental consequences. Romance frauds are common where individuals manipulate users in order to extract either financial gains or confidential information from them. Not only does this discourage such users, but also warns other users about the potential risks involved, and thus hinders their regular engagement with the website.

Differentiating real users from fraudsters puts a lot of pressure on the website’s moderation process. While artificial intelligence verification systems keep getting better and better, there is still scope for improvement. This lack of perfection not only discourages regular users but also hampers their engagement with the platform, especially in regions that lack digital literacy skills and awareness against frauds.

Opportunities: AI integration and niche platform expansion

Growing adoption of artificial intelligence and machine learning is revolutionizing user experience on online dating apps, generating substantial market opportunities. AI and machine learning inspect user behavior patterns, choices, and usage to provide more precise matches, enhancing success rates and user satisfaction. AI also facilitates filtering out objectionable content, detecting fake profiles, and individualized communication recommendations. Smart matching algorithms, behavior analytics, and sentiment detection enabled platforms achieve competitive advantage by driving user engagement.

With users wanting more personalized experiences, apps leveraging AI to provide compatibility insights or interactive features such as chatbots are becoming popular. Voice and video AI are also being used to simulate real conversations prior to meetings, creating commercial opportunity for platforms capable of demonstrating measurable improvement in match quality and user satisfaction outcomes. This technology based innovation offers a pathway to improve the overall quality of online dating and increase the addressable market across both developed and emerging regional markets.

Recent Developments:

-

2024: Bumble Inc. expanded its safety verification features in 2024 with enhanced photo verification and identity confirmation tools designed to reduce fake profile prevalence and increase user trust on the platform.

-

2023: Match Group launched enhanced AI powered compatibility features across its portfolio of dating applications in 2023, incorporating behavioral pattern analysis to improve match recommendation accuracy.

-

2024: Grindr LLC introduced enhanced safety and content moderation tools in 2024, addressing user requests for improved platform security and reduced exposure to inappropriate content during platform interactions.

-

2023: Hinge expanded its prompt based profile feature set in 2023, allowing users to share more personality driven content designed to facilitate more meaningful initial conversations between matched users.

-

2024: eHarmony, Inc. updated its compatibility matching algorithm in 2024, incorporating additional behavioral and psychographic data points to improve long term relationship outcome predictions for subscribers.

Online Dating Application Market Key Players

-

Match Group Inc. (Tinder)

-

Bumble Inc.

-

Grindr LLC

-

eHarmony Inc.

-

Plentyoffish Media ULC

-

Badoo (Bumble Inc.)

-

OkCupid (Match Group)

-

Hinge Inc. (Match Group)

-

Zoosk Inc.

-

The Meet Group Inc.

-

Spark Networks SE

-

Coffee Meets Bagel Inc.

-

The League App Inc.

-

Happn SAS

-

Cupid Media Pty Ltd.

-

rsvp.com.au Pty Ltd.

-

Hily Inc.

-

Tantan (MoMo Inc.)

-

Lunar Dating Inc.

-

Once Dating Inc.

Online Dating Application Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 9.78 Billion |

| Market Size by 2035 | USD 18.13 Billion |

| CAGR | CAGR of 7.00% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Revenue Generation (Subscription, Advertisement) • by Age (18 to 25 Years, 26 to 34 Years, 35 to 50 Years, Above 50 Years) • by Gender (Male, Female) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Match Group Inc. (Tinder), Bumble Inc., Grindr LLC, eHarmony Inc., Plentyoffish Media ULC, Badoo (Bumble Inc.), OkCupid (Match Group), Hinge Inc. (Match Group), Zoosk Inc., The Meet Group Inc., Spark Networks SE, Coffee Meets Bagel Inc., The League App Inc., Happn SAS, Cupid Media Pty Ltd., rsvp.com.au Pty Ltd., Hily Inc., Tantan (MoMo Inc.), Lunar Dating Inc., Once Dating Inc. |

Frequently Asked Questions

The Subscription segment dominated the Online Dating Application Market with a 72% revenue share in 2025 and is also forecasted to grow at the fastest CAGR of 8.07% through 2035.

North America held the largest market share of approximately 39% in 2025, while Asia Pacific is expected to record the highest CAGR of around 8.78% through 2035.

The Online Dating Application Market was valued at USD 9.78 Billion in 2025.

Rising smartphone penetration and greater internet accessibility making digital romantic engagement increasingly accessible, particularly in emerging economies, and growing adoption of artificial intelligence and machine learning technologies that improve matchmaking accuracy and enhance user satisfaction across platforms.

The Online Dating Application Market is expected to grow at a CAGR of 7.00% from 2026 to 2035.

Get in Touch