Content Intelligence Market Report Scope & Overview:

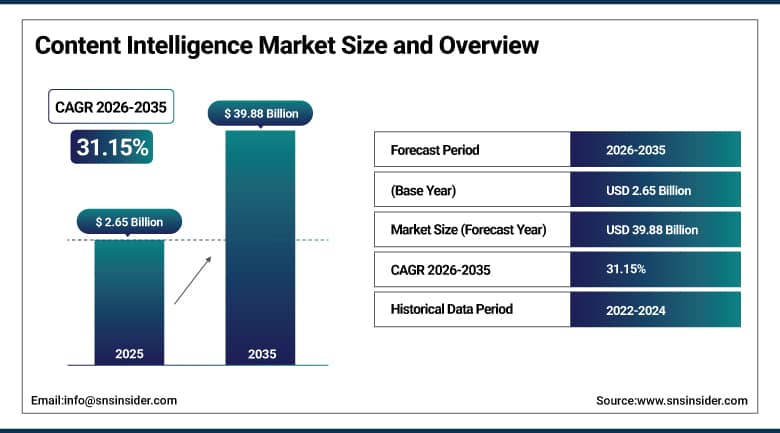

The Content Intelligence Market was valued at USD 2.65 Billion in 2025 and is expected to reach USD 39.88 Billion by 2035, growing at a CAGR of 31.15% from 2026–2035.

Content intelligence platforms take the flood of blogs, videos, social posts, and other digital content that organizations now produce and turn it into structured insight. Traditional content management systems were never built to handle this volume or variety, so businesses are turning to smarter tools that can classify, tag, and monitor content performance automatically, cutting the manual labor involved by a wide margin. As content keeps expanding into new formats, podcasts, AR and VR experiences, interactive video, the need for scalable analysis tools has become impossible to ignore. Organizations are increasingly treating content intelligence as a strategic operational requirement, particularly as remote and distributed teams need better ways to connect with measurable performance data.

At Adobe MAX in October 2025, Adobe announced major innovations in GenStudio, its integrated content supply chain platform, including Firefly Design Intelligence, a new tool that trains custom StyleIDs to codify a brand's design rules for use across Creative Cloud apps. The launch came with a new version of the Firefly Creative Production suite and a Content Production Agent built in GenStudio for Performance Marketing, showing how fast generative AI is evolving from a feature that creates content to a deeply integrated piece of enterprise content operations.

Market Size and Forecast

-

Market Size in 2026E: USD 3.47 Billion

-

Market Size by 2035: USD 39.88 Billion

-

CAGR: 31.15% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Content Intelligence Market - Request Free Sample Report

Content Intelligence Market Trends

-

Generative AI integration is enabling content intelligence platforms to automate content creation, optimization, and performance analysis within unified workflows.

-

Real-time sentiment and audience analytics are helping brands monitor customer engagement and respond quickly across digital communication channels.

-

Growing data privacy regulations are driving adoption of advanced consent management, anonymization, and secure data processing capabilities in content intelligence platforms.

-

Integration with CRM and marketing automation platforms is improving content performance tracking and campaign optimization through connected business insights.

-

User-generated content analytics are helping organizations extract actionable insights from reviews, social media, and online community interactions.

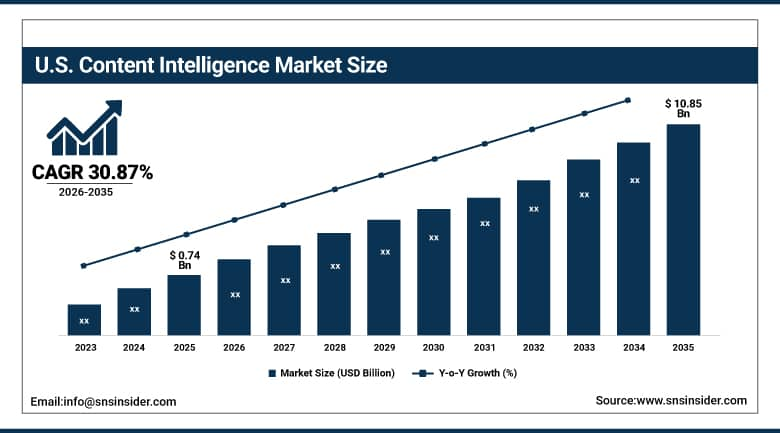

U.S. Content Intelligence Market Outlook

The U.S. content intelligence market was valued at approximately USD 0.74 Billion in 2025 and is expected to reach approximately USD 10.85 Billion by 2035, growing at a CAGR of approximately 30.87%.

Such phenomenal growth is being witnessed due to the growing demand within the corporate sector for content strategies tailored to their data needs. With businesses trying to get maximum engagement and conversion rates, there has been an urgent requirement for implementing artificial intelligence and machine learning into the content processes. Some of the factors which have driven the market to exhibit such high growth include the rise in the adoption of omnichannel marketing approaches, requirement for more precise and faster sentiment analysis of customers, and the need for adherence to new data protection regulations.

An example of this includes M-Files, which has enhanced its partner program with Dyanix in 2024 in relation to its data management and artificial intelligence capabilities in the UK, Benelux, and Spain. This strategy corresponds to a general tendency for content intelligence providers to expand their regional partner networks in order to speed up implementation of localized content management through AI co-creation.

Content Intelligence Market Segment Analysis

-

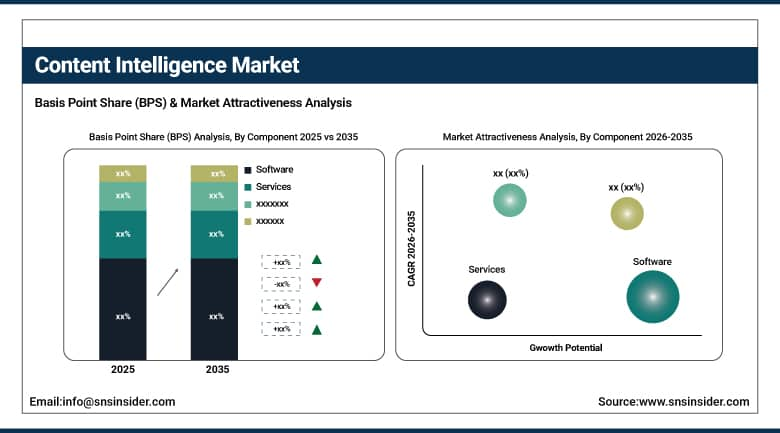

By Component, the software segment dominated the content intelligence market with approximately 71% share in 2025, while the services segment is the fastest growing with a CAGR of approximately 32.55%.

-

By Enterprise Size, the large enterprises segment dominated the content intelligence market with a 68% revenue share in 2025, while the SME segment is the fastest growing with a CAGR of approximately 32.89%.

-

By Deployment, the cloud segment dominated the content intelligence market with approximately 51% share in 2025, while the hybrid segment is the fastest growing with a CAGR of approximately 33.41%.

-

By End-Use, the media & entertainment segment dominated the content intelligence market with a 25% revenue share in 2025.

By Component, software dominates, services grow fastest

Software dominated the industry with approximately 71% share of revenues in 2025, due to the critical importance of software in delivering scalable and automated solutions for content generation, analysis, and optimization. Companies are making substantial investments in artificial intelligence-powered platforms, which facilitate content production processes, provide real-time performance measurement and analytics, and thanks to their flexibility in integrating into the existing digital architecture, have become an important component of digital transformations.

However, services have been growing at the fastest pace, at a CAGR of approximately 32.55% due to increased demand for customized and implementing services, in addition to consultancy. With businesses increasingly adopting content intelligence solutions, there is increasing demand for guidance from professionals, especially when trying to maximize their returns on investments as well as due to the high rate of adoption of AI tools causing some knowledge gaps.

By Enterprise Size, large enterprises dominate, SMEs grow fastest

Large firms led the market in 2025 with 68% of revenue generated, primarily owing to the advanced content activities and complex data ecosystem of such companies. The firms had enough financial capability and technological expertise to deploy advanced analytics systems, AI platforms, and integration frameworks; and since they had many customers in various digital channels, they needed intelligent solutions to conduct content marketing campaigns effectively.

Small and medium enterprises are currently experiencing a high growth rate, which is expected to be at around 32.89% CAGR as a result of increased availability of low-cost content intelligence software in the clouds. With increased competition, small firms are using AI-based applications in an attempt to optimize their available resources and develop unique messaging capabilities, with cloud-based systems bringing down the costs of setting up such infrastructure.

By Deployment, cloud dominates, hybrid grows fastest

Cloud deployment captured the highest revenue market share in 2025, accounting for around 51%. This was due to the benefits of flexibility, scalability, and ease of deployment associated with the cloud deployment model. Cloud platforms allow real-time collaborations, easy access to data, and easy updates, features that are essential for dynamic content environments. Companies are adopting the cloud deployment model since it helps avoid costs associated with the on-premises deployment model.

However, hybrid deployment is the most rapidly growing type of deployment and is estimated to have a Compound Annual Growth Rate of about 33.41%. It represents a compromise solution for enterprises seeking a balance between data governance and agility. With hybrid deployments, companies can maintain their sensitive data and content within private settings but also leverage cloud computing capabilities.

By End-Use, media & entertainment dominates and grows fastest

The Media and Entertainment sector was the leader in the marketplace in 2025 with its strong 25% revenue share, considering that the sector is based on high volumes of content creation in real time. Content intelligence is now used by streaming service providers, digital publishers, and broadcasting channels in order to gain insights into their audience preferences and optimize the delivery of content.

The industry is always developing with innovative ways of content creation such as interactive videos, podcasts, and even augmented reality and virtual reality. The development is possible thanks to the use of smart content optimization solutions. As the level of competition increases, media enterprises rely on the use of content intelligence in order to achieve maximum value of the content lifecycle, increase monetization efforts, and stay relevant from the creative perspective.

Regional Insights

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

78.0% |

|

Europe |

Germany |

23.0% |

|

Asia Pacific |

China |

39.0% |

|

Middle East & Africa |

UAE |

28.0% |

|

Latin America |

Brazil |

37.0% |

North America Content Intelligence Market Insights

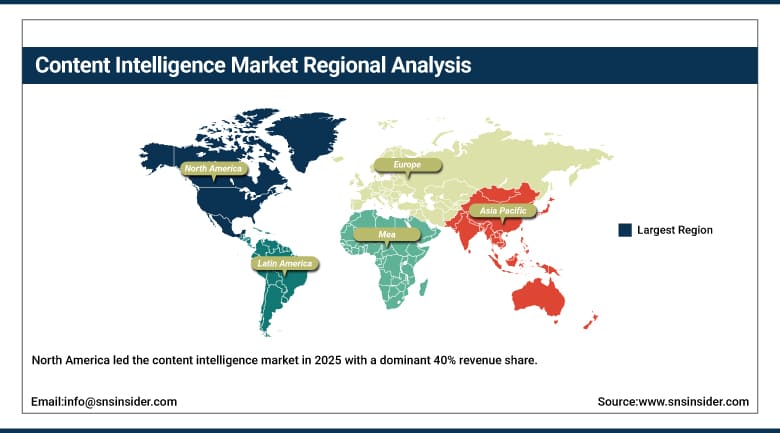

North America led the content intelligence market in 2025 with a dominant 40% revenue share, supported by advanced digital infrastructure, high AI adoption rates, and the presence of leading content intelligence vendors. The use of content intelligence by firms in media, retail, and technology industries in order to distinguish themselves and connect with their consumers better has been spurred by the region's highly developed marketing frameworks and data-based approach.

Supportive regulatory frameworks and deep technical resources give North American firms the means to embed AI into their content operations at scale, and the region's leading vendors continue rolling out their most advanced generative AI features domestically first. This combination of infrastructure, capital, and vendor concentration keeps North America firmly in the lead even as other regions grow faster in percentage terms.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Content Intelligence Market Insights

Europe remains a technically capable content intelligence market, shaped by strict data protection regulation and a strong base of established media and marketing organizations. Germany leads regional demand, drawing on its dense base of enterprise software users and marketing technology adoption across manufacturing, retail, and media sectors.

The United Kingdom and France follow as significant secondary markets, where GDPR compliance requirements have pushed vendors toward content intelligence platforms with stronger built-in governance and consent management capabilities. This regulatory emphasis has, in some ways, made European deployments a proving ground for privacy-conscious content intelligence features that are increasingly valued in markets outside Europe as well.

Asia Pacific Content Intelligence Market Insights

Asia Pacific is projected to register the fastest CAGR in the content intelligence market, at roughly 33.55% through 2035, driven by accelerated digitalization, increasing internet penetration, and rising interest in localized content across diverse markets. China, India, and Southeast Asia are witnessing a content consumption boom, particularly across social and mobile platforms, creating substantial new demand for tools that can make sense of that volume.

The growth in artificial intelligence (AI) spending, the development of e-commerce ecosystems, and the rise of digital-native start-ups are all propelling the uptake of content intelligence in the region. The rise in government-led digitalization efforts and the rising trend toward data-based marketing strategies are all contributing to this explosive growth trajectory for the Asia Pacific market.

MEA & Latin America Content Intelligence Market Insights

Middle East and Africa continue to represent a nascent content intelligence market, spearheaded by the investments that the UAE has made in digital media and marketing technologies in its efforts to create a content and entertainment hub within the region. The same case applies to Saudi Arabia, whose media investments have been on the rise thanks to the economic diversification initiatives in place in the country.

Latin America is seeing steady adoption led by Brazil, where media companies and large retailers are investing in content intelligence to manage growing digital content volumes and improve audience engagement. Mexico follows as the region's second-largest market, supported by a growing digital media sector and rising demand for data-driven marketing across the region's expanding e-commerce industry.

Growth Drivers: Explosion in digital content creation demanding scalable analysis tools

The huge amount of digital content that exists in the realm of websites, social media sites, and mobile devices has become too much for traditional content management systems. Companies require a good solution to sift through large volumes of unstructured data and glean meaningful information from them, and content intelligence can provide automation in this process.

As content becomes richer through media and covers blogs, videos, podcasts, and AR/VR, the need for scalable tools for analysis becomes paramount. With such tools, marketers get an insight into what is working, how and why, and how to duplicate success. As remote working speeds up content creation by making it decentralized, the focus has been on the integration of content creation with analytics.

Restraints: Data privacy concerns and compliance requirements limiting adoption

Since content intelligence solutions base their insights on user data, they raise significant privacy, consent, and data governance concerns. Organizations need to ensure that their processes regarding the handling of data adhere to international laws such as GDPR and CCPA, as well as any other data privacy laws that continue to change, making it costly for organizations to stay compliant.

Failure to manage personal data properly may lead to bad reputation and even legal penalties, and as the customers become more vigilant about data usage, companies need to adopt better anonymization and opt-in measures during the collection process. These measures may limit the level of insights available via content intelligence technologies, and businesses working in multiple territories have difficulty synchronizing processes and thus stall platform implementation.

Opportunities: Generative AI integration opening new frontiers in content creation

The fusion of generative AI and content intelligence is creating opportunities for just-in-time content generation. AI tools such as GPT-based language models and image generators provide marketers the ability to brainstorm and create content according to their audience’s needs, and when used in combination with intelligence platforms, they can even adjust the tone and messaging to fit the analytical data being generated in real time.

This synergy cuts down the content lifecycle considerably and delivers better engagement metrics, while connecting with CRM and martech stacks enables hyper-targeted campaigns that adapt dynamically to various data inputs. As generative AI becomes more accessible, content intelligence is positioned to drive smarter, faster, and more personalized content experiences at scale across every industry that produces content.

Recent Developments:

-

2026: Adobe Inc. expanded its generative AI capabilities across Adobe Experience Cloud, enabling automated content creation, personalization, and performance optimization for enterprise marketing teams.

-

2026: OpenText Corporation introduced enhanced AI-powered content intelligence features within its Information Management Cloud, improving enterprise document classification, semantic search, and compliance automation.

-

2026: Google Cloud launched new generative AI and multimodal content intelligence capabilities through Vertex AI, enabling organizations to analyze, summarize, and optimize large volumes of enterprise content.

-

2026: Acrolinx released advanced AI-driven content governance and quality assurance tools, helping enterprises improve brand consistency, regulatory compliance, and multilingual content optimization across digital channels.

Content Intelligence Market key players are:

-

Adobe Inc.

-

M-Files

-

OpenText Corporation

-

IBM Corporation

-

Google Cloud

-

MarketMuse

-

Acrolinx

-

Salsify

-

BrightEdge

-

ABBYY

-

Optimizely

-

Acquia

-

Siteimprove

-

Coveo

-

Progress Sitefinity

-

Messagepoint Inc.

-

Scoop.it

-

Sinequa

Content Intelligence Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.65 Billion |

| Market Size by 2035 | USD 39.88 Billion |

| CAGR | CAGR of 31.15% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Software, Services) • By Deployment (Cloud, On-premises, Hybrid) • By Enterprise Size (Large Enterprises, SMEs) • By End-Use (BFSI, IT & Telecommunication, Media & Entertainment, Retail & Consumer Goods, Travel & Hospitality, Government & Public Sector, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Adobe Inc., M-Files, OpenText Corporation, IBM Corporation, Google Cloud, ChapsVision, MarketMuse, Acrolinx, Salsify, BrightEdge, ABBYY, Optimizely, Emplifi, Acquia, Siteimprove, Coveo, Progress Sitefinity, Messagepoint Inc., Scoop.it, Sinequa |

Frequently Asked Questions

North America dominated the Content Intelligence Market in 2025 with a 40% market share.

The Content Intelligence Market is expected to grow at a CAGR of 31.15% from 2026 to 2035.

The Content Intelligence Market was valued at USD 2.65 Billion in 2025.

The explosion in digital content creation across platforms and formats, which requires scalable tools to manage and derive insights from unstructured data at scale.

Software dominated with approximately 71% share in 2025.

Get in Touch