Continuous Positive Airway Pressure Cleaning Devices Market Report Scope & Overview:

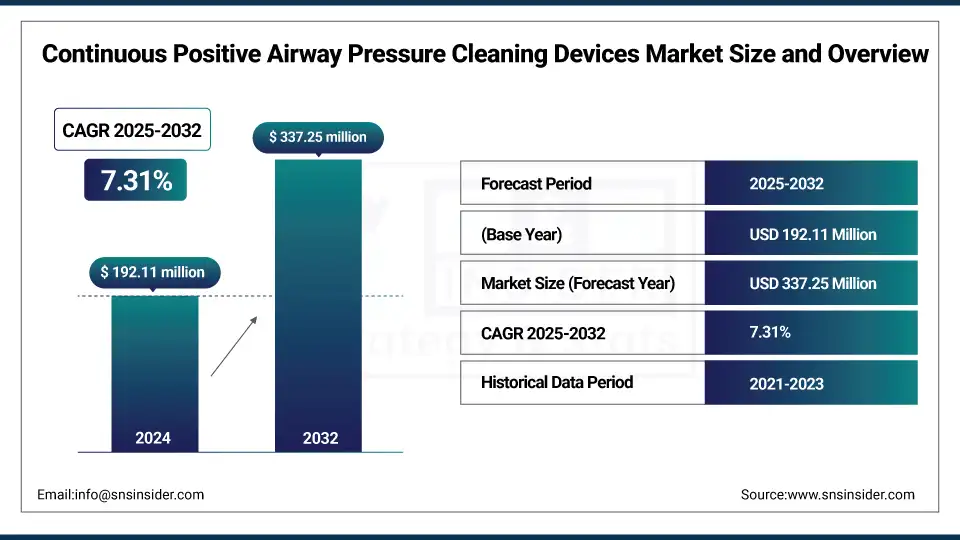

The Continuous Positive Airway Pressure Cleaning Devices Market size was valued at USD 192.11 million in 2024 and is expected to reach USD 337.25 million by 2032, growing at a CAGR of 7.31% over 2025-2032.

The global continuous positive airway pressure cleaning devices market is witnessing strong demand across the world on account of the increasing prevalence of obstructive sleep apnea globally, affecting more than 900 million people. Growing awareness of respiratory hygiene, particularly among geriatric populations and home-care patients, is supporting the demand for automated CPAP cleaning devices. The market is characterised by strong supply-side momentum from technology advancements in disinfection technologies (such as UV light and activated oxygen/ozone), which are being developed for domestic/consumer applications.

For instance, regulatory authorities have increased their focus on unlisted ozone-based CPAP cleaners, urging manufacturers to shift towards safer and regulatory-compliant technologies that propel the continuous positive airway pressure cleaning devices market globally.

To Get more information On Continuous Positive Airway Pressure Cleaning Devices Market - Request Free Sample Report

Increasing healthcare investments and spending on R&D by major companies are driving the development of smart, user-friendly, safe devices with high efficacy to eliminate pathogens. Strong regulatory edicts and expanded CPAP hygiene restrictions are prompting manufacturers to focus on the safety and efficacy of device development, that are also boosting patient confidence. Increasing reimbursement coverage and increasing awareness of CPAP adherence & device maintenance are anticipated to drive the continuous positive airway pressure cleaning devices market growth.

In 2024, next-generation CPAP cleaners featuring internal sensors and automated cycle tracking were introduced, increasing the efficiency and convenience of devices available on the market but also indicating a direction towards more intelligent disinfection options.

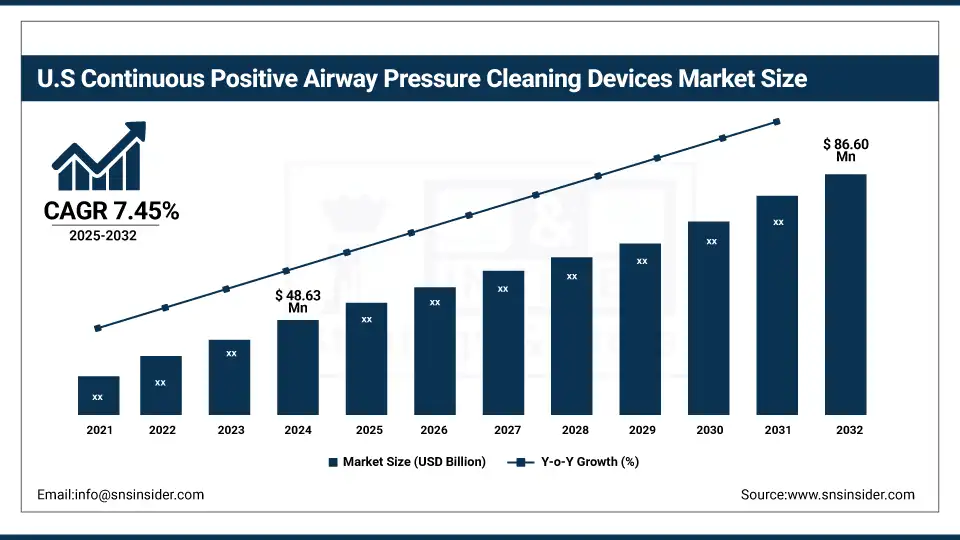

The U.S. continuous positive airway pressure cleaning devices market size was valued at USD 48.63 million in 2024 and is expected to reach USD 86.60 million by 2032, growing at a CAGR of 7.45% over 2025-2032. In 2024, the U.S. led the North American market and accounted for more than 78% share in North America on account of high usage of CPAP devices coupled with easy availability of automated cleaners, along with growing awareness among consumers related to device cleanliness. Dominant players and the FDA’s focus on cleanliness-related safety also further accelerate product conversion. In 2024, Canada became the fastest-growing country in the region due to an increase in rates of OSA diagnosis, a higher penetration by CPAP, and the development of e-commerce for home respiratory care.

Continuous Positive Airway Pressure Cleaning Devices Market Dynamics

Drivers:

-

Increasing Sleep Apnea Burden, Tech Upgrades, and Healthcare Investments Accelerating the Growth of the Market

The continuous positive airway pressure cleaning devices market is primarily driven by the growing adoption of home care therapeutic devices and a higher requirement for clean CPAP machines with increasing compliance. More than 70% of CPAP users admit that they don’t clean their CPAP masks regularly, which potentially exposes them to viruses and bacteria and can make it difficult for the mask to fully adhere during sleep. This is making way for automated solutions. Increased awareness of health-conscious behavior and proliferation of device-associated infections (e.g., bacterial pneumonia or sinusitis originating from unclean CPAP tubing) are responsible for increasing the usage of devices such as these.

On the supply end, a lot of R&D spending by manufacturers SoClean and 3B Medical is putting mobile app connections, IoT for better tracking of hygiene, and device diagnostics. These pressures from regulatory changes (e.g., more stringent sanitation guidance by sleep organizations and DME accreditation criteria) are forcing hospitals and retailers to recommend approved, safe cleaning systems. Moreover, increasing insurance reimbursement for CPAP-related supplies is lowering the patient cost burden and driving equipment replacement and cleaning. Rising prevalence in recent years of patients suffering from chronic obstructive pulmonary disease (COPD) and central sleep apnea is also driving the market for reliable, completely automated CPAP maintenance solutions, justifying the long-term, continuous positive airway pressure cleaning devices market analysis and R&D investment.

Restraints:

-

Safety Controversies, Regulatory Scrutiny, and Limited Clinical Validation Challenges Limiting Market Growth

The continuous positive airway pressure cleaning devices market share growth may be restricted due to numerous challenges. A significant concern is the safety and effectiveness of ozone- or UV-based cleaning technologies. The US FDA had repeatedly warned about the danger of such devices in 2020, and for that reason, consumer confidence was affected due to possible risk exposure while their cards were not validated. Most available devices are not adequately clinically endorsed, or published data that they exert meaningful in vitro efficacy to recommend them to physicians.

In addition, high device prices (USD 250–USD 400) inhibit purchase in lower-income and uninsured populations. Some insurers have even removed CPAP cleaners from lists of devices. More, product recalls because of safety issues (e.g., ozone leakage and insufficient sterilization) also postpone the entry into markets as well as brand reliability. Regulatory constraints on the approval of sanitation devices, especially those for home use, are a drag on innovation pipelines as developers face increased testing and documentation costs. The market is influenced as well by counterfeit or non-FDA-cleared import products offered online, which undermine customer confidence in safe devices. These factors together reduce the continuous positive airway pressure cleaning devices market growth, especially in regions where stringent regulatory requirements are currently unmet and a limited number of DME providers service a vast population.

Continuous Positive Airway Pressure Cleaning Devices Market Segmentation Analysis:

By Product Type

In 2024, automated CPAP cleaning devices occupied the largest market share at around 42.7%, attributed to their ease of use with low user involvement and time efficiency, which is favorable for the elderly population or people with restricted movement during sleep & need devices cleaning regularly. They are also compatible with the majority of CPAP models for wider adoption rates across different user types.

Hybrid cleaners (UV + Ozone) are the fastest growing, propelled by consumer preference for a double-layer disinfection guarantee. These devices provide better germ-kill rates and eliminate doubt about one-method cleaners, especially in post-pandemic hygiene-sensitive homes.

By Distribution Channel

Online retail held a dominant share of 39.5% in the same year, on account ease associated with it and a wide variety of products offered along with discounts by e-commerce platforms (e.g., Amazon) & direct brand websites. Consumer trust in online reviews and digital health product trends has also helped to drive the channel.

Direct-to-consumer (DTC) channels are becoming increasingly formidable, driven by brand-affiliated personalized conversational offerings, including value-added bundled offers with CPAP machines and filter/refill subscription services designed to maintain ongoing customer relationships.

By Technology

Ozone-based disinfection technology was the largest contributor with a market share of 36.2% in 2024. Despite FDA attention, the plug-and-play simplicity of this small retrofitting unit, along with its huge installed user base, guaranteed it remained ubiquitous - particularly in areas that struggled to enforce regulation.

Dual (Ozone + UV-C) technology has taken the market by storm, with users wanting hospital-grade disinfection in their homes. Manufacturers are introducing small hybrid models aimed at tech-savvy consumers worried about airborne pathogens and mold in CPAP tubing.

By End Use

Home care settings held the dominant position with 47.9% and have respiratory mask installations due to the global trend toward home care respiratory care shift & increasing CPAP compliance. Huge focus on personal hygiene and avoiding infections in the wake of COVID-19 has made home cleaning products a necessity.

Hospitals & sleep clinics are growing the fastest as clinics implement CPAP cleaners for infection control compliance and reuse protocols. These organizations are purchasing industrial-strength or multi-device compatible cleaners (for outpatient services and diagnostic labs).

Regional Insights:

North America held a considerable portion of the market for CPAP cleaning devices, owing to the high prevalence of OSA, a favorable reimbursement scenario, and a well-established home healthcare industry in this region.

Get Customized Report as per Your Business Requirement - Enquiry Now

The Asia Pacific is growing steadily on account of the higher diagnosis for sleep disorders, accelerating healthcare expenditure, and expanding a digital-based retail network. China was the largest regional market in 2024, accounting for more than 35% of revenue share on account of high CPAP adoption along with technological advancement and the establishment of sleep labs across urban areas. India was projected to be the fastest expanding nation in the region, driven by a rising urban population, higher incidence of OSA (including an estimated 22% prevalence amongst adults), as well as increased demand for affordable UV and manual cleaning add-ons.

Continuous Positive Airway Pressure Cleaning Devices Market Key Players:

Notable companies offering continuous positive airway pressure cleaning devices include SoClean Inc., MedView Systems, Hammacher Schlemmer, SaniBot, CleanFlash, Shenzhen Yimi Care Co., Ltd., VirtuCLEAN, React Health, 3B Medical, RedSky Medical, Lofta, LIVILITI Health Products, Sinoriko, Snorflex, Sper Scientific Direct, Proline Medical, Sleep8 Inc., Lumin, Purify 03, and MVAP Medical Supplies.

Recent Developments:

In August 2024, the FDA granted De Novo clearance to SoClean’s SoClean 3+ device, making it the first-ever FDA-cleared home-use bacterial reduction system for compatible CPAP hoses and masks, offering 99.9% bacterial reduction and elevating regulatory trust in the category.

In November 2023, SoClean issued a voluntary recall for SoClean 2 and 3 models, introducing updated user manuals and ozone-sealing adapters to enhance user safety and reduce residual ozone exposure aligned with FDA safety guidance on ozone-based CPAP devices.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 192.11 million |

| Market Size by 2032 | USD 337.25 million |

| CAGR | CAGR of 7.31% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Automated CPAP Cleaning Devices, Ozone-Based CPAP Cleaners, UV-Light CPAP Cleaners, Hybrid Cleaners (UV + Ozone), and Manual Cleaning Accessories (Cleaning Brushes & Tube Rinses, Cleaning Wipes & Disinfectant Sprays, Cleaning Tablets & Soaking Solutions)) • By Distribution Channel (Online Retail (eCommerce platforms, brand websites), Offline Retail (Pharmacies, Medical Supply Stores), Direct-to-Consumer (DTC) Channels, DME Distributors & Suppliers) • By Technology (Ozone-Based Disinfection Technology, UV-C Light Disinfection Technology, Dual (Ozone + UV-C) Technology, Heat or Steam-Based Cleaning) • By End Use (Home Care Settings, Hospitals & Sleep Clinics, Durable Medical Equipment (DME) Providers, and Others (Long-term Care Centers, Rehabilitation Facilities, Assisted Living Facilities)) |

| Regional Analysis/Coverage | North America (U.S., Canada), Europe (Germany, France, UK, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America) |

| Company Profiles | SoClean Inc., MedView Systems, Hammacher Schlemmer, SaniBot, CleanFlash, Shenzhen Yimi Care Co., Ltd., VirtuCLEAN, React Health, 3B Medical, RedSky Medical, Lofta, LIVILITI Health Products, Sinoriko, Snorflex, Sper Scientific Direct, Proline Medical, Sleep8 Inc., Lumin, Purify 03, and MVAP Medical Supplies. |

Frequently Asked Questions

Ans: Rising sleep apnea cases are expanding the installed base of CPAP users, directly increasing demand for easy-to-use, automated cleaning solutions to ensure device hygiene.

Ans: Key trends include portable and travel-friendly devices, smartphone connectivity, and a shift toward ozone- and UV-free disinfection methods due to safety concerns.

Ans: Key players include SoClean Inc., 3B Medical, VirtuOx, Sleep8, and Liviliti Health Products, offering UV and ozone-based cleaning technologies.

Ans: North America leads due to a large CPAP user base and high sleep apnea prevalence, followed by Europe and Asia Pacific with growing awareness and device adoption.

Ans: As of 2024, the global CPAP cleaning devices market is valued at USD 192.11 million, driven by rising sleep apnea diagnoses and device hygiene awareness.

Get in Touch