Ovarian Cancer Diagnostics Market Report Scope & Overview:

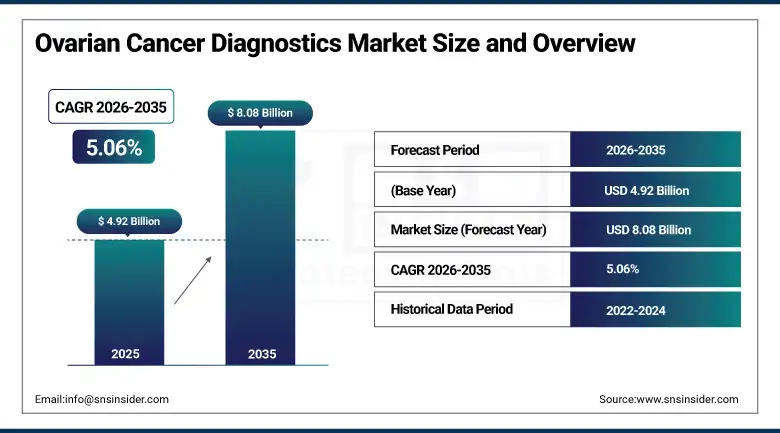

The Ovarian Cancer Diagnostics Market was valued at USD 4.92 Billion in 2025 and is expected to reach USD 8.08 Billion by 2035, growing at a CAGR of 5.06% from 2026–2035.

Global Ovarian Cancer Diagnostic Services Market is seeing continuous growth owing to the growing incidences and prevalence of ovarian cancer around the world, which calls for proper and better diagnoses of the same. The employment of advanced technologies such as imagery using artificial intelligence, liquid biopsies, and next generation sequencing is adding to the efficacy of the diagnostic process right from the initial stages. The increase in awareness about the diseases coupled with the presence of advanced healthcare infrastructure across the globe, in addition to substantial research funding from bodies like NIH and OCRA, is aiding market growth.

In January 2025, researchers at Karolinska Institutet, Sweden, demonstrated that AI-driven neural networks can surpass human experts in detecting ovarian cancer from ultrasound images. The study, published in Nature Medicine, highlights the potential of AI in enhancing early diagnosis and improving patient survival outcomes by enabling detection at earlier and more treatable stages of the disease, representing the clinical direction of ovarian cancer diagnostics development toward AI-assisted precision screening whose accuracy and scalability advantages sustain premium adoption across developed healthcare markets.

Market Size and Forecast

-

Market Size in 2026E: USD 5.17 Billion

-

Market Size by 2035: USD 8.08 Billion

-

CAGR: 5.06% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Ovarian Cancer Diagnostics Market - Request Free Sample Report

Ovarian Cancer Diagnostics Market Trends

-

AI-powered imaging and neural network diagnostics are advancing early-stage ovarian cancer detection beyond conventional human expert capability.

-

Liquid biopsy technologies are enabling real-time, minimally invasive monitoring of cancer progression and treatment response through blood-based biomarker analysis.

-

Next-generation sequencing (NGS) and multi-panel biomarker platforms are improving diagnostic precision and enabling personalized treatment pathway identification.

-

Home diagnostic solutions and telemedicine-integrated testing services are expanding accessibility for rural and underserved patient populations globally.

-

Government-funded early detection programs in North America, Europe, and Asia Pacific are accelerating adoption of advanced screening technologies across healthcare systems.

U.S. Ovarian Cancer Diagnostics Market Outlook

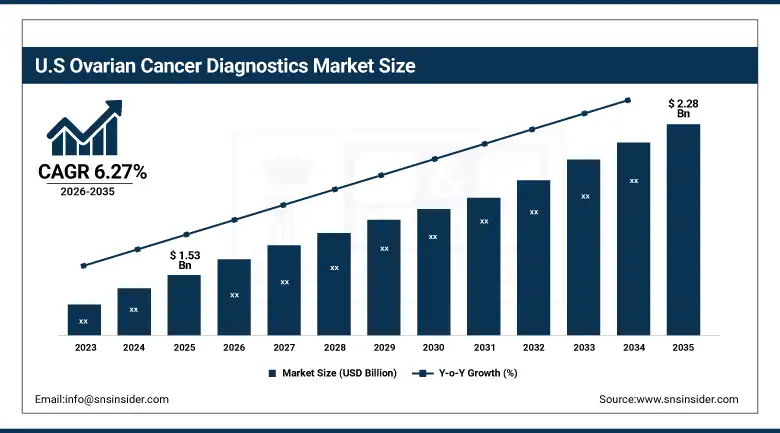

The U.S. Ovarian Cancer Diagnostics Market was valued at approximately USD 1.53 Billion in 2025 and is expected to reach approximately USD 2.28 Billion by 2035, growing at a CAGR of approximately 6.27%.

The United States is the most commercially significant ovarian cancer diagnostics market within the largest North American region. Growing federal investments in cancer research through the NCI and NIH, expansion of early screening initiatives, broadening insurance coverage for advanced diagnostic procedures, and continued FDA regulatory backing accelerating approval of new testing technologies collectively sustain the U.S. market’s above-average per-unit commercial value and above-CAGR growth trajectory. Key players including Myriad Genetics, Quest Diagnostics, Roche, and Abbott’s U.S. commercial operations serve the domestic hospital laboratory, cancer diagnostic center, and research institute end-use channels.

In July 2024, Mayo Clinic researchers identified a distinct ovarian cancer microbiome that may aid in early detection and predicting treatment response. Published in Scientific Reports, this discovery could enhance efforts to diagnose ovarian cancer at a more treatable stage and assess patient outcomes, representing the direction of precision diagnostic development whose biomarker innovation creates new early-stage detection capability sustaining premium clinical adoption above conventional imaging and blood test alternatives.

Ovarian Cancer Diagnostics Market Segment Analysis

-

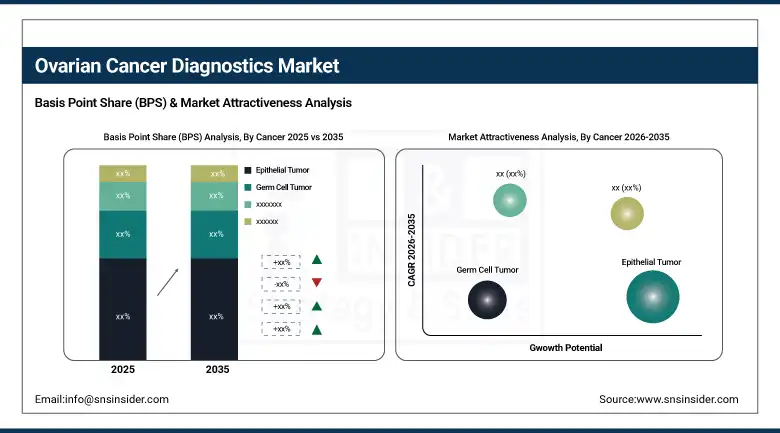

By Cancer, the Epithelial Tumor segment dominated the ovarian cancer diagnostics market with approximately 78.6% share in 2025, while the Germ Cell Tumor segment is the fastest growing as genetic testing advances and awareness expands.

-

By Diagnosis, the Imaging segment dominated the ovarian cancer diagnostics market with approximately 52.3% share in 2025, while the Blood Test segment is the fastest growing as liquid biopsy and biomarker adoption accelerates.

-

By End-use, the Hospital Laboratories segment dominated the ovarian cancer diagnostics market with approximately 61.2% share in 2025, while the Cancer Diagnostic Centers segment is the fastest growing as specialized testing centers adopt advanced AI and NGS technologies.

By Cancer, epithelial tumor dominates, germ cell tumor grows fastest

Epithelial tumors retained the dominant position in the ovarian cancer diagnostics market in 2025 with approximately 78.6% revenue share. Epithelial ovarian cancer’s commercial primacy reflects its extraordinary prevalence, representing approximately 90% of all ovarian cancer cases, whose high disease burden creates consistent and structured diagnostic demand. The asymptomatic nature of epithelial ovarian cancer during early stages results in late detection, creating high and sustained demand for sophisticated diagnostic technologies including imaging, CA-125 and HE4 blood testing, and biopsy procedures. Each healthcare system that invests in epithelial ovarian cancer screening infrastructure creates institutional procurement whose aggregate across global hospital networks sustains the segment’s dominant commercial position through the forecast period.

Germ cell tumors represent the fastest-growing cancer segment because rising awareness, enhanced screening methods, increasing research investments, and the younger patient demographic’s demand for accurate and non-invasive diagnostic solutions create above-average growth momentum. Although rare, germ cell tumors’ occurrence in younger women creates clinical urgency for sensitive and specific diagnostic approaches whose early detection requirement drives adoption of blood tests for tumor markers including alpha-fetoprotein (AFP) and human chorionic gonadotropin (hCG).

By Diagnosis, imaging dominates, blood tests grow fastest

Imaging retained the dominant diagnostic position with approximately 52.3% of the ovarian cancer diagnostics market in 2025. Imaging methods including ultrasound, MRI, CT scans, and PET scans remain the standard of care for identifying ovarian cancer because they provide real-time, non-invasive measurement of tumor size, position, and metastasis extent. Increased incorporation of artificial intelligence and machine learning in imaging diagnostics has substantially enhanced precision and workflow productivity, further reinforcing adoption across hospital imaging centers and teleradiology service networks. The progressive expansion of high-resolution transvaginal ultrasound and contrast-enhanced MRI capability within hospital-based imaging infrastructure sustains imaging’s dominant diagnostic position.

Blood tests represent the fastest-growing diagnostic category, supported by expanding demand for minimally invasive and early-onset ovarian cancer diagnostic solutions whose clinical appeal creates above-average commercial momentum. Increasing dependence on biomarker-based diagnostics including CA-125 and HE4 assays drives blood test adoption across hospital laboratories and cancer diagnostic centers. Liquid biopsy’s emergence as a new diagnostic platform for real-time tracking of cancer development and treatment response creates premium adoption whose sensitivity advantage over conventional imaging creates clinical differentiation sustaining above-average commercial growth through the 2025-2035 forecast period.

By End-use, hospital laboratories dominate, cancer diagnostic centers grow fastest

Hospital laboratories retained the dominant end-use position with approximately 61.2% of the ovarian cancer diagnostics market in 2025. Hospitals remain the first preference for ovarian cancer diagnosis because of their well-equipped integrated facilities, availability of advanced diagnostic technologies, and specialized oncologists and pathologists whose expertise creates diagnostic accuracy that specialized centers cannot fully replicate. The growing prevalence of ovarian cancer and increased hospitalizations for screening create sustained hospital laboratory procurement whose integrated testing capability across imaging, biopsy, and molecular analysis under one facility sustains dominant commercial position.

Cancer diagnostic centers represent the fastest-growing end-use category as patient preference for specialized, efficient testing laboratories with compact turnaround times creates structured above-average procurement. The swift adoption of advanced technologies including AI-based imaging and next-generation sequencing for genomics testing substantially enhances diagnostic accuracy at specialized centers whose focused oncology capability creates clinical differentiation. Each cancer diagnostic center that deploys NGS and liquid biopsy platforms for ovarian cancer screening creates procurement whose institutional investment sustains segment growth momentum through 2035.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

41.2% |

|

Europe |

Germany |

22.1% |

|

Asia Pacific |

China |

33.6% |

|

Middle East & Africa |

UAE |

38.2% |

|

Latin America |

Brazil |

44.0% |

North America Ovarian Cancer Diagnostics Market Insights

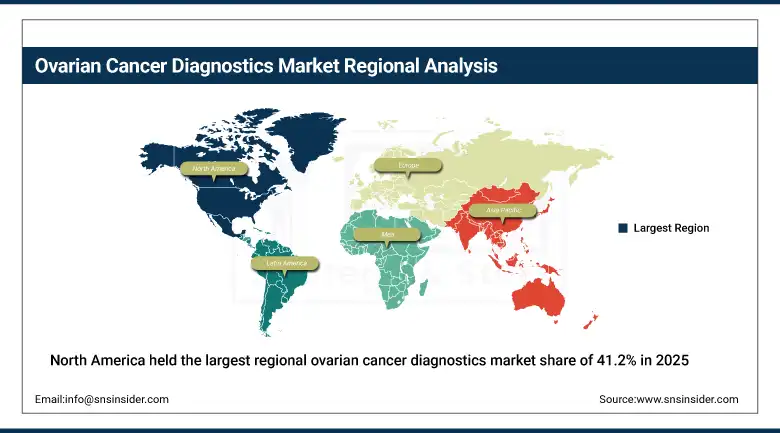

North America held the largest regional ovarian cancer diagnostics market share of 41.2% in 2025, driven by well-developed healthcare infrastructure, high awareness rates, and a strong base of major diagnostic firms including Roche, Abbott, Quest Diagnostics, and Myriad Genetics. The National Cancer Institute (NCI) invested more than USD 185 million in ovarian cancer research in 2024, sustaining early detection innovation whose commercial value compounds with expanding insurance coverage for advanced diagnostic procedures. Growing federal investment in cancer research, continued FDA regulatory advancement accelerating new testing technology approval, and high adoption of genetic testing for BRCA1 and BRCA2 risk assessment sustain North America’s dominant regional position through 2035.

The United States accounts for the substantial majority of North American revenues through its advanced hospital laboratory infrastructure, expanding cancer diagnostic center network, and the domestic research institute’s clinical trial investment. Canada contributes meaningful secondary revenues through its national healthcare system’s cancer screening program investment and expanding adoption of biomarker-based diagnostic technologies.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Ovarian Cancer Diagnostics Market Insights

Europe represents a technically sophisticated ovarian cancer diagnostics market where advanced healthcare systems, established oncology networks, and regulatory frameworks supporting diagnostic innovation create structured and consistent demand. Germany accounts for approximately 22.1% of European revenues through its pharmaceutical industry’s companion diagnostic development, the enterprise healthcare sector’s advanced imaging infrastructure, and the national cancer research program’s sustained investment in early detection technology.

The United Kingdom, France, and the Netherlands are significant secondary markets where national health service procurement, medical research institution investment, and expanding genetic testing adoption create consistent ovarian cancer diagnostics revenue. The EU’s In Vitro Diagnostic Regulation (IVDR) framework creates structured quality standards whose compliance investment sustains premium diagnostic technology adoption across Western European healthcare systems.

Asia Pacific Ovarian Cancer Diagnostics Market Insights

Asia Pacific is the fastest-growing regional ovarian cancer diagnostics market, driven by growing cancer prevalence, expanding healthcare spending, and government-driven cancer screening campaigns across China, India, and Japan. The WHO projects that ovarian cancer incidence in Asia will grow more than 20% by 2030, creating sustained diagnostic demand whose volume growth compounds with progressive healthcare infrastructure investment.

China accounts for approximately 33.6% of Asia Pacific revenues through its position as the region’s largest healthcare market, the domestic pharmaceutical industry’s diagnostic investment, and the government’s national cancer screening program expansion. Japan’s precision medicine initiative, South Korea’s advanced biomedical research infrastructure, and India’s rapidly growing consumer healthcare market create significant secondary revenue streams whose combined procurement sustains Asia Pacific’s fastest-growing regional status through the 2025-2035 forecast period.

MEA & Latin America Ovarian Cancer Diagnostics Market Insights

UAE leads MEA revenues at approximately 38.2% through its advanced healthcare infrastructure, government investment in oncology diagnostic capability, and the regional medical tourism sector’s demand for sophisticated cancer screening technology. Saudi Arabia and South Africa represent significant secondary MEA markets through government healthcare expansion programs and growing private hospital investment in advanced diagnostic technology. Brazil leads Latin American revenues at approximately 44.0% through its public healthcare system’s expanding cancer screening investment, the domestic pharmaceutical sector’s diagnostic innovation, and the growing private healthcare network’s adoption of biomarker-based and imaging diagnostic technologies. Argentina and Colombia represent growing secondary markets whose healthcare system modernization sustains above-average regional procurement growth.

Market Dynamics

Growth Drivers: Technological advancements, rising incidence, and increasing awareness drive market growth

The growing global incidence of ovarian cancer represents the most commercially consistent demand driver for the diagnostics market. The World Cancer Research Fund reported more than 313,000 new ovarian cancer cases diagnosed globally, with continuous increase driven by aging populations and evolving lifestyle factors creating sustained and expanding diagnostic demand. Advanced technologies including AI-based imaging, liquid biopsy, and multi-biomarker blood tests are substantially enhancing early detection rates and promoting adoption across hospital and specialized diagnostic center channels. Government initiatives including the CDC’s Inside Knowledge Campaign and equivalent programs globally are promoting early diagnosis awareness whose clinical uptake creates commercial procurement that sustains above-average growth through 2035.

Research funding from the NIH, which invested more than USD 185 million in ovarian cancer research in 2024, the Ovarian Cancer Research Alliance (OCRA), and leading pharmaceutical companies including Roche and Thermo Fisher Scientific drives biomarker innovation and diagnostic platform development whose commercial deployment creates new market categories. The integration of personalized medicine and next-generation sequencing in ovarian cancer diagnosis improves precision and enables more targeted therapeutic pathway identification, creating clinical value that sustains premium diagnostic adoption.

Restraints: High diagnostic costs and absence of universal screening programs hinder market growth

Higher diagnostic costs can be seen as a major limiting factor in the ovarian cancer diagnosis market. Advanced diagnostic techniques such as MRI scans and PET scans can cost between USD 1,000 to USD 7,000 per diagnostic process, making them unaffordable for many individuals in developing countries. Biomarkers, such as HE4 and CA-125, although useful, may demand additional follow-up diagnostic processes, which increase overall costs.

The absence of universally established ovarian cancer screening programs represents a structural market restraint that limits systematic early detection comparable to mammography for breast cancer or Pap testing for cervical cancer. Without standardized periodic screening recommendations, most women remain undetected until advanced disease stages whose late diagnosis creates poor clinical outcomes that moderate the market’s public health impact and sustain advocacy pressure for screening program development.

Opportunities: Emerging technologies, biomarker advancements, and increasing research investments present significant growth prospects

The accelerating development of biomarker-based diagnostics, AI-aided imaging, and liquid biopsy technologies creates substantial market expansion opportunities whose clinical utility sustains premium adoption investment. NGS and multi-panel biomarker platforms are enhancing early detection accuracy, reducing false positives, and providing treatment personalization whose combined clinical value creates procurement motivation across sophisticated healthcare systems. Recent research demonstrating liquid biopsy’s ability to identify ovarian cancer months ahead of conventional imaging creates a valuable clinical window for early treatment intervention whose outcome improvement sustains premium diagnostic adoption.

Home diagnostic solutions and telemedicine-integrated ovarian cancer testing services represent a growing opportunity whose remote testing and consultation capability enhances accessibility for rural patients and creates new commercial channels beyond traditional hospital and clinic settings. More than USD 500 million was invested in ovarian cancer research in 2024 by pharmaceutical and biotechnology firms creating diagnostic innovation pipelines whose commercial deployment sustains market growth through the 2025-2035 forecast period.

Recent Developments:

-

2025: Researchers at Karolinska Instituted demonstrated that AI-driven neural networks can surpass human experts in detecting ovarian cancer from ultrasound images, as published in Nature Medicine, highlighting AI’s potential to transform early ovarian cancer screening capability.

-

2024: Mayo Clinic researchers identified a distinct ovarian cancer microbiome that may aid in early detection and predicting treatment response, as published in Scientific Reports, opening new biomarker-based diagnostic avenues for earlier and more accurate ovarian cancer identification.

-

2024: Roche expanded its Cobas platform with enhanced CA-125 and HE4 assay capabilities, supporting broader adoption of standardized biomarker-based ovarian cancer diagnostics within hospital laboratory settings globally.

Ovarian Cancer Diagnostics Market Key Players

-

F. Hoffmann-La Roche AG

-

Johnson & Johnson Services, Inc.

-

GlaxoSmithKline Plc (GSK)

-

AstraZeneca Plc

-

Siemens Healthineers AG

-

Abbott Laboratories

-

Thermo Fisher Scientific Inc.

-

Bio-Rad Laboratories, Inc.

-

Quest Diagnostics Incorporated

-

Illumina, Inc.

-

Becton, Dickinson and Company (BD)

-

Agilent Technologies, Inc.

-

QIAGEN N.V.

-

Myriad Genetics, Inc.

-

Exact Sciences Corporation

-

Hologic, Inc.

-

Sysmex Corporation

-

Danaher Corporation

-

PerkinElmer, Inc.

-

Guardant Health, Inc.

Ovarian Cancer Diagnostics Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.92 Billion |

| Market Size by 2035 | USD 8.08 Billion |

| CAGR | CAGR of 5.06% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Cancer (Epithelial Tumor, Germ Cell Tumor, Stromal Cell Tumor, Others) • By Diagnosis (Imaging, Blood Test, Biopsy, Others) • By End-use (Hospital Laboratories, Cancer Diagnostic Centers, Research Institutes, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | F. Hoffmann-La Roche AG, Johnson & Johnson Services, Inc., GlaxoSmithKline Plc (GSK), AstraZeneca Plc, Siemens Healthineers AG, Abbott Laboratories, Thermo Fisher Scientific Inc., Bio-Rad Laboratories, Inc., Quest Diagnostics Incorporated, Illumina, Inc., Becton, Dickinson and Company (BD), Agilent Technologies, Inc., QIAGEN N.V., Myriad Genetics, Inc., Exact Sciences Corporation, Hologic, Inc., Sysmex Corporation, Danaher Corporation, PerkinElmer, Inc., and Guardant Health, Inc. |

Frequently Asked Questions

North America dominated the Ovarian Cancer Diagnostics Market in 2025 with the highest revenue share of 41.2%, while Asia Pacific is the fastest-growing region.

Epithelial Tumor dominated the Ovarian Cancer Diagnostics Market in 2025 with approximately 78.6% revenue share, while the Germ Cell Tumor segment is the fastest-growing cancer segment.

Rising global incidence of ovarian cancer, advancements in AI-powered imaging, liquid biopsy, and next-generation sequencing diagnostic technologies, combined with increasing government and institutional investment in early detection programs, are the primary growth factors driving the Ovarian Cancer Diagnostics Market.

The Ovarian Cancer Diagnostics Market was valued at USD 4.92 Billion in 2025.

The Ovarian Cancer Diagnostics Market is expected to grow at a CAGR of 5.06% from 2026 to 2035.

Get in Touch