Cooling Tower Market Report Scope & Overview:

The Cooling Tower Market Size was estimated at USD 3.35 billion in 2023 and is expected to arrive at USD 5.15 billion by 2032 with a growing CAGR of 4.89% over the forecast period 2024-2032.

To get more information on Cooling Tower Market - Request Free Sample Report

This report offers a unique perspective on the Cooling Tower Market by analyzing installed capacity trends across key regions, utilization efficiency, and water consumption metrics, highlighting sustainability concerns. It provides insights on maintenance and downtime metrics, evaluating operational reliability. The study explores the adoption of advanced cooling technologies by region, tracking the shift toward energy-efficient and eco-friendly solutions. Additionally, it presents export/import trends of cooling towers and components, mapping global trade flows. Emerging trends such as AI-based predictive maintenance, hybrid cooling systems, and the impact of stricter environmental regulations further enhance this comprehensive market assessment.

Market Dynamics

Drivers

-

The rising demand for energy-efficient cooling solutions is driven by sustainability concerns, regulatory compliance, and advancements in hybrid, dry, and smart cooling tower technologies.

The growing demand for energy-efficient cooling solutions is transforming the cooling tower market, driven by rising awareness of energy conservation and strict government regulations on emissions and water usage. As a result, industries are moving towards energy-efficient cooling technologies to optimise operational costs and meet environmental regulations. To use less water and energy, hybrid and dry cooling towers are becoming more popular. Real-time performance optimization and predictive maintenance through IoT and AI-based monitoring systems further improves efficiency. Closed-loop and smart cooling systems are increasingly favored in the power generation, manufacturing, and HVAC sectors, following market trends. With the industries moving towards sustainability and compliance to regulation, high-efficiency cooling towers are expected to see a considerable uptake. This paradigm shift is not just fuelling technological advancements but also widening the market for sustainable and energy efficient cooling solutions, globally.

Restraint

-

The high capital and maintenance costs of cooling towers make adoption challenging for SMEs due to expensive installation, upkeep, and operational expenses.

The high initial investment and maintenance costs of cooling towers pose a significant challenge, especially for small and medium enterprises (SMEs). Cooling tower costs include significant capital outlay for purchase, physical system construction, and economic capital depreciation into existing infrastructures. That cost is additionally elevated by advanced cooling towers with energy-efficient designs and modern technologies. Routine maintenance is also vital for preventing scaling, corrosion, and microbial growth, all of which can affect efficiency and longevity. Operational expenses are further accumulated by the need for water treatment chemicals, periodic inspections, and components replacements. These costs can be prohibitive for SMEs with limited budgets, hence making it difficult for them to adopt new or upgrade existing cooling tower systems. In addition to this, sudden breakdowns may necessitate expensive fixes, resulting in a dip in production. In response to this crisis, organizations need to find economical resolutions and employ hybrid cooling systems and predictive maintenance solutions to boost performance and lower long-term costs.

Opportunities

-

The integration of IoT and AI in cooling towers enables real-time monitoring, predictive maintenance, and improved efficiency, reducing downtime and operational costs.

The adoption of smart cooling tower technologies is revolutionizing the industry by integrating IoT and AI for real-time monitoring and predictive maintenance. IoT-enabled sensors provide real-time tracking of temperature, humidity, water levels, and energy consumption, enabling operators to optimize their performance and identify problems before they arise. AI-led analytics also add efficiency in predicting maintenance, thus reducing downtime and improving overall operational reliability. Such solutions enable sectors to optimize energy use, reduce maintenance expenses, and prolong the lifespan of machinery. Also, rugged monitoring features allow monitoring operations in harsh field acting environments, plants, and factories. The further ongoing need for automation and data-driven decision-making, along with the rising requirement for energy-efficient options, is promoting the usage of smart cooling towers. Following regulatory bodies advocating for sustainable, water-efficient cooling solutions, the smart technologies are projected to be a game changer in cooling tower operations within diverse industry verticals.

Challenges

-

Cooling tower manufacturers face compliance challenges due to stringent global safety and environmental regulations, requiring continuous investment in eco-friendly solutions and technological advancements.

Cooling tower manufacturers must adhere to stringent national and international safety and environmental regulations, making compliance a significant challenge. Strict standards for emission, water and energy efficiency to control the environmental impact are imposed by governments and regulatory bodies. Regulations like the U.S. EPA’s Clean Water Act or OSHA’s workplace safety guidelines require environmentally safe materials, Legionella controls, and responsible wastewater treatments. Cooling towers also need to be certified in the industry standards like ASHRAE and ISO for their testing, quality control. Non-compliance could lead to significant penalties, closure of facilities, or damage to reputation. Moreover, changing regulations require ongoing investment in research, development, and technology updates to adapt to new standards. Manufacturers also have to contend with policies that differ across regions, leading to more complexity in expanding in global markets. Therefore, organizations need to invest in compliance strategies for providing winning solutions in risk management while ensuring cost-efficient quality standards in line with regulatory requirements.

Segmentation Analysis

By Product

The Open Circuit segment dominated with a market share of over 43% in 2023, due to its wide application in various industries, including, but not limited to, power generation, HVAC systems, oil & gas, and manufacturing. Cooling towers expose water directly to air for the efficient removal of heat. In industries where large-scale cooling is needed, they are favored as they cost less to install and operate than other types. Moreover, the open circuit cooling towers have lower maintenance costs and are also better suited for high heat applications. Due to rising demand for all kinds of energy-efficient cooling solutions, the adoption of cross flow cooling towers remains particularly steadfast, especially in the regions undergoing rapid industrialization and infrastructure development, thereby highlighting their dominance in the global cooling tower market.

By Material

The FRP (Fiber-Reinforced Plastic) segment dominated with a market share of over 32% in 2023, owing to its excellent corrosion resistance, lightweight construction, durability, and cost-effectiveness. FRP resists chemical exposure and environmental factors much more than conventional materials like steel and concrete, which make them preferable across industries such as power generation, HVAC, petrochemical and manufacturing. This is a major contributing factor to its widespread adoption, as well as its easy installation, low maintenance requirement, and long service life. Moreover, FRP cooling towers enable better thermal efficiency and structural integrity, which will lower operational cost for end users. As industries continue to focus on energy efficiency and sustainability, the need for FRP cooling towers will likely be robust, cementing its position as the dominant material in the market.

By Application

The Industrial segment dominated with a market share of over 34% in 2023, due to its widespread use in industries such as chemicals, food & beverage, and manufacturing. Efficient heat dissipation is crucial in these industries to maintain optimal working conditions, enhance energy efficiency, and extend the life of the equipment. Cooling towers are a temporary solution used for achieving process temperature control, avoiding thermal stress, improving productivity. Besides, strict environmental regulations and demand for energy-efficient cooling solutions, in the industrial segment, further fuel demand for energy-efficient cooling solutions. The increasing demand for reliable cooling systems is due to rapid industrialization, especially in the case of developing economies. Consequently, the industrial segment accounts for the largest share in driving the growth of the market, coming on the heels of continuous upgrades in the cooling tower technologies and sustainable cooling solutions.

Regional Analysis

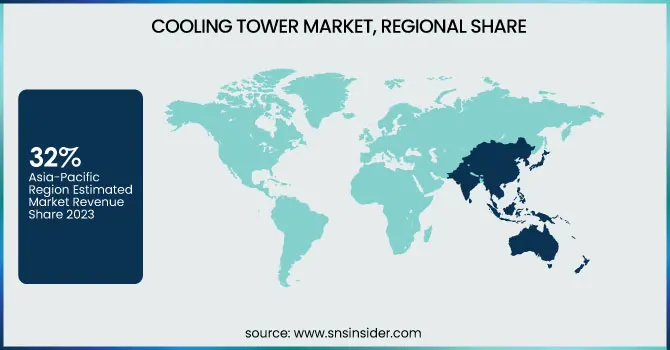

Asia-Pacific region dominated with a market share of over 32% in 2023, primarily due to rapid industrialization and increasing energy demand across countries like China, India, and Japan. Power Plants, Chemical Processing, and Manufacturing facilities are all expanding quickly in the region, which will require cooling solutions. Around the world, the growing rate of urbanization and rapid infrastructure development has greatly contributed to the increase of HVAC systems, thereby aiding market expansion. Dominance in the market is also supported by government initiatives promoting industrial expansion and sustainable cooling technologies. The factors such as the presence of major market players and innovative cooling tower designs for efficiency and minimum environmental impact reiterate the Asia-Pacific market share in the cooling tower market. The economy will continue growing, and technology will continue to advance, cementing the region's position as the most prominent in the world.

North America is emerging as the fastest-growing region in the cooling tower market due to rising investments in power generation and industrial expansion. Rising need for energy efficient cooling solutions in oil & gas, chemical processing, and manufacturing industries is supporting the market growth. Moreover, there are various developments in HVAC systems in commercial and residential sectors in the region, which in turn, is driving demand. U.S. Environmental Protection Agency (EPA) agencies have implemented increasingly stringent environmental regulations, promoting the adoption of sustainable and water-efficient technologies for cooling solutions. The increasing emphasis on carbon reduction and energy efficiency, as well as advances in cooling tower technology, are driving market growth across North America.

Get Customized Report as per Your Business Requirement - Enquiry Now

Key players

-

SPIG S.p.A (Field-Erected Cooling Towers, Modular Cooling Towers)

-

Absolute Cooling Tower Services Ltd. (Cooling Tower Maintenance, Repair & Components)

-

ESINDUS S.A (Hamon Group) (Natural Draft Cooling Towers, Induced Draft Cooling Towers)

-

Paharpur Cooling Towers Limited (Crossflow Cooling Towers, Counterflow Cooling Towers)

-

FANS a.s. (Evaporative Cooling Towers, Dry Cooling Towers)

-

LIANG CHI INDUSTRY (THAILAND) CO., LTD. (FRP Cooling Towers, Closed Circuit Cooling Towers)

-

Delta Cooling Towers, Inc. (HDPE Cooling Towers, Factory-Assembled Cooling Towers)

-

SPX Corporation (Cooling Tower Systems, Parts & Components)

-

Cooling Tower Depot, Inc. (Field-Erected Cooling Towers, Cooling Tower Parts)

-

Superchill Australia Pty Ltd. (Industrial Cooling Towers, Energy-Efficient Cooling Towers)

-

Baltimore Aircoil Company (Hybrid Cooling Towers, Closed-Circuit Cooling Towers)

-

EVAPCO, Inc. (Wet Cooling Towers, Adiabatic Cooling Systems)

-

Babcock & Wilcox Enterprises, Inc. (Large Industrial Cooling Towers, Dry Cooling Systems)

-

Marley Cooling Technologies (SPX Cooling Technologies, Inc.) (Crossflow Cooling Towers, Counterflow Cooling Towers)

-

Enexio Water Technologies GmbH (Wet & Dry Cooling Towers, Cooling Tower Fill Media)

-

Hamon & Cie (International) S.A. (Air-Cooled Condensers, Induced Draft Cooling Towers)

-

Johnson Controls (HVAC Cooling Towers, Industrial Cooling Towers)

-

Thermax Limited (Natural Draft Cooling Towers, Field Erected Cooling Towers)

-

Yuan Chang Tsay Industry Co., Ltd. (FRP Cooling Towers, Modular Cooling Towers)

-

Artech Cooling Towers Pvt. Ltd. (Wooden Cooling Towers, Concrete Cooling Towers)

Suppliers for the Cooling Tower Market

-

SPX Cooling Technologies

-

Evapco

-

Baltimore Aircoil Company

-

Hamon Group

-

Paharpur Cooling Towers

-

Delta Cooling Towers

-

Enexio

-

Marley Cooling Towers

-

Mesan Cooling Towers

-

DONGGUAN CARNO MACHINERY CO., LTD.

Recent Development

- In January 2024: SPX Cooling Tech, LLC, a full-service company specializing in the design and manufacture of evaporative cooling towers and fluid coolers, inaugurated a new manufacturing facility in Springfield, Missouri. This expansion enhances the company's operations, increases capacity, and optimizes its legacy Marley brand products.

- In February 2023: Baltimore Aircoil Company (BAC) introduced the Trillium Series Adiabatic Cooler, an energy-efficient cooling tower designed for applications with limited water usage. The innovative design prioritizes water and energy efficiency, lowering overall costs while streamlining installation and maintenance.

- In August 2024: BAC signed an exclusive global licensing agreement with DUG Technology, granting access to DUG's patented immersion-cooling technology for high-density data centers. This collaboration aims to address the rising demand for data center cooling by integrating sustainable, high-efficiency solutions that reduce energy consumption and operational costs.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | USD 3.35 Billion |

| Market Size by 2032 | USD 5.15 Billion |

| CAGR | CAGR of 4.89% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Open circuit, Closed circuit, Hybrid) • By Material (FRP, Steel, Concrete, Wood, HDPE) • By Application (HVAC, Power Generation, Oil & Gas, Industrial) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | SPIG S.p.A, Absolute Cooling Tower Services Ltd., ESINDUS S.A (Hamon Group), Paharpur Cooling Towers Limited, FANS a.s., LIANG CHI INDUSTRY (THAILAND) CO., LTD., Delta Cooling Towers, Inc., SPX Corporation, Cooling Tower Depot, Inc., Superchill Australia Pty Ltd., Baltimore Aircoil Company, EVAPCO, Inc., Babcock & Wilcox Enterprises, Inc., Marley Cooling Technologies (SPX Cooling Technologies, Inc.), Enexio Water Technologies GmbH, Hamon & Cie (International) S.A., Johnson Controls, Thermax Limited, Yuan Chang Tsay Industry Co., Ltd., Artech Cooling Towers Pvt. Ltd. |

Frequently Asked Questions

Asia-Pacific dominated the Cooling Tower Market in 2023.

The “Open circuit” segment dominated the Cooling Tower Market.

The rising demand for energy-efficient cooling solutions is driven by sustainability concerns, regulatory compliance, and advancements in hybrid, dry, and smart cooling tower technologies.

The Cooling Tower Market was USD 5.15 billion in 2023 and is expected to reach USD 3.35 billion by 2032.

The Cooling Tower Market is expected to grow at a CAGR of 4.89% during 2024-2032.

Get in Touch