Crosslinking Agent Market Report Scope & Overview:

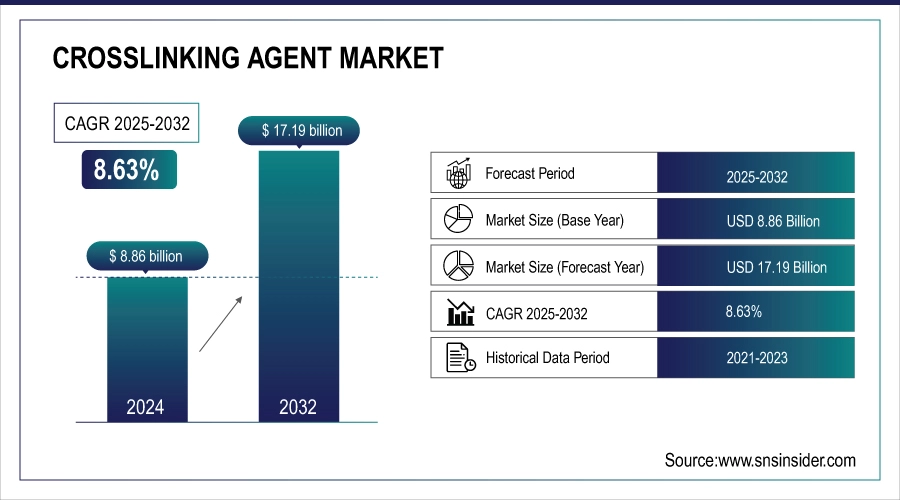

The Crosslinking Agent Market Size was valued at USD 8.86 Billion in 2024 and is expected to reach USD 17.19 Billion by 2032, growing at a CAGR of 8.63% over the forecast period of 2025-2032.

Crosslinking agent market analysis that increasing demand for high-performance coatings, adhesives, & sealants in the automotive and construction/ infrastructure industry is also driving the crosslinking agent market. These compounds improve the mechanical strength, thermal aging, and chemical resistance of the polymers for long service. Rising urbanization, growing infrastructural activities, and demand for long-lasting, eco-friendly materials are driving the crosslinking agent market growth.

To Get more information On Crosslinking Agent Market - Request Free Sample Report

In July 2025, Evonik Industries will also concentrate on the research and development of eco-friendly crosslinking agents owing to the increasing trend of sustainable material demand. Their interest in cutting back on (VOCs) has also helped comply with a rise in green demand, no matter where they are located in the world.

Key Crosslinking Agent Market Trends

-

Environmental regulations drive adoption of sustainable and bio-based crosslinkers

-

Demand for lightweight, high-strength materials boosts crosslinker use in automotive and aerospace

-

Need for faster, energy-efficient processes accelerates UV and radiation curing technologies

-

Urbanization and industrial growth expand demand in emerging markets

-

Development of smart and high-performance polymers promotes integration with advanced crosslinkers

-

Market competition and innovation increase investment in R&D for advanced crosslinkers

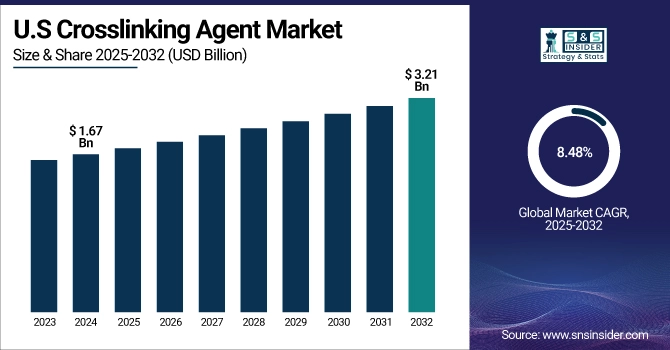

The U.S. Crosslinking Agent Market size was valued at USD 1.67 Billion in 2024 and is projected to reach USD 3.21 Billion by 2032, growing at a CAGR of 8.48%during 2025-2032.

The U.S. Crosslinking Agent Market is expanding on account of robust sales from end-usage industries such as automotive, construction, and industrial manufacturing. Increasing usage of high-performance coatings, adhesives, and sealants has created demand for crosslinking agents that offer higher durability, chemical resistance, and thermal resistance. Furthermore, the increasing environmental legislation is promoting the demand for eco-friendly and low-VOC polyurethane crosslinkers.

Crosslinking Agent Market Growth Drivers

-

Rising Demand for High-Performance Coatings and Adhesives Drives the Market Growth

There is a growing demand for high-performance coatings and adhesives in the automotive, architectural, and industrial sectors. Crosslinking agents are widely employed for improving the mechanical properties, thermal stability, and chemical resistance of the polymers in coatings applications, adhesive, and sealant industries. This provides for extended service life, better wear and corrosion resistance, and the ability to withstand operation in harsh environments. Lightweight, high-strength materials used in the automotive industry, to facilitate fuel economy and emission control, directly promote the crosslinking agents applied in paint, coatings, and composites.

Evonik Industries, for example, supported new R&D infrastructure in 2024 for advanced epoxy and urethane-based crosslinkers for industrial coating, toward superior performance, sustainability, and regulatory compliance. In addition to addressing current needs, such investment supports the capturing of growth in developing industrial applications and premium markets worldwide.

Crosslinking Agent Market Restraints

-

High Production Costs, Which May Hamper the Market Growth

Specialized crosslinkers manufacturing a specialized synthetic crosslinking agent entails complex chemical processes and expensive raw materials, which may preclude its use by smaller-sized manufacturers. The cost dimension is also affected by the instability of petrochemical raw materials. The difficulty at the small company level is the scaling of production, as this requires large capital investment, and a lot of smaller chemical companies are never going to move their business model to a mass production model.

Crosslinking Agent Market Opportunities

-

Development of Sustainable and Bio-Based Crosslinkers Create an Opportunity for the Market

Growing global attentiveness to sustainability and tighter environmental legislation, combined with consumer demand for development and production of greener products, are spurring innovation in the crosslinker market. Previous crosslinkers are typically based on petrochemical-derived chemicals and can release volatile organic compounds (VOCs), damaging the environment. In a similar vein, makers are investing in bio-based, recyclable, and low-VOC crosslinkers that deliver low-environmental impact solutions with high performance. These environmentally friendly alternatives are being used in applications including packaging, automotive, construction, and coatings, where durability and sustainability are key requirements.

For example, in July 2025, Evonik introduced a new line of epoxy crosslinkers based on renewable energy to meet global sustainability and reduce carbon footprint.

Crosslinking Agent Market Segment Analysis:

-

By Type, Amines led with around 28% share in 2024; Isocyanates are the fastest growing (CAGR 9.0%) due to their increasing use in high-performance coatings and adhesives.

-

By Technology, Thermal Crosslinking dominated with 35% share in 2024; UV / Radiation Crosslinking is the fastest growing (CAGR 8.8%) owing to faster curing times and energy-efficient processes.

-

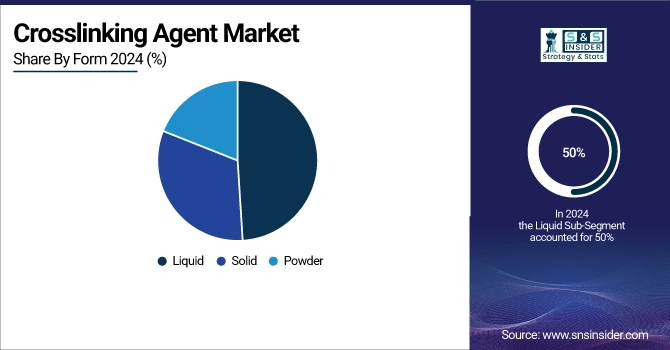

By Form, Liquid form held 50% share in 2024; Powder form is the fastest growing (CAGR 8.7%) driven by ease of handling and stability in industrial applications.

-

By End-Use Industry, Automotive & Transportation led with 38% share in 2024; Healthcare & Pharmaceutical is the fastest growing (CAGR 8.9%) due to the rising need for durable, sterilizable coatings and adhesives.

By Type

Amines dominate the crosslinking agent market with approximately 28% share in 2024, due to their wide applicability in coatings, adhesives, and sealants across the automotive and construction industries. They offer excellent chemical resistance and thermal stability, making them preferred in high-performance polymer formulations. Isocyanates are the fastest-growing type with a CAGR of 9%, driven by the increasing use in polyurethane coatings and adhesives for lightweight materials in automotive and industrial manufacturing. Their ability to enhance mechanical properties and durability makes them a preferred choice for emerging applications.

By Technology

Thermal crosslinking holds the largest market share of around 35% in 2024, as it is widely used in industrial coatings, adhesives, and composite manufacturing due to its simplicity and consistent performance. UV and radiation curing technologies are the fastest-growing segment with a CAGR of 8.8%, owing to faster curing times, lower energy consumption, and compatibility with modern eco-friendly formulations. These technologies are increasingly adopted in packaging, electronics, and specialty coatings, where rapid processing and environmental compliance are critical.

By Form

Liquid crosslinking agents dominate the market with a 50% share in 2024, as they are easy to handle, mix, and apply in coatings and adhesive formulations across multiple industries. Powder forms are the fastest-growing segment with a CAGR of 8.7%, supported by their longer shelf life, stability during storage, and suitability for industrial-scale processing. Industries such as construction and automotive prefer powder crosslinkers for customized formulations and consistent performance in high-temperature applications.

By End-Use Industry

Automotive & transportation is the dominating end-use industry with a 38% share in 2024, driven by the adoption of lightweight polymers, protective coatings, and high-performance adhesives to improve fuel efficiency and durability. Healthcare & pharmaceutical is the fastest-growing segment with a CAGR of 8.9%, fueled by increasing demand for sterilizable, chemically resistant coatings and adhesives in medical devices, packaging, and hospital infrastructure. Rising standards for safety and durability are accelerating growth in these applications.

Asia-Pacific Crosslinking Agent Market Insights

Asia Pacific held the largest crosslinking agent market share in 2024, around 38.04% 2024. It is owing to the high industrial growth in this region in the past two decades, where the overall sales of the crosslinking agent market remained high. Demand for high-performance coatings and adhesives for infrastructure, automotive, and packaging in states such as China, India, and Japan is soaring. The increased domestic production, coupled with the emergence of global chemical manufacturing hubs, further bolsters market leadership. For instance, a new crosslinking agent production plant from Arkema Group in India, which will enter operation in 2024, will result in an increase in the capacity of high-performance polymers to serve the local market and for export, and will reduce lead times.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Crosslinking Agent Market Insights

North America continues to be at the forefront of the crosslinking agent market, due to the metal industries and construction. South East Asia and North Asia will rise rapidly on the back of increasing production. Rigorous environmental regulations in the US and Canada are fostering the demand for low-VOC and sustainable crosslinkers. Advanced R&D capabilities lead to innovations in high-performance adhesives, coatings, and polymers. In 2024, Evonik Industries increased its U.S. R&D capabilities to include next-generation epoxy and urethane crosslinkers and products that support automotive and industrial end use while conforming to environmental regulations.

Europe Crosslinking Agent Market Insights

Europe holds a considerable market share, as there is a high requirement for sustainable and tough coatings and adhesives in the automotive, construction, and industrial production industries. Regulations against VOCs and toxicants are driving technology to be “greener,” involving sustainable crosslinker development. Investment - The most recent development is LANXESS investing in a next-generation polymer additives facility in Germany in 2023 to manufacture environmentally friendly crosslinking agents for industrial coatings and automotive industries, again reinforcing the European supply chain.

Latin America (LATAM) and Middle East & Africa (MEA) Crosslinking Agent Market Insights

The market in Latin America and MEA for crosslinking agents is expanding on account of swift industrialization, infrastructure buildup, and the rising automotive and construction industries. Increased demand for durable, low-cost crosslinkers in coatings, adhesives, and construction applications is observed in Brazil and Mexico in Latin America. In the MEA, investments in the oil & gas, industrial manufacturing, and harsh-environment coatings sectors are expected to be the key factors influencing the demand for high-performance coatings. Recent examples include BASF increasing its polymer additives capacity in Brazil in 2024, by Solvay opening a crosslinking agent plant in the UAE in 2023, to supply adhesives and coatings for industrial and infrastructure projects, thereby increasing local production and the export potential.

Competitive Landscape for Crosslinking Agent Market:

BASF is a leading global chemical company providing crosslinking agents for coatings, adhesives, and construction applications. Their portfolio focuses on enhancing polymer durability, chemical resistance, and thermal stability, while also offering low-VOC and sustainable solutions for environmentally conscious industries.

-

In June 2024, BASF inaugurated a new production line in Brazil to manufacture high-performance crosslinking agents for automotive coatings and industrial adhesives. This expansion strengthens local supply, reduces lead times, and supports growing demand in Latin America’s automotive and construction sectors.

Evonik Industries specializes in advanced polymer and coating solutions, supplying crosslinking agents for industrial, automotive, and healthcare applications. Their products are engineered for enhanced adhesion, chemical stability, and energy-efficient processing.

-

In August 2024, Evonik launched a renewable-energy-powered epoxy crosslinker line in Germany, targeting sustainable coatings and adhesives. This initiative aligns with global environmental standards, enabling manufacturers to meet stricter regulations while improving product performance and processing efficiency.

Lanxess offers crosslinking agents for polyurethane, epoxy, and specialty coating applications, emphasizing high-performance, durability, and thermal resistance. Their solutions are widely used in automotive, construction, and industrial sectors.

-

In May 2023, Lanxess expanded its polymer additive facility in India to boost production of crosslinking agents for industrial coatings. The investment addresses growing demand in the Asia-Pacific and supports faster delivery to regional customers while enhancing R&D capabilities.

Crosslinking Agent Market Key Players

Some of the Crosslinking Agents Companies

-

BASF

-

Dow Inc.

-

Arkema Group

-

Evonik Industries

-

Lanxess

-

Wacker Chemie AG

-

Huntsman Corporation

-

Momentive Performance Materials

-

Solvay S.A.

-

Mitsubishi Chemical

-

Covestro AG

-

Clariant AG

-

Perstorp Holding AB

-

Hexion Inc.

-

Celanese Corporation

-

Allnex

-

Aditya Birla Chemicals

-

The Lubrizol Corporation

-

Evonik Goldschmidt GmbH

-

Kaneka Corporation

| Report Attributes | Details |

| Market Size in 2024 | USD 8.86 Billion |

| Market Size by 2032 | USD 17.19 Billion |

| CAGR | CAGR of8.63% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type: Amines, Amides, Isocyanates, Aziridines, Carbodiimides, Others (e.g., epoxies, silanes, peroxides) • By Technology: Thermal Crosslinking, UV / Radiation Crosslinking, Moisture / Humidity Curing, Chemical / Catalyst-Induced Crosslinking, Enzymatic Crosslinking, Others (dual-cure, hybrid systems) • By Form: Liquid, Solid, Powder • By End-Use Industry: Automotive & Transportation, Building & Construction, Industrial Manufacturing, Healthcare, Consumer Goods, Others (aerospace, electronics, packaging) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, France, UK, Italy, Spain, Poland, Russsia, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia,ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia Rest of Latin America) |

| Company Profiles | BASF, Dow Inc., Arkema Group, Evonik Industries, Lanxess, Wacker Chemie AG, Huntsman Corporation, Momentive Performance Materials, Solvay S.A., Mitsubishi Chemical, Covestro AG, Clariant AG, Perstorp Holding AB, Hexion Inc., Celanese Corporation, Allnex, Aditya Birla Chemicals, The Lubrizol Corporation, Evonik Goldschmidt GmbH, Kaneka Corporation |

Frequently Asked Questions

Ans BASF, Dow Inc., Arkema Group, Evonik Industries, Lanxess, Wacker Chemie, Huntsman Corporation, Momentive Performance Materials, Solvay S.A., Mitsubishi Chemical, Covestro AG, Clariant AG, Perstorp Holding AB, Hexion Inc., and Celanese Corporation

Ans Asia-Pacific, due to rapid industrialization, urbanization, and high demand from the automotive, construction, and electronics sectors.

Ans Automotive & transportation, construction & building, industrial manufacturing, healthcare & pharmaceutical, and consumer goods.

Ans Rising demand for high-performance coatings, adoption of sustainable agents, growth in automotive, construction, and healthcare industries, and industrialization in emerging markets.

Ans It involves chemicals that bond polymer chains to enhance strength, durability, and chemical resistance in coatings, adhesives, sealants, and composites.

Get in Touch