Bisphenol A Market Report Scope & Overview:

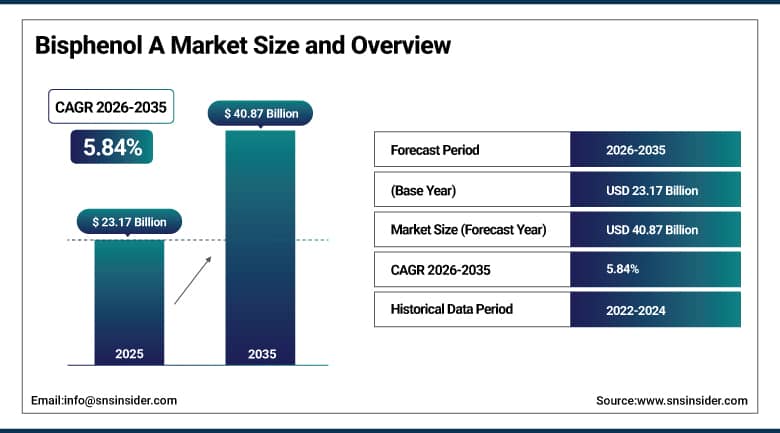

The Bisphenol A Market was valued at USD 23.17 Billion in 2025 and is expected to reach USD 40.87 Billion by 2035, growing at a CAGR of 5.84% from 2026 to 2035.

The global bisphenol A market is witnessing steady and sustainable growth on account of rising demands for polycarbonate plastics and epoxy resins within significant end use verticals such as the automotive, construction, electrical & electronics, and packaging sectors. Bisphenol A, which is a chemical compound with a molecular structure of C15H16O2, is a colorless crystalline solid which finds extensive use as a monomer for the manufacture of polycarbonates and as a curing agent for epoxy resins. Both these products find more than 95% application of all the global usage of BPA. The growth is fueled by polycarbonates' unrivaled ability to deliver unmatched toughness, transparency, thermal resistance, and light weight properties for which there is no replacement in automotive glazing, electrical housings, optical disc, and safety applications. At the same time, BPA usage growth from epoxy resins in coating, adhesive, printed circuit boards, and wind turbine blades applications is sustaining the market.

In December 2023, Nan Ya Plastics Corporation made an announcement of the commissioning of a new BPA production line at Ningbo, Zhejiang Province, China with a production capacity of 170,000 tonnes per year. This project is part of the planned integration of the supply chain for polycarbonate in China, due to the increasing demand for polycarbonate within the auto industry and other applications such as electronics and construction.

Market Size and Forecast

-

Market Size in 2026E: USD 24.52 Billion

-

Market Size by 2035: USD 40.87 Billion

-

CAGR: 5.84% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get More Information On Bisphenol A Market - Request Free Sample Report

Bisphenol A Market Trends

-

Electric vehicle production growth is increasing demand for BPA-based polycarbonate materials used in lightweight automotive components and battery systems.

-

Bio-based BPA development is gaining momentum as manufacturers pursue sustainable alternatives to meet evolving environmental and corporate sustainability goals.

-

Expansion of wind energy infrastructure is driving higher consumption of BPA-derived epoxy resins used in turbine blade manufacturing.

-

Recycling and circular economy initiatives are supporting BPA recovery and reuse through advancements in polycarbonate depolymerization technologies.

-

Development of high-purity BPA grades is creating premium market opportunities in electronics, semiconductor packaging, and other high-performance applications.

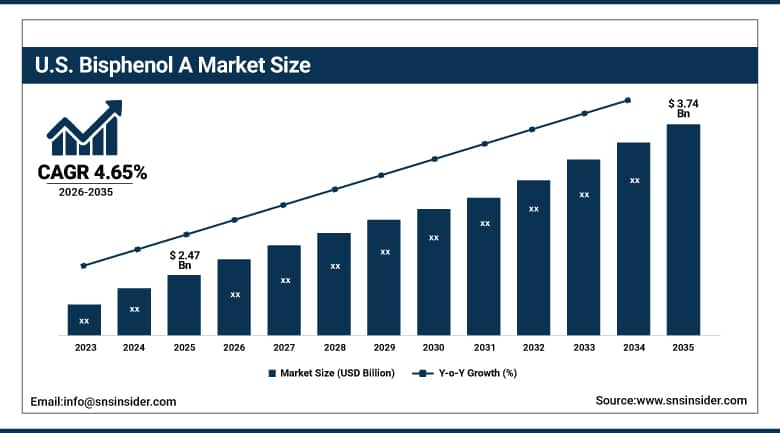

The U.S. Bisphenol A Market Outlook

The U.S. Bisphenol A Market was valued at approximately USD 2.47 Billion in 2025 and is expected to reach approximately USD 3.74 Billion by 2035, growing at a CAGR of approximately 4.65%.

The U.S. is the most commercially important market for bisphenol A in North America due to high demand in the packaging, cosmetics, pharmaceutical, and automobile industries. The existence of leading companies such as Covestro, SABIC, Dow, and Hexion, modern refining processes, and an established petrochemical industry make the U.S. the leader of this market. The increased use of natural and artificial substitutes for BPA due to sustainability practices and regulations in food contact products makes this change the current trend of some end-use markets, while others without regulatory exposure continue to purchase steadily. The regulation of bisphenol A in food contact materials by the FDA has led to a shift to BPA-free packaging in the consumer industry, while the other main drivers of domestic demand include electronics, automobiles, and construction.

In June 2023, INEOS Nitriles launched its bio-based Invireo acrylonitrile with a 90% reduction in greenhouse gas emissions compared to conventionally produced acrylonitrile. While not BPA itself, the launch reflects the broader sustainability direction of the North American industrial chemical sector whose bio-based feedstock investments are influencing BPA derivative producers to develop lower-carbon epoxy resin and polycarbonate formulations that respond to corporate carbon footprint reduction commitments from major downstream customers.

Bisphenol A Market Segment Analysis

-

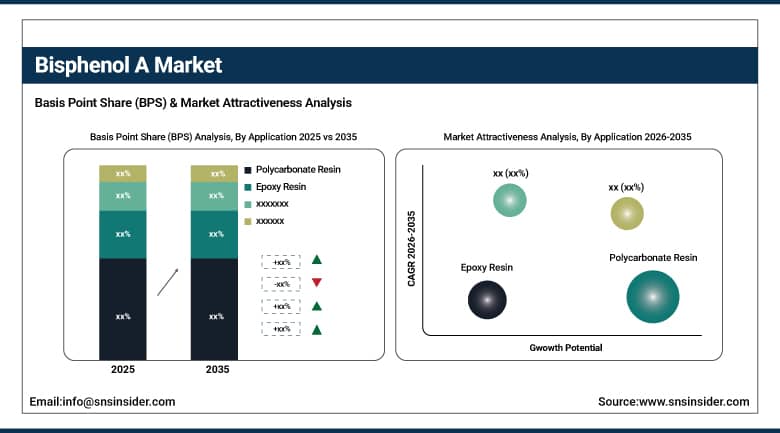

By Application, the polycarbonate resin segment dominated the bisphenol A market with approximately 45% share in 2025, while the polycarbonate resin segment is also the fastest growing.

-

By End Use, the electrical & electronics segment dominated the bisphenol A market with the largest revenue share in 2025, while the automotive segment is the fastest growing as.

By Application, polycarbonate resin dominates and grows fastest

Polycarbonate resin retained the dominant and fastest growing application position with approximately 45% of the bisphenol A market in 2025. The commercial primacy of polycarbonate resin reflects the uniquely comprehensive performance profile that BPA-derived polycarbonate delivers across multiple demanding applications. The automotive industry's systematic adoption of polycarbonate glazing for sunroofs, windows, and headlamp lenses creates commercial procurement proportional to global vehicle production. The consumer electronics sector’s polycarbonate use in laptop housings, tablet back panels, smartphone internal structural components, and electronic connectors creates consistent per-device BPA content that aggregates across billions of units annually. Construction security panels, roofing sheets, and glazing applications in commercial and industrial buildings create another substantial polycarbonate demand stream.

Epoxy resin is the second most commercially significant BPA application, encompassing protective coatings for metal can interiors, structural adhesives for construction and aerospace applications, printed circuit board substrates, and wind turbine blade composites. Each wind turbine installation that uses epoxy resin composite blades creates BPA procurement whose commercial aggregate grows proportionally with global wind energy capacity expansion. The food-contact epoxy can coating application, while subject to regulatory scrutiny for BPA migration, retains widespread use in metal can interiors where no BPA-free alternative delivers equivalent corrosion protection and food safety performance at competitive cost.

By End Use, electrical and electronics dominates, automotive grows fastest

Electrical and electronics retained the dominant end-use position with the largest revenue share of the bisphenol A market in 2025, absorbing more than a quarter of global BPA volume. The electrical and electronics sector's commercial primacy reflects Asia Pacific’s extraordinary electronics manufacturing concentration, where China, Japan, South Korea, and Taiwan's PCB, semiconductor, and consumer electronic device manufacturing industries create the world's most commercially concentrated BPA procurement from a single end-use category. Each new generation of consumer electronics whose miniaturisation creates higher-performance material requirements sustains above-average BPA demand for ultra-pure epoxy resin encapsulants and high-clarity polycarbonate optical components. The growth of 5G network infrastructure, with its extensive PCB and epoxy resin encapsulant demand, creates an additional structural BPA demand driver in the electronics segment.

Automotive is the fastest growing end use because the unprecedented expansion of electric vehicle production creates new BPA-derived material applications beyond conventional internal combustion engine vehicle polycarbonate content. Each EV's battery management system whose high-voltage epoxy encapsulant and polycarbonate cell separator requirements create above-average BPA content per vehicle relative to ICE alternatives. Tesla, BYD, Volkswagen, and GM's combined EV production expansion creates polycarbonate and epoxy resin procurement whose aggregate grows proportionally with the EV production ramp.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Saudi Arabia |

31.2% |

|

Latin America |

Brazil |

44.2% |

Asia Pacific Bisphenol A Market Insights

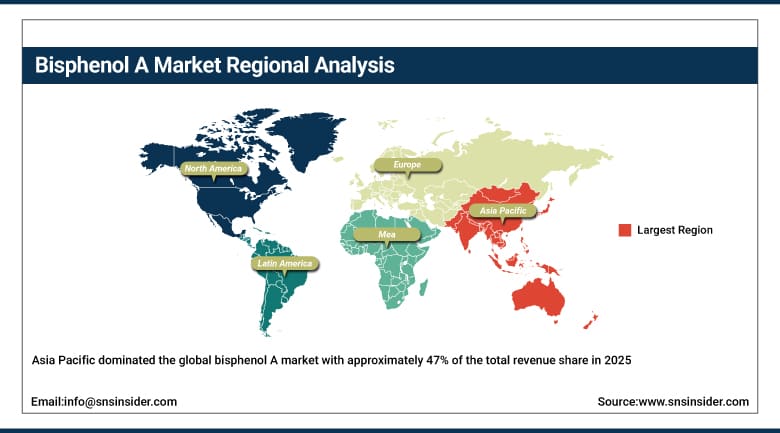

Asia Pacific dominated the global bisphenol A market with approximately 47% of the total revenue share in 2025, driven by China's extraordinary polycarbonate and epoxy resin manufacturing concentration, Japan’s advanced electronics and automotive material demand, South Korea’s consumer electronics sector, and India’s growing construction and packaging industry. China accounts for approximately 44.8% of Asia Pacific revenues through its integrated BPA-polycarbonate supply chain, Wanhua, Qingdao Haiwan, Hengli, and Nan Ya's domestic capacity, and the extraordinary scale of Chinese electronics and automotive manufacturing.

India represents the most commercially dynamic emerging market within Asia Pacific where a USD 37 billion petrochemical industry build-out through 2030, the government's drive to reduce reliance on organic chemical imports, and the rapidly expanding construction, packaging, and automotive sectors create above-average BPA demand growth from a substantial import-dependent base.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Bisphenol A Market Insights

North America is a mature bisphenol A market supported by established polycarbonate and epoxy resin manufacturing, strong automotive and electronics demand, and the presence of major BPA producers including Covestro, SABIC, and Dow. The United States accounts for approximately 87.4% of North American revenues through its integrated petrochemical infrastructure, diverse end-use industry base, and the domestic polycarbonate manufacturing sector that procures BPA for automotive and construction applications.

Canada contributes approximately 12.6% of North American revenues through its construction sector’s epoxy resin demand, the automotive manufacturing sector’s polycarbonate procurement, and the packaging industry’s BPA consumption for metal can coating applications.

Europe Bisphenol A Market Insights

Europe is a technically sophisticated BPA market where the EU's chemical regulatory framework, REACH compliance requirements, and tightening restrictions on BPA in food-contact applications have created formulation shifts toward industrial applications. Germany accounts for approximately 22.3% of European revenues through Covestro's domestic polycarbonate manufacturing, the automotive industry’s epoxy resin demand, and the construction sector’s polycarbonate glazing procurement.

France, the United Kingdom, and Italy are significant secondary markets where the construction sector’s protective coating demand, the automotive manufacturing sector’s polycarbonate procurement, and the packaging industry’s can coating consumption create consistent BPA demand. Europe is anticipated to grow at an above-average CAGR driven by wind energy infrastructure investment creating epoxy resin composite demand.

MEA & Latin America Bisphenol A Market Insights

Saudi Arabia leads MEA revenues through SABIC's domestic BPA and polycarbonate production, the construction sector's epoxy resin demand for protective coatings and structural adhesives, and the growing electronics manufacturing sector. UAE's industrial free zones add complementary Gulf demand. Brazil leads Latin American revenues through its automotive manufacturing sector's polycarbonate and epoxy resin demand, the construction industry's protective coating consumption, and the packaging sector's can coating application. Mexico's automotive manufacturing base and Argentina's construction sector collectively sustain regional market growth through 2035.

Market Dynamics

Growth Drivers: Polycarbonate resin demand from electric vehicle production and electronics manufacturing creating structural above-average BPA procurement

Electric vehicle production expansion is the bisphenol A market's most commercially transformative structural growth driver beyond the baseline industrial demand trajectory. Each EV requires substantially more polycarbonate content than a conventional ICE vehicle through battery management system components, high-voltage connector housings, glazing applications, and exterior panel elements. Global EV production growing from approximately 10 million vehicles in 2022 toward 30 to 40 million annually by 2030 creates polycarbonate demand growth whose BPA procurement aggregate sustains above-market market expansion in the automotive end-use segment.

Electronics manufacturing expansion, particularly 5G infrastructure deployment and consumer electronics demand in Asia Pacific, creates consistent epoxy resin and polycarbonate procurement growth. Each new generation of electronic devices whose PCB density increase and miniaturization create higher-specification epoxy encapsulant requirements sustains BPA demand that grows proportionally with global device production volume.

Restraints: Regulatory restrictions on BPA in food-contact applications and endocrine disruption concerns

Regulatory restrictions on BPA in food-contact applications represent the most commercially impactful market constraint, with EU, U.S., and Canadian regulations prohibiting BPA in baby bottles and restricting its use in food packaging creating formulation substitution trends that erode demand in consumer-facing applications. Each national regulatory action that mandates BPA-free labelling or creates consumer awareness of BPA endocrine disruption concerns creates procurement substitution toward alternative materials in food-contact packaging.

Health concerns regarding BPA's status as an endocrine disruptor create consumer pressure and corporate sustainability commitment that motivate major downstream customers to seek BPA-free formulations even where regulatory mandates do not yet require substitution. Each major consumer goods brand that commits to BPA-free packaging creates supply chain demand substitution that moderates BPA procurement growth in consumer packaging applications.

Opportunities: High-purity BPA grades for semiconductor applications and bio-based BPA development

High-purity BPA grade development for advanced semiconductor packaging represents the most commercially premium near-term market opportunity whose hydrogenated BPA derivatives and ultra-pure epoxy formulations for chip-on-wafer encapsulation create a growing premium product category insulated from food-contact regulatory pressure. The semiconductor packaging market's extraordinary growth driven by AI chip demand creates BPA epoxy resin procurement whose premium specification sustains above-commodity pricing.

Bio-based BPA development represents the most commercially transformative longer-term opportunity whose biomass-derived BPA production via Mitsui Chemicals and Teijin's joint programme creates a sustainability-differentiated product that enables downstream polycarbonate and epoxy resin producers to address corporate carbon footprint commitments without substituting away from BPA-derived material performance.

Recent Developments:

-

2024: Wanhua Chemical Group expanded its BPA production capacity in China in 2024 as part of its integrated polycarbonate manufacturing complex expansion, adding above-average domestic BPA capacity that reinforces China's position as the global production leader for both BPA and downstream polycarbonate resin.

-

2024: Covestro AG commissioned a new high-purity BPA production line at its Krefeld facility in Germany in 2024, targeting electronics-grade polycarbonate applications requiring reduced impurity profiles for optical disc, automotive lens, and semiconductor packaging applications.

-

2023: Nan Ya Plastics announced the launch of a new BPA production line in Ningbo, China in December 2023 with 170,000 tonnes of annual capacity, reinforcing the integrated supply chain investment that supports China's expanding domestic polycarbonate manufacturing.

Bisphenol A Market Key Players are:

-

Covestro AG

-

SABIC (Saudi Basic Industries Corporation)

-

Dow Inc.

-

Mitsui Chemicals Inc.

-

LG Chem Ltd.

-

Chang Chun Group

-

Nan Ya Plastics Corporation

-

Kumho P&B Chemicals Inc.

-

Teijin Limited

-

INEOS Group Holdings SA

-

Momentive Performance Materials Inc.

-

Hexion Inc.

-

China National Bluestar Group Co. Ltd.

-

Samyang Holdings Corporation

-

Vinmar International Ltd.

-

Lihuayi Weiyuan Chemical Co. Ltd.

-

Qingdao Haiwan Chemical Co. Ltd.

-

Wanhua Chemical Group Co. Ltd.

-

Hengli Petrochemical Co. Ltd.

-

PTT Global Chemical PCL

Bisphenol A Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 23.17 Billion |

| Market Size by 2035 | USD 40.87 Billion |

| CAGR | CAGR of 5.84% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Application (Polycarbonate Resin, Epoxy Resin, Flame Retardants, Vinyl Ester Resin, Unsaturated Polyester Resin, Others) • By End Use (Electrical & Electronics, Automotive, Construction, Packaging, Consumer Goods, Healthcare, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Covestro AG, SABIC (Saudi Basic Industries Corporation), Dow Inc., Mitsui Chemicals Inc., LG Chem Ltd., Chang Chun Group, Nan Ya Plastics Corporation, Kumho P&B Chemicals Inc., Teijin Limited, INEOS Group Holdings SA, Momentive Performance Materials Inc., Hexion Inc., China National Bluestar Group Co. Ltd., Samyang Holdings Corporation, Vinmar International Ltd., Lihuayi Weiyuan Chemical Co. Ltd., Qingdao Haiwan Chemical Co. Ltd., Wanhua Chemical Group Co. Ltd., Hengli Petrochemical Co. Ltd., and PTT Global Chemical PCL |

Frequently Asked Questions

The Bisphenol A Market is expected to grow at a CAGR of 5.84% from 2026 to 2035.

Polycarbonate Resin dominated the Bisphenol A Market with approximately 45% share in 2025.

Increasing demand for polycarbonate and epoxy resins across automotive, electrical and electronics, and construction industries, with electric vehicle production expansion creating above-average polycarbonate procurement growth and 5G electronics infrastructure driving sustained epoxy resin demand.

The Bisphenol A Market was valued at USD 23.17 Billion in 2025.

Asia Pacific dominated the Bisphenol A Market in 2025 with the largest revenue share.

Get in Touch