Custom Software Development Market Report Scope & Overview:

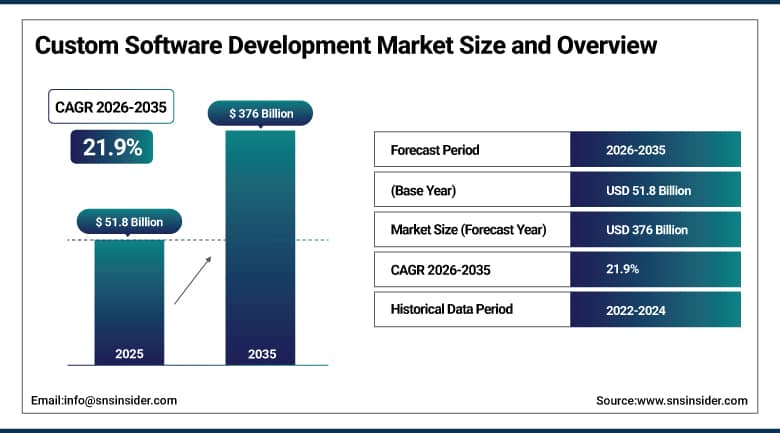

Custom Software Development Market was valued at USD 51.8 billion in 2025 and is expected to reach USD 376 billion by 2035, growing at a CAGR of 21.9% from 2026-2035.

The Custom Software Development market is expanding because of increased demands for custom digital solutions, widespread use of the cloud, increasing digital transformation of enterprises, use of AI and analytics, scalability requirements, and competitive advantage via customized software.

IDC's 2024 Worldwide Software Development Services Forecast documents that enterprise spending on custom software development is growing at 2.3x the rate of packaged software spending reflecting organizational preference for tailored solutions as competitive differentiation becomes increasingly software-dependent. The World Economic Forum's Future of Jobs report identifies software developers as the single occupational category with the largest absolute projected growth in employment globally through 2030.

Custom Software Development Market Size and Forecast

-

Market Size in 2025: USD 51.8 Billion

-

Market Size by 2035: USD 376 Billion

-

CAGR: 21.9% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get More Information On Custom Software Development Market - Request Free Sample Report

Custom Software Development Market Trends

-

AI-assisted code generation tools GitHub Copilot, AWS Code Whisperer, Google Duet AI are accelerating custom development timelines by 30-50% for experienced developers who use them to automate boilerplate code, generate unit tests, and suggest algorithmic approaches.

-

Low-code and no-code development platforms are enabling business analysts and process owners to build custom workflow applications and data integrations without professional developer involvement, expanding the custom software market's reach into organizations without large IT departments.

-

API-first architecture has become the dominant custom development paradigm, enabling custom software to integrate seamlessly with existing enterprise systems and third-party services without custom integration code for each connection.

-

DevSecOps practices are being integrated from the beginning of custom development projects rather than treated as a deployment phase activity, reducing security vulnerabilities in custom applications that have historically been a significant enterprise risk.

-

Edge computing integration is becoming a custom software requirement for manufacturing, logistics, and retail applications where processing latency from cloud roundtrip is unacceptable for real-time operational decisions.

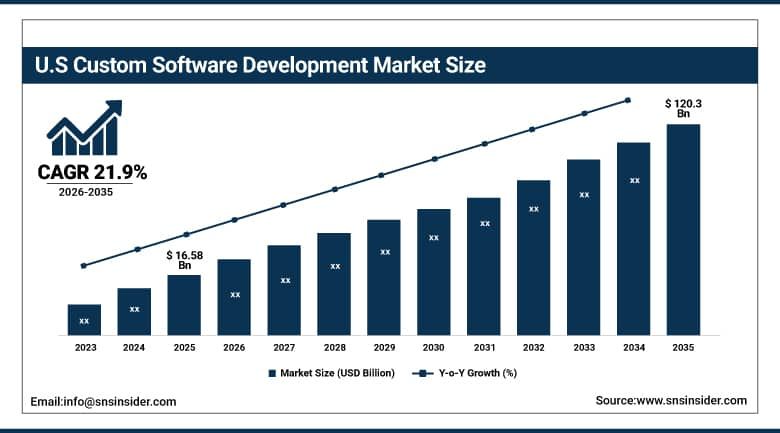

U.S. Custom Software Development Market was valued at USD 16.58 billion in 2025 and is expected to reach USD 120.3 billion by 2035, growing at a CAGR of 21.9% from 2026-2035.

The United States is the world's largest custom software development market, home to the highest concentration of technology companies that both produce and consume custom software, the most sophisticated enterprise technology buyer base, and the global center of software development methodology innovation.

Gartner's 2024 IT Budget Survey documents that North American enterprises allocate an average of 23% of their IT budgets to custom software development and modernization the highest regional proportion globally and nearly double the Asia Pacific average of 13%. Deloitte's State of Custom Software 2024 report found that 74% of U.S. Fortune 500 executives identify proprietary software as a strategic competitive differentiator in their industry.

Custom Software Development Market Segment Analysis

-

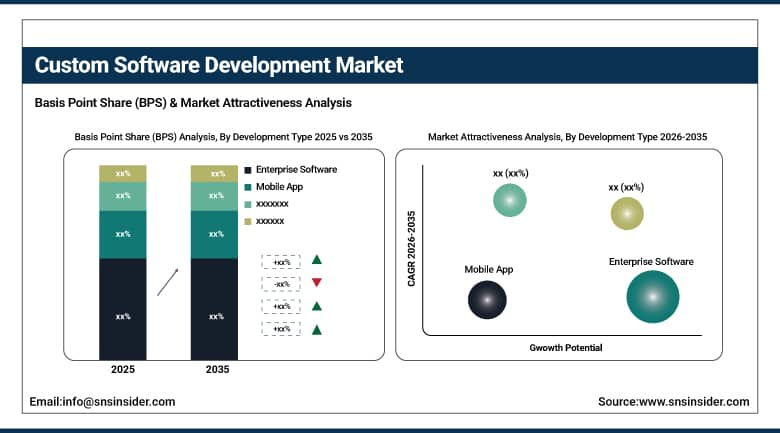

By Development Type, Enterprise Software dominated the Custom Software Development Market in 2025; Mobile App growing fastest (CAGR).

-

By Deployment Mode, Cloud-based dominated the Custom Software Development Market in 2025; On-Premise maintaining position in regulated industries.

-

By Enterprise Size, Large Enterprises dominated the Custom Software Development Market in 2025; SMEs growing fastest (CAGR) with accessible platforms.

-

By Industry Vertical, IT & Telecom dominated with ~24% share in 2025; Government fastest growing at ~24.18% CAGR.

By Development Type: Enterprise Software dominates, Mobile App growing fastest

Enterprise Software held the dominant development type position in the Custom Software Development Market in 2025, encompassing the custom ERP integrations, proprietary CRM implementations, supply chain management systems, data analytics platforms, and operational technology software that organizations build when off-the-shelf alternatives cannot serve their specific requirements. The enterprise software custom development market is characterized by high project values averaging USD 500,000 to USD 10 million per engagement for significant implementations long development timelines, complex stakeholder environments, and deep integration with existing systems and data architectures.

Mobile App is growing at the fastest development type CAGR, driven by the ubiquity of smartphones as the primary interaction point for consumers with commercial and government services and as the preferred work tool for field service, logistics, retail, and healthcare workers who require mobile-optimized workflows. Custom mobile applications built for iOS and Android ranging from enterprise field service management apps to consumer-facing loyalty programs to clinical decision support tools for physicians represent development investments that generic app frameworks cannot adequately serve because the competitive advantage they provide depends on specific functionality that competitors cannot simply license from the same platform vendor.

By Deployment Mode: Cloud dominates, On-Premise maintaining regulated industry presence

The default architectural pattern for any custom application software development in 2025 will be cloud deployment due to the benefits that come with cloud infrastructure when developing custom software applications. The provision of scalable computing and storage capacity according to the actual requirements of the system instead of provisioning for maximum requirements on dedicated servers makes it more economical to deploy systems in the cloud where actual demand is variable, while at the same time providing optimal performance when the demands are highest. Cloud deployment will save organizations from investing in expensive server hardware.

On-premise deployment maintains its position in regulated industries defense, intelligence, banking, healthcare processing, and critical infrastructure where data sovereignty requirements, regulatory mandates, or security classifications preclude cloud processing of specific data categories. The defense and intelligence sector's air-gapped computing requirements make on-premise the only viable deployment option for classified applications. Financial sector custom applications processing trading data or managing core banking ledgers often maintain on-premise components for latency, data custody, or regulatory reasons even when peripheral applications are cloud-deployed.

By Enterprise Size: Large Enterprises dominate, SMEs growing fastest

Large enterprises maintained their dominant position as the primary custom software development buyers in 2025, because the custom development investment case which requires amortizing development costs across large user populations, justifying complex integrations with existing systems, and sustaining ongoing maintenance teams works most favorably for organizations with scale, financial capacity, and operational complexity that makes custom solutions worth the investment over off-the-shelf alternatives. Fortune 500 enterprises routinely maintain internal development teams of hundreds or thousands of engineers building and maintaining proprietary software alongside partnerships with technology services firms for capacity scaling and specialized skill access.

The SMEs are experiencing the highest rate of growth by CAGR compared to other enterprise sizes due to the democratization of software development economics by cloud infrastructure, open-source architectures, and low-code platforms for developing software. An application that may have taken US$500,000 worth of resources to build back in 2010 now only costs US$50,000-US$100,000 thanks to advanced cloud-based development software and services. The lowering of costs is resulting in the increase of proprietary software development within the mid-market firms, whose revenues are ranging from US$10 million to US$500 million.

By Industry Vertical: IT & Telecom dominates, Government growing fastest

IT & Telecom held approximately 24% of the Custom Software Development Market's industry vertical breakdown in 2025, reflecting the self-consuming nature of technology companies' software development investment technology firms build custom software both for their own operational needs and as the commercial products they sell to others, creating a uniquely dense concentration of development investment within the sector. Telecom operators build custom operational support systems (OSS), business support systems (BSS), network management platforms, and customer experience applications that their vendor ecosystem cannot adequately serve because the complexity and scale of each operator's network environment creates requirements too specific for generic products to address.

Government is the fastest-growing industry vertical at approximately 24.18% CAGR, driven by digital government transformation programs across federal, state, and local levels globally. The U.S. federal government's Technology Modernization Fund, the UK's Government Digital Service, India's Digital India program, and equivalent initiatives across dozens of other national governments are systematically directing government IT investment from legacy system maintenance toward custom digital service delivery platforms, citizen engagement portals, AI-powered regulatory compliance tools, and open-source government digital infrastructure.

Custom Software Development Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

85% |

|

Asia Pacific |

India |

32% |

|

Europe |

Germany |

22% |

|

Middle East & Africa |

UAE |

35% |

|

Latin America |

Brazil |

50% |

North America Custom Software Development Market Insights

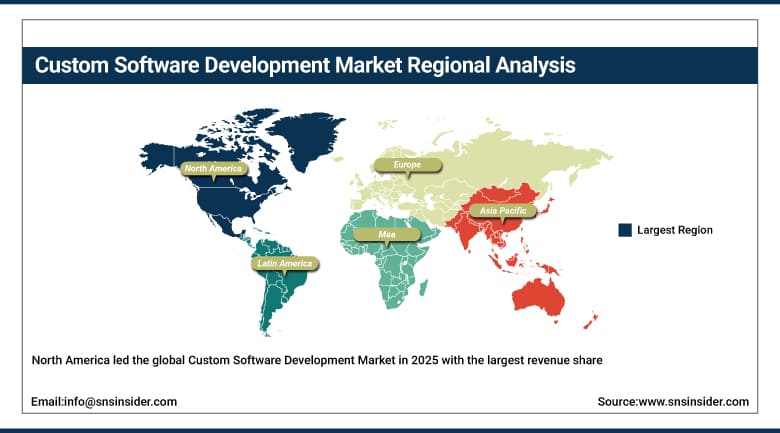

North America led the global Custom Software Development Market in 2025 with the largest revenue share, anchored by the United States' extraordinary enterprise technology investment and the highest concentration of technology services firms globally. The U.S. market's maturity is reflected in the diversity of custom development engagements it supports from billion-dollar financial system modernizations at major banks to USD 50,000 startup MVP builds at Series A companies, from defense department proprietary application development to small retailer custom loyalty program builds. American enterprises' cultural comfort with technology investment as competitive differentiation, their access to sophisticated development talent both domestically and through outsourcing, and the financial depth to sustain multi-year software modernization programs collectively sustain a custom development market density unmatched in any other geography.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific Custom Software Development Market Insights

Asia Pacific is the fastest-growing regional Custom Software Development Market, driven by the dual forces of India's world-dominant technology services industry and the region's rapidly expanding domestic digital economy creating internal custom development demand. India's IT services industry generating over USD 220 billion in annual revenue — is the primary delivery center for custom software development outsourced by North American, European, and Asia Pacific enterprises, positioning India as simultaneously the world's largest exporter and growing domestic consumer of custom development services. Companies including Tata Consultancy Services, Infosys, Wipro, HCL Technologies, and hundreds of mid-tier firms collectively employ over 5 million software developers who execute custom development programs for global clients. China's enormous domestic enterprise digital transformation investment, South Korea's smart manufacturing software programs, and Australia's government digital transformation initiatives add substantial regional custom development demand beyond India's outsourcing-driven contribution.

NASSCOM reports that India's technology services industry added 290,000 net new employees in fiscal year 2024, with custom software development services representing the fastest-growing service line. China's Ministry of Industry and Information Technology's Software Industry Development Report documents that China's domestic custom software market grew to CNY 1.2 trillion (approximately USD 170 billion) in 2023.

Europe Custom Software Development Market Insights

Europe's Custom Software Development Market is characterized by strong enterprise demand for custom applications in highly regulated industries banking, insurance, healthcare, and industrial manufacturing where compliance requirements create software specificity needs that off-the-shelf products cannot satisfy. Germany's industrial sector Siemens, Volkswagen, BASF, and thousands of Mittelstand manufacturers sustains large custom industrial software development programs for production optimization, quality management, and supply chain digitalization. The UK has developed a sophisticated fintech software development ecosystem, with London's financial technology cluster producing more custom financial software than any comparable geographic concentration outside New York. GDPR compliance requirements create a distinctive European custom development driver: organizations needing to build consent management, data subject rights fulfillment, and privacy-by-design architectures that off-the-shelf alternatives do not provide with adequate jurisdiction-specific compliance certainty.

Middle East & Africa and Latin America Custom Software Development Market Insights

The Middle East's custom software development market is growing rapidly, driven primarily by Saudi Arabia's Vision 2030 digital economy investment and the UAE's established position as a regional technology hub. Saudi Arabia's government digital transformation programs including Absher citizen services platform, Tawakkalna health application, and numerous smart city management systems represent large-scale custom software development investments coordinated by the Saudi Digital Government Authority. Dubai's Smart City program has generated custom software development investment across transport management, government services, and public safety systems that positions it as the Middle East's most advanced digital government implementation. Africa's custom software development market is nascent outside South Africa and Nigeria, where growing technology startup ecosystems and mobile-first application development are creating custom software investment beyond the legacy enterprise market.

Custom Software Development Market Growth Drivers:

-

Digital transformation urgency and AI integration demand driving unprecedented global custom software development market growth

The custom software development market's 21.9% CAGR is driven by the convergence of a business environment where software capability determines competitive positioning with a technology environment where AI is transforming what software can do and how quickly it can be built. Organizations that would previously have accepted off-the-shelf software's limitations are finding that those limitations now cost them customers, operational efficiency, and competitive position in ways that justify custom development investment. Simultaneously, AI is both an accelerator AI-assisted development reduces custom software build time and cost and driver AI integration requirements are so specific to each organization's data, workflows, and competitive context that off-the-shelf AI products rarely serve these needs adequately, creating a new category of AI-powered custom software demand.

Custom Software Development Market Restraints:

-

High development costs and cybersecurity complexity limiting custom software development adoption among SMEs globally

Custom software's cost disadvantage relative to off-the-shelf alternatives is not merely a perception challenge it is real and significant for organizations whose scale cannot amortize development investment across large user populations or high transaction volumes. A CRM system that a large enterprise can build for USD 2 million and use for 10,000 employees costs the same per-hour of development but cannot be spread across 50 employees at a small business, making per-user economics prohibitive. Data security complexity in custom software creates a second constraint: custom applications must implement authentication, authorization, encryption, and vulnerability testing without benefiting from the security investment that commercial software vendors have made in their products across millions of customers. When a custom application's security fails, the organization bears the full reputational and regulatory cost without a vendor to share accountability.

Custom Software Development Market Opportunities:

-

AI-powered development automation and government digital transformation creating transformative custom software market growth opportunities globally

AI-powered development automation where AI generates code, tests software, creates documentation, and suggests architectural improvements is the most commercially significant productivity multiplier that the custom software development market has encountered in its history. GitHub Copilot's enterprise adoption has demonstrated at commercial scale that AI assistance reduces time-to-completion for common development tasks by 30-55% for experienced developers. As these tools mature into more capable AI software engineers that can handle increasingly complex development tasks, the economics of custom software development will shift in ways that make it viable for organizations and project types where the cost has previously been prohibitive. Government digital transformation represents the most visible large-scale custom development opportunity globally governments have the largest legacy system portfolios, the most urgent modernization needs, and the political and financial commitment to invest in digital service delivery that citizens increasingly expect.

Recent Developments:

-

2026: Microsoft expanded its GitHub Copilot Workspace capability to support full feature development cycles from natural language feature specification through code generation, testing, and pull request creation reducing the developer effort for standard feature implementation by an estimated 60% and positioning Copilot Workspace as the dominant AI-powered custom development tool for enterprise development teams.

-

2025: Accenture launched its AI Refinery custom software factory model, combining Nvidia's AI computing infrastructure, Microsoft Azure cloud development tools, and Accenture's industry-specific solution templates to enable enterprise clients to build proprietary AI-powered custom applications within 90-day delivery cycles for standard use cases less than half the conventional custom development timeline for equivalent scope.

Custom Software Development Market Key Players

Some of the Custom Software Development Market Companies

-

Microsoft Corporation

-

IBM Corporation

-

Accenture plc

-

Tata Consultancy Services Ltd.

-

Infosys Ltd.

-

Wipro Ltd.

-

HCL Technologies Ltd.

-

Capgemini SE

-

Cognizant Technology Solutions Corp.

-

Tech Mahindra Ltd.

-

Fujitsu Ltd.

-

SAP SE

-

Oracle Corporation

-

Salesforce Inc.

-

ServiceNow Inc.

-

Epam Systems Inc.

-

Globant SA

-

Grid Dynamics Holdings Inc.

-

Perficient Inc.

-

Thoughtworks Holding Inc.

Custom Software Development Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 51.8 Billion |

| Market Size by 2035 | USD 376 Billion |

| CAGR | CAGR of 21.9% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Development Type (Web-based Solutions, Mobile App, Enterprise Software) • By Deployment Mode (Cloud-based, On-Premise) • By Enterprise Size (Large Enterprises, SMEs) • By Industry Vertical (IT & Telecom, Government, Healthcare, BFSI, Retail, Manufacturing, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Microsoft Corporation, IBM Corporation, Accenture plc, Tata Consultancy Services Ltd., Infosys Ltd., Wipro Ltd., HCL Technologies Ltd., Capgemini SE, Cognizant Technology Solutions Corp., Tech Mahindra Ltd., Fujitsu Ltd., SAP SE, Oracle Corporation, Salesforce Inc., ServiceNow Inc., Epam Systems Inc., Globant SA, Grid Dynamics Holdings Inc., Perficient Inc., Thoughtworks Holding Inc. |

Frequently Asked Questions

Ans: North America dominated the Custom Software Development Market in 2025.

Ans: Mobile App development is expected to register the fastest CAGR in the Custom Software Development Market through 2035.

Ans: IT & Telecom dominated with approximately 24% share in 2025; Government is the fastest growing at ~24.18% CAGR.

Ans: The Custom Software Development Market was valued at USD 51.8 billion in 2025.

Ans: The Custom Software Development Market is expected to grow at a CAGR of 21.9% from 2026 to 2035.

Get in Touch