Quantum Cryptography Market Report Scope & Overview:

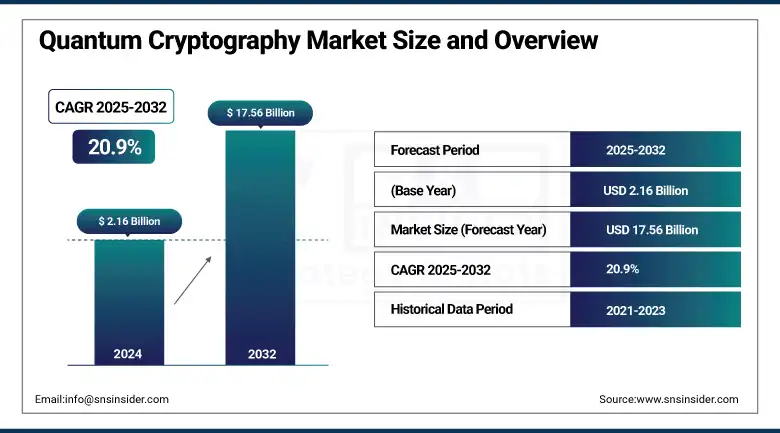

The Quantum Cryptography Market size was valued at USD 2.16 billion in 2024 and is expected to reach USD 17.56 billion by 2032, expanding at a CAGR of 20.9% over the forecast period of 2025-2032.

The growing cybersecurity concerns, along with the inability of classical encryption to stand against future quantum attacks, are the factors available for the rapid growth of the market. This technology employs quantum mechanics principles to carry out the ultimate secure data transmission through Quantum Key Distribution. High levels of adoption across prominent sectors, with stringent data privacy regulations driving it. The high prices and dedicated hardware pose some serious issues, but R&D continues to balance the accessibility and change prices to make them lower and embrace something more scalable. The U.S. and Europe dominate the market, while Asia-Pacific is the fastest-growing region. In conclusion, quantum cryptography will bring a paradigm shift in secure communications across the globe.

To Get more information On Quantum Cryptography Market - Request Free Sample Report

According to research, over 80 quantum-resilient algorithms have been submitted to NIST, yet only 12% of Fortune 500 firms are quantum-ready, despite quantum computing potentially cracking RSA-2048 encryption in just 8 hours.

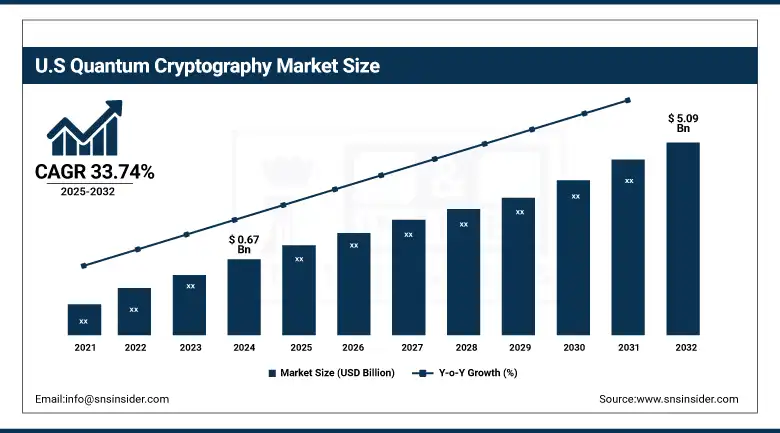

The U.S Quantum Cryptography Market size reached USD 0.67 billion in 2024 and is expected to reach USD 5.09 billion in 2032 at a CAGR of 33.74% from 2025 to 2032.

The U.S. maintains dominance in the global market due to dynamic investments in quantum research, extensive cybersecurity infrastructure, and the adoption of post-quantum encryption in government and defense. The primary factors include growing incidences of data theft, increasing cyber threats due to emerging quantum computing capabilities, and stringent regulations specific to data protection. In addition to that, tech giants, startups, and federal agencies keep on driving innovation together through collaborations. Moreover, the rise in demand for secure communications in essential industries such as finance, healthcare, and military is expected to bolster quantum cryptography market growth throughout the nation.

Quantum Cryptography Market Dynamics

Drivers:

-

Growing Demand for Unbreakable Encryption Systems Across Government and Defense Drives Market Growth.

This expansion is driven by the rising requirement for break-proof encryption systems in various aspects, including government, defense, and banking. By using the principles of quantum mechanics, quantum cryptography provides a level of security that is almost impossible to hack, even for quantum computers. For instance, investments by the U.S. Department of Defense have begun to flow, while major technology firms have initiated quantum communication pilot networks. The new enhancements highlight a national focus on bolstering national cyber defense. Additionally, quantum key distribution (QKD) for the protection of sensitive information is gaining traction, creating demand in numerous high-risk sectors.

According to research, over 60% of quantum cryptography deployments in 2024 occurred within the government, defense, and financial services sectors.

Restraints:

-

High Cost of Deployment and Infrastructure Limits Widespread Adoption in Budget-Constrained Sectors.

The available quantum cryptography systems are still expensive and well beyond the financial reach of most organizations, and particularly, small and medium-sized enterprises (SME). The need for infrastructure, along with specific hardware, which requires money and resources to be mounted in the core space, also. Even though there is an increased awareness of sand as a solution, the access to solutions that are more affordable and could be scaled prohibit more wide spread marketing of sand, rather than the same familiar solutions. In addition, the lack of trained professionals and continued R&D efforts in the field make its implementation only affordable to well-funded sectors like defense and high-end finance for now.

Opportunities:

-

Rising Integration of Quantum Networks in Commercial Telecommunications Opens New Avenues for Growth.

The incorporation of quantum networks into commercial telecommunications generates enormous prospects for expansion. Telecom companies are looking into quantum key distribution (QKD) solutions to encrypt and protect transmission of data over fiber optic networks, and are starting to deploy such technology. The real contest is already on to defend against futuristic quantum computer-based cyber threats, which is what is driving this transition. In recent months, this includes quantum networking tests done jointly by AT&T and academic institutions to develop a quantum secure communications infrastructure with potentially compatible protocols between carrier operations and quantum technology manufacturers.

Challenges:

-

Technical Complexity and Interoperability Issues Pose Challenges to Practical Implementation Across Existing Systems.

The technical sophistication and inability to interface with out more classic communication infrastructure has made it one of the typical challenges towards the implementation of quantum cryptography. Legacy systems may by design require integration with legacy systems, but quantum systems require higher precision than usual, such as operating at low temperature or synchronization, making them more difficult to integrate. There are still no standardized quantum communication protocols, resulting in fragmentation in quantum science and technology development and their deployment.

Quantum Cryptography Market Segmentation Analysis

By Component

In 2024, the software segment holds the largest revenue share of 47.30%, owing to the increasing number of enterprises and government organizations that are adopting quantum key distribution (QKD) platforms and encryption software. Quantum cryptographic software is advancing rapidly as demand for high-security encryption grows, with firms like ID Quantique and QuintessenceLabs developing innovative QKD suites and SDKs. This segment is primarily driven by a strong demand to protect the data that is at risk of compromise in the not-too-distant quantum future, resulting in critical ends in both the banking and national defense industries.

The services segment is expected to grow at the fastest rate of 36.13% due to an increase in the requirement for consulting, integration, and support services during the deployment of quantum cryptographic systems. Quantinuum and others highlight challenges in scaling quantum technology, prompting service providers like Toshiba and Quantum Xchange to expand quantum-resilient security services, including recent partnerships offering QKD-as-a-service with telecom operators. This segment is mainly driven by the rising demand for professional assistance in operationalizing quantum solutions that allow a smooth transition from classical to quantum-secure systems in enterprise security frameworks.

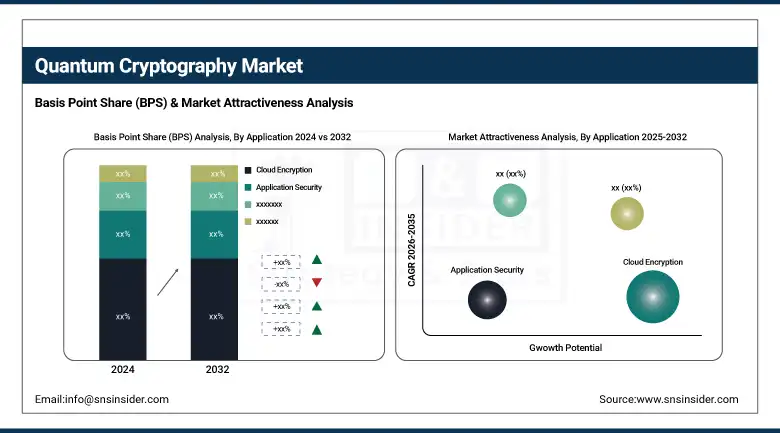

By Application

The cloud encryption segment accounted for the largest revenue share of 33.98% in 2024, attributed to increasing cloud adoption and the rising demand for securing data in distributed networks. This resurgence in quantum computing threat awareness, however, has also revealed technical solutions to this issue, leading cloud service providers such as Google Cloud and Microsoft Azure to begin testing quantum-safe encryption tools to address the vulnerabilities of traditional cloud encryption tools. Amazon Web Services (AWS) also recently announced its plans to incorporate quantum-resistant algorithms into its cloud platforms.

The application security segment is anticipated to grow at the fastest CAGR of 35.92%. This growth is primarily driven by to increasing number of sophisticated cyberattacks on enterprise application software, which is to prepare digital assets for the future, quantum cryptographic solutions are being progressively deployed as part of secure application development. Developers Arqit and SandboxAQ are creating post-quantum cryptographic APIs for software developers to integrate into their applications. The main driving force is a greater emphasis on secure-by-design approaches in DevSecOps practices to be resilient to quantum-era threats.

By Industry

In 2024, the BFSI sector held the largest Quantum Cryptography Market share of 27.21%, due to its early adoption of quantum cryptography, protecting transactions, client data, and interbank communications. Financial institutions are implementing QKD systems and quantum-safe encryption to mitigate new cybersecurity risks. For example, JPMorgan Chase has partnered with Toshiba and Ciena for quantum key distribution tests. The need for continuous and seamless data security solutions in the quantum cryptography industry is facing an increased quantum of cyber-attacks, and high growth of this segment can be seen for strict data protection regulations.

Healthcare & life sciences is anticipated to record the fastest CAGR of 38.32% throughout the forecast period, owing to the increasing use of digital records, telemedicine, and the exchange of health data. Quantum cryptography would allow for safe use of patient data in clinical trials and the protection of biomedical research from future computing attacks. QuantumCTek and QNu Labs have linked up with healthcare providers to test secure data transfer systems based on QKD. The most critical factor is a rise in ransomware and data breaches within the healthcare market, which, in turn, translates into capital invested in next-gen cybersecurity frameworks.

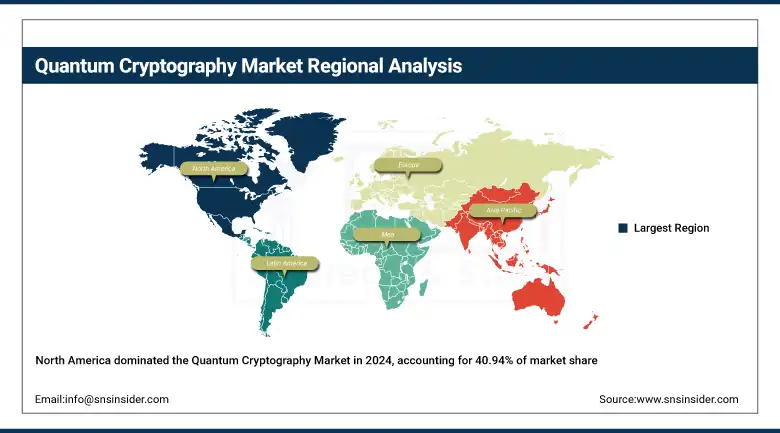

Quantum Cryptography Market Regional Analysis

North America leads the market revenue share of 40.94%, owing to substantial investments in quantum research and advanced cybersecurity infrastructure with strong government support. Innovation in quantum key distribution (QKD) and quantum-resistant encryption technologies in the finance, defense and healthcare sectors will speed up due to the near presence of major technology firms and defense contractors.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. dominance in the region is due to having early research & commercializing quantum technologies, the provision of federal funding initiatives, and strategic cooperation between tech firms & research institutions with government agencies.

Europe has taken a huge leap with the European Union quantum flagship initiative. at the national level, for instance, Germany and France have put a lot of public money in this field, boosting work in quantum cryptography. From developing scalable quantum communication infrastructure to deploying quantum-safe technologies in telecommunications and in public sector use cases, we see a lot of activity from both research institutions and private firms around the globe.

Germany, with its ongoing research and development, is a leader in quantum technologies, government-led innovation projects, and cooperation between universities and top quantum companies, dominating the European market.

Asia Pacific is at a rapid pace to emerge as a key region in the cryptography market with a CAGR of 36.54%, due to growing investment in quantum research and increasing awareness towards cyber threats, Per the Article, National quantum initiatives are being prioritized in countries such as China, Japan, and South Korea, and the roll-out of quantum secure communication networks is in progress.

This region is dominated by China because of massive government funding, successful satellite-based quantum communication experiments, and progress in quantum hardware and software.

Middle East & Africa and Latin America markets are in the early adoption phase of quantum cryptography technology and it can be mainly attributed to the ongoing digital transformation coupled with smart city initiatives and increasing awareness for cyber security among organizations in this district, with the UAE & Brazil leading the bifurcation by engaging with strategic investment and global collaboration.

Key Players

The major key players of the Quantum Cryptography Market are Toshiba, Thales, ID Quantique, IBM, Palo Alto Networks, QuantumCtek, Quintessence Labs, NXP Semiconductors, DigiCert, MagiQ Technologies, and others.

Recent Developments

-

In March 2025, Toshiba EMEA incorporated Post-Quantum Cryptography (PQC) and Quantum Key Distribution (QKD) into its offerings, providing a strong, end-to-end solution for quantum-safe networking across industries.

-

In January 2024, Thales, in collaboration with Quantinuum, launched a Post-Quantum Cryptography (PQC) Starter Kit, which allows businesses to rapidly evaluate and improve their quantum-safe encryption preparedness and security infrastructure.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 2.16 Billion |

| Market Size by 2032 | USD 17.56 Billion |

| CAGR | CAGR of 20.9% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Component (Appliances, Software, Services) •By Application (Network Encryption, Database Encryption, Application Security, Cloud Encryption) •By Industry (BFSI, Healthcare & Life Science, Government & Defense, IT & Telecom, Energy & Utilities, Retail & e-Commerce, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Toshiba, Thales, ID Quantique, IBM, Palo Alto Networks, QuantumCtek, Quintessence Labs, NXP Semiconductors, DigiCert, MagiQ Technologies |

Frequently Asked Questions

North America dominated the Quantum Cryptography Market in 2024, accounting for the largest revenue share of 40.94%, due to strong government support, advanced cybersecurity infrastructure, and extensive quantum R&D.

The Software segment dominated the Quantum Cryptography Market by component in 2024, holding a 47.30% revenue share, driven by high adoption of QKD platforms and quantum encryption tools by enterprises and government entities.

The major growth factor driving the Quantum Cryptography Market is the growing demand for unbreakable encryption systems, especially in government, defense, and BFSI sectors, due to increasing threats from quantum computing.

The market size of the Quantum Cryptography Market in 2024 was valued at USD 2.16 billion.

The Quantum Cryptography Market is expected to grow at a CAGR of 20.9% from 2025 to 2032.

Get in Touch