CyberSecurity Insurance Market Report Scope & Overview:

Get more information on Cybersecurity Insurance Market - Request Sample Report

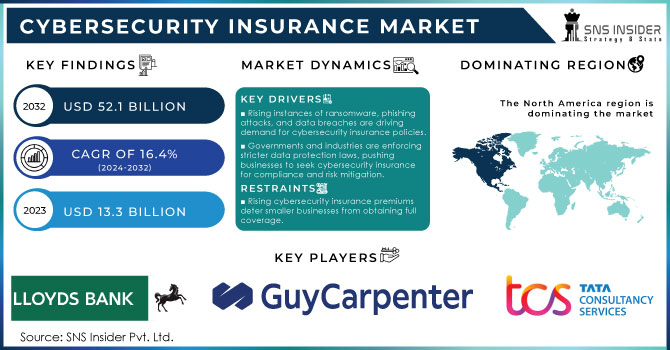

Cybersecurity Insurance Market Size was valued at USD 13.3 Billion in 2023 and is expected to reach USD 52.1 Billion by 2032, growing at a CAGR of 16.4% over the forecast period 2024-2032.

The cybersecurity insurance market is driven by the rising number of cyberattacks and data breaches, with governments globally taking action to mitigate the risks. According to the latest statistics from the U.S. Department of Homeland Security (DHS), cyberattacks in the U.S. increased by 27% in 2023 compared to the previous year, largely affecting financial institutions and healthcare sectors. In US the data breaches will increase 78% in 2023 as compared to 2022. The European Union Agency for Cybersecurity (ENISA) also reported a 20% increase in ransomware attacks across Europe in 2023. This has led to heightened awareness among businesses and governments regarding the need for cybersecurity insurance to mitigate the financial impact of data breaches. Additionally, various national and international regulatory bodies, such as the U.S. Federal Trade Commission (FTC) and the General Data Protection Regulation (GDPR) in Europe, have set stringent compliance requirements. These mandates incentivize organizations to purchase cybersecurity insurance policies, driving market growth further. Government funding for cybersecurity resilience and risk mitigation programs has also seen a significant uptick, contributing to the expansion of the cybersecurity insurance market.

Cyberattacks are on the rise globally, with many individuals, enterprises, and governments losing a lot of money because of these threats. Criminals are targeting a variety of IT infrastructures for political, financial, radical reasons, and others. The ransomware attacks that targeted thousands of organizations include SamSam, Petya, and WannaCry attacks. Atlanta city was also a victim of ransomware that left the administration with a demand to pay $50,000 by SamSam. Businesses are the biggest casualties of these emerging threats and thus, the best way to protect the most important IT infrastructure and data from any malicious attack. Besides the increased number and complexity of attacks, organizations are also spending a lot of money on cybersecurity products and services. The most notable trend is the high cybersecurity insurance buying rate by the different organizations that shield them from huge financial losses because of cyberattacks. About 40% of the breaches affect multiple environments, increasing the breach cost to slightly under $4.75 million. Breach costs will also affect the healthcare sector, affecting $11 million by 2023. However, the cost of critical infrastructure breaches is slightly above $5 million, increasing the cybersecurity cyber defense demand.

Market dynamics

Drivers:

-

Rising instances of ransomware, phishing attacks, and data breaches are driving demand for cybersecurity insurance policies.

-

Governments and industries are enforcing stricter data protection laws, pushing businesses to seek cybersecurity insurance for compliance and risk mitigation.

-

As businesses embrace cloud computing, Internet of Things (IoT), and remote work, they face heightened cybersecurity risks, boosting the need for insurance coverage.

-

Small and medium-sized enterprises are increasingly recognizing the importance of cybersecurity insurance as they become frequent targets of cyberattacks.

The rapid increase in the frequency and severity of cyberattacks and data breaches across industries is one of the major factors driving the cybersecurity insurance market. Cybercriminals are growing more sophisticated and employ a multitude of methods such as ransomware, phishing, and malware to affect and harm organizations of any size. According to a recent study, ransomware attacks across the globe increased 37 percent in 2023. The attack frequency sufficiently affected critical businesses including but not limited to healthcare, finance, and education. Data shows numerous colossal events occurred recently highlighting the pressing need for cybersecurity insurance. For instance, in May 2023, the MOVEit ransomware attack impacted over 1,000 organizations and released sensitive information to the public. It includes personal data from various businesses and government enterprises. Furthermore, MGM Resorts was targeted during a cyberattack in September 2023. The data leakage caused financial loss, affected customer reputation, and parallaxed company operations with staggering expenses and lawsuits.

The average cost of a data breach event reached $4.45 million, as compared to $4.24 million in 2022. The expense of financial loss drives organizations to seek cybersecurity insurance as a protective mechanism. It covers noticeable shares of the expenses related to incident response, legal fees, and reputation damage. With cyberattacks becoming more frequent and costly, companies are increasingly turning to cybersecurity insurance as a safeguard against the unpredictable and growing financial impacts of cybercrime, further fuelling the demand for coverage.

Restraints:

-

The rising cost of cybersecurity insurance premiums, especially for full-coverage policies, deters smaller businesses from purchasing adequate protection.

-

The absence of standardized policy frameworks and definitions complicates the underwriting process, leading to inconsistent coverage and creating challenges for policyholders.

-

Insurers face challenges in accurately assessing risk due to the evolving nature of cyber threats and limited historical data on cyber incidents, which can impact the cost and scope of policies.

One of the major restraints in the cybersecurity insurance market is the lack of standardization of policy frameworks and definitions. Cyber insurance policies vary widely in terms of coverage, definitions of cyber incidents, and the scope of protection offered. This inconsistency can create confusion for businesses, particularly when they need to file claims. Lack of a clear standard on an industry level or national level makes it problematic for businesses to understand whether they are protected correctly and play into the hands of the insurer during disappointment consideration matters. Many insurers may have varying understandings of ‘cyber incidents’ and ‘related events’ mentioned in their policy. This could lead to potentially legal battles with the insurer when the insured files a claim. As a result of such a lax framework, underwriters are forced to engage in the permanent redefinition of risks and the development of products for each new client. This led to significant delays in policy execution. Therefore, on the shortage of businesses purchasing cybersecurity insurance or purchasing it in inadequate scopes and with insufficient coverage.

Market Segmentation

By Insurance Type

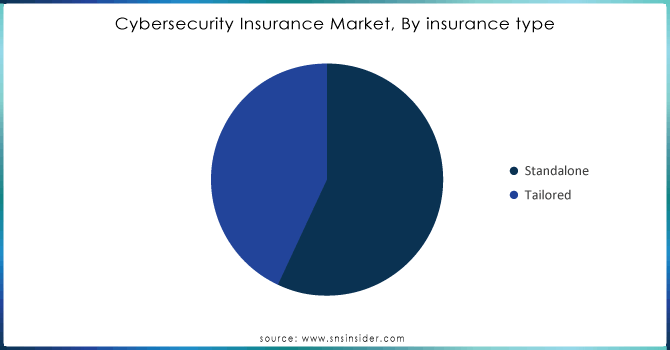

The standalone segment dominated the market in 2023, due to the comprehensive cover against cyber risk and because of its use among large enterprises. According to The U.S. In 2023, this type of insurance contributed to 58% share of the cybersecurity insurance market. Standalone cyberspace insurance provides broad protection against multiple cyber risks, ranging from data breaches to ransomware and business interruptions. In response to the numerous reports about cyber breaches in the past few years, organizations are increasingly selecting this type of insurance as the most effective maintenance of robust protection. However, the tailored segment is estimated to account for the highest compound annual growth rate in insurance type in the forecast period. According to The U.S. Small Business Administration’s data, SMEs account for 99.9% of all U.S.-based businesses. More and more of these organizations and companies within particular sectors, such as healthcare and retail, are selecting the cyber insurance marketed to meet their specific needs as cheaper, and more focused on their vulnerabilities. This growing preference is expected to drive the tailored segment’s rapid expansion.

Need any customization research on Cybersecurity Insurance Market - Enquiry Now

By Insurance Coverage

The cyber liability segment held a larger market share by insurance coverage. Cyber liability insurance accounted for 52% share of the market in 2023. The coverage primarily accounts for costs related to data breaches, including legal defense, public relations, notification of customers, and other costs. As businesses face increasing regulatory scrutiny, such policies are becoming critical to mitigating the financial and reputational damage caused by cyber incidents. The implementation of stringent data protection laws, like the California Consumer Privacy Act (CCPA) and GDPR, is further boosting the demand for cyber liability insurance, as non-compliance can result in hefty fines. The government’s push for stronger cybersecurity standards in the private sector is another factor driving demand for cyber liability policies.

Regional Analysis

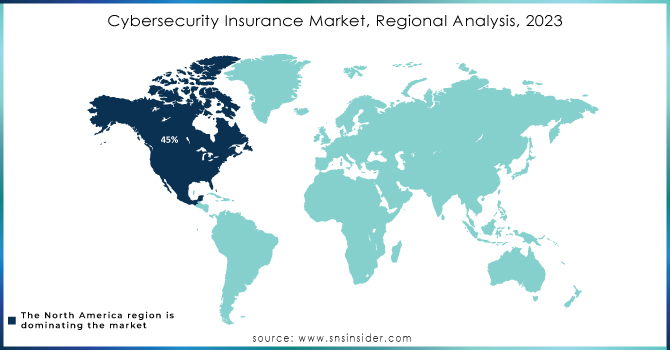

North America has led the cybersecurity insurance market in 2023 with a 45% share of the global market. The region dominates the market due to the high incidence of cyberattacks and stringent regulations. According to the Cybersecurity and Infrastructure Security Agency, the U.S. alone experienced over 2,500 significant attacks in 2023, leading to nearly $6.2 billion in losses. North America’s advanced technology infrastructure is a lucrative target for perpetrators, which has resulted in further market growth. Owing to the numerous threat actors in the area, such as Russia, North Korea, Iran, and China, insurance providers are able to deliver a large number of insurance schemes. Furthermore, the U.S. government’s intention to ensure that all federal departments and contractors have more robust cybersecurity frameworks, embodied by the U.S. Executive Order on Improving the Nation’s Cybersecurity, contributes to the growth of the target market. With the highest CAGR, the Asia-Pacific region is anticipated to undergo substantial growth led by escalating cyber threats, burgeoning digitalization, and mounting awareness regarding cyber risks across China, India, Japan, and others. Booming implementation of regulatory frameworks and cybersecurity solutions will boost the APAC market size for cybersecurity insurance.

Key Players

-

Tata Consultancy Services Limited (TCS) (Cyber Insurance Advisory Services, Threat Management and Cybersecurity Insurance Solutions)

-

Guy Carpenter & Company LLC (Cyber Risk Analytics Platform, Cyber Reinsurance Services)

-

At-Bay Inc. (Cyber Insurance Coverage, Risk Monitoring Platform)

-

Lloyds Bank PLC (Cyber Liability Insurance, Cyber Event Response Services)

-

AXA SA (AXA Cyber Protect Insurance, AXA Risk Prevention Services)

-

Cisco Systems Inc. (Cisco Secure Endpoint Protection, Cisco Umbrella (Cybersecurity Insurance Support))

-

Chubb Limited (Cyber ERM (Enterprise Risk Management), Cyber Insurance Solution Suite)

-

Apple Inc. (Apple Device Security (Data Protection), iCloud Secure Backup (Cyber Risk Mitigation))

-

American International Group Inc. (AIG) (AIG CyberEdge Insurance, AIG Cyber Loss Prevention Services)

-

Zurich Insurance Group (Zurich Cyber Security & Privacy Insurance, Zurich Risk Engineering Cyber Solutions)

-

Marsh & McLennan Companies, Inc. (Marsh Cyber Policy Solutions, Marsh Cyber Risk Assessment Tools

-

Munich Re Group (Munich Re Cyber Insurance Solutions, Munich Re Risk Intelligence Service)

-

Travelers Companies, Inc. (Travelers CyberFirst Insurance, Travelers CyberRisk Assessment Services)

-

Beazley Group (Beazley Breach Response (BBR), Beazley InfoSec Cyber Insurance)

-

Aon PLC (Aon Cyber Insurance Brokerage Services, Aon Cyber Resilience Solutions)

-

Allianz SE (Allianz Cyber Protect, Allianz Cyber Risk Consulting)

-

Hiscox Ltd (Hiscox CyberClear Insurance, Hiscox Incident Response Services)

-

Liberty Mutual Insurance (Liberty Cyber Liability Insurance, Liberty Cyber Incident Management Services)

-

Sompo International (Sompo Cyber Liability Insurance, Sompo Cyber Risk Management Services)

-

XL Group Ltd (AXA XL) (AXA XL Cyber Insurance, AXA XL CyberRisk Mitigation Solutions)

and others in final Report.

Latest News from Key Players

-

AIG Cyber Insurance Product (March 2024) – AIG has revealed its new product of cybersecurity insurance that is expected to protect against an extended array of digital threats. The product includes coverage for vulnerabilities associated with different artificial intelligence applications, which is caused by the increasing implementation of AI technologies across a broad spectrum of industries.

-

Chubb Cyber Risk Services Expansion (June 2023) – Chubb has made an announcement regarding the expansion of its cybersecurity risk assessment operations targeted at company policyholders focusing on mid-sized companies in North America. These policies are designed to satisfy cyberattacks that are ever-growing in number across North American SMEs, frequently observed in the manufacturing and medical technology fields.

-

Government’s Promotion of Public-Private Partnership for Cybersecurity (September 2023) – The U.S. Department of Homeland Security has launched a new project that is aimed at establishing closer relationships between the private sector and the governing agencies. The program supports the implementation of various information exchange and risk mitigation strategies aimed at enhancing cybersecurity of the nation. Moreover, businesses that employ the advanced cybersecurity systems will be rewarded with insurance discounts.

| Report Attributes | Details |

| Market Size in 2023 | USD 13.3 Bn |

| Market Size by 2032 | USD 52.1 Bn |

| CAGR | CAGR of 16.4% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By offering (Solution {Cybersecurity insurance analytics platform, Disaster recovery and business continuity, Cybersecurity solution}, Service {Consulting/ Advisory, Security awareness training, Others}) • By coverage (Data breach, Cyber liability) • By Compliance Requirements (Healthcare Compliance, Financial Services Compliance, GDPR Compliance, Data Privacy Compliance, Others) • By insurance type (Tailored, Stand-alone) • By end user (Technology provider {Insurance companies, Third-party administrators, brokers, and consultancies, Government agencies}, Insurance provider {Financial services, IT and ITES, Healthcare and life science, Retail and ecommerce, Telecom, Travel, tourism, and hospitality, Others}) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Tata Consultancy Services Limited, Guy Carpenter and Company LLC., At-Bay Inc., Lloyds Bank PLC, AXA SA, Cisco Systems Inc., Chubb Limited, Apple Inc., American International Group Inc., Zurich Insurance Group |

| Key Drivers | • Increased cybersecurity rules and legislation will increase demand for insurance cover • High rate of financial loss recovery to boost market growth |

| Market Opportunity | • The rising cost of cybersecurity insurance premiums, especially for full-coverage policies, deters smaller businesses from purchasing adequate protection. |

Frequently Asked Questions

The study includes a comprehensive analysis of Cyber Security Insurance Market trends, as well as present and future market forecasts. DROC analysis, as well as impact analysis for the projected period. Porter's five forces analysis aids in the study of buyer and supplier potential as well as the competitive landscape etc.

The major key players are Tata Consultancy Services Limited, Guy Carpenter and Company LLC., At-Bay Inc., Lloyds Bank PLC, AXA SA, Cisco Systems Inc., Chubb Limited, Apple Inc., American International Group Inc., Zurich Insurance Group.

The United States is often regarded as the world's most important market for cybersecurity insurance.

The Cyber Security Insurance Market is to grow at a CAGR of 16.4% over the forecast period 2024-2032.

The estimated market size for the Cyber Security Insurance market for the year 2032 is USD 52.1 Bn.

Get in Touch