Data Center Outsourcing Market Report Scope & Overview:

The Data Center Outsourcing Market size was valued at USD 149.74 billion in 2025 and is expected to reach USD 258.21 billion by 2035, growing at a CAGR of 5.60% during 2026-2035.

Data Center Outsourcing Market growth is driven by the increasing focus of organizations towards the core competencies, reduction of operational costs, and adoption of cloud-based infrastructure. The increasing need for scalable IT infrastructure and managed services is one of the major growth-driving factors. The other factors that increase the market growth include enhanced security, compliance, and disaster recovery. The Data Center Outsourcing market analysis presents banking, healthcare, and retail as the top adopting sectors owing to the requirements of data efficiency and continuity. The data center outsourcing market trend also encompasses hybrid cloud integration and automation for seamless operations. The growth of the market in the future can be mainly attributed to the increase in the digital transformation across the industries, as the proliferation of IT over the past decade and the upcoming decade would only aid the market, driving a global shift towards agile, economical IT infrastructures.

Market Size and Forecast: 2025

-

Market Size in 2025 USD 149.74 Billion

-

Market Size by 2035 USD 258.21 Billion

-

CAGR of 5.60% From 2026 to 2035

-

Base Year 2025

-

Forecast Period 2026-2035

-

Historical Data 2022-2024

To Get more information on Data Center Outsourcing Market - Request Free Sample Report

Data Center Outsourcing Market Trends:

-

Increasing shift from in-house data centers to outsourced models to reduce capital expenditure and operational complexity.

-

Growing adoption of hybrid cloud and multi-cloud strategies driving demand for flexible and scalable outsourced data center services.

-

Rising integration of AI-driven automation and predictive analytics to improve uptime, efficiency, and resource utilization.

-

Expanding focus on cybersecurity, compliance, and data protection as enterprises rely more on third-party data center providers.

-

Higher demand for intelligent workload management and automated operations to support digital transformation and data-driven business models.

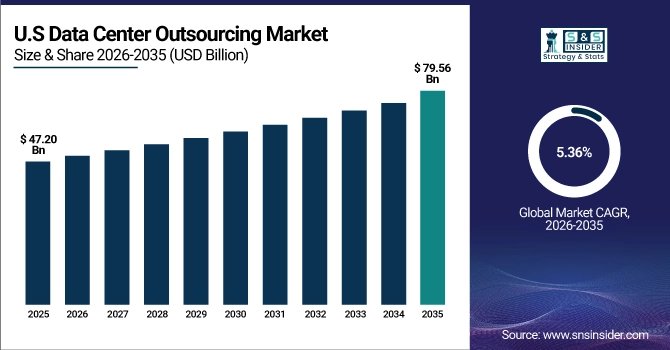

The U.S. Data Center Outsourcing Market is projected to grow from USD 47.20 billion in 2025 to USD 79.56 billion by 2035, reflecting a CAGR of 5.36%. This growth is driven by increasing demand for cloud services, scalable IT infrastructure, and cost-efficient data management solutions. Enterprises are increasingly outsourcing data center operations to enhance efficiency, ensure business continuity, and leverage advanced technologies such as AI, IoT, and edge computing. The trend highlights a shift toward strategic IT partnerships and digital transformation initiatives across industries.

Data Center Outsourcing Market Growth Drivers:

-

Rising Operational Expenses and Demand for Flexibility Cause Businesses to Outsource for Efficient and Scalable Data Management.

However, organizations are now choosing data center outsourcing to lower capital expenditure and operational costs. As they have hardware, staffing, energy, and security demands, maintaining an in-house data center is no hydroponic garden, and you will be charged accordingly. Scalable solutions: Outsourcing provides scalable solutions that can expand as needed and do not require large upfront investments. Providers also provide cloud, automation, and cybersecurity services, capabilities that would be prohibitively costly to take on in-house. By catering to cost efficiency along with flexibility and access to state-of-the-art technology, outsourcing becomes alluring for enterprises regardless of the industry they serve. In addition, the trend toward digital transformation and hybrid cloud environments will further accelerate the demand for outsourced data center services.

For instance, businesses can achieve up to 60% in operational cost savings through outsourcing strategies.

Data Center Outsourcing Market Restraints:

-

Fear of Breaches and Compliance Violations Prevents Organizations from Fully Embracing Outsourced Data Center Solutions.

While this is beneficial, the downside to data center outsourcing is data privacy, sovereignty, and compliance. The biggest concern of businesses when it comes to outsourcing critical operations is that of data being compromised, loss of control, or a third party mismanaging something. With heavy compliance mandates like HIPAA, GDPR, and CCPA, organizations cannot blindly trust external vendors without guarantees of compliance. Failure to comply can lead to expensive fines and damage to your reputation. In addition, certain sectors, like finance and healthcare, handle some of the most sensitive data, meaning that they will need strong encryption, audit trails, and continuous monitoring, which not all outsourcing providers are able to offer at scale.

In 2024, 61% of organizations reported that security and compliance issues were primary obstacles in their cloud adoption strategies.

Data Center Outsourcing Market Opportunities:

-

Automation and Predictive Analytics Enhance Performance, Driving Increased Adoption of Outsourced Data Center Services.

While AI and automation are advancing, they are also now key enablers that can immensely improve the long-term landscape of the data center. Outsourcing companies are employing AI-powered predictive maintenance, resource optimization, anomaly detection, etc. It enables enhanced efficiency, lesser downtime, and decreased operational costs for the clients. AI also facilitates more dynamic and resilient IT landscapes by allowing for intelligent workload management, capacity planning , and automated issue resolution. For clients, this means a better level of service and less manual handling time. With enterprises embracing close-knit workforces and data-driven organisations, AI-augmented services will give a competitive edge to service providers in the outsourcing arena.

For instance, AI-driven automation can reduce equipment downtime by up to 45%, boost server utilization rates by 25%, and improve data processing speeds by 40%.

Data Center Outsourcing Market Segment Analysis:

By Enterprise Size

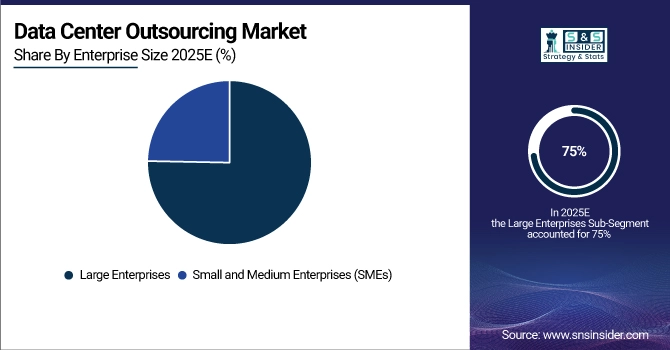

The large enterprise segment leads the data center outsourcing market and helds a revenue share of more than 75% of revenue share in 2025, as large enterprises operate the largest and most complex IT infrastructures, have a higher outsourcing budget, and require more complex data, making this segment lucrative. A tire that prioritizes ultimate performance, compliance, and global scale, usually in partnership with a leading provider. Large enterprises will continue to drive demand for data center outsourcing, with increased investment in hybrid models, AI integration, and data security. Small and Medium-sized Enterprises are anticipated to grow at the fastest CAGR, owing to the rising number of SMEs outsourcing to minimize capital expenditure and gain access to enterprise-grade infrastructure. The dawning of affordable cloud, easy-to-hire managed services, and horizontal scalability has created the right time for the SME transition to outsourced data centers. Above all, the growth in the future bigger because of the digitalization trends, remote working employee models, and IT agility.

By Service

The managed hosting services segment dominated the data center outsourcing market and accounted for a significant revenue share in 2025, due to growing enterprise demand for reliable, scalable, and fully managed Infrastructure Services. Outsourcing is also preferred by businesses as they want to avoid annoying their internal IT, even while ensuring that they stay compliant and perform well. This segment is set to maintain its lead with greater adoption of hybrid IT models and higher digital workloads, especially in the case of SMEs and industries that prefer cost-effective solutions. The security management services are expected to register the fastest CAGR during the forecast period, due to rising cyber threats, stringent data regulations, and the rise in demand for cloud. Enterprises want to safeguard against risk, maintain compliance, and respond to incidents without artificially inflating internal expenses. Over the next decade, it aims for this segment to grow substantially, as AI-based threat detection and zero-trust security models become mainstream in outsourced environments by 2035.

By Deployment

The on-premises deployment segment dominated the market and accounted for 68% of the data center outsourcing market share in 2025. Legacy systems, tight compliance requirements higher control over the data landscape, particularly in finance, healthcare, and government sectors. Organizations with critical security needs still opt for on-premises infrastructure. For mission-critical workloads, still a lot of large organizations maintain on-prem data centers to run workloads with slower growth still to large organizations and are still investing in modernization and hybrid integration. The cloud segment is expected to witness the fastest growth rate owing to high scalability, affordability, and rapid digital transformation. Many businesses are moving towards the cloud to take advantage of these benefits, like scalable infrastructure, disaster recovery, and accessibility anywhere in the globe. This segment is expected to witness exponential growth across all key industries till 2035 as cloud-native applications, AI integration, and multi-cloud strategies advance.

By End-Use

The IT sector dominated the data center outsourcing market and accounted for a significant revenue share in 2025, due to its high dependency on data processing, cloud computing, and digital services. Outsourcing is a consistent investment of enterprises for better scalability, security, and innovation. As IT consists of the largest consumer of outsourced data center services in the world, sustainable demand is expected due to the penetrating adoption of AI, big data, and hybrid cloud solutions. Telecom will have the fastest CAGR during the forecast period as 5G networks are implemented and data traffic volume rises. By outsourcing critical areas of operation, telecom operators are better positioned to meet the crippling demands placed on their infrastructures while simultaneously providing a more reliable network experience. In addition, the adoption of edge computing and growing IoT push will support the telecom segment to be a significant part of future growth in data center outsourcing.

Data Center Outsourcing Market Regional Analysis:

North America Data Center Outsourcing Market Insights

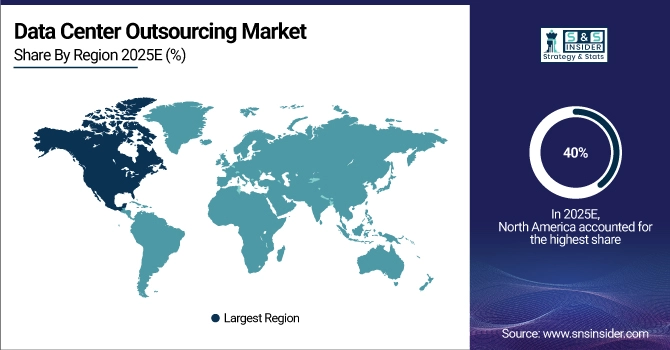

North America dominated the data center outsourcing market and accounted for 40% of revenue share in 2025, attributed to its advanced IT infrastructure, early adoption of cloud technologies, and the presence of several leading data center providers in this region. Data Center Outsourcing, High demand from sectors such as BFSI, healthcare, IT services, and outsourcing is complemented by stringent regulatory compliance as well as innovation in AI and automation, thus maintaining its leadership position.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Data Center Outsourcing Market Insights

Rapid digitalization, increasing penetration for the internet, and growing adoption of cloud across both SMEs and large enterprises will drive the fastest CAGR for Asia Pacific in the forecast period. The strong market growth until 2032 supported by government initiatives, increasing IT infrastructure investments, and demand in telecom and e-commerce sectors will help the region emerge as a future hot spot.

China leads the Asia Pacific data center outsourcing space owing to its large digital economy, robust government support, and quick acceptance of cloud technology. Tech giants, smart city projects, and 5G expansion are driving demand. A larger IT outsourcing and infrastructure investment growth will drive the market to grow even more.

Europe Data Center Outsourcing Market Insights

Europe is expanding its market thanks to strict data regulations (such as the GDPR), growing use of the cloud, and demand for energy-efficient infrastructure. For enterprises, outsourcing is a means of fulfilling compliance and scaling requirements. The growth will be driven by green data center initiatives and accelerating digital transformation across industries, etc, and the market is expected to continue growing at least until 2032.

The UK dominated the European data center outsourcing market, driven by a well-established tech ecosystem, early cloud adoption, and a robust demand from the financial sector. The additional growth fueled by digital investments post-Brexit and the everlasting trend of hybrid work. With cybersecurity becoming more of an intrinsic part of business strategy and more companies embracing outsourcing in a regulatory-compliant manner, the market is expected to grow gradually.

Latin America (LATAM) and Middle East & Africa (MEA) Data Center Outsourcing Market Insights

The Latin America (LATAM) and Middle East & Africa (MEA) data center outsourcing market is gaining momentum due to rising digitalization, cloud adoption, and growing demand for cost-efficient IT infrastructure. Enterprises are increasingly outsourcing data center operations to reduce capital expenditure and improve scalability. Expanding internet penetration, government digital initiatives, and increasing demand from BFSI, telecom, and e-commerce sectors are supporting market growth across both regions.

Data Center Outsourcing Market Key Players:

The major data center outsourcing market companies are IBM Corporation, HCL Technologies, Atos SE, Fujitsu Ltd., DXC Technology, NTT Data Corporation, Capgemini SE, TCS (Tata Consultancy Services), Wipro Limited, Cognizant Technology Solutions and others.

Competitive Landscape for Data Center Outsourcing Market:

DXC Technology is a global IT services provider offering data center outsourcing, infrastructure management, and cloud solutions. The company helps enterprises modernize legacy data centers, migrate to hybrid and multi-cloud environments, and improve operational efficiency through automation, security, and scalable managed services across industries.

-

In February 2025, DXC Technology entered into a strategic agreement with Skanska AB to modernize Skanska’s global IT infrastructure. As part of this collaboration, DXC will manage Skanska’s Azure cloud and on-premises environments, enhance cybersecurity, and deliver modern workplace solutions, aiming to improve operational efficiency and security across Skanska’s operations in Europe and the United States.

NTT DATA is a global IT services and consulting company providing comprehensive data center outsourcing and managed infrastructure services. It supports enterprises with data center operations, cloud migration, hybrid IT management, security, and automation solutions, enabling scalable, reliable, and cost-efficient IT environments worldwide.

-

In April 2025, NTT DATA released its first sustainability report for its data center division, NTT Global Data Centers. The report highlights the company's commitment to achieving Net-Zero emissions by 2030, with initiatives such as achieving 51% renewable energy usage for non-IT load globally and securing 1.7 TWh of renewable energy through Power Purchase Agreements.

|

Report Attributes |

Details |

|---|---|

| Market Size in 2025 | USD 149.74 Billion |

| Market Size by 2035 | USD 258.21 Billion |

| CAGR | CAGR of 5.60% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

|

Report Scope & Coverage |

Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

|

Key Segments |

• By Service (Managed Hosting Services, Colocation Services, Infrastructure Management Services, Disaster Recovery and Backup Services, Network Management Services, Storage Management Services, Security Management Services, Migration and Consolidation Services, Consulting and Advisory Services, Others) |

|

Regional Analysis/Coverage |

North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

|

Company Profiles |

IBM Corporation, HCL Technologies, Atos SE, Fujitsu Ltd., DXC Technology, NTT Data Corporation, Capgemini SE, TCS (Tata Consultancy Services), Wipro Limited, Cognizant Technology Solutions and others in report |

Frequently Asked Questions

Ans- North America region dominated the Data Center Outsourcing Market with 39% of revenue share in 2025.

Ans- The on-premises deployment segment dominated the market and accounted for 68% of the data center outsourcing market share in 2025.

Ans- Rising Operational Expenses and Demand for Flexibility Cause Businesses to Outsource for Efficient and Scalable Data Management.

Ans- The Data Center Outsourcing Market size was valued at USD 149.74 billion in 2025 and is expected to reach USD 258.21 billion by 2035, growing at a CAGR of 5.60% during 2026-2035.

Ans- The CAGR of the Data Center Outsourcing Market during the forecast period is 5.60% during 2026-2035.

Get in Touch