RegTech Market Size & Overview:

To Get More Information on RegTech Market - Request Sample Report

RegTech Market size was valued at USD 13.6 billion in 2023 and is expected to grow to USD 88.13 billion by 2032 and grow at a CAGR of 23.1 % over the forecast period of 2024-2032.

The growth of the RegTech market is driven by the increasing regulatory pressure on organizations across various sectors, particularly in financial services. Governments and regulatory bodies worldwide are intensifying their scrutiny to ensure that businesses comply with an evolving landscape of compliance requirements and industry standards. For instance, according to the latest government statistics, the U.S. Financial Crimes Enforcement Network indicated that suspicious activity reports increased by 15% in 2023. Similarly, the European Central Bank revealed that regulatory fines in the Eurozone locations exceeded five billion Euro. One of the key forces fostering high demand for RegTech is government promotion of digital transformation in regulatory compliance. The U.K. Financial Conduct Authority, for instance, is pushing the uptake of regulatory technologies through its “RegTech Sandbox” initiative, which offers companies an opportunity to test their solutions in a controlled environment.

Globally, the Financial Action Task Force has been pushing member states to adopt technology tools in the Anti Money Laundering (AML) and counter-terrorist financing processes. These international dynamics and local policies have powered RegTech solutions adoption as more and more companies seek to automate their compliance to minimize risk and reduce operational costs.

Moreover, the factors propelling the growth of the RegTech market are the continuously evolving government policies, the application of mobile banking, and the exponential growth of internet users which fuel the expansion of the industry on a global scale. The enhancement of the quality of reported data will also contribute to the growth of the RegTech market. RegTech solutions offer automated and intelligent tools that enable organizations to monitor and analyze vast amounts of data, identify suspicious activities, and ensure compliance with regulatory standards.

RegTech Market dynamics

Drivers

-

Growing global regulatory frameworks demand advanced solutions to ensure compliance, and financial institutions are increasingly adopting RegTech to manage diverse and evolving regulations.

-

Cloud technology offers scalability and flexibility for regulatory compliance operations, enhanced security and real-time data analytics are driving cloud-based RegTech deployments.

-

Governments are enforcing stringent AML regulations, driving demand for automated compliance tools, RegTech solutions provide rapid identification and reporting of suspicious financial activities.

The financial services industry is becoming increasingly complex due to the surge in regulatory frameworks introduced by governments and international bodies. These financial institutions and corporations are required to adhere to a vast array of regulations that in many cases are not just localized to one specific country or locale. This inherent complexity of managing a wide array of regulations is what makes the use of Regulatory Technology (RegTech) solutions more beneficial. Various rules and regulations such as the European Union’s General Data Protection Regulation, Markets in Financial Instruments Directive II, and U.S. Dodd-Frank Act have increased the stringency of reporting and transparency requirements. According to recent study in 2023 financial institutions will need to manage an average of 200 regulatory updates a day. Management of manual compliance with such a large number of changes on a daily basis becomes almost impossible.

RegTech solutions offer unique advantages of providing automation, real-time monitoring, and data analytics tools to mitigate the risks and minimize instances of human errors. An important example is the use of AI for developing and delivering Know Your Customer software. Companies such as Trulioo and Onfido are using AI to manage customer verification processes faster, thus tightening compliance processes and minimizing the risk of compliance violations. Already, many companies that are using blockchain technology to prevent fraud. This growing regulatory pressure, combined with the complexity of managing global standards, is driving the rapid adoption of RegTech solutions across industries.

Restraints:

-

Small and medium enterprises (SMEs) often face financial barriers to adopting advanced RegTech systems, High integration and training costs discourage adoption for many businesses.

-

Handling sensitive financial and regulatory data increases concerns around data breaches, Strict data protection laws like GDPR create additional challenges for RegTech vendors.

Data privacy and security concerns are prominent restraints. As RegTech solutions require managing large volumes of sensitive financial and personal data, this creates a higher risk of data breaches and cybercriminals attacks. When discussing regulations technologies, it is important to consider the fact that they normally interact with many systems; as a result, they might be attacked by numerous maleficent actors. Besides, in this particular context, companies need to comply not only with financial regulations but also with data protection laws. For instance, in Europe, corporations need to follow GDPR, while other regions have specific privacy frameworks, which complicate the management of data securely. The adoption of RegTech demands firms to bear increased costs and allocate significant resources to maintain secure systems, including encryption and adequate storage of data. The potential outcomes of sensitive data loss or inappropriate management will be devastating, as companies will face harsh financial penalties and notable reputational loss.

RegTech Market Segment analysis

By Deployment

In 2023, the cloud deployment segment accounted for the largest revenue share of about 64% in the global RegTech market. Cloud solutions offer certain cost efficiency and scalability. The growing advantages of cloud deployment segment are also the result of the increasing ease of integration of cloud solutions in different industries. In 2023, cloud-based solutions were actively supported by governments worldwide, and the cloud-first strategy became widespread. For example, the U.S. government’s Federal Cloud Computing Strategy was updated in 2023 and became a substantial boost for federal agencies to focus on cloud solutions. Financial and healthcare industries are regulated, and new government rules automatically require successful companies in the industry to adopt the new technologies. In addition, the new administration is expected to maintain the emphasis on cloud solutions, maintaining the growth of the market share for the cloud deployment segment.

Furthermore, the European Union’s Digital Strategy also supported cloud-based solutions implemented by financial institutions for the purpose of compliance management, carrying out huge volumes of data. Furthermore, cloud-based solutions simultaneously use real-time updates, enabling companies to be sure they are keeping compliant with the latest regulations. Finally, cloud deployment is preferred by SMEs because of its lower upfront cost, and therefore it is likely to experience a significant increase in its vast market share.

By Application

The risk and compliance management segment accounted for the largest revenue share in the RegTech market in 2023. The main reason for the rise in this segment’s dominance is an increase in the complexity of compliance regulations across various industries. For example, government bodies such as the U.S. Securities and Exchange Commission reported a 20% rise in compliance investigations in 2023, which highlights the need for automated compliance solutions. Meanwhile, the cost of non-compliance is rising, with organizations facing significant fines for violations. In 2023, the U.S. Department of Justice imposed a total of $2.8 billion in fines due to compliance breaches. Consequently, all these factors encourage businesses to invest in risk and compliance management tools.

Additionally, the number of businesses that operate on a global scale ensures that these companies have to comply with numerous regulations in several jurisdictions. In this regard, cloud-based and AI-driven RegTech tools play a critical role due to the solutions’ centralized nature, enabling firms to benefit from a single platform that offers automatic regulatory updates and compliance reports. Moreover, governments actively support the deployment of RegTech tools. In the 2023 annual risk survey results of the UK’s Prudential Regulation Authority, better compliance management was highlighted, with RegTech solutions automatically identified as essential tools in the regulator’s report.

By End-User

The BFSI segment dominated the global RegTech market in 2023 owing to the increasing regulatory scrutiny in financial services. In 2023, the BFSI sector held around 26% of the global RegTech market. This is primarily attributed to stringent regulations and the increasing number of financial transactions that ought to be monitored round the clock to prevent financial crimes, including money laundering and fraud. Government agencies, such as the U.K. Financial Conduct Authority and the U.S. Office of the Comptroller of the Currency, have imposed stringent compliance rules thereby requiring financial institutions to use advanced tools to ensure they meet the evolving standards. Moreover, the introduction of the Payment Services Directive 2 (PSD2) in the European Union has pushed banks and other payment services to take RegTech solutions to handle open banking securely. This adoption trend is mirrored in the U.S. with the Bank Secrecy Act (BSA) modernization initiative, which emphasizes the need for advanced compliance monitoring technologies.

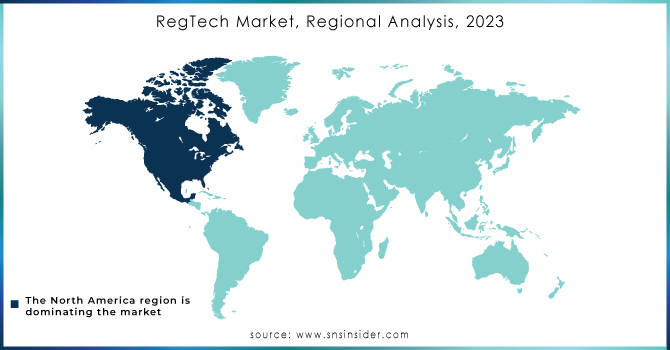

Regional Insights

The global RegTech market was dominated by North America in 2023, with a significant share of 42%. The region’s dominance can be attributed to the robust financial services sector in the region and stringent regulatory frameworks, such as the Dodd-Frank Act, which promotes the adoption of RegTech. Market growth has been further enhanced by government-sponsored initiatives, including the U.S. National AI Initiative, and federal funding to promote innovation within the market. The U.S. government’s increased focus on anti-money laundering regulations alongside FinCEN’s promotion of digital tools has also contributed to market growth.

However, Asia-Pacific is expected to grow simultaneously at the fastest CAGR, driven by the rapid growth of financial services in emerging economies, including China and India. In 2023, the Asia-Pacific RegTech market had a 22% share of the global market. The governments of the two countries have implemented stringent regulations in response to the increasing financial crime and fraud. In 2023, India’s Reserve Bank launched a new guideline demanding the application of technology to promote transparency in financial transactions, thereby ensuring the quick adoption of RegTech. Additionally, the Chinese government's demand for the adoption of digital tools for regulatory compliance is expected to fuel market growth.

Do You Need any Customization Research on RegTech Market - Enquire Now

Key Players

Key Service Providers

-

CUBE (Automated Regulatory Intelligence, RegPlatform)

-

Thomson Reuters (Regulatory Intelligence, CLEAR Compliance)

-

Hummingbird RegTech (Compliance Workflow Tools, Investigation Platform)

-

Ascent Technologies, Inc. (Compliance Confidence Scorecard, Regulatory Knowledge)

-

Fenergo (Client Lifecycle Management, Regulatory Rules Engine)

-

ComplyAdvantage (Transaction Monitoring, Risk Monitoring)

-

NICE Actimize (Surveillance, AML Solutions)

-

ClauseMatch (Policy Management, Compliance Workflow)

-

Trunomi (Data Rights Management, Consent Management)

-

Chainalysis (Cryptocurrency Transaction Monitoring, KYT – Know Your Transaction)

Key Users (Service Consumers)

-

HSBC

-

JPMorgan Chase

-

Goldman Sachs

-

Deutsche Bank

-

BNP Paribas

-

Standard Chartered

-

Citibank

-

Barclays

-

Morgan Stanley

-

Wells Fargo

Recent Developments:

- In March 2023, new guidelines were introduced by the U.S. Department of the Treasury that would promote the advent of AI-fueled RegTech tools for managing risk and AML. This government-related group has worked to ensure that compliance can be adapted to new industry regulations while reducing operational costs on the part of financial business institutions.

- In May 2024, CUBE, RegTech’s leader in the creation of Automated Regulatory Intelligence acquired Thomson Reuters’ RegTech. Consequently, the number of customers and the number of highly skilled professionals working within the company increased significantly.

- In April 2023, Hummingbird RegTech released an app for compliance professionals. By using its tools, they would be able to assure that the financial crime can be countered and that the business would stay in line with all industry-specific regulations.

- In March 2023, Ascent Technologies, Inc. released its own product called the Compliance Confidence Scorecard, which provides its clients with regulatory change analysis and monitoring. In turn, this allows them to better understand regulatory compliance mapping.

| Report Attributes | Details |

| Market Size in 2022 | USD 13.6 billion |

| Market Size by 2030 | USD 88.13 billion |

| CAGR | CAGR of 23.1 % From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Solutions, Services) • By Enterprise Size (Large Enterprises, SMEs) • By Application (Risk & Compliance Management, Identity Management, Regulatory Reporting, AML and Fraud Management, Regulatory Intelligence) • By Deployment Type (Cloud, On-premises) • By End-user (BFSI, Manufacturing, IT & Telecom, Healthcare, Government, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe [Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia Rest of Latin America) |

| Company Profiles |

CUBE, Thomson Reuters, Hummingbird RegTech, Ascent Technologies, Inc., Fenergo, ComplyAdvantage, NICE Actimize, ClauseMatch, Trunomi, Chainalysis |

| Key Drivers | •Growing global regulatory frameworks demand advanced solutions to ensure compliance, and financial institutions are increasingly adopting RegTech to manage diverse and evolving regulations •Cloud technology offers scalability and flexibility for regulatory compliance operations, enhanced security and real-time data analytics are driving cloud-based RegTech deployments. •Governments are enforcing stringent AML regulations, driving demand for automated compliance tools, RegTech solutions provide rapid identification and reporting of suspicious financial activities. |

| Market Challenges | •Small and medium enterprises (SMEs) often face financial barriers to adopting advanced RegTech systems, High integration and training costs discourage adoption for many businesses. •Handling sensitive financial and regulatory data increases concerns around data breaches, Strict data protection laws like GDPR create additional challenges for RegTech vendors. |

Frequently Asked Questions

There are Five segments are covered in RegTech Market report, By Component, By Enterprise Size, By Application, By Deployment Type, By Vertical.

Yes, you can ask for the customization as pas per your business requirement.

The forecast period for the RegTech Market is 2023-2032.

The CAGR of the RegTech Market for the forecast period 2024-2032 is 23.1 %.

USD 13.6 billion in 2023 is the market share of the RegTech Market.

Get in Touch