Data Center Power Management Market Analysis & Overview:

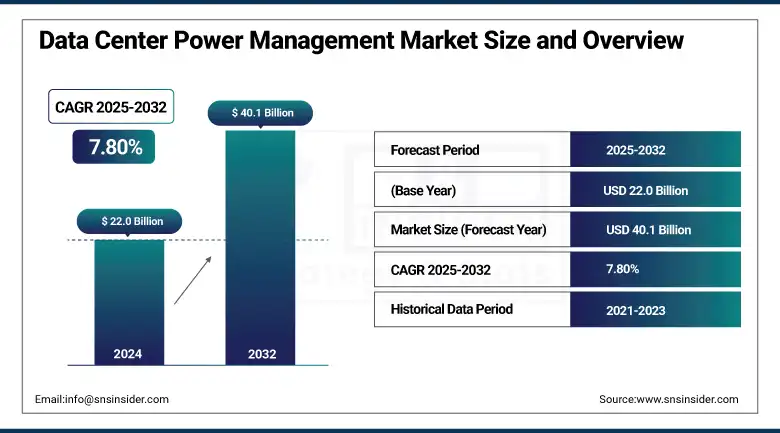

The Data Center Power Management Market size was valued at USD 22.0 billion in 2024 and is expected to reach USD 40.1 billion by 2032, growing at a CAGR of 7.80% during 2025-2032.

The global data center power management market growth is driven by escalating data consumption globally, growing demand for energy-efficient infrastructure, and the exponential rise of cloud and hyperscale data centers. Increasing demand for intelligent power solutions in alignment with renewable energy sources and real-time system monitoring for energy consumption and carbon footprint reduction is propelling the market growth. The growth is primarily driven by an ongoing wave of digitalisation, regulatory mandate for operating sustainably, and an associated rise in the demand for uninterrupted power supply.

To Get more information On Data Center Power Management Market - Request Free Sample Report

Data center power management market trends include powered charging, adoption of AI-powered data center energy optimization modular power solutions for data centers. The data center power management market analysis report recently published highlights that the market will continue to grow steadily towards the end of the decade, owing to the growing demand for optimization of power-related operations across various organizations.

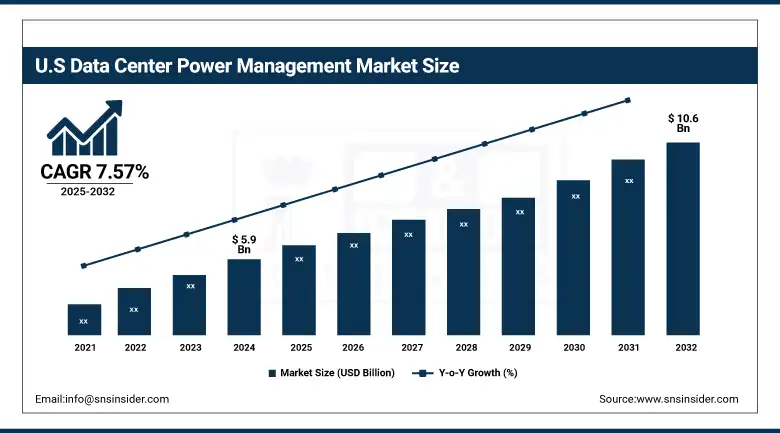

The U.S. Data Center Power Management Market was valued at USD 5.9 billion in 2024 and is expected to reach USD 10.6 billion by 2032, at a CAGR of 7.57% during the forecast period.

The addition of energy-efficient solutions, the integration of renewables, and the explosion of hyperscale and edge data centers are the primary fuels for this growth. Moreover, there is a surge in cloud computing and AI technologies, which boosts the demand for key and efficient power management systems to improve operational efficiency and sustainable development.

Data Center Power Management Market Dynamics:

Drivers:

-

Rising Energy Costs and Regulations Drive Adoption of Intelligent Power Management in Data Centers

With rapidly growing global data consumption, the pressure for enterprises to minimize operational expenditure and the exposure to the environmental footprint is mounting. As the focus on saving electrical energy has increased, the requirement for EV power management systems has made a mark in the industry for reducing electrical energy consumption and delivering optimal performance. Industry sector adoption of advanced technologies, such as intelligent PDUs, UPS systems, and DCIM software, is seen for the improvement of power usage effectiveness. The U.S. regulatory instruments and ESG commitments are also pushing the market to transition to sustainable infrastructure. This focus not only enhances operational efficiencies but is also in line with corporate sustainability targets, ensuring that the demand for intelligent, scalable power management solutions will continue to grow across colocation, hyperscale, and edge data centers.

For instance, Artificial Intelligence workloads are significantly contributing to increased power consumption in data centers. By the end of 2025, AI is projected to account for up to 49% of total data center power usage.

Restraints:

-

High Infrastructure Costs Slow Adoption in Small and Mid-Sized Data Centers

The upfront cost of deploying advanced power management solutions, however, tends to be a significant barrier despite the long-term savings. For example, deploying energy-efficient systems requires investments in the intelligent hardware, monitoring software, and retrofitting of even older infrastructure to support the smart management tools, things that take time and intellectual capital. This is quite a capital expenditure for the small and mid-sized data center. Moreover, the challenge of integrating these systems into existing business IT infrastructure often necessitates the involvement of skilled workers, which also contributes to high installation costs. Yet this upfront cost can extend payback periods, stifling adoption, particularly in emerging markets or cost-sensitive segments, ultimately removing the opportunity for deeper, more meaningful market penetration, even when the case for the long term is there.

For instance, Power and Cooling are major ongoing expenses, with costs ranging from USD 0.05 to USD 0.15 per kWh. Annual costs can run into several million dollars.

Opportunities:

-

Sustainability Goals Boost Demand for Renewable Energy-Integrated Power Systems

An important opportunity for the power management market is the increasing interest of several organizations in green data centers. As the governments and enterprises promised carbon neutrality, data centers are also adopting renewable energy, such as solar, wind, and hydropower. Power management solutions are essential for managing load balancing, back-up, and the variability of renewable inputs. This potential is bolstered by advancements in energy storage and other grid interactions. This well-founded integration is a key growth enabler for the kind of data centers that are built today to meet future requirements, as companies can leverage power management systems in these facilities to manage usage, cut costs, and improve sustainability targets when investing in renewable-powered facilities.

Challenges:

-

Hybrid and Edge Environments Complicate Unified Power Management

Hybrid cloud models and geographically distributed data centers have added immense complexity to power management. With different infrastructure and usage patterns globally, it can certainly be a technical challenge to achieve consistency in energy efficiency, monitoring, and control across multiple sites. These setups make it even harder to achieve real-time visibility and analytics, making it more difficult to predict your energy demands and identify any inefficiencies. Bringing all these together for power management across cloud, on-premise, and edge environments will need higher-level DCIM platforms and skilled professionals. Clearing these hurdles is critical for a robust value proposition for power optimization, thus, a major challenge for market players.

For instance, Edge sites experienced an average of 5.39 outages over 24 months, surpassing the 4.81 outages reported by centralized data centers. This higher frequency underscores the challenges in maintaining consistent power management across distributed environments.

Data Center Power Management Market Segmentation Analysis:

By Component:

The hardware segment dominated the market and accounted for 48% of data center power management market share in 2024. This dominance can be explained due to the necessity of hardware components to provide reliable and efficient power management of data centers, such as Uninterruptible Power Supply (UPS) systems, Power Distribution Units (PDUs), and cooling systems.

The services segment is projected to record the fastest CAGR during the forecast period in the data center power management market. It shows rapid growth due to the rising complexity of data center operations, demanding specialized services for power management systems design, installation, maintenance, and optimization. The operators of data center utilities are strongly dependent on professional services to keep their power supply system’s functional, avoid any downtimes, and also increase the lifetime of power supply devices.

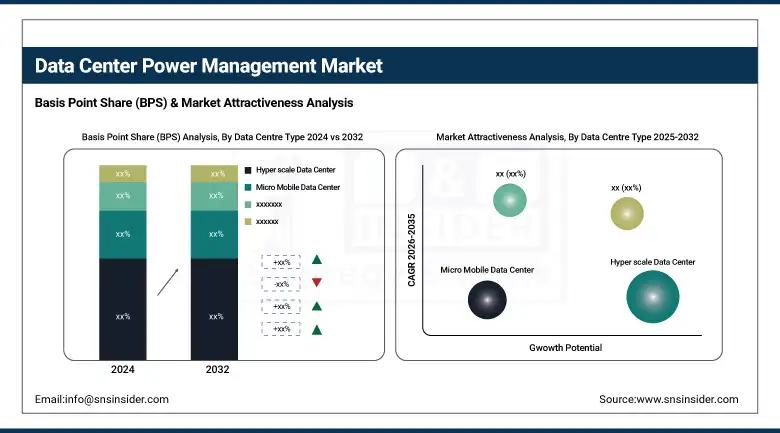

By Data Centre Type:

Hyperscale data centers dominated the data center power management market in 2024 and accounted for 26% of revenue share, as they can process massive workloads of data and support large-scale cloud services, big data analytics motives, and AI applications. Advanced power management solutions are essential to ensure energy efficiency and reliability for the proper operation of these facilities. This segment benefits from the rising demand for digital services and the rapid development of cloud infrastructure by large tech corporations.

The edge data centers are expected to register the fastest CAGR during the forecast period, as they perform low-latency data processing and real-time analytics closer to end-users. Internet of Things devices, autonomous systems, and smart apps driving edge computing need local computing power, which makes edge data centers critical. This helps better service quality and less congestion in the network, which is why they are rapidly expanding in the market.

By Industry:

The IT & Telecom dominated the data center power management market in 2024 and accounted for a significant revenue share, owing to growing requirements for cloud computing, increasing 5G network expansion, big data analytics, and IoT continue to grow, resulting in significant investments in data center infrastructure.

Retail segment is expected to register the fastest CAGR during the forecast period, due to rapid growth of E-commerce activities and demand for robust IT infrastructure for E-commerce platforms. Demand is also being driven by the increasing use of data analytics, artificial intelligence and machine learning for consumer personalization and inventory management.

Data Center Power Management Market Regional Outlook:

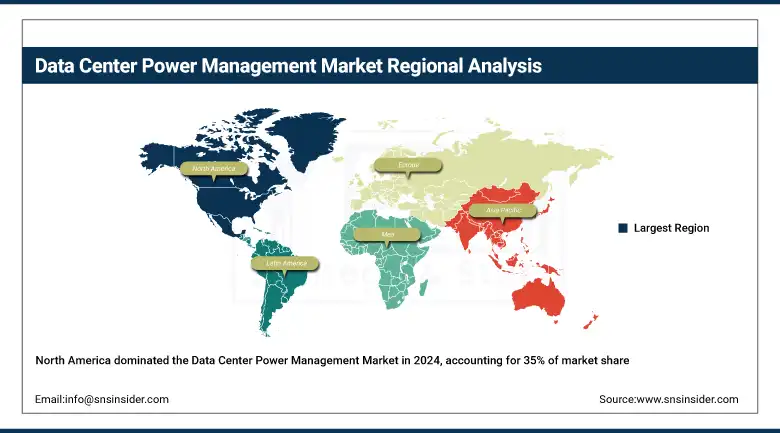

North America dominated the market and accounted for 35% of the revenue share in 2024. The increasingly advanced digital infrastructure, the presence of large-scale data centers, and early adoption of cloud technologies. As a result, stringent energy efficiency regulations and investments in renewable energy increase the demand for power management solutions. Continued advancements in technology, along with a heavy concentration on sustainable data centers, are expected to keep the region in the lead through 2032.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia-Pacific is the fastest-growing region during the forecast period driven by rapid digitalization, expanding cloud adoption, and the increasing deployment of edge computing. And growth is driven by massive expenditure on Data center infrastructure in different countries, such as China, India, and Japan. Through 2032, the highest CAGR in this region will be driven by government initiatives supporting smart technologies and the usage of renewable energy, rapidly expanding its market footprint.

China leads the data center power management market in Asia-Pacific due to high investments in cloud infrastructure, and government support toward digitalization and rapid growth of both hyperscale and edge data centers. China has been emphasizing energy efficiency and enhanced integration for the last decade, and the shift will continue propelling the broad market growth through 2032.

The European market is fueled by stringent energy regulations, increasing data traffic, and rising usage of green data centers. Investments in hyperscale facilities and the rising need for sustainable IT infrastructure are likely to further boost growth through 2032, featuring energy-efficient power management systems as a regional focus.

Germany is at the top of the European market with more data centers, an advanced industrial base, and deeper integration of renewables into the electricity production. Germany will benefit from government benefits for energy-efficient technologies sectors and a vital digital ecosystem that is likely to sustain the growth of power management solutions until 2032.

Key Players:

The major data center power management market companies are Schneider Electric, Eaton Corporation, ABB Ltd., Vertiv Holdings Co., Siemens AG, Delta Electronics, Huawei Technologies Co., Ltd., Rittal GmbH & Co. KG, Tripp Lite, Legrand SA, and others.

Recent Developments:

-

In April 2024, Schneider Electric introduced the Galaxy VXL, a compact, high-density uninterruptible power supply (UPS) designed for AI and large-scale data center workloads. Additionally, they co-developed a reference design with NVIDIA to support liquid-cooled AI clusters, optimized for NVIDIA’s Blackwell chips.

-

In July 2024, Vertiv launched the MegaMod CoolChip, a prefabricated modular data center solution equipped with high-density liquid cooling. This solution aims to accelerate global deployment of AI compute by reducing deployment time by up to 50%.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 22.0 Billion |

| Market Size by 2032 | USD 40.1 Billion |

| CAGR | CAGR of 7.80% From 2024 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2024-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | •By Component (Hardware, Software, Services) •By Data Center Type (Modular Data Center, Colocation Data Center, Cloud Data Center, Edge Data Center, Hyperscale Data Center, Micro Mobile Data Center) •By Industry (BFSI, Healthcare, Manufacturing, IT & Telecom, Media & Entertainment, Retail, Government, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Germany, France, UK, Italy, Spain, Poland, Turkey, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Rest of Latin America) |

| Company Profiles | Schneider Electric, Eaton Corporation, ABB Ltd., Vertiv Holdings Co., Siemens AG, Delta Electronics, Huawei Technologies Co., Ltd., Rittal GmbH & Co. KG, Tripp Lite, Legrand SA and others in the report |

Frequently Asked Questions

North America region dominated the Data Center Power Management Market with 35% of revenue share in 2024.

The hardware segment dominated the market and accounted for 48% of data center power management market share in 2024.

Rising Energy Costs and Regulations Drive Adoption of Intelligent Power Management in Data Centers.

The Data Center Power Management Market size was valued at USD 22.0 billion in 2024 and is expected to reach USD 40.1 billion by 2032.

The CAGR of the Data Center Power Management Market during the forecast period is 7.80% over 2025-2032.

Get in Touch