Data Center Renovation Market Report Scope & Overview:

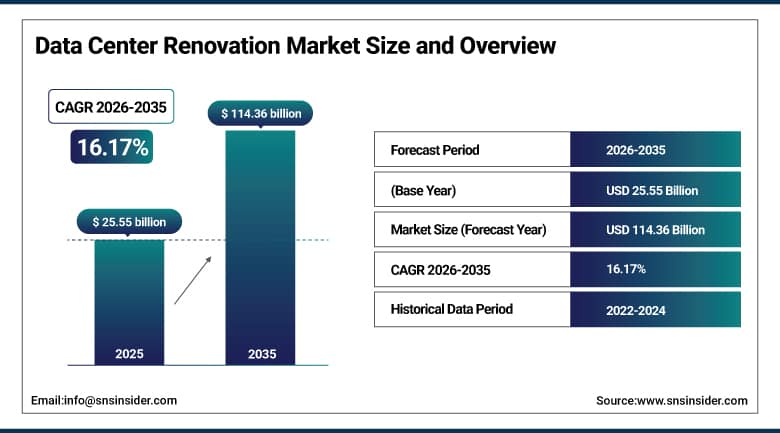

The Data Center Renovation Market size was valued at USD 25.55 billion in 2025 and is expected to reach USD 114.36 billion by 2035, expanding at a CAGR of 16.17% over the forecast period of 2026-2035.

With organizations looking to improve energy efficiency, security, and computing capacity, the Data Center Renovation Market has seen a rapid improvement in energy efficiency over time. As cloud, edge, and AI technology improve, many companies are choosing to renovate their legacy instead of building greenfield. This includes efficient cooling and even integration of renewable energy because of sustainability goals and carbon regulations, which are spurring green renovations as well. This process can perform electrical upgrades, optimize space, and enhance power and cooling Services. The market in North America is expected to hold the largest share, due to the aged infrastructure and high demand for digital upgradation, while in terms of growth, Asia-Pacific is projected to grow at the fastest due to increasing IT investments with the growing digital infrastructure.

Data Center Renovation Market Size and Forecast:

-

Market Size in 2025: USD 25.55 Billion

-

Market Size by 2035: USD 114.36 Billion

-

CAGR: 16.17% during 2026–2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On Data Center Renovation Market - Request Free Sample Report

Data Center Renovation Market Key Trends:

-

Adoption of Energy-Efficient Infrastructure: Increasing upgrades of legacy data centers with energy-efficient cooling systems, power distribution units, and advanced airflow management solutions to reduce operational costs and carbon footprint.

-

Integration of Modular and Scalable Designs: Data center operators are adopting modular infrastructure and scalable layouts during renovation to support rapid expansion and flexible IT capacity management.

-

Growth of Liquid Cooling Technologies: Rising deployment of high-density servers and AI workloads is driving the integration of liquid and immersion cooling solutions in renovated data center facilities.

-

Implementation of Advanced Monitoring & Automation: Renovated facilities are increasingly integrating AI-driven monitoring, predictive maintenance tools, and automated infrastructure management for improved operational efficiency.

-

Focus on Sustainability and Green Data Centers: Organizations are renovating existing facilities to comply with sustainability targets by integrating renewable energy sources, efficient cooling technologies, and low-carbon building materials.

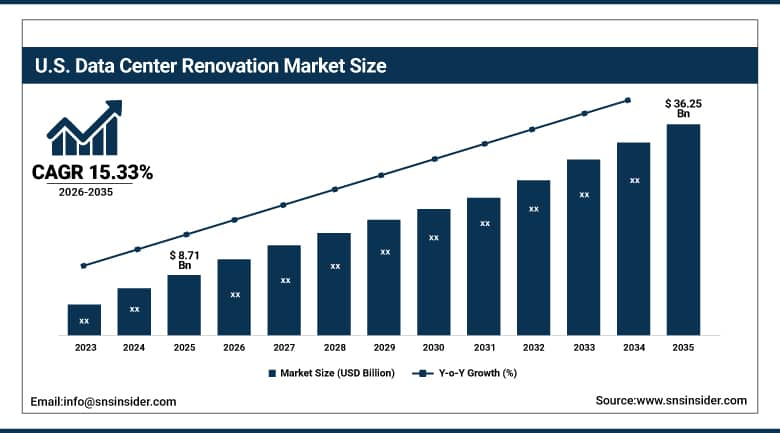

The U.S Data Center Renovation Market size reached USD 8.71 billion in 2025 and is expected to reach USD 36.25 billion in 2035 at a CAGR of 15.33% from 2026-2035.

The market in the United States is the largest, supported by the abundance of legacy data centers present in the country and the rapid transition towards digital technologies, as well as increase in demand for energy-efficient infrastructures. At the heart of this are cloud computing, edge computing and AI workloads that require these facilities to be up to speed, creating a need to install more power and cooling systems. Furthermore, stricter environmental laws and corporate sustainability goals are forcing operators to retrofit existing centers with green technologies.

Data Center Renovation Market Key Drivers:

-

Rising demand for high-performance computing and modernization of aging data center infrastructure.

The Data Center Renovation market is being driven primarily by the need to upgrade older data center infrastructure to support new IT workloads including cloud computing, artificial intelligence and big data analytics. Most enterprises and colocation providers are repurposing, upgrading today built facilities with capabilities to rise power, cooling optimization and high-density server range these days. Stricter regulatory requirements for energy efficiency, burgeoning demand for reliable data storage, and proliferation of digital services are driving organizations to upgrade their old data centers further instead of constructing new facilities.

Data Center Renovation Market Key Restraints:

-

High renovation costs and operational disruptions during infrastructure upgrades.

Data Center Renovation market also has its few challenges, with capital outlay being a big factor in renovating power systems, cooling infrastructure, network components, and even structural components. Another issue that would hinder renovation projects is the risk of disruption, which is quite significant, especially for organizations that require 24/7 uptime and data availability. In certain areas, however, the pace of renovation activities may be hindered by the challenges inherent in adopting new technologies alongside existing infrastructure as well as regulatory and compliance requirements surrounding renovation activity.

Data Center Renovation Market Key Opportunities:

-

Growth of sustainable and energy-efficient data centers creates strong renovation opportunities.

Data Center Renovation Projects to Utilize Data Centers in a Sustainable and Energy-Efficient Manner as Global Attention on Sustainability Increases. To minimize operational expenditure and carbon footprint, organizations are focusing on developing energy-efficient technologies such as advanced cooling systems and integration of renewable energy together with smart energy management systems. In addition to this, the increase in edge computing, 5G networks, and AI-driven workloads is prompting enterprises to modernize and refurbish the older facilities to meet modern infrastructure needs. As a result, these commotions in data center tailor and design are eventually paving new paths for data center fitting and modernization service providers.

Data Center Renovation Market Segments:

-

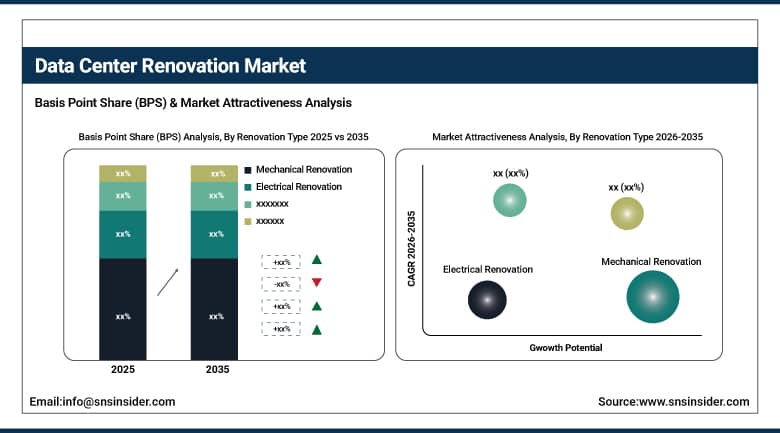

By Renovation Type: In 2025, Mechanical Renovation dominated with 41% share; Electrical Renovation fastest growing segment during 2026–2035

-

By Renovation Goal: In 2025, Improved Energy Efficiency dominated with 46% share; Increased Capacity and Density fastest growing segment during 2026–2035

-

By Infrastructure Component: In 2025, Cooling Systems dominated with 38% share; Power Systems fastest growing segment during 2026–2035

-

By Data Center Age: In 2025, 11–15 Years dominated with 33% share; 16–20 Years fastest growing segment during 2026–2035

Data Center Renovation Market Segment Analysis:

By Renovation Type

Infrastructure Renovation leveraged an impressive 46.25% of market share in 2024, largely representing the need to replace old data center sites to accommodate new workloads. Infrastructure refurbishment is often just a change of structure like a newly created raised floor, a larger server room, improved fire suppression systems, and better physical security. Earlier this year, market leaders such as Equinix and Digital Realty backed larger scale retrofitting projects to improve resiliency and extend the useful life of these facilities. As it happens, the newest trends in the data center renovation market industry, especially those around modular building innovations and pre-fab answers for development, decrease the time expected for a remodel. These aspects are essential to keep business workflow intact, meet compliance prescriptions, and run the data center business with more efficiencies in the new-age data center.

Particularly, Electrical Renovation segment, is projected to dominate with the fastest CAGR of 16.94%, due to the growing investment in retrofitting the obsolete power distribution units (PDUs), switchgear, and back-up power systems to accommodate denser computing, Cloud workloads, & AI applications which demand stable and scalable power systems. Companies such as Vertiv, Schneider Electric, have been launching new modular electrical infrastructure solution as part of renovation needs. As companies become more aware of energy efficiency, avoiding downtime due to capacity issues, and complying with regulations, electrical upgrades are an important form of a data center renovation.

By Renovation Goal

The Modernization and Upgrading segment captured 44.02% of the revenue share in 2024, as data centers try to stay relevant with the newest tech. Everything from swapping legacy systems for high-performance servers to automation, disaster recovery capabilities. The upgrading of legacy centers with edge computing and AI integration by Amazon Web Services and Microsoft Azure is a recent illustration of this. In essence, the driver is a greater need for agility, reliability, and readiness to go digital. With an ever-increasing digital transformation, modernization is by far the most dominating part of renovation initiatives across industries, keeping it at the top of its game in the market.

The Improved Energy Efficiency segment is projected to grow at a CAGR of 16.85%, due to escalating energy prices as well as stricter environmental regulations. As a result, operators are currently investing in efficient UPS units, speed-controlled cooling fans, and state-of-the-art energy monitoring technologies. AI-powered real-time energy optimization for data centers, such as by Google and Meta. Operators are transitioning facilities to sustainable energy designs driven by efforts to reduce operational costs and meet ESG goals. Green data centres are quickly becoming the de facto standard, and this segment is gaining rapid momentum and will become a heterogeneous investment type in the market.

By Infrastructure Component

The Power Systems segment led with 37.73% of revenue share in 2024, due to the fundamental need for power anytime and at scale for data centers. Today's workloads require the highest redundant and resilient power infrastructure. Data centers have these requirements in mind as companies are launching new products, like Eaton has launched scalable UPS systems, and ABB has launched smart switchgear. It is purely driven by the high-density servers, which are being deployed and pushing the limits of legacy power systems. Renewable power availability, reliability, and load management are triggering investments in renovation efforts that are putting this segment as a key pillar in maintaining the efficiency of next-generation data centers.

Cooling systems that operate within this segment are growing at a rate of 17.20% over the forecast period as power densities are rapidly increasing due to high-performance computing and AI-centric workloads. In the renovation projects, Liquid cooling and energy-efficient air-handling units will be launched from data centre renovation market companies such as Vertiv and STULZ. Better cooling is also required for uptime and hardware lifespan. However, regulations about energy consumption as well as sustainability goals are also driving modern cooling solutions. High demand for low PUE combination of efficient cooling upgrades generated is inescapable from growing demand, which, further, is driving this segment growth in the renovation market.

By Data Center Age

Data centers aged 11–15 years held the largest revenue share at 30.18% in 2024, because these facilities are still operational but require immediate upgrades. The centers are inefficient and ill-equipped to meet modern digital needs. Factors operating behind are accelerating speed of technological obsolescence and high energy utilization. IBM and NTT address middle of the cycle refreshes with the drive towards server consolidation and infrastructure optimization to provide for greater efficiency without a full rebuild. These renovations offer optimal ROI by enabling compliance, boosting energy efficiency, enhancing performance, and extending asset lifespan, making this age group highly attractive for targeted upgrade investments.

The Over 20 Years segment is projected to grow at a CAGR of 17.47%, fueled by the desperate need to replace aging infrastructure that no longer meets the demands of today's workloads. These legacy centers often suffer from lower energy efficiency and higher operational risk. Iron Mountain and Cyxtera are two recent examples of efforts to redevelop existing facilities with new monitoring, power, and cooling systems. The main motivator is the cost-benefit of a renovation in locations where rebuilding is impractical, or via real estate limitations. This rapidly growing segment further pushes investments with a strong focus on sustainability and compliance.

Data Center Renovation Market Regional Analysis:

North America Data Center Renovation Market Insights:

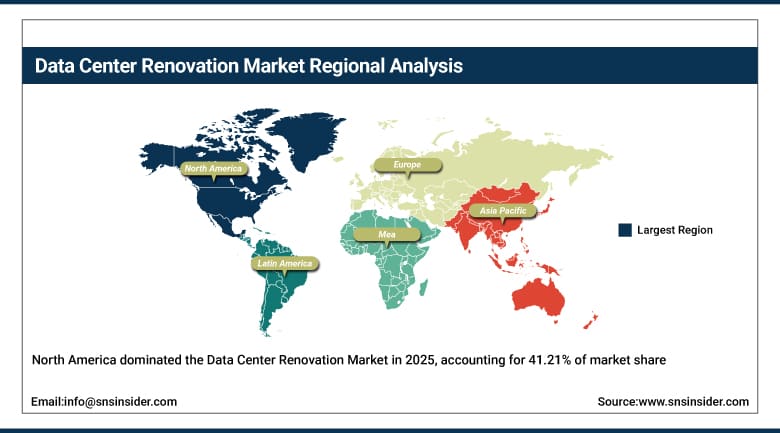

North America leads the Data Center Renovation Market share of 41.21%. As North America has Technologies & Tools for a great infrastructure, coupled with many aging data centers needing renovation, the data center renovation market can be observed. It is a highly digital transforming place, has solid energy-efficient and secure data center technologies investment in the region.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Live Data Center Renovation Market Insights:

Europe continues to experience gradual growth in data center renovations with stringent environmental regulations and growing green technology adoption, The area prioritizes data center operation energy efficiency and carbon footprint reduction as far as possible.

Asia-Pacific Data Center Renovation Market Insights:

Asia Pacific is the fastest-growing region with a CAGR of 17.07% as growing digital infrastructure, increasing cloud adoption, and quick industrialisation. As consumption and performance demand continue to increase, investments toward modernization of older, expansive facilities are climbing.

Latin America & Middle East & Africa (MEA) Data Center Renovation Market Insights:

Driving factors such as growing digital transformation trends, internet adoption, and energy-efficient infrastructure are contributing to data center renovation adoption in regions such as the Middle East & Africa, and Latin America. Underpinned by government stimulus and rising demand for cloud and edge computing infrastructure, the UAE and Brazil are driving the growth in their regions.

Data Center Renovation Market Competitive Landscape:

Schneider Electric (Schneider Electric SE) is a France-based company founded in 1836, specializing in energy management and industrial automation solutions. Schneider Electric provides data center infrastructure solutions including power management systems, cooling technologies, racks, monitoring software, and integrated data center renovation and modernization services for enterprises and colocation facilities worldwide.

-

In 2024, Schneider Electric expanded its sustainable data center renovation solutions by introducing advanced energy-efficient power distribution units, intelligent cooling technologies, and AI-based monitoring platforms to help operators modernize aging data center infrastructure and improve operational efficiency.

Vertiv (Vertiv Holdings Co.) is a US-based company founded in 1946, specializing in digital infrastructure technologies that support data centers, communication networks, and commercial facilities. Vertiv offers critical infrastructure solutions including thermal management systems, power management equipment, integrated racks, and data center modernization services.

-

In 2024, Vertiv introduced upgraded cooling and power management solutions designed to support high-density computing environments and AI workloads, enabling data center operators to renovate legacy facilities and improve energy efficiency and operational reliability.

Eaton Corporation (Eaton Corporation plc) is an Ireland-based power management company founded in 1911, providing electrical systems, power distribution solutions, and backup power technologies for data centers and industrial applications. Eaton offers uninterruptible power supplies (UPS), power distribution units, energy management software, and infrastructure upgrade solutions for data center modernization.

-

In 2024, Eaton expanded its portfolio of intelligent power management solutions and high-efficiency UPS systems aimed at supporting data center renovation projects, helping operators enhance power reliability, reduce energy consumption, and upgrade aging electrical infrastructure.

Data Center Renovation Market Key Players:

-

ABB

-

Dell Technologies

-

Hewlett Packard Enterprise (HPE)

-

Huawei

-

Rittal

-

Schneider Electric

-

Vertiv

-

Cisco Systems

-

IBM

-

Microsoft (Azure / hybrid infrastructure)

-

Amazon Web Services (AWS)

-

Juniper Networks

-

Arista Networks

-

Siemens

-

Hitachi

-

Fujitsu

-

Oracle

-

NTT Data / NTT Ltd.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 25.55 Billion |

| Market Size by 2035 | USD 114.36 Billion |

| CAGR | CAGR of 16.17% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Renovation Type (Mechanical Renovation, Electrical Renovation, Infrastructure Renovation) •By Renovation Goal (Improved Energy Efficiency, Increased Capacity and Density, Modernization and Upgrading) •By Infrastructure Component (Cooling Systems, Power Systems, Racks and Enclosures, Security Systems) •By Data Center Age (0-5 Years, 6-10 Years, 11-15 Years, 16-20 Years, over 20 Years) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | ABB, Dell Technologies, Eaton, Hewlett Packard Enterprise (HPE), Huawei, Rittal, Schneider Electric, Vertiv, Cisco Systems, IBM, Microsoft, Google Cloud, Amazon Web Services (AWS), Juniper Networks, Arista Networks, Siemens, Hitachi, Fujitsu, Oracle, NTT Data/NTT Ltd. |

Frequently Asked Questions

Ans: The expected CAGR is 16.17% during the forecast period from 2026 to 2035.

Ans: The market size was valued at USD 25.55 billion in 2025 and is expected to reach USD 114.36 billion by 2035.

Ans: The major growth factor is the growing demand for energy-efficient and sustainable data centers, driven by cloud, edge computing, AI workloads, and regulatory sustainability targets.

Ans: The Infrastructure Renovation segment held the largest share of 46.25% in 2025 and is dominant due to extensive upgrades of old data center sites.

Ans: North America dominated the Data Center Renovation Market in 2025 holding 41.21% market share.

Get in Touch