Data Center Robotics Market Report Scope and Overview:

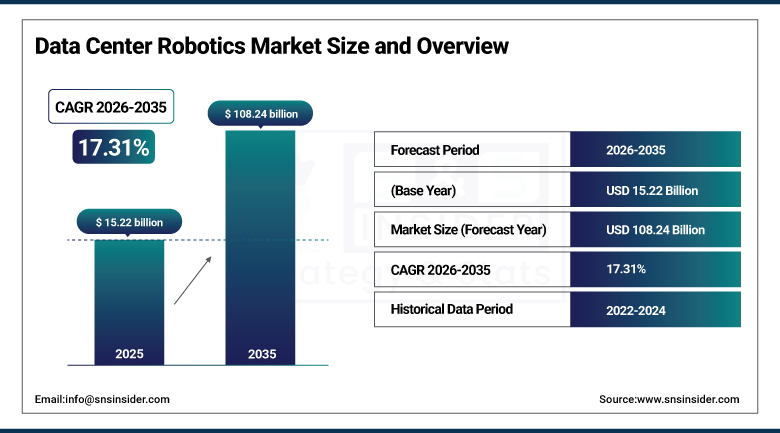

The Data Center Robotics Market was valued at USD 15.22 billion in 2025 and is expected to reach USD 108.24 billion by 2035, growing at a CAGR of 17.31% from 2026-2035.

The Data Center Robotics sector is witnessing high growth because of the increasing capital expenditure in hyperscale clouds architecture, AI-powered data centers, and automation. Increasing complexity in operational management, high server density, and constant uptime requirements are making companies adopt robotics systems that can help in monitoring the infrastructure, performing predictive maintenance, conducting thermal inspections, managing material handling, and surveillance.

Modern robotic equipment integrated with AI, machine learning, computer vision, and LIDAR sensors are helping in improving efficiency, reducing downtime, energy conservation, and automation of tasks. The use of autonomous mobile robots, automatic guided vehicle, robotic arms, and inspection robotics is increasing at hyperscale and colocation facilities.

Data Center Robotics Market Size and Forecast

-

Market Size in 2025: USD 15.22 Billion

-

Market Size by 2035: USD 108.24 Billion

-

CAGR: 17.31% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information on Data Center Robotics Market - Request Free Sample Report

Data Center Robotics Market Trends

-

Increasing reliance on autonomous mobile robots for inspections and maintenance.

-

Growing use of artificial intelligence-driven predictive maintenance and thermal imaging systems.

-

Greater adoption of digital twin systems combined with robotic infrastructure management software.

-

Hyper-scale and edge data centers requiring higher levels of automation.

-

Growing application of robotic surveillance and environmental controls.

-

Robot-as-a-Service (RaaS) making robots more affordable to deploy.

-

Growing use of collaborative robots and robot arms to manage servers and hardware.

-

Increasing application of machine learning and computer vision techniques in robots' functioning.

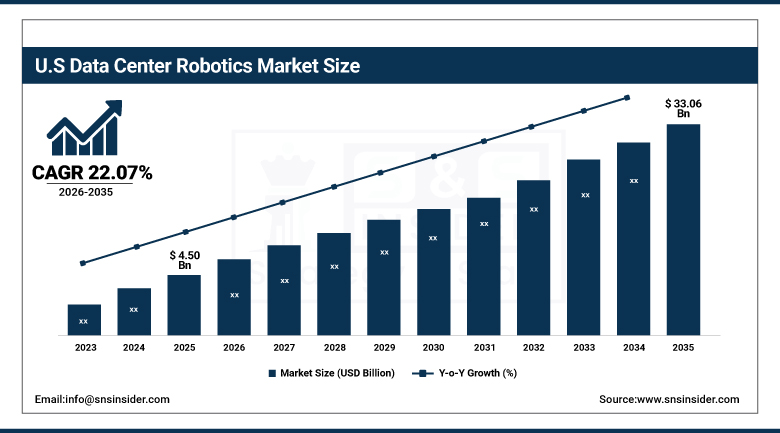

U.S. Data Center Robotics Market was valued at USD 4.50 billion in 2025 and is expected to reach USD 33.06 billion by 2035, growing at a CAGR of 22.07%.

There is strong dominance of the US on the North American market due to fast growth in hyper-scale cloud infrastructures, increased investment in AI data center technologies, and growing utilization of robotic automation technologies among large IT firms. Large players are increasingly utilizing robotic automation technologies to ensure reliability, increase efficiency, and minimize human interference at highly packed computer infrastructure sites. Increasing deployment of AI server and GPU clusters, cloud computing infrastructures, and edge computing facilities is further complicating operations at data centers in the US, hence the need for robotic automation systems.

Data Center Robotics Market Segment Analysis

-

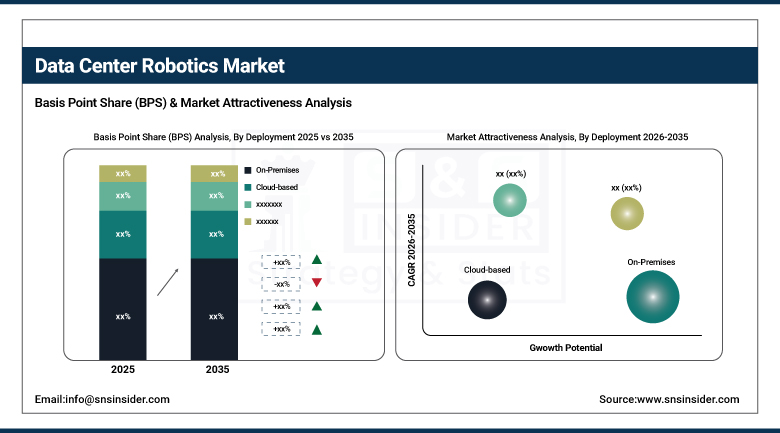

Based on deployment, On-Premises dominated the market in 2025 with approximately 52% revenue share.

-

Based on Enterprise Size, Large Enterprises accounted for nearly 64% market share in 2025 owing to rising deployment of robotic infrastructure systems.

-

Based on Vertical, IT & Telecom dominated the market with around 32% share in 2025 and are expected to maintain strong growth throughout the forecast period.

-

Based on Robot Type, Industrial Robots dominated the market with around 49% share in 2025

-

Based on Component, Hardware segment dominated the market with around 49% share in 2025

By Deployment: On-Premises dominates, Cloud deployment growing rapidly

The On-Premises category held the leading position in the Data Center Robotics Market in 2025, accounting for around 52% market share, owing to the requirement for more effective control, improved cybersecurity, and low latency in robot management in the case of hyperscale and enterprise data centers. Large-scale businesses still favor the on-premise robotics infrastructure for tasks such as server manipulation, automation, maintenance, monitoring of devices, and smart cooling management because of issues related to data privacy, reliability, and compliance. Robotic systems' integration into the internal IT infrastructure enables enterprises to exert full control over the automation processes and reduce the risk of operational disruptions.

The cloud deployment segment is estimated to experience rapid growth during the forecast period, owing to growing demand for AI-powered robotics management systems, remote monitoring solutions, and cloud-based automation systems.

By Enterprise Size: Large Enterprises dominate, SMEs emerging rapidly

Almost 64% share of the Data Center Robotics Market was captured by Large Enterprises in 2025 owing to huge investments made in automation using Artificial Intelligence, infrastructure robotics management, and intelligent operations. Hyperscale cloud providers, telecommunication companies, and global tech giants are increasingly turning towards robotics in order to achieve higher efficiency while performing maintenance, inventory automation, cable management, and environmental monitoring within data centers. Large enterprises have the necessary resources to deploy advanced robotics along with AI analytics, predictive maintenance, and digital twins at various locations within the data center.

The SME category is likely to be the fastest-growing category with regards to the Compound Annual Growth Rate (CAGR). The reason behind such growth would be increased availability of Robotics-as-a-Service, modular automation, and managed robotic systems via cloud computing platforms.

By Vertical: IT & Telecom dominates, BFSI and Healthcare expanding steadily

The IT & Telecom industry held a significant market share of 32% in the Data Center Robotics market share owing to the rise in investments towards the use of hyperscale data centers, cloud computing system, 5G networks, and networks built using artificial intelligence. Robotic automation in telecommunications and cloud service providers is carried out to facilitate automatic server management and smart cooling optimization. Data volume, edge computing, and digitalization remain some of the factors driving the adoption of robotics in the data center.

The BFSI sector and the healthcare sector are set to register substantial growth during the forecast period on account of the rising importance placed on security, system availability, and facility management through robots. The BFSI and healthcare industries are making heavy investments towards the application of robotic data centers based on the adoption of AI analytics, digital banking, telemedicine, and electronic health records.

By Robot Type: Industrial Robots dominate, Collaborative Robots gaining momentum

In the year 2025, the segment of Industrial Robots gained 49% of the total market share due to its high usage in automatic loading and unloading of servers, transportation of hardware components, assembling racks, and infrastructure maintenance. By using industrial robots, there is increased accuracy, less human dependency, and efficiency in performing huge computations in data centers with massive computations. Expenditures in hyperscale infrastructure and the use of a warehouse approach to manage servers boost the requirement for industrial robots.

The segment of collaborative robots is projected to record quick growth throughout the forecast period. Collaborative robots are safe to work in tandem with humans in confined areas in the data center. Collaborative robots are affordable and flexible when compared to industrial robots and are used in inspection, cable management, component replacement, and predictive maintenance.

By Component: Hardware dominates, Software segment growing fastest

The Hardware segment dominated the Data Center Robotics Market with around 49% share in 2025 driven by increasing deployment of robotic arms, autonomous mobile robots, sensors, LiDAR systems, cameras, actuators, and AI-enabled monitoring devices across modern data center facilities. Rising investments in robotic infrastructure modernization, automated cooling systems, and intelligent maintenance equipment continue generating strong demand for advanced hardware components. Growth in hyperscale data centers and edge computing infrastructure is further supporting hardware deployment globally.

The Software segment is expected to register the fastest CAGR throughout the forecast period owing to increasing integration of AI, machine learning, predictive analytics, and robotic orchestration platforms. Advanced robotics management software enables real-time monitoring, autonomous decision-making, predictive maintenance scheduling, and optimization of robotic workflows across complex data center operations.

Data Center Robotics Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

~74% |

|

Europe |

United Kingdom |

~26% |

|

Asia Pacific |

China |

~44% |

|

Middle East and Africa |

UAE |

~30% |

|

Latin America |

Brazil |

~48% |

North America Data Center Robotics Market Insights

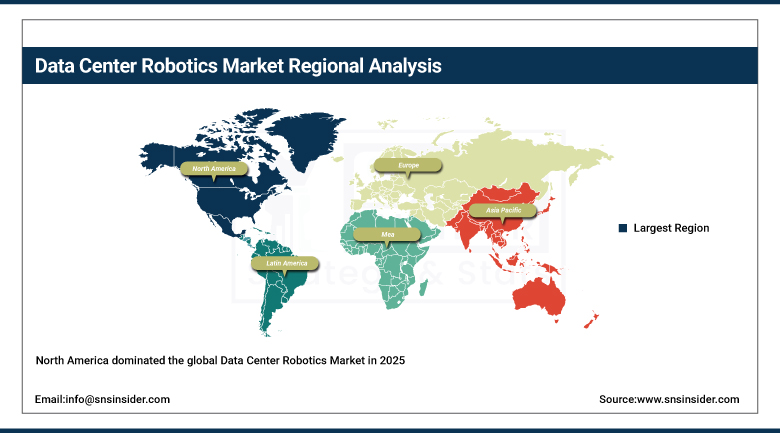

North America dominated the global Data Center Robotics Market in 2025 owing to the region’s strong hyperscale data center ecosystem, high adoption of AI-driven automation technologies, and large-scale investments in cloud computing infrastructure across the United States and Canada. The United States remains the leading regional market due to the presence of major cloud service providers, colocation operators, and technology giants heavily investing in robotic automation for server management, predictive maintenance, cooling optimization, and intelligent infrastructure monitoring. Rapid growth in AI workloads, edge computing deployment, and high-density data centers is accelerating demand for robotic systems capable of improving operational efficiency and minimizing downtime. Increasing focus on energy-efficient infrastructure, autonomous maintenance operations, and smart facility management solutions continues supporting regional market expansion. Rising cybersecurity concerns and the need for uninterrupted data center operations are further encouraging adoption of advanced robotics and AI-enabled automation platforms across North America.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Data Center Robotics Market Insights

Europe represents a significant market for Data Center Robotics driven by increasing digital infrastructure investments, stringent energy efficiency regulations, and growing demand for automated data center management solutions across Germany, the UK, France, the Netherlands, and Nordic countries. Germany remains the largest regional market owing to its advanced industrial automation ecosystem and expanding cloud infrastructure investments. European data center operators are increasingly adopting robotics technologies to optimize power consumption, reduce operational costs, and improve server management efficiency in highly regulated environments. The rapid expansion of AI applications, digital banking services, and enterprise cloud adoption is further fueling demand for robotic automation in regional data centers. Sustainability initiatives and carbon neutrality targets established by the European Union are encouraging adoption of intelligent cooling systems, autonomous monitoring robots, and AI-driven predictive maintenance platforms. Increasing investment in green data centers and smart infrastructure modernization continues supporting long-term market growth across Europe.

Asia Pacific Data Center Robotics Market Insights

Asia Pacific is anticipated to witness the fastest CAGR in the global Data Center Robotics Market in the forecast period attributed to the fast pace of digitalization, growth of hyperscale cloud infrastructure, and growing investment in AI-based automation technology in China, India, Japan, South Korea, and Southeast Asia. China leads in the regional market owing to huge investment in the development of AI infrastructure, rapid growth in domestic cloud companies, and rapid expansion of edge computing infrastructure. India is becoming a significant market owing to the rise in data localization projects, higher internet penetration, and investments in hyperscale data center by leading cloud service providers in the region. Expansion in telecom infrastructure, rollout of 5G technology, and growing requirement for high performance computing have led to an increased demand for robotic automation in regional data centers.

Latin America Data Center Robotics Market Insights

The Robotics Market in Latin American Data Centers is experiencing steady growth driven by growing adoption of cloud technology, digital transformations, and increasing infrastructure of enterprise data centers in Brazil, Mexico, Argentina, and Colombia. The Brazilian market continues to hold leadership in the region due to investments in hyperscale data centers, fintech platforms, and banking infrastructure that require the use of automated data center processes. The increasing demand for cloud-based services and streamers, along with enterprise digitalization, motivates local players to introduce robots in data centers in order to ensure the proper functioning of intelligent monitoring systems and servers. Another significant market is the Mexican one, as a result of growing investments in colocation data centers and cloud infrastructure development.

Middle East & Africa Data Center Robotics Market Insights

The Middle East & Africa Data Center Robotics market is witnessing robust growth because of higher capital expenditures being made on digital infrastructure development, smart cities, and cloud computing. The GCC nations will be at the forefront of adoption in the region as they invest heavily in their digital transformation programs and AI strategy. Countries like Saudi Arabia and the UAE have been quick to develop their cloud computing infrastructures to facilitate smart government solutions, fintech innovations, AI implementations, and other digitalization efforts. Robots are increasingly becoming part of data center operations for maintenance, environmental monitoring, cooling, and improving efficiencies. Increasing internet connectivity and development of more colocation facilities in the region will keep driving the use of robot automation solutions.

Market Growth Drivers:

-

Rising hyperscale data center expansion, AI adoption, and automation requirements driving market growth

The fast growth of hyperscale data centers, cloud computing infrastructure, and AI workloads has been driving up demand for robotics applications in data centers at a faster pace. Robotic technologies that can be used to automate server maintenance, optimize cooling systems, manage assets, and predict potential problems have helped operators to increase efficiency while reducing any possibility of downtime and labor dependence. The fast growth of edge computing infrastructure, 5G infrastructure, and high-density servers is further boosting the demand for robotic technologies capable of handling data center operations. The fast growth of efficient infrastructure, real-time monitoring, and automation of data center facilities is also contributing to strong future demand.

Market Restraints:

-

High infrastructure investment and integration complexity limiting adoption

The implementation of sophisticated robots within the data centers calls for considerable amounts of financial investments in AI-related infrastructure, sensor technology, automation equipment, robotic navigation systems, and software integration solutions. Many firms struggle with the issue of integrating their robotic solutions with already established infrastructure and networks, along with difficulties connected with the management of such technologies. Additionally, issues connected with the risk of cyber-attacks, problems with reliability, and the absence of personnel that is knowledgeable about operating the new technology also limit the use of robotics.

Market Opportunities:

-

AI-powered autonomous operations and edge data center expansion creating future opportunities

With more and more companies adopting AI-based automation solutions, autonomous infrastructure management solutions, and robotics as a service (RaaS), huge potential growth is being generated within the Data Center Robotics market space. With an increase in edge computing infrastructure, smart city infrastructure, and real-time processing environments, there is increased demand for small robotic solutions that can work within distributed data centers. Innovations in areas such as machine learning, predictive maintenance analysis, digital twin solutions, and autonomous monitoring solutions are making robotic systems smarter and more efficient. Increased focus on sustainable and carbon neutral data centers will further fuel growth.

Recent Developments:

-

2026: Equinix launches AI-powered robotic monitoring and automated maintenance at several hyperscale data centers for enhanced operations and infrastructure management.

-

2025: Schneider Electric unveils new generation autonomous robotic technology to provide intelligent cooling, server monitoring, and infrastructure monitoring services within smart data centers.

Data Center Robotics Market Key Players

Some of the Data Center Robotics Market Companies

• ABB Ltd.

• FANUC Corporation

• KUKA AG

• Yaskawa Electric Corporation

• Siemens AG

• Schneider Electric SE

• Vertiv Holdings Co.

• Eaton Corporation plc

• Huawei Technologies Co., Ltd.

• Dell Technologies Inc.

• Hewlett Packard Enterprise (HPE)

• IBM Corporation

• Cisco Systems, Inc.

• Nvidia Corporation

• SoftBank Robotics Group

• Boston Dynamics, Inc.

• Zebra Technologies Corporation

• Omron Corporation

• Mitsubishi Electric Corporation

• Rockwell Automation, Inc

Data Center Robotics Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 15.22 Billion |

| Market Size by 2035 | USD 108.24 Billion |

| CAGR | CAGR of 17.31% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Hardware, Software, Services) • By Deployment (Cloud-based, On-Premises) • By Enterprise Size (Large Enterprises, Small and Medium Enterprises (SMEs)) • By Robot Type (Collaborative Robots, Industrial Robots, Service Robots) • By Vertical (BFSI, Healthcare, Education, IT & Telecom, Government, Retail & E-commerce, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | ABB Ltd., FANUC Corporation, KUKA AG, Yaskawa Electric Corporation, Siemens AG, Schneider Electric SE, Vertiv Holdings Co., Eaton Corporation plc, Huawei Technologies Co., Ltd., Dell Technologies Inc., Hewlett Packard Enterprise (HPE), IBM Corporation, Cisco Systems, Inc., Nvidia Corporation, SoftBank Robotics Group, Boston Dynamics, Inc., Zebra Technologies Corporation, Omron Corporation, Mitsubishi Electric Corporation, and Rockwell Automation, Inc. |

Frequently Asked Questions

Asia Pacific is expected to grow at the fastest CAGR of 23.56% in the Data Center Robotics Market.

Large Enterprises dominated with approximately 64% share in 2025.

On-Premises dominated with approximately 52% share in 2025.

The Data Center Robotics Market was valued at USD 15.22 Billion in 2025.

The Data Center Robotics Market is expected to grow at a CAGR of 17.31% from 2026 to 2032.

Get in Touch