Deep Learning Market Report Scope & Overview:

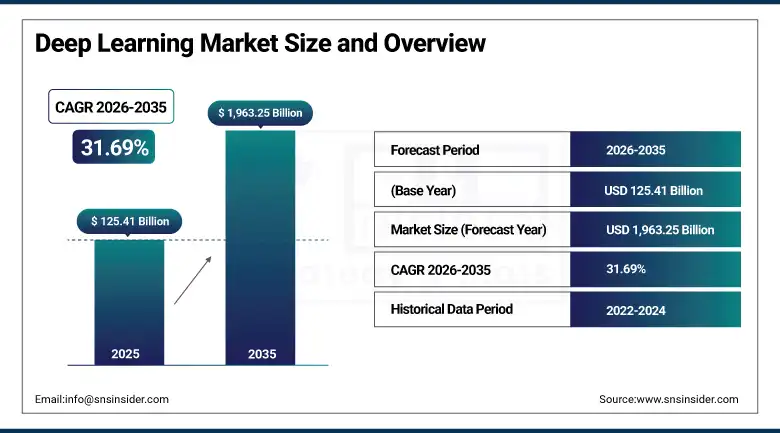

The Deep Learning Market was valued at USD 125.41 Billion in 2025 and is expected to reach USD 1,963.25 Billion by 2035, growing at a CAGR of 31.69% from 2026–2035.

The global deep learning market is growing at a transformative and commercially exceptional pace. Deep learning is a subset of machine learning that uses multi-layered artificial neural networks to extract high-level features from raw data including images, text, audio, and numerical datasets, enabling applications from image recognition and natural language processing to autonomous vehicle perception and medical diagnosis. The market is growing rapidly driven by rising adoption across sectors like healthcare, finance, and automotive, increased investments in AI infrastructure, growing datasets boosting model complexity, and rising training expenses fueling developments in energy-efficient computing. Organizations pursuing deep learning to automate and make decisions create the need for cost-effective and scalable solutions that define market trends and drive innovation.

In 2024, Google DeepMind released Gemini 1.5 Pro, a multimodal deep learning model with a 1 million token context window enabling processing of entire codebases, hour-long videos, and extensive documents in a single inference call. The model’s breakthrough long-context capability creates new commercial deep learning application categories in legal document analysis, scientific literature synthesis, and multimedia content understanding whose practical value sustains enterprise procurement of advanced deep learning infrastructure and API services whose per-token pricing creates recurring commercial revenue.

Market Size and Forecast

-

Market Size in 2026E: USD 165.21 Billion

-

Market Size by 2035: USD 1,963.25 Billion

-

CAGR: 31.69% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Deep Learning Market - Request Free Sample Report

Deep Learning Market Trends

-

Generative deep learning models are driving adoption across content creation, software development, drug discovery, and enterprise AI applications, creating strong demand for advanced AI infrastructure and services

-

Expansion of edge AI deployment in smartphones, autonomous vehicles, IoT devices, and industrial automation is accelerating large-scale adoption of deep learning technologies

-

Multimodal deep learning models capable of processing text, images, audio, and video are enabling more advanced and versatile AI applications across industries

-

Federated learning is gaining traction as organizations seek privacy-preserving AI solutions that support regulatory compliance and secure data utilization

-

Development of energy-efficient AI hardware and optimized model architectures is improving the scalability and cost-effectiveness of deep learning deployment worldwide

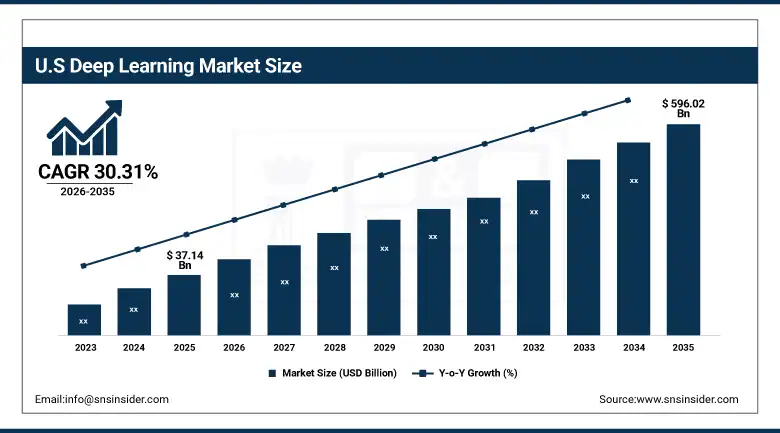

U.S. Deep Learning Market Outlook

The U.S. Deep Learning Market was valued at approximately USD 37.14 Billion in 2025 and is expected to reach approximately USD 596.02 Billion by 2035, growing at a CAGR of approximately 30.31% (SNS Insider confirmed).

The U.S. is the world’s most commercially sophisticated deep learning market within North America’s dominant revenue position. Google, Microsoft, NVIDIA, Meta, and Amazon collectively define the global deep learning technology frontier whose U.S. headquarters creates domestic commercial concentration. The extraordinary U.S. AI investment ecosystem, whose venture capital and corporate R&D sustains the world’s highest concentration of frontier deep learning model development, creates commercial procurement whose scale compounds with model complexity growth. Healthcare AI, autonomous vehicle perception, financial fraud detection, and enterprise automation collectively create the world’s most commercially diverse deep learning application deployment.

NVIDIA launched the Blackwell B200 GPU in 2024 with 20 petaflops of AI performance, specifically optimized for deep learning inference at scale with a new transformer engine architecture that improves large language model inference efficiency by 30x over the prior generation Hopper architecture. The launch demonstrates the extraordinary commercial investment in deep learning infrastructure whose performance improvement per generation sustains enterprise procurement cycles at above-normal capital investment frequency.

Deep Learning Market Segment Analysis

-

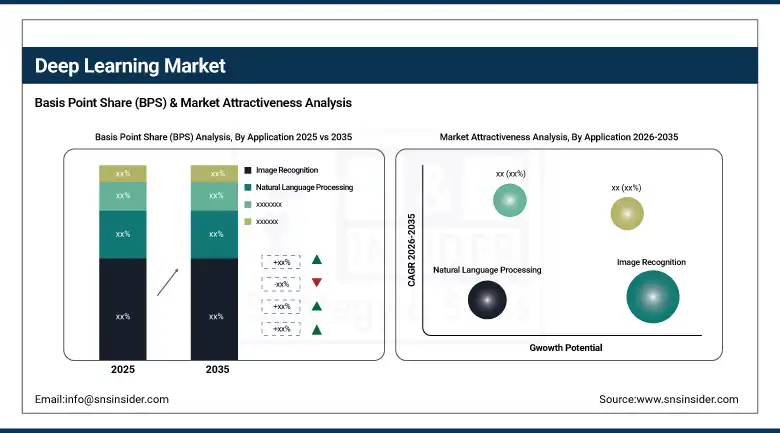

By Application, the Image Recognition segment dominated the Deep Learning Market with approximately 43% share in 2025, while the Data Mining segment is the fastest growing with a CAGR of approximately 34.98%.

-

By Component, the Software segment dominated the Deep Learning Market with approximately 46% share in 2025, while the Hardware segment is the fastest growing.

-

By End User, the Healthcare & Life Sciences segment dominated the Deep Learning Market with approximately 22% share in, while the Automotive & Transportation segment is the fastest growing.

By Application, image recognition dominates, data mining grows fastest

Image recognition retained the dominant application position with approximately 43% of the deep learning market in 2025. Image recognition’s commercial primacy reflects its extraordinary application breadth spanning facial recognition biometrics, medical imaging diagnosis, manufacturing quality inspection, retail visual inventory management, agricultural crop disease detection, and autonomous vehicle environment perception. Each smartphone’s facial unlocks, each hospital’s radiology AI system, and each factory’s automated visual inspection creates image recognition deep learning procurement whose aggregate across billions of daily interactions creates the most commercially significant application category. The computer vision field’s progressive improvement in accuracy, speed, and computational efficiency sustains specification preference for deep learning over classical computer vision alternatives.

Data mining is the fastest-growing application at approximately 34.98% CAGR because the extraordinary growth of enterprise unstructured data is creating demand for deep learning algorithms that extract structured insights from text, logs, transactions, and multimedia data at scale that conventional analytical tools cannot match. Each enterprise digital transformation that creates new data streams whose insights create competitive advantage creates deep learning data mining investment whose commercial motivation compounds with data volume growth. The generative AI revolution’s ability to synthesize insights from previously intractable unstructured data volumes is creating above-average commercial motivation for deep learning data mining investment.

By Component, software dominates, hardware grows fastest

Software retained the dominant component position with approximately 46% of the deep learning market in 2025. Deep learning software’s commercial primacy reflects the foundational requirement for model development frameworks, training orchestration platforms, and inference serving infrastructure whose procurement defines the primary commercial relationship in every deep learning deployment. TensorFlow, PyTorch, JAX, and the commercial AI platform ecosystems built on these foundations create software procurement whose subscription, consumption, and support revenue sustains above-commodity commercial relationships. Each enterprise that deploys deep learning creates software platform procurement whose multi-year relationship sustains recurring revenue that hardware replacement cycles cannot match equivalently.

Hardware is the fastest-growing component because the extraordinary scale of deep learning model training’s computational requirements creates GPU and specialized AI chip capital procurement whose per-quarter investment growth reflects the frontier AI race’s compute escalation. Each new foundation model generation that requires above-prior-generation training compute creates hardware procurement cycles whose frequency exceeds conventional enterprise IT replacement. NVIDIA’s extraordinary revenue growth from AI hardware demonstrates the commercial scale whose per-generation performance improvement sustains premium capital procurement.

By End User, healthcare dominates, automotive grows fastest

Healthcare and life sciences retained the dominant end-user position with approximately 22% of the deep learning market in 2025. The healthcare sector’s extraordinary deep learning application breadth—medical imaging diagnosis, drug discovery, clinical decision support, patient outcome prediction, and genomic analysis—creates the most commercially diverse and highest per-application-value deep learning deployment of any industry. Each FDA-cleared AI medical imaging application creates institutional procurement whose clinical validation evidence sustains adoption across hospital radiology and pathology departments. The pharmaceutical industry’s deep learning drug discovery investment, whose molecular property prediction and clinical trial optimization create quantifiable R&D efficiency improvement, sustains premium procurement that compounds with the drug pipeline’s growth.

Automotive and transportation is the fastest-growing end user because autonomous driving perception, ADAS object and pedestrian detection, and connected vehicle AI system deployment create structured deep learning procurement whose technical requirements create above-average hardware and software investment per vehicle. Each autonomous vehicle program’s sensor fusion deep learning creates training data procurement, model development infrastructure investment, and inference hardware deployment whose combined commercial scale compounds with the vehicle fleet’s progressive AI content increase.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

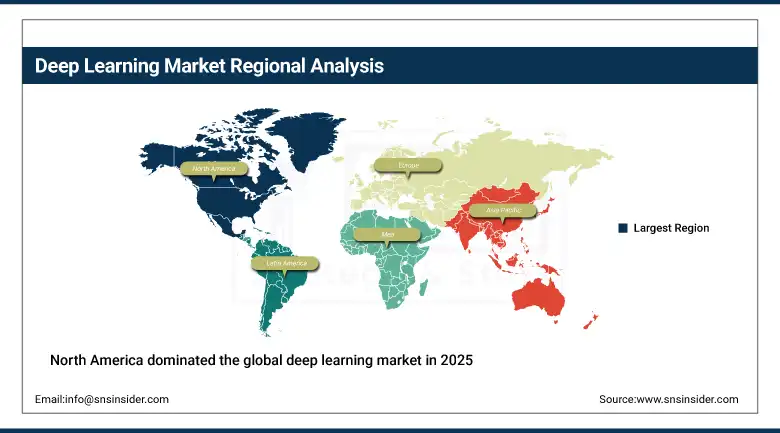

North America Deep Learning Market Insights

North America dominated the global deep learning market in 2025 with the highest AI infrastructure investment and most commercially advanced deep learning application ecosystem. The United States accounts for approximately 87.4% of North American revenues through Google, Microsoft, NVIDIA, Meta, Amazon, and Anthropic’s commercial dominance whose combined portfolio creates the global deep learning technology standard. The extraordinary U.S. AI investment ecosystem sustains frontier model development whose commercial infrastructure creates domestic procurement concentration.

Canada contributes approximately 12.6% of North American revenues through its AI research community including the Vector Institute and Montreal Institute for Learning Algorithms, the technology sector’s deep learning adoption, and international AI firm’s Canadian research operations.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Deep Learning Market Insights

Europe is a technically sophisticated deep learning market where EU AI Act’s regulatory framework, European research excellence in deep learning fundamentals, and industrial sector’s AI adoption create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its automotive AI program me, the manufacturing sector’s industrial AI adoption, and SAP and Siemens’ enterprise AI platform investment.

The United Kingdom, France, and the Netherlands are significant secondary markets where DeepMind’s London operations, national AI strategy’s research investment, and the financial services sector’s deep learning application create consistent premium deep learning procurement.

Asia Pacific Deep Learning Market Insights

Asia Pacific is the fastest-growing regional deep learning market, driven by China’s extraordinary AI investment programme, Baidu’s and Alibaba’s deep learning platform development, Japan’s industrial AI adoption, and India’s rapidly growing AI services sector. China accounts for approximately 44.8% of Asia Pacific revenues through its national AI strategy’s deep learning infrastructure investment, the domestic large model development ecosystem, and the manufacturing sector’s industrial AI deployment.

South Korea’s Samsung and SK Hynix’s AI semiconductor investment, Japan’s SoftBank’s AI portfolio, and India’s technology services sector’s deep learning practice development create significant secondary markets whose combined procurement reinforces Asia Pacific’s fastest-growing regional status.

MEA & Latin America Deep Learning Market Insights

UAE leads MEA revenues at approximately 38.4% through its extraordinary AI infrastructure investment, G42’s deep learning research, and the government’s AI strategy creating structured public sector deep learning procurement. Brazil leads Latin American revenues at approximately 44.2% through its financial services sector’s deep learning fraud detection, the technology sector’s AI adoption, and the growing research community’s model development.

Growth Drivers: Generative AI adoption creating unprecedented model training demand and enterprise automation creating pervasive deployment

Generative AI’s extraordinary commercial adoption is the deep learning market’s most commercially transformative growth driver. The progressive deployment of large language models, image generation systems, and multimodal AI across enterprise software creates deep learning infrastructure procurement whose commercial momentum compounds with each new AI application category’s adoption. Each enterprise that deploys generative AI for productivity, content creation, or decision support creates deep learning infrastructure investment whose recurring operational cost sustains ongoing procurement. Goldman Sachs’ projection of over USD 1 trillion in AI infrastructure investment by 2030 creates the commercial trajectory whose deep learning component creates extraordinary market growth.

Enterprise automation’s progressive deep learning deployment creates pervasive adoption that sustains market growth beyond the frontier AI model training market’s concentrated investment. Each enterprise process that deploys deep learning for automation, prediction, or optimization creates commercial procurement whose aggregate across thousands of simultaneous enterprise AI programmes creates commercial scale. The automation motivation’s ROI measurability in labor cost reduction and error rate improvement creates financial justification that sustains investment through business cycle variation.

Restraints: Energy consumption regulatory pressure and data privacy constraints limiting training data accessibility

Deep learning’s extraordinary energy consumption—with training a single large language model consuming megawatt-hours equivalent to hundreds of households’ annual consumption—creates sustainability pressure whose regulatory and corporate ESG motivation moderates the pace of computational scale escalation. Each data center power purchase agreement at gigawatt scale creates utility infrastructure requirement whose approval process creates deployment timeline constraints.

Data privacy regulation’s restriction on training data collection and use creates capability constraints in privacy-sensitive domains. GDPR’s purpose limitation restricting personal data repurposing for model training, HIPAA’s clinical data protection, and national data localization requirements collectively create training data accessibility limitations that moderate deep learning performance in regulated application domains.

Opportunities: Healthcare diagnostic AI regulatory approval and autonomous vehicle deep learning commercialization

Healthcare diagnostic deep learning’s FDA approval pipeline represents the most commercially premium near-term opportunity whose clinical validation evidence creates institutional adoption motivation. Each new FDA-cleared AI diagnostic application creates hospital procurement that compounds with the imaging AI’s clinical evidence base. The FDA’s progressive approval of AI/ML-based SaMD creates a regulatory framework whose systematic expansion sustains healthcare deep learning commercial development.

Autonomous vehicle deep learning commercialization represents the most commercially transformative automotive opportunity whose full realization would create per-vehicle AI system procurement at global production scale. Each autonomous driving program’s commercial deployment creates deep learning inference hardware and software procurement whose per-vehicle content compounds with fleet electrification and autonomy adoption.

Recent Developments:

-

2024: Google DeepMind released Gemini 1.5 Pro in 2024 with a 1 million token context window enabling processing of entire codebases, hour-long videos, and extensive documents in a single inference call, creating new commercial deep learning applications in legal, scientific, and multimedia content analysis.

-

2024: NVIDIA launched the Blackwell B200 GPU in 2024 with 20 petaflops of AI performance and a new transformer engine that improves large language model inference efficiency by 30x over the prior Hopper architecture, establishing a new deep learning infrastructure performance standard.

-

2024: Microsoft announced Phi-3 Mini, a 3.8 billion parameter small language model in 2024 that achieves large model performance in an on-device deployable format, creating new edge deep learning deployment categories whose memory and compute efficiency enables smartphone and IoT inference without cloud connectivity requirement.

Deep Learning Market Key Players

-

Google LLC (DeepMind/Google Brain)

-

Microsoft Corporation (Azure AI)

-

Amazon Web Services (SageMaker)

-

Meta Platforms Inc. (PyTorch/FAIR)

-

IBM Corporation (Watson AI)

-

Intel Corporation (oneAPI AI)

-

Qualcomm Technologies Inc.

-

Apple Inc. (Core ML)

-

Baidu Inc. (PaddlePaddle)

-

SAP SE

-

Salesforce Inc. (Einstein AI)

-

OpenAI Inc.

-

Anthropic PBC

-

ARM Holdings PLC (Ethos NPU)

-

Clarifai Inc.

-

DataRobot Inc.

-

H2O.ai Inc.

-

C3.ai Inc.

-

Scale AI Inc

Deep Learning Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 125.41 Billion |

| Market Size by 2035 | USD 1963.25 Billion |

| CAGR | CAGR of 31.69% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Component (Hardware/Processors & Chips, Software/Frameworks & Platforms, Services) • by Application (Image Recognition, Natural Language Processing, Data Mining, Speech Recognition, Recommendation Systems, Fraud Detection, Others) • by End User (Healthcare & Life Sciences, Automotive & Transportation, BFSI, Retail & E-Commerce, IT & Telecom, Manufacturing, Media & Entertainment, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | NVIDIA Corporation, Google LLC, Microsoft Corporation, Amazon Web Services, Meta Platforms Inc., IBM Corporation, Intel Corporation, Qualcomm Technologies Inc., Apple Inc., Baidu Inc., SAP SE, Salesforce Inc., OpenAI Inc., Anthropic PBC, ARM Holdings PLC , Clarifai Inc., DataRobot Inc., H2O.ai Inc., C3.ai Inc., Scale AI Inc. |

Frequently Asked Questions

The Deep Learning Market is expected to grow at a CAGR of 31.69% from 2026 to 2035.

The Deep Learning Market was valued at USD 125.41 Billion in 2025.

Rising adoption across sectors like healthcare, finance, and automotive, increased investments in AI infrastructure, and growing datasets boosting model complexity, with generative AI’s extraordinary commercial deployment creating unprecedented deep learning infrastructure procurement demand.

Image Recognition dominated the Deep Learning Market with approximately 43% share in 2025 as confirmed by SNS Insider, while Data Mining is the fastest growing at approximately 34.98% CAGR.

The U.S. Deep Learning Market was valued at approximately USD 37.14 Billion in 2025, growing at a CAGR of 30.31% from 2026 to 2035 as confirmed by SNS Insider.

Get in Touch