Location Intelligence Market Report Scope & Overview:

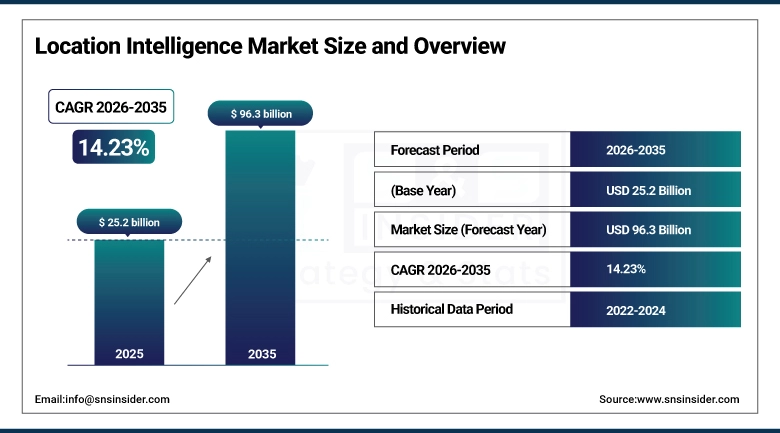

The Location Intelligence Market was valued at USD 25.2 billion in 2025 and is expected to reach USD 96.3 billion by 2035, growing at a CAGR of 14.23% from 2026–2035.

The Location Intelligence Market is experiencing massive growth because businesses across the board realize that location-based information acts as the foundation for any business intelligence, optimization, and strategy planning processes. The location intelligence technology is able to harness the power of geospatial data, IoT feed data, mobile technologies, and advanced analytic features in order to provide businesses with insights on consumer behavior, asset tracking, logistics management, and other market insights.

Industry data consistently demonstrates that organizations deploying location intelligence solutions achieve measurable competitive advantages including 15–25% improvements in field service efficiency, 10–20% reductions in logistics costs through route optimization, and 20–35% increases in retail location-based marketing campaign effectiveness compared to organizations relying on traditional non-spatial analytics approaches.

Location Intelligence Market Size and Forecast

-

Market Size in 2025: USD 25.2 Billion

-

Market Size by 2035: USD 96.3 Billion

-

CAGR: 14.23% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Location Intelligence Market - Request Free Sample Report

Location Intelligence Market Trends

-

Integration of AI and machine learning into geospatial analytics platforms enabling predictive spatial modeling, automated pattern detection, and intelligent route optimization.

-

Growing adoption of real-time location intelligence for supply chain visibility, last-mile delivery optimization, and fleet management across logistics sectors.

-

Expanding use of indoor positioning systems and indoor location analytics in retail, healthcare, and smart building management applications.

-

Rising demand for location intelligence in climate risk assessment, ESG reporting, and environmental compliance monitoring across financial and industrial sectors.

-

Growth of hyperlocal advertising and marketing platforms leveraging location data for precise consumer targeting and foot traffic attribution analytics.

-

Increasing integration of location intelligence with CRM platforms enabling location-contextualized customer journey analytics and field service optimization.

-

Expanding deployment of location intelligence in public health surveillance, epidemic tracking, and healthcare access optimization by government agencies.

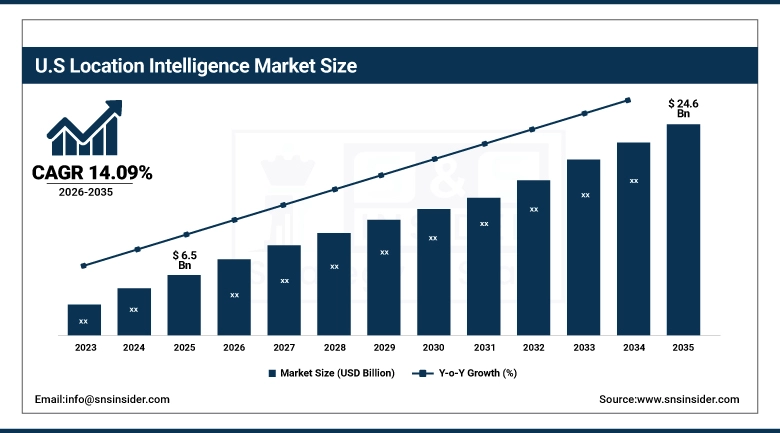

U.S. Location Intelligence Market was valued at USD 6.5 billion in 2025 and is expected to reach USD 24.6 billion by 2035, registering a CAGR of 14.09% during 2026–2035.

The United States Location Intelligence Market is propelled by the world’s most sophisticated geospatial technology ecosystem, the home base location of top platform providers such as Esri, Google, HERE Technologies, and Mapbox, and extensive enterprise deployment of spatial analytics in retail, insurance, real estate, logistics, and public sector organizations. Government spending on geospatial data platforms, smart cities projects, and emergency management solutions generates significant institutional demand.

The U.S. Department of Defense and intelligence agencies’ sustained investment in advanced geospatial intelligence (GEOINT) capabilities, combined with growing state and local government adoption of location intelligence for public safety, emergency management, infrastructure planning, and public health surveillance, represents a large and consistently funded government market segment that is expected to contribute significantly to U.S. location intelligence market growth through 2035.

Location Intelligence Market Segment Insights

-

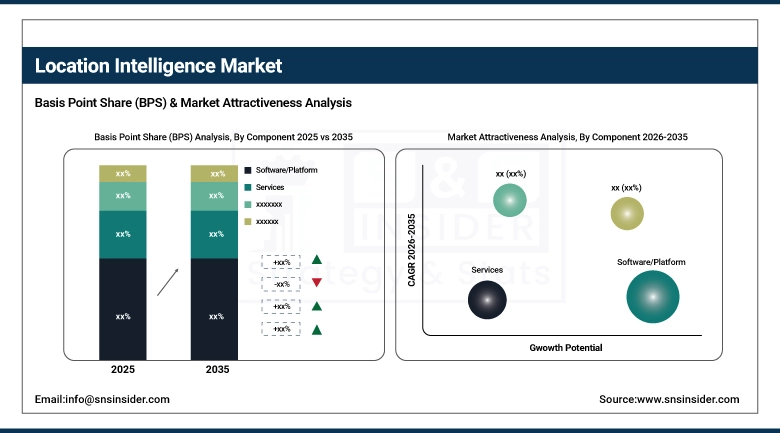

Based on Component, Software/Platform accounted for the largest market share in 2025; Services segment expected to be the fastest-growing segment (CAGR).

-

Based on Deployment, Cloud accounted for the largest market share in 2025; On-Premises holding significant share in government and regulated industries.

-

Based on Organization Size, Large Enterprises accounted for the largest market share in 2025; SMEs expected to grow rapidly as affordable cloud-based platforms expand access.

-

Based on Industry, Government & Public Sector and Retail accounted for the largest market shares in 2025; Transportation & Logistics expected to be among the fastest-growing verticals (CAGR).

Location Intelligence Market Segment Analysis

By Component, Software/Platform dominates, Services expected to grow fastest

Segment-wise, the Software and Platforms category represented the most dominant market share in 2025 due to the rising uptake of location intelligence solutions in enterprises, which combine geospatial data management, spatial analysis, visualization, and app development capabilities. Cloud-native geospatial platforms offered by vendors such as Esri (ArcGIS Online), Google Maps Platform, HERE Technologies, and Mapbox have enabled enterprises to implement location intelligence apps without the need for GIS infrastructure, thereby expanding the market potential across other industry verticals not reliant on GIS software.

The Services category is anticipated to record the highest CAGR during the forecast period. With growing complexity in the development and deployment of location intelligence solutions leveraging multiple data sources, IoT streams, and advanced analytics models, enterprises are looking at service providers for assistance in implementing their projects and deriving insights. Companies that want to ensure maximum value out of their investments in geospatial data are working with service providers to develop implementation roadmaps, identify use cases, and build unique analytics models.

By Industry, Government & Retail lead, Transportation & Logistics expected to grow fastest

Public Sector organizations, including Governments, are the most significant adopters of location intelligence platforms, deploying location analysis for city planning, emergency preparedness, public safety dispatching, environment monitoring, infrastructure assets management, and public health surveillance. Given the geographical aspect inherent in all Government activities such as tax collection, infrastructure management, emergency services, among others, location analysis is one of the critical functions that must be performed in all layers of Government, from the Federal level down to the local Government.

The Transportation & Logistics vertical will record significant growth till 2035, owing to the rapid implementation of real-time location analysis across fleet management, last mile routing, network design, and AV navigation use cases. The exponential rise in E-commerce is driving immense demand for location-based analysis for delivering optimal delivery routes, assessing the performance of carriers, and managing the customer delivery experience. The rise of EV fleets and AVs for deliveries is fueling the adoption of location intelligence within this vertical.

By Application, Sales & Marketing Optimization leads in enterprise, Risk Management growing fastest

Optimizing Sales and Marketing is one of the highly used applications within Location Intelligence, where retailers, real estate firms, financial organizations, and consumer product brands use spatial intelligence for optimization of their store networks, analyzing their trade areas, performing customer segmentation, and managing location-specific marketing campaigns. ROI from location-based marketing, which includes location tracking, competitors’ proximity assessments, and customer catchment modeling is driving the high level of adoption of these techniques.

The Risk Management and Safety vertical is poised to grow at a high CAGR during the forecast period until 2035. Banks, insurers, and industrial organizations are adopting location intelligence capabilities to assess their spatial risk exposures, including climate hazard risks for loans, natural disaster risks for insurance products, and environmental compliance mapping. With the rising emphasis on ESG principles and their integration with location intelligence technology, there is a huge demand for geospatial modeling based on climate risk and ESG reporting.

|

Region |

Major Country |

Share within Region (%) |

|

North America |

United States |

74% |

|

Europe |

United Kingdom |

28% |

|

Asia Pacific |

China |

44% |

|

Middle East & Africa |

UAE |

37% |

|

Latin America |

Brazil |

52% |

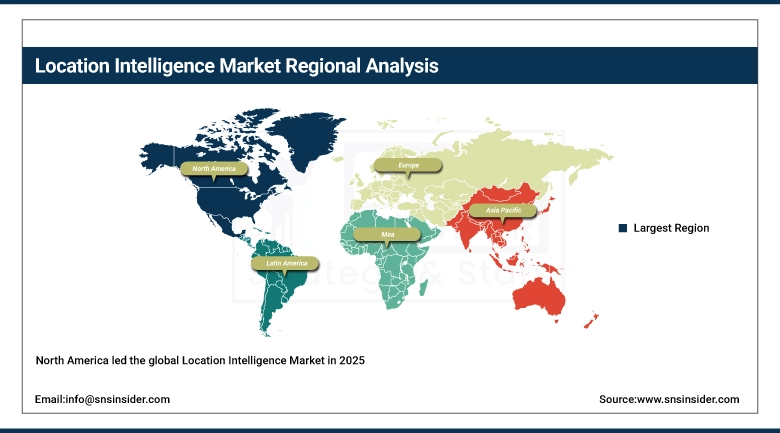

North America Location Intelligence Market Insights

North America led the global Location Intelligence Market in 2025, with the United States accounting for the dominant share. The U.S. benefits from the world’s most advanced geospatial technology ecosystem anchored by Esri’s global GIS platform leadership, Google’s mapping and location services infrastructure, and a vibrant location technology startup ecosystem – combined with high enterprise analytics maturity and strong institutional demand from federal, state, and local government geospatial programs. North America’s advanced retail, financial services, and logistics industries represent particularly intensive location intelligence user segments.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Location Intelligence Market Insights

Asia Pacific is expected to register the fastest CAGR during the forecast period, driven by rapid urbanization, explosive smartphone penetration generating vast location data streams, and government-led smart city development initiatives across China, India, Japan, and Southeast Asia that are creating institutional demand for geospatial analytics platforms. China’s advanced location-based services ecosystem, India’s rapidly digitalizing government and enterprise sectors, and Singapore’s smart nation program represent major regional market opportunities. The region’s large and rapidly expanding IoT device deployment base provides the location data foundation for advanced spatial analytics applications.

Europe Location Intelligence Market Insights

Europe maintained a significant position in the Location Intelligence Market in 2025, with the United Kingdom, Germany, France, and the Netherlands representing primary markets. GDPR data privacy requirements impose meaningful constraints on the collection and processing of individual location data for commercial purposes, creating compliance complexity for location intelligence solution providers but also driving demand for privacy-preserving geospatial analytics capabilities. European government investment in digital infrastructure, smart city programs, and national geospatial data platforms creates consistent institutional market demand.

Middle East & Africa and Latin America Location Intelligence Market Insights

The Middle East & Africa and Latin America Location Intelligence Markets represent high-growth opportunities, driven by rapid urbanization creating demand for smart city geospatial analytics, expanding mobile internet connectivity generating location data at scale, and growing government investment in digital public infrastructure. Gulf Cooperation Council smart city projects including NEOM in Saudi Arabia and UAE’s Smart Dubai initiative are creating significant demand for advanced spatial analytics platforms. Latin America’s growing retail chains, logistics operators, and telecom companies are deploying location intelligence for network planning and customer analytics.

Location Intelligence Market Growth Drivers:

-

Proliferation of IoT devices and mobile platforms generating location data and fueling demand for spatial analytics

The primary growth driver for the Location Intelligence Market is the exponential expansion of location data generated by the proliferation of GPS-enabled smartphones, IoT sensors, connected vehicles, and smart city infrastructure that collectively create an increasingly rich and actionable spatial data environment. As organizations recognize that virtually every business decision has a geographic dimension – from customer acquisition and supply chain design to risk management and asset deployment – the strategic value of location intelligence capabilities is becoming universally recognized. The declining cost and increasing accessibility of cloud-native geospatial platforms are enabling organizations across all sizes and industries to deploy location analytics capabilities that were previously accessible only to large enterprises with specialist GIS teams.

The rapid deployment of 5G network infrastructure is enabling a transformational expansion of real-time location intelligence capabilities, with sub-millisecond positioning accuracy for connected devices, massive IoT sensor network connectivity, and edge computing integration that together enable autonomous vehicle navigation, real-time emergency response coordination, and dynamic infrastructure management applications that represent the next frontier of commercial location intelligence value creation.

Location Intelligence Market Restraints

-

Data privacy regulations and location data security concerns limiting commercial location intelligence adoption

A significant restraint on Location Intelligence Market growth is the complex and evolving global landscape of data privacy regulations that govern the collection, processing, and commercialization of individual location data. GDPR in Europe, CCPA in California, and emerging data protection frameworks globally impose meaningful compliance obligations on organizations collecting and processing individual location data for commercial analytics purposes. The reputational and financial risks of privacy violations are compelling many organizations to adopt conservative location data governance approaches that limit the scope and granularity of location analytics programs, constraining market expansion in certain commercial applications.

Location Intelligence Market Opportunities

-

AI-powered predictive geospatial analytics and real-time location intelligence for autonomous systems

The integration of AI and machine learning into location intelligence platforms represents a transformative growth opportunity, enabling organizations to move from descriptive spatial analytics understanding where things are to predictive and prescriptive geospatial intelligence predicting where things will be and optimizing decisions accordingly. AI-powered location intelligence applications including predictive footfall modeling for retail, dynamic last-mile delivery routing, climate risk-adjusted property valuation, and real-time disaster response optimization are creating compelling new commercial value propositions. The growing adoption of digital twin technologies – which create real-time virtual replicas of physical infrastructure synchronized with live location data – is creating an entirely new category of location intelligence demand aligned with smart city, industrial automation, and autonomous systems applications.

Recent Developments:

-

2026: Esri launched ArcGIS Pro 4.0 with integrated AI-powered geospatial model training capabilities, enabling enterprise users to develop custom spatial prediction models without requiring data science expertise. Google expanded Google Maps Platform with enhanced real-time fleet management and supply chain visibility APIs targeting logistics, last-mile delivery, and field service management enterprise customers.

-

2025 (November): HERE Technologies launched HERE Workspace, an enterprise collaboration platform integrating real-time location data sharing, spatial analytics, and team-based geospatial project management tools, enabling organizations to coordinate location intelligence workflows across distributed teams and partner ecosystems.

Location Intelligence Market Key Players

Some of the Location Intelligence Market Companies

• Esri – ArcGIS Platform, ArcGIS Online

• Google LLC – Google Maps Platform, BigQuery Geo

• HERE Technologies – HERE Location Services, HERE Workspace

•Apple Inc. – Apple Maps, MapKit

• TomTom N.V. – TomTom Maps APIs, TomTom Navigation

• Mapbox Inc. – Mapbox Studio, Mapbox GL

• Hexagon AB – Luciad Portfolio, HxGN Connect

• Pitney Bowes Inc. – Spectrum Spatial, MapInfo Pro

• TIBCO Software Inc. – TIBCO GeoAnalytics

• Oracle Corporation – Oracle Spatial and Graph

• Microsoft Corporation – Azure Maps, Bing Maps Platform

• SAP SE – SAP HANA Spatial Services

• CartoDB, Inc. (Carto) – Carto Platform, Carto Builder

• Foursquare Labs, Inc. – Foursquare Places, Foursquare Analytics

• Trimble Inc. – Trimble GPS Solutions, eCognition

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 25.2 Billion |

| Market Size by 2035 | USD 96.3 Billion |

| CAGR | CAGR of 14.23% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Software/Platform, Services) • By Deployment (Cloud, On-Premises) • By Organization Size (Large Enterprises, SMEs) • By Application (Risk Management & Safety, Sales & Marketing Optimization, Supply Chain Management, Asset Tracking, Customer Experience Management, Others) • By Industry Vertical (Retail, Government & Public Sector, Transportation & Logistics, Healthcare, BFSI, Energy & Utilities, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Esri, Google LLC, HERE Technologies, Apple Inc., TomTom N.V., Mapbox Inc., Hexagon AB, Pitney Bowes Inc., TIBCO Software Inc., Oracle Corporation, Microsoft Corporation, SAP SE, CartoDB, Inc. (Carto), Foursquare Labs, Inc., Trimble Inc. |

Frequently Asked Questions

Asia Pacific is expected to register the fastest CAGR during the forecast period, driven by rapid urbanization, smartphone proliferation generating location data, and government-led smart city development programs across China, India, and Southeast Asia.

Government & Public Sector and Retail segments jointly dominated the Location Intelligence Market in 2025, driven by extensive spatial analytics deployment for urban planning, emergency management, site selection, and consumer behavior analysis.

The proliferation of IoT devices and GPS-enabled mobile platforms generating vast location data streams, combined with the maturation of AI-powered geospatial analytics platforms and growing enterprise recognition of spatial data as a strategic business intelligence asset.

The Location Intelligence Market was valued at USD 25.2 billion in 2025.

The Location Intelligence Market is expected to grow at a CAGR of 14.23% from 2026 to 2035.

Get in Touch