Data Center Transformation Market Report Scope and Overview:

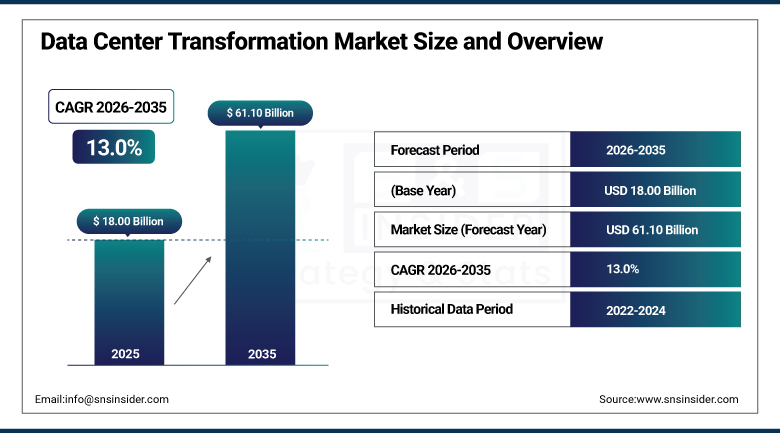

The Data Center Transformation Market was valued at USD 18.00 Billion in 2025 and is projected to reach USD 61.10 Billion by 2035, registering a CAGR of 13.0% from 2026 to 2035.

The Data Center Transformation Market covers the global industry involved in optimizing, upgrading, or reorganizing existing data centers to improve efficiency, scalability, and the ability to serve the needs of modern business, typically taking the form of hardware consolidation, server virtualization, and software upgrades starting with automation and moving toward cloud and hybrid-cloud infrastructures. This transformation involves modernizing infrastructure through virtualization, automation, and deployment of advanced networking solutions, which collectively enhance performance and reduce operational costs. The increased need for agility to support real-time data processing, a requirement heightened by trends such as edge computing and 5G that rely on highly responsive, localized data centers, continues driving organizations to replace legacy systems with agile, scalable, and hybrid environments that boost automation, sustainability, and real-time processing capability.

Equinix continued expanding its global data center footprint throughout 2025, adding new hyperscale capacity across multiple metro markets and reinforcing the company's position as a leading provider of interconnection and colocation infrastructure supporting enterprise data center transformation and hybrid cloud deployment strategies worldwide.

Market Size and Forecast

-

Market Size in 2026E: USD 20.34 Billion

-

Market Size by 2035: USD 61.10 Billion

-

CAGR: 13.0% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

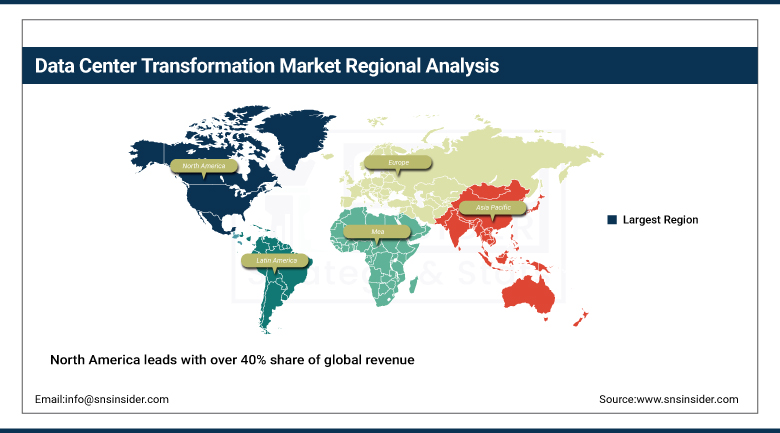

Largest Region: North America (40% share in 2025)

To Get more information On Data Center Transformation Market - Request Free Sample Report

Data Center Transformation Market Trends

-

Cloud integration continues dominating transformation initiatives, particularly in North America, which remains the largest market for these projects.

-

Automation and orchestration continue proving increasingly vital in the Asia Pacific region, reflecting its status as the fastest-growing market for transformation services.

-

Organizations continue deploying software-defined networking and software-defined storage technologies to enhance resource efficiency and agility.

-

Rapid capital inflows from hyperscalers and private equity continue fueling expansion and energy optimization initiatives across the broader data center industry.

-

Regulatory compliance mandates continue accelerating the shift toward higher-tier facilities capable of meeting increasingly stringent uptime and security requirements.

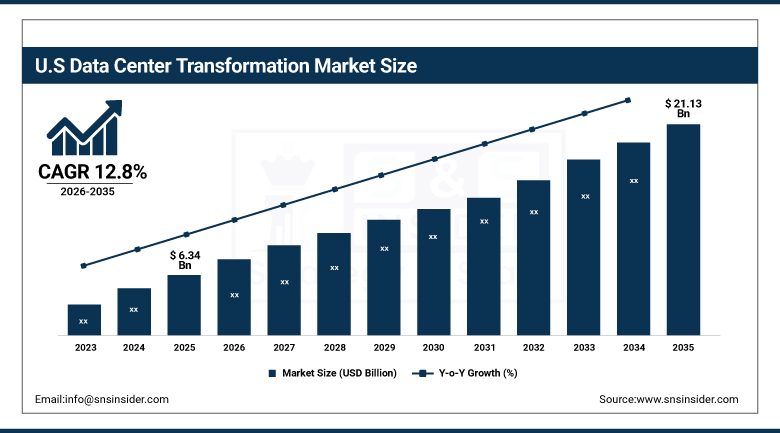

US Data Center Transformation Market Outlook

The US Data Center Transformation Market was valued at approximately USD 6.34 Billion in 2025 and is projected to reach approximately USD 21.13 Billion by 2035, registering a CAGR of approximately 12.8% from 2026 to 2035.

Demand across the United States continued to be shaped by rapid hybrid and multi-cloud infrastructure adoption, letting organizations blend on-premises data centers with public and private cloud resources. This model continued offering flexibility and scalability, helping businesses manage diverse workloads across different cloud environments while maintaining control over sensitive data. Organizations across the country continued embracing cloud solutions for enhanced flexibility and scalability, optimizing energy efficiency to reduce costs and environmental impact, and leveraging AI and automation for smarter data management, evolving industry dynamics that kept the domestic market firmly in the lead globally.

Digital Realty Trust continued expanding its data center partnership and joint venture portfolio throughout 2025, targeting hyperscale and enterprise customers seeking flexible, interconnected data center capacity across major American metro markets to support ongoing digital infrastructure modernization initiatives.

Data Center Transformation Market Segment Analysis

-

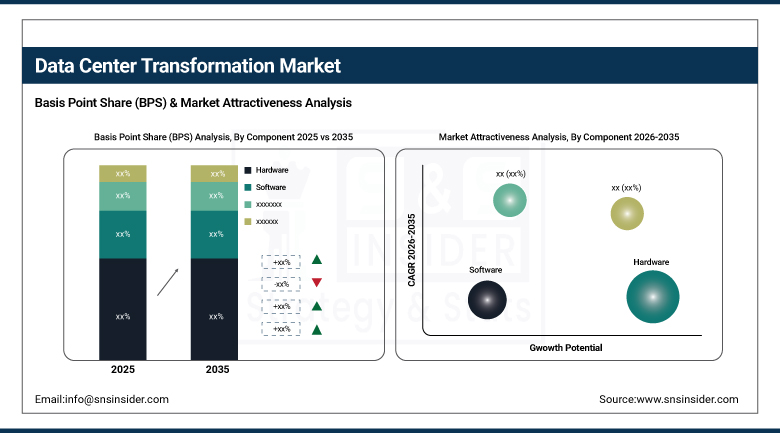

By Component, Hardware led the market with the largest share in 2025, while Software was the fastest-growing component, tracking rising demand for data center infrastructure management platforms.

-

By Service Type, Consolidation Services led the market with an estimated 36.0% share in 2025, while Automation Services was the fastest-growing service type.

-

By Industry Vertical, IT and Telecommunication led the market with an estimated 36.0% share in 2025, while Healthcare was the fastest-growing industry vertical.

-

By Data Center Tier, Tier-3 led the market with an estimated 38.4% share in 2025, while Tier-4 was the fastest-growing data center tier, tracking a projected 15.2% CAGR.

By Component, Hardware led the market, Software grew fastest

The Hardware segment dominated the Data Center Infrastructure Management Market in 2025 owing to the rise in the spending on servers, storage, networking, power management, and cooling equipment required for growing data centers. Growing amount of data generated, cloud services, and deployment of HPC facilities have created a need for robust physical infrastructure. Companies keep focusing on dependable hardware solutions in order to manage data processing and availability efficiently.

The Software segment is the fastest-growing component owing to the rising use of data center infrastructure management software for real-time monitoring, automation, capacity planning, and management. The advanced software helps enterprises perform activities such as prediction of trends, energy management, asset management, and better utilization of resources in data centers. The rising requirement for intelligent infrastructure management, AI, and automation of data centers has increased the use of software solutions in recent times.

By Service Type, Consolidation Services led the market, Automation Services grew fastest

The Consolidation Services segment led the Data Center Infrastructure Management Market in 2025 with an estimated 36.0% share as organizations are making continuous efforts to optimize their existing infrastructure to reduce costs and increase resource utilization. Enterprises are consolidating server, storage, and network resources to make the infrastructure more efficient and manageable. There is an increased emphasis on modernizing, virtualizing, and optimizing the data center infrastructure which is increasing the demand for consolidation services.

The Automation Services segment is the fastest-growing due to the fact that as the data center requirements become more complex, there is a greater need for intelligent solutions in order to manage these processes with minimal human interaction. Automation allows for quicker provisioning, predictive maintenance, optimizing workloads, and efficient energy management. Growth in the usage of artificial intelligence and machine learning is pushing the demand for automation services.

By Industry Vertical, IT and Telecommunication led the market, Healthcare grew fastest

The IT and Telecommunication segment dominated the Data Center Infrastructure Management Market in 2025 with an estimated 36.0% share owing to heavy dependence on big data centers for enabling cloud services, connectivity, digital platforms, and massive data processing capabilities. The growing usage of internet services, rollout of 5G technologies, and digital transformation initiatives by enterprises has led to an increase in demand for infrastructure management solutions in telecom and IT sectors.

The Healthcare segment is the fastest-growing because of the growing generation of digital data from health record systems, medical images, telemedicine applications, and AI-driven diagnostics within healthcare organizations. Data center infrastructure management solutions help healthcare institutions manage their data center workloads and enhance data security and compliance. Increased digitization in the healthcare industry, cloud adoption, and data processing requirements are boosting growth in this market.

By Data Center Tier, Tier-3 led the market, Tier-4 grew fastest

The Tier-3 segment dominated the Data Center Infrastructure Management Market in 2025 with an estimated 38.4% share owing to its optimal mix of reliability, cost-effectiveness, and flexibility. The Tier-3 data center infrastructure management systems offer high availability through the provision of redundant facilities, making it ideal for enterprises which want to conduct operations with minimal disruptions without having to pay extra for high-end tier offerings. This segment is further driven by the growing adoption of collocation services and critical mission applications among enterprises.

The Tier-4 segment is the fastest-growing data center tier, tracking a projected 15.2% CAGR, owing to the increased demand for optimal availability, fault tolerance, and uninterrupted operations. Companies managing mission-critical workloads, AI applications, transactions, and digital services are gradually migrating to Tier-4 centers. The focus on business continuity, high-performance computing, and resilience is boosting Tier-4 data centers.

Regional Insights

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

79.75% |

|

Europe |

Germany |

24.40% |

|

Asia Pacific |

China |

30.90% |

|

Middle East and Africa |

UAE |

26.85% |

|

Latin America |

Brazil |

35.10% |

North America Data Center Transformation Market Insights

North America leads with over 40% share of global revenue, driven by well-equipped infrastructure and significant investments in smart power distribution and cloud infrastructure technologies by major hyperscale operators. Cloud integration continues dominating transformation initiatives across the continent, and that combination of infrastructure maturity and sustained capital investment kept North America the largest addressable market for transformation vendors by a considerable margin.

The United States accounted for roughly 79.75% of regional revenue, anchored by rapid hybrid and multi-cloud infrastructure adoption across enterprise and hyperscale customers alike. Canada added further regional demand through its own growing data center infrastructure investment, and that combined strength kept the continent the largest addressable market for data center transformation vendors through the forecast period.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Data Center Transformation Market Insights

Europe Data Center Transformation Market supported by growing regulatory emphasis on data sovereignty and sustainability alongside continued enterprise digital transformation investment across the region's major economies. Federal and regional compliance mandates including GDPR-driven data residency requirements continued shaping how European organizations approached data center modernization strategy.

Germany led demand at roughly 24.40% of European revenue, supported by its substantial enterprise and industrial digital transformation investment. The UK and France contributed substantial additional demand, and continued European regulatory emphasis on data sovereignty and sustainability should keep regional demand for data center transformation climbing through the forecast period.

Asia Pacific Data Center Transformation Market Insights

Asia Pacific records the fastest growth with CAGR of 14.56% in Data Center Transformation Market, supported by a 50% rise in expected data center capacity, power, and revenue between 2022 and 2026. Internet penetration across the region continues climbing toward roughly 60% by 2025, and such increased demand continues necessitating enhanced data center capability across the region's largest and fastest-digitizing economies.

China led the pack, supported by substantial domestic hyperscale and colocation infrastructure investment. South Korea is anticipated to lead the region's growth specifically, with major players including Alibaba Cloud, Microsoft, and GDS Holdings making substantial investments in expanding data center capacity to satisfy rising demand for cloud services and digital solutions across the broader region.

MEA and Latin America Data Center Transformation Market Insights

The Middle East and Africa and Latin America both showed steady growth, driven by expanding hyperscale and colocation infrastructure investment, growing cloud adoption, and rising government focus on digital infrastructure modernization across both areas. As these markets continued building out modern digital infrastructure, transformation activity grew correspondingly from a considerably smaller base than in more mature data center markets.

The UAE led Middle East and Africa demand, supported by the country's ambitious digital infrastructure agenda and growing status as a regional cloud and colocation hub. Saudi Arabia contributed further demand through its own digital transformation programs. In Latin America, Brazil accounted for the largest share of regional revenue, with growing enterprise cloud adoption continuing to anchor regional demand for data center transformation services.

Growth Drivers: Hybrid Cloud Adoption and Edge Computing Requirements

The increased need for agility to support real-time data processing, a requirement heightened by trends such as edge computing and 5G that rely on highly responsive, localized data centers, continues serving as a primary driver of this market. Cost optimization and energy efficiency remain major growth drivers in the broader data center transformation industry, as organizations recognize that modernized infrastructure delivers measurable operational savings alongside improved performance.

Rapid cloud adoption, AI workloads, edge computing, and IoT data growth continue driving a fundamental shift in global digital infrastructure. Organizations continue replacing legacy systems with agile, scalable, and hybrid environments that boost automation, sustainability, and real-time processing, and that combination of technical necessity and genuine cost benefit is exactly what keeps demand climbing at such a sustained pace across virtually every major industry vertical.

Restraints: Migration Complexity and Security Compliance Challenges

Migration complexity continues delaying a meaningful share of transformation projects, as organizations face genuine technical and operational risk when transitioning mission-critical workloads from legacy infrastructure to modernized, cloud-integrated environments. That complexity keeps some organizations proceeding more cautiously than the broader market's overall growth pace might suggest.

Security concerns and compliance challenges continue affecting a meaningful share of organizations pursuing data center transformation, as regulatory compliance mandates including HIPAA and PCI DSS require genuine care in how sensitive data gets migrated and managed across hybrid and multi-cloud environments. That compliance burden adds real cost and timeline extension to transformation projects, particularly across heavily regulated industries including healthcare and financial services.

Opportunities: AI-Driven Infrastructure Management and Sustainable Data Center Solutions

Revolutionizing data storage with AI-driven technologies represents a genuinely significant opportunity, as organizations increasingly seek infrastructure management platforms capable of leveraging AI and automation for smarter data management. Vendors offering genuinely intelligent, self-optimizing infrastructure management stand to capture meaningful share as enterprises consolidate around fewer, more capable transformation technology partners.

Empowering businesses with sustainable data center solutions offers a second substantial opportunity, as organizations increasingly prioritize optimizing energy efficiency to reduce costs and environmental impact alongside pure performance gains. Vendors that can demonstrate genuinely measurable sustainability improvements alongside operational efficiency stand to capture meaningful share as environmental considerations increasingly factor into enterprise data center modernization decisions.

Recent Developments:

-

2025: Equinix continued expanding its global data center footprint, adding new hyperscale capacity across multiple metro markets to support enterprise interconnection and colocation demand.

-

2025: NTT continued advancing its data center modernization initiatives across Asia Pacific, targeting expanded capacity and improved energy efficiency to meet rising regional cloud services demand.

-

2024: Schneider Electric continued expanding its data center infrastructure management software portfolio, integrating enhanced AI-driven monitoring and energy optimization capability for enterprise and hyperscale customers.

Data Center Transformation Market Key Players

-

Amazon Web Services, Inc.

-

Microsoft Corporation

-

Google LLC (Google Cloud)

-

International Business Machines Corporation (IBM)

-

Oracle Corporation

-

Alibaba Cloud (Alibaba Group)

-

Hewlett Packard Enterprise Company

-

Cisco Systems, Inc.

-

Equinix, Inc.

-

Schneider Electric SE

-

Hitachi Vantara Corporation

-

Tech Mahindra Limited

-

NetApp, Inc.

-

NTT Communications Corporation

-

HCL Technologies Limited

-

Accenture plc

-

Wipro Limited

-

Digital Realty Trust, Inc.

Data Center Transformation Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 18.00 Billion |

| Market Size by 2035 | USD 61.10 Billion |

| CAGR | CAGR of 13.0% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Component (Hardware, Software, Services) • By Service Type (Consolidation Services, Automation Services, Optimization Services, Infrastructure Management Services) • By Industry Vertical (IT and Telecommunication, BFSI, Government, Healthcare, Others) • By Data Center Tier (Tier-1, Tier-2, Tier-3, Tier-4) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Amazon Web Services, Inc., Microsoft Corporation, Google LLC (Google Cloud), International Business Machines Corporation (IBM), Oracle Corporation, Alibaba Cloud (Alibaba Group), Dell Technologies Inc., Hewlett Packard Enterprise Company, Cisco Systems, Inc., Equinix, Inc., Schneider Electric SE, Hitachi Vantara Corporation, Tech Mahindra Limited, Cognizant Technology Solutions Corporation, NetApp, Inc., NTT Communications Corporation, HCL Technologies Limited, Accenture plc, Wipro Limited, Digital Realty Trust, Inc. |

Frequently Asked Questions

The Data Center Transformation Market is expected to grow at a CAGR of approximately 13.0% from 2026 to 2035, based on triangulated secondary research estimates.

The Data Center Transformation Market was valued at approximately USD 18.00 Billion in 2025, based on triangulation across multiple independent research sources.

The major growth factor is the increased need for agility to support real-time data processing, driven by edge computing and 5G trends, combined with cost optimization and energy efficiency demands.

The Consolidation Services segment dominated the Data Center Transformation Market by service type, representing an estimated 36.0% of revenue in 2025.

North America dominated the Data Center Transformation Market in 2025, holding over 40% share of total global market revenue.

Get in Touch