De-identified Health Data Market Report Scope & Overview:

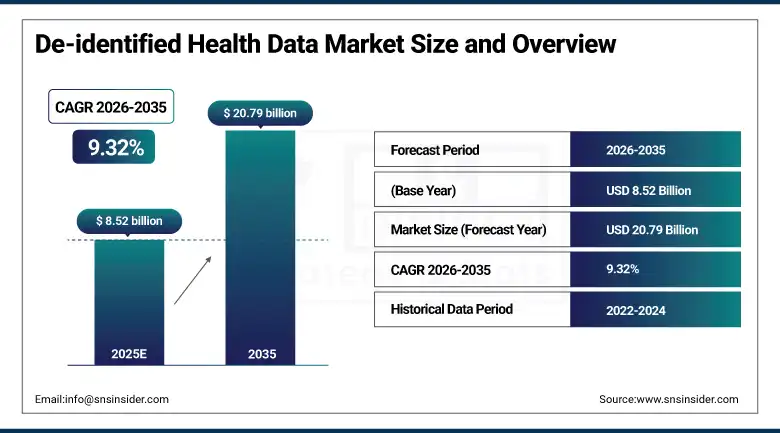

De-identified Health Data Market was valued at USD 8.52 billion in 2025 and is expected to reach USD 20.79 billion by 2035, growing at a CAGR of 9.32% from 2026–2035.

The global De-identified Health Data Market sits at the intersection of the most transformative forces reshaping modern healthcare: the exponential growth of electronic health records creating unprecedented volumes of structured clinical information, the escalating regulatory imperative to protect patient privacy under frameworks including HIPAA and GDPR, and the simultaneous explosion of demand for large-scale, privacy-compliant health datasets to power artificial intelligence model training, real-world evidence generation, clinical research, population health management, and precision medicine programmes. De-identification is the systematic removal or transformation of protected health information and personally identifiable information from patient records, creating datasets that enable legal and ethical secondary use of sensitive medical data without compromising individual patient privacy. The market encompasses data aggregation platforms, de-identification software tools, privacy-preserving analytics infrastructure, and the data products themselves, serving a rapidly expanding ecosystem of pharmaceutical companies, biotechnology firms, health technology developers, research institutions, insurance payers, and government agencies that require large-scale, privacy-compliant health datasets to drive clinical and commercial innovation. The value proposition of de-identified health data is extraordinary: it enables drug developers to analyse real-world treatment outcomes across millions of patients that no clinical trial could cost-effectively recruit, allows AI developers to train diagnostic algorithms on diverse patient populations that improve generalisation across demographic groups, and enables population health programmes to identify at-risk populations before acute health events occur.

The De-identified Health Data Market's 9.32% CAGR from 2026 to 2035 reflects the structural demand acceleration created by the convergence of AI model training requirements that need unprecedented health data volumes, real-world evidence regulatory pathways that are progressively substituting de-identified population data for traditional randomised controlled trials in drug approval submissions, and the healthcare system's transition to value-based care models that require longitudinal, population-scale data analytics impossible without de-identified health data infrastructure. Regulatory frameworks including HIPAA's Safe Harbor and Expert Determination de-identification pathways and GDPR's pseudonymisation provisions are providing the legal certainty that encourages broad institutional investment in de-identified data programme development.

De-identified Health Data Market Size and Forecast

-

Market Size in 2025: USD 8.52 Billion

-

Market Size by 2035: USD 20.79 Billion

-

CAGR: 9.32% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On De-identified Health Data Market - Request Free Sample Report

De-identified Health Data Market Trends

-

Accelerating adoption of federated learning and privacy-enhancing computation technologies that enable AI model training on distributed health datasets without centralising patient records, enabling multi-institutional research collaboration that produces more generalisable models while maintaining institutional data governance and HIPAA compliance.

-

Growing integration of real-world evidence platforms with de-identified health data repositories, enabling pharmaceutical companies to generate post-approval effectiveness and safety evidence from de-identified EHR and claims data that supports regulatory submissions, label expansions, and comparative effectiveness research.

-

Rising investment by health technology companies in longitudinal de-identified patient data platforms that link clinical records, insurance claims, pharmacy dispensing, laboratory results, and patient-reported outcomes across years of care to create the comprehensive patient journey datasets that precision medicine and population health analytics require.

-

Growing demand from AI healthcare developers for de-identified medical imaging datasets, clinical note text corpora, and structured laboratory and vital sign data to train diagnostic models across radiology, pathology, genomics, and clinical decision support applications.

-

Increasing sophistication of re-identification risk assessment methodologies and privacy-preserving technologies including differential privacy, synthetic data generation, and k-anonymity frameworks that enable higher-fidelity de-identified datasets while maintaining stronger privacy guarantees against re-identification attacks.

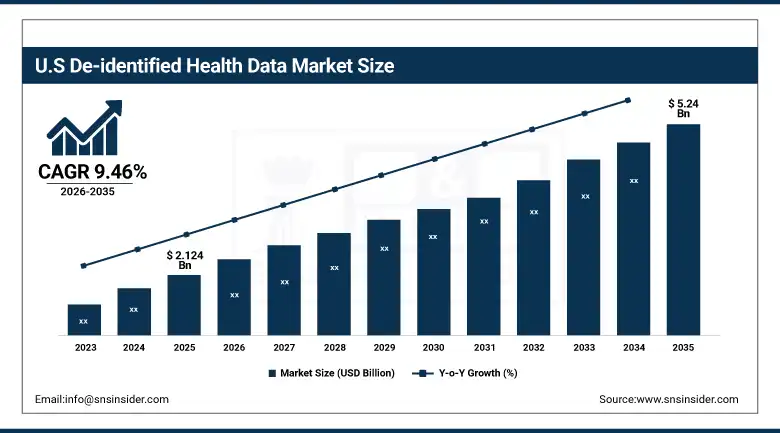

U.S. De-identified Health Data Market was valued at USD 2.124 billion in 2025 and is expected to reach USD 5.24 billion by 2035, growing at a CAGR of 9.46% during 2026–2035.

The U.S. leads the world De-identified Health Data market owing to its extensive infrastructure of electronic health records with more than 96% of all hospitals in the country utilizing the services of certified EHRs, availability of both HIPAA Safe Harbor and Expert Determination regulations for facilitating data-sharing activities, and high density of pharmaceutical, biotechnology and health technology firms that invest in evidence generation and AI-driven healthcare advancements. The U.S. market leadership is ensured by the presence of a robust commercial environment centered around prominent players in the space such as IQVIA, Optum, Veradigm, HealthVerity, Truveta and Komodo Health, in addition to the considerable investments the country is making in precision medicine via the All of Us Research Programme, the data sharing efforts undertaken by the National Cancer Institute, and expanding RWE framework developed by the FDA. One of the latest examples of innovations in this domain include disease-specific cardiometabolic clinical data registries with de-identified patient data announced by Veradigm in February 2025.

The February 2025 Veradigm release of its disease-specific Cardiometabolic Clinical Data Registry datasets, providing de-identified patient health and treatment data for those with targeted cardiometabolic diseases to accelerate clinical research and enhance care outcomes, demonstrates the growing market for curated, disease-specific de-identified health data products that combine the breadth of real-world patient populations with the clinical depth and treatment linkage that pharmaceutical research programmes require. This product category evolution from general data warehouses to curated disease-area data products is creating premium market segments that sustain U.S. De-identified Health Data Market value growth through the 2026 to 2035 forecast period.

De-identified Health Data Market Segment Insights

-

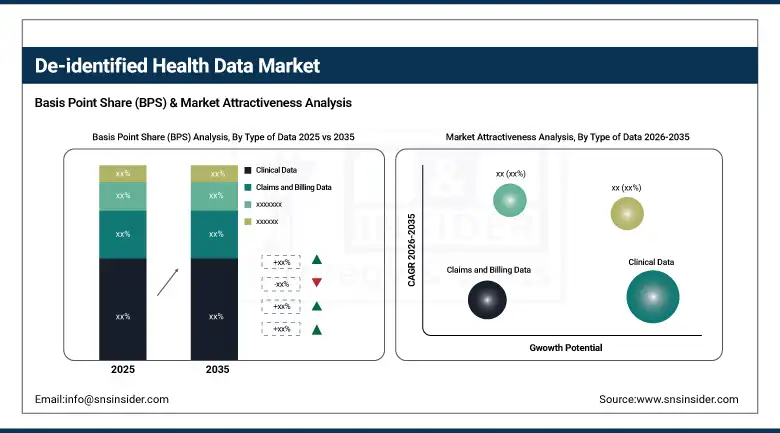

According to Type of Data, Clinical Data dominated with approximately 20.6% market share in 2025, driven by the widespread adoption of electronic health records and the fundamental importance of clinical records in research, treatment development, and patient care optimisation; Behavioral and Patient-Reported Data is expected to grow at the fastest CAGR during the forecast period.

-

In terms of Application, Clinical Research and Trials dominated with approximately 25.62% market share in 2025, driven by the growing reliance on de-identified real-world data for patient cohort identification, protocol optimisation, and regulatory submissions; Drug Discovery and Development is expected to grow at the fastest CAGR as AI-driven drug development accelerates demand for large-scale molecular and clinical datasets.

-

By End-User, Healthcare Providers dominated with the largest revenue share in 2025 through their critical role in clinical decision-making, research, and population health management; Pharmaceutical Companies are expected to grow at the fastest CAGR driven by their essential role in AI-powered drug development, clinical trials, and precision medicine requiring extensive de-identified datasets.

By Type of Data: Clinical Data dominates, Behavioral and Patient-Reported Data grows fastest

Clinical Data retained the dominant position in the De-identified Health Data Market in 2025 with approximately 20.6% of revenues, reflecting the fundamental centrality of structured electronic health record data in research, drug development, population health management, and AI model training applications. Clinical data encompasses diagnoses, medications, procedures, laboratory results, vital signs, imaging reports, and clinical notes from inpatient and outpatient care encounters that collectively represent the most comprehensive and clinically validated record of patient health status and treatment over time. The widespread adoption of certified EHR systems across U.S. and European healthcare systems, which now cover over 96% of U.S. acute care hospitals and the majority of primary care practices in developed markets, has created an unprecedented volume of structured clinical data that can be de-identified and analysed for research and commercial purposes. Clinical data's dominance is sustained by the broad range of applications it serves, from oncology real-world evidence that Tempus contributed de-identified tumor profiles to the National Cancer Institute's Data Enclave in March 2024, through population health analytics that use de-identified clinical records to identify at-risk patient populations, to AI diagnostic model training that requires diverse clinical datasets.

Behavioral and Patient-Reported Data is expected to grow at the fastest CAGR through 2035, driven by the growing recognition that mental health, social determinants of health, lifestyle behaviours, patient-reported symptom burden, and treatment preferences are critical determinants of health outcomes that purely clinical and claims-based datasets cannot capture. The explosion of digital health monitoring through wearable sensors, mobile health applications, and remote patient monitoring platforms is generating unprecedented volumes of continuous behavioural health data including physical activity, sleep patterns, heart rate variability, and mood tracking that, when appropriately de-identified, provide uniquely valuable longitudinal health behaviour datasets for precision wellness and mental health research applications. The growing academic and commercial recognition that social determinants of health including housing stability, food security, and social connection are major predictors of chronic disease progression is creating demand for de-identified datasets that integrate clinical records with social determinant information.

By Application: Clinical Research and Trials dominates, Drug Discovery and Development grows fastest

Clinical Research and Trials retained the dominant application position in 2025 with approximately 25.62% of de-identified health data market revenues, reflecting the pharmaceutical and biotech research industry's extensive and growing use of real-world de-identified patient data for clinical trial feasibility assessment, patient cohort identification, comparator arm construction, safety signal detection, and post-marketing surveillance. The expanding FDA and EMA regulatory acceptance of real-world evidence derived from de-identified health data as supporting evidence for drug approval, label expansion, and pharmacovigilance is progressively converting de-identified data from a research convenience into a regulatory requirement that pharmaceutical companies must invest in to maintain competitive regulatory timelines. ClinicalTrials.gov reporting 564,447 registered studies as of January 2026 confirms the extraordinary scale of global clinical research activity driving demand for de-identified data.

Drug Discovery and Development is projected to grow at the fastest application CAGR through 2035, as AI-powered drug discovery programmes at pharmaceutical companies, biotechnology startups, and technology companies including Insilico Medicine, Recursion Pharmaceuticals, and Exscientia require unprecedented volumes of de-identified molecular, genomic, proteomic, and clinical data to train the machine learning models that identify novel drug targets, predict compound efficacy and toxicity, and optimise clinical trial designs. The integration of de-identified genomic data with longitudinal clinical outcomes data is enabling the identification of genetic variants associated with treatment response that was previously impossible without multi-thousand-patient cohorts assembled through traditional research methods, creating new premium market segments for linked genomic and clinical de-identified datasets commanded by companies like Illumina's Connected Insights and commercial genomics data platforms.

By End-User: Healthcare Providers dominate, Pharmaceutical Companies grow fastest

Healthcare Providers retained the dominant end-user position in 2025, driven by their critical institutional role as both the primary generators and significant consumers of de-identified health data through research, quality improvement, population health management, and AI-enabled clinical decision support programs. Major academic medical centers including Mayo Clinic, Cleveland Clinic, and Johns Hopkins are simultaneously the world's most valuable de-identified health data sources and significant purchasers of de-identified data from complementary healthcare systems and commercial data providers, building comprehensive research platforms that serve their own research programs while creating commercial data products and insights. Hospital systems use de-identified data internally to identify quality improvement opportunities, benchmark clinical outcomes against peer institutions, and power the predictive analytics that enable early identification of high-risk patients for care management intervention.

Pharmaceutical Companies are projected to grow at the fastest end-user CAGR through 2035, driven by the industry's systematic integration of de-identified real-world data into drug development, clinical trial design, post-approval evidence generation, and commercial launch optimization workflows that was previously concentrated at the largest global pharmaceutical companies but is progressively expanding through the mid-size and specialty pharma segments as de-identified data platforms commoditized access. The largest pharmaceutical companies including Pfizer, Roche, AstraZeneca, and Eli Lilly are building multi-year data partnerships with commercial de-identified data platforms that provide continuous access to linked claims, clinical, and specialty data enabling real-world evidence generation across their full development and commercial portfolio, creating premium long-term contract revenue for leading de-identified health data providers.

De-identified Health Data Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|---|---|---|

|

North America |

United States |

~83% |

|

Europe |

Germany |

~30% |

|

Asia Pacific |

China |

~42% |

|

Middle East & Africa |

UAE |

~27% |

|

Latin America |

Brazil |

~43% |

North America De-identified Health Data Market Insights

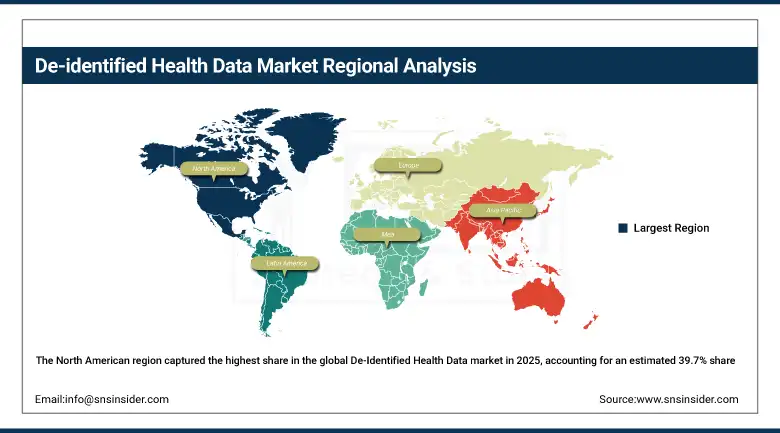

The North American region captured the highest share in the global De-Identified Health Data market in 2025, accounting for an estimated 39.7% share of total global market revenues, headed by the U.S. at around 83% of North American revenues. Leadership of the U.S. market is supported by the world's largest EHR deployment base, HIPPA's de-identification regulatory structure and certainty, and the high concentration of drug discovery and health tech companies whose need for real-world evidence and training data fuels the market's dynamics. The growing NIH mandate on data sharing and FDA expansion of the real-world evidence regime are structurally driving market revenues higher.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific De-identified Health Data Market Insights

Asia Pacific is the fastest-growing regional de-identified health data market, driven by rapid healthcare digitization in China, India, Japan, and South Korea, government-led health information exchange program development, and rising investments in genomics and precision medicine research that require large-scale de-identified dataset access. China's national health information system expansion and India's Ayushman Bharat Digital Mission are creating government-managed health data infrastructure that is progressively enabling de-identified data utilization for population health research and pharmaceutical innovation. Japan and South Korea's advanced genomics research programs and sophisticated pharmaceutical industries create growing regional demand for linked genomic and clinical de-identified datasets.

Europe De-identified Health Data Market Insights

Europe represents a significant and growing de-identified health data market, shaped by GDPR's stringent requirements for data anonymization that have simultaneously raised the compliance standard for de-identification while creating clear legal pathways for compliant data use. The European Health Data Space initiative is progressively creating cross-border health data sharing infrastructure that will enable pan-European research datasets of unprecedented scale. Germany's national health data research network, the UK Biobank's world-class longitudinal research dataset, and France's Health Data Hub are each creating distinctive national de-identified health data infrastructure attracting substantial pharmaceutical and academic research investment.

Middle East & Africa and Latin America De-identified Health Data Market Insights

MEA and Latin America are growing de-identified health data markets supported by national digital health reform programmers and public-private partnerships that are creating the EHR infrastructure and data governance frameworks enabling de-identified data utilization. Brazil leads Latin American revenues through its unified health system's extensive patient database and growing collaboration with international pharmaceutical companies seeking real-world evidence from Latin American patient populations with distinct genetic diversity and disease burden characteristics.

De-identified Health Data Market Growth Drivers:

-

AI model training requirements and real-world evidence regulatory acceptance creating structural demand for privacy-compliant, large-scale health datasets

The primary structural growth drivers for the De-identified Health Data Market are the exponential demand for large-scale, diverse, privacy-compliant health datasets to train increasingly capable healthcare AI models, and the regulatory expansion of real-world evidence frameworks that are progressively accepting de-identified health data as supporting or primary evidence in drug approval and medical device clearance submissions. Healthcare AI developers require millions of annotated patient records spanning diverse demographics, disease presentations, and treatment patterns to build diagnostic models that generalize reliably across real-world clinical populations, creating a structural demand for de-identified health data that grows proportionally with AI model complexity and ambition.

Oracle Health's March 2024 delivery of its Oracle Health Data Intelligence suite enhancements, including a generative AI service for care management and deeper data integration across EHR systems, combined with Epic's October 2025 preview of new developer tools and interoperability features supporting cloud-native data exchange, collectively confirm that the world's dominant EHR platform providers are building the data infrastructure that will progressively unlock larger volumes of de-identified clinical data for research and commercial analytics applications through the 2026 to 2035 forecast period.

De-identified Health Data Market Restraints

-

Re-identification risk concerns, inconsistent de-identification methodology standards, and complex multi-jurisdictional regulatory compliance limiting cross-border data sharing

A significant restraint on the De-identified Health Data Market is the persistent concern about re-identification risk, where advances in data science and the availability of auxiliary information sources enable statistical re-identification of supposedly de-identified individuals with increasing precision, creating liability risk and regulatory scrutiny for organizations that share de-identified health data. The absence of globally harmonized de-identification standards creates regulatory complexity for organizations operating across HIPAA, GDPR, and national health privacy law jurisdictions, where different legal definitions of adequate anonymization, different approved de-identification methods, and different regulatory enforcement approaches create compliance uncertainty that limits cross-border data sharing programs. High costs of implementing enterprise-grade de-identification infrastructure including software licensing, technical expertise, legal review, and ongoing monitoring create adoption barriers particularly for smaller healthcare organizations and research institutions with limited data management budgets.

De-identified Health Data Market Opportunities

-

Synthetic health data generation, federated learning partnerships, and European Health Data Space infrastructure development

Synthetic health data generation, where statistical models trained on real patient records create entirely artificial patient records that preserve the statistical properties and clinical relationships of the original population without containing any real patient information, represents the most privacy-preserving data sharing approach and is progressively gaining regulatory acceptance as a complement to traditional de-identification for AI training and population simulation applications. Federated learning partnerships that enable AI model training across distributed healthcare system datasets without centralizing patient records represent a transformative approach to multi-institutional research collaboration that maintains institutional data governance while enabling the model performance improvements achievable through larger training populations. The European Health Data Space's progressive implementation is expected to unlock cross-border European health data access at scale, creating the world's largest unified de-identified health data research environment and attracting substantial pharmaceutical and academic investment.

Recent Developments:

-

February 2025: Veradigm introduced its disease-specific Cardiometabolic Clinical Data Registry datasets comprising de-identified patient health and treatment data for specific cardiometabolic diseases, which were meant to speed up clinical research and improve patient outcomes for pharmaceutical and research customers.

-

October 2025: Epic Systems announced developer tools and interoperability upgrades like API improvements and data exchange functionality between patients and providers, making it easier to use cloud-based workflows that allowed wider access to de-identified research datasets.

-

March 2024: Oracle Health announced updates to its Oracle Health Data Intelligence platform suite, which included introduction of its new generative AI tool for care management and improvements in EHR agnostic data integration for enhanced de-identification of clinical data sets.

-

2025: Truveta extended its health data de-identification platform through partnership agreements with more hospital systems, expanding its linked real world patient dataset to include a more diversified pool of patients in the United States for its research customers.

-

2025: HealthVerity introduced a solution that could be used for building patients’ de-identified journeys via claims, clinical, specialty pharmacy and laboratory data sources, while avoiding the necessity of obtaining patient consent for data de-identification for its oncology and rare disease pharmaceutical customers.

De-identified Health Data Market Key Players

-

IQVIA Holdings Inc.

-

Oracle Health (Cerner Corporation)

-

Merative (IBM Watson Health)

-

Optum Inc. (UnitedHealth Group)

-

Veradigm LLC

-

HealthVerity Inc.

-

Truveta Inc.

-

Komodo Health Inc.

-

Clarify Health Solutions Inc.

-

Tempus Labs Inc.

-

Flatiron Health Inc.

-

H1 Insights Inc.

-

TriNetX LLC

-

Aetion Inc.

-

Verantos Inc.

-

Privacy Analytics Inc. (IQVIA)

-

Mendel.ai Inc.

-

Datavant Inc.

-

Nference Inc.

-

SAS Institute Inc.

De-identified Health Data Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 8.52 Billion |

| Market Size by 2035 | USD 20.79 Billion |

| CAGR | CAGR of 9.32% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type of Data (Clinical Data, Claims and Billing Data, Pharmaceutical and R&D Data, Genomic and Molecular Data, Behavioral and Patient-Reported Data, Others) • By Application (Clinical Research and Trials, Drug Discovery and Development, Population Health Management, AI and ML Model Training, Value-Based Care and Quality Improvement, Others) • By End-User (Pharmaceutical Companies, Healthcare Providers, Health Insurance and Payers, Biotechnology Firms, Academic and Research Institutions, Government and Regulatory Agencies, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | IQVIA Holdings Inc., Oracle Health (Cerner Corporation), Merative (IBM Watson Health), Optum Inc. (UnitedHealth Group), Veradigm LLC, HealthVerity Inc., Truveta Inc., Komodo Health Inc., Clarify Health Solutions Inc., Tempus Labs Inc., Flatiron, Health Inc., H1 Insights Inc., TriNetX LLC, Aetion Inc., Verantos Inc., Privacy Analytics Inc. (IQVIA), Mendel.ai Inc., Datavant Inc., Nference Inc., SAS Institute Inc. |

Frequently Asked Questions

North America dominated the market with approximately 39.7% of global revenues in 2025, led by the United States with the world's most extensive EHR infrastructure, HIPAA's established de-identification frameworks, and the concentration of pharmaceutical, biotechnology, and health technology companies whose demand for real-world evidence and AI training data drives market leadership.

Clinical Data dominated with approximately 20.6% of revenues in 2025, driven by the widespread adoption of certified EHR systems across hospitals and primary care practices, the fundamental centrality of structured clinical records for research and AI model training, and the broad range of pharmaceutical, population health, and precision medicine applications that clinical datasets serve.

The exponential demand for large-scale, privacy-compliant health datasets to train healthcare AI models, combined with the expanding FDA and EMA regulatory acceptance of real-world evidence derived from de-identified health data in drug approval submissions, and the universal healthcare transition toward value-based care models requiring population-scale longitudinal data analytics.

The De-identified Health Data Market was valued at USD 8.527 billion in 2025.

The De-identified Health Data Market is expected to grow at a CAGR of 9.32% from 2026 to 2035.

Get in Touch