Deep Packet Inspection Market Report Scope & Overview:

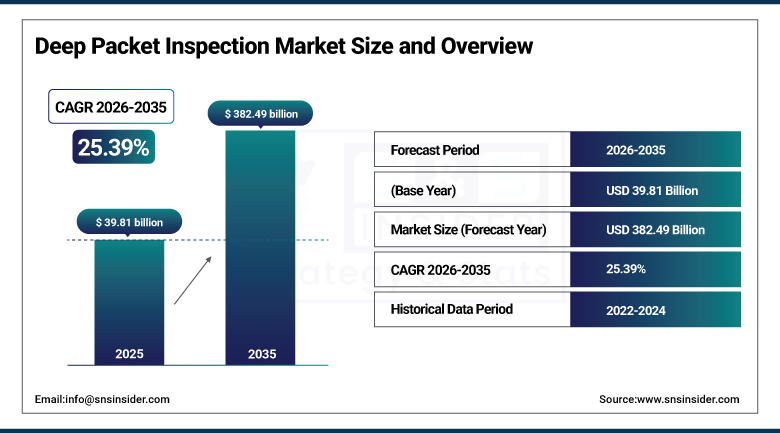

The Deep Packet Inspection Market was valued at USD 39.81 Billion in 2025 and is expected to reach USD 382.49 Billion by 2035, growing at a CAGR of 25.39% from 2026–2035.

Deep packet inspection is the technology that lets a network actually look inside the data flowing through it, not just the address it's headed to, but what's in the payload itself. That distinction matters a lot for security teams, because plenty of modern attacks hide inside traffic that looks perfectly normal at a glance. DPI tools dig deeper, flagging malware, policy violations, or bandwidth hogs that simpler filtering would miss entirely. Demand has taken off as 5G networks and the sprawling growth of IoT devices push traffic volumes to levels that older network management tools just weren't built for, and as cyberattacks keep getting more sophisticated, organizations are under real pressure to see what's actually moving across their networks rather than guessing.

In February 2024, ipoque showcased its next-generation DPI and Encrypted Traffic Intelligence solutions at MWC Barcelona, using machine learning and deep learning to improve application classification even when traffic is encrypted. The approach reduces the blind spots that have become an increasing headache for network operators as encryption adoption climbs, giving security teams better visibility into what applications are actually running on their networks without needing to decrypt every session.

Market Size and Forecast

-

Market Size in 2026E: USD 49.92 Billion

-

Market Size by 2035: USD 382.49 Billion

-

CAGR: 25.39% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Deep Packet Inspection Market - Request Free Sample Report

Deep Packet Inspection Market Trends

-

AI and machine learning are getting folded into DPI platforms so they can spot unusual traffic patterns and flag emerging threats without waiting on a human analyst to notice something's off.

-

Encrypted traffic intelligence is becoming a must-have feature, since more of the internet runs over TLS now and traditional DPI can't peek inside encrypted payloads the way it used to.

-

Telecom operators are leaning on DPI harder as 5G rolls out, since the sheer volume and speed of 5G traffic demands far more sophisticated real-time analysis than 4G networks ever needed.

-

Standalone DPI appliances are gaining traction with governments and critical infrastructure operators who need deep, customizable inspection that integrated firewall modules can't quite match.

-

Content regulation use cases are expanding fast in regions with stricter internet governance rules, pushing DPI beyond pure security into policy enforcement territory.

U.S. Deep Packet Inspection Market Outlook

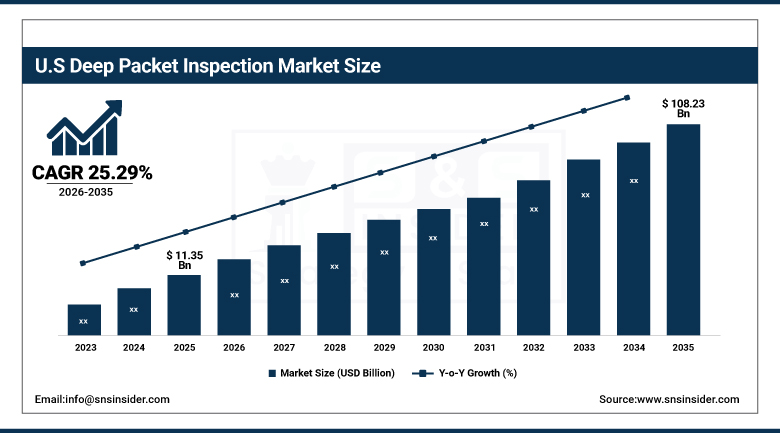

The U.S. Deep Packet Inspection Market was valued at approximately USD 11.35 Billion in 2025 and is expected to reach approximately USD 108.23 Billion by 2035, growing at a CAGR of approximately 25.29%.

Cybersecurity threats keep escalating, network performance demands keep climbing, and regulatory compliance keeps getting stricter, and all three of those are pushing U.S. organizations toward DPI at a pretty aggressive pace. As digital transformation accelerates and more workloads shift to the cloud, companies are investing heavily in tools like DPI to keep data secure and communications intact. The rapid rollout of IoT devices and 5G infrastructure has only added to network traffic volumes, meaning the kind of granular analysis DPI provides isn't optional anymore for a lot of enterprises. Add in a national policy focus on cybersecurity, and you've got a market that's growing about as fast as any in this report.

In late February 2025, NETSCOUT enhanced its Arbor Threat Mitigation System with additional AI and machine learning functionality built on its deep packet inspection foundation, aimed at better detecting and blocking malicious traffic. The update came as the company reported DDoS attacks had climbed 55% over the prior four years, underscoring why network operators are increasingly demanding DPI-powered defenses that can adapt to new attack patterns automatically rather than relying on static signature updates alone.

Deep Packet Inspection Market Segment Analysis

-

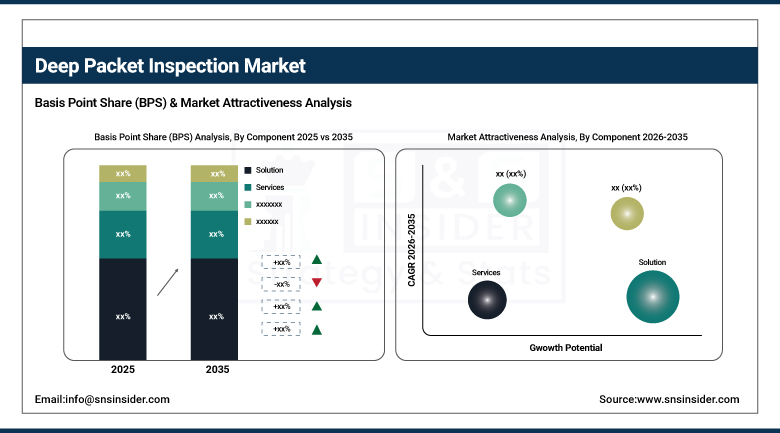

By Component, the Solution segment dominated the Deep Packet Inspection Market with approximately 71% share in 2025, while the Services segment is the fastest growing with a CAGR of approximately 26.63%.

-

By Installation, the Integrated segment dominated the Deep Packet Inspection Market with approximately 59% share in 2025, while the Standalone segment is the fastest growing with a CAGR of approximately 26.47%.

-

By Enterprise Size, the Large Size Enterprises segment dominated the Deep Packet Inspection Market with approximately 39% share in 2025, while the SME segment is the fastest growing with a CAGR of approximately 24.57%.

-

By Application, the Network Security segment dominated the Deep Packet Inspection Market with approximately 45% share in 2025, while the Content Regulation segment is the fastest growing with a CAGR of approximately 28.21%.

-

By End-use, the BFSI segment dominated the Deep Packet Inspection Market with approximately 29% share in 2025, while the Retail segment is the fastest growing with a CAGR of approximately 27.95%.

By Component, solutions dominate, services grow fastest

Solutions made up about 71% of the market in 2025, and that's really a reflection of how central DPI software has become to traffic management, threat detection, and bandwidth optimization across enterprise and telecom networks alike. These platforms give real-time analytics and filtering that plug into existing IT infrastructure fairly cleanly, which is exactly why they've stayed the default choice over other approaches for so long.

Services are growing faster, at around 26.63% CAGR, as more organizations lean on managed security providers to actually deploy and run these systems day to day. Moving to cloud and hybrid environments has made expert-led consulting and integration support more valuable than it used to be, especially for companies that don't have deep in-house networking expertise but still need DPI running reliably.

By Installation, integrated leads, standalone grows fastest

Integrated installations, meaning DPI built directly into firewalls, routers, and intrusion prevention systems, held around 59% of the market in 2025. Bundling DPI into equipment organizations are buying anyway cuts down deployment complexity and hardware costs, which is a pretty easy sell for most IT teams that would rather avoid managing yet another standalone system.

Standalone DPI is growing faster, at roughly 26.47% CAGR, mostly because governments and critical infrastructure operators need something more customizable than what's bundled into off-the-shelf network gear. Law enforcement applications and specialized policy enforcement use cases benefit from dedicated processing power and finer-grained control that integrated solutions simply can't offer at the same depth.

By Enterprise Size, large enterprises dominate, SMEs grow fastest

Large enterprises accounted for about 39% of the market in 2025, which makes sense given their bigger budgets, sprawling network footprints, and heavier regulatory obligations. Operating across multiple countries and industries means these organizations need advanced DPI capable of securing data flows and enforcing policy at a scale smaller businesses just don't have to worry about.

SMEs are the fastest-growing segment, at around 24.57% CAGR, as cyber threats increasingly target smaller businesses that used to fly under the radar, and as more of them shift to cloud-based operating models. DPI gives SMEs a scalable, relatively affordable way to protect their networks, and better awareness combined with flexible pricing is making that option a lot more attainable than it used to be.

By Application, network security dominates, content regulation grows fastest

Network security led application-based demand with roughly 45% share in 2025, driven by the steady rise of advanced persistent threats, zero-day attacks, and encrypted traffic that's harder to police with older tools. DPI's ability to look past packet headers into the actual payload gives real-time visibility into malicious patterns that other approaches miss, which is exactly why it keeps anchoring broader cybersecurity strategies.

Content regulation is growing fastest, at around 28.21% CAGR, fueled by governments around the world tightening control over what content flows across their networks. DPI gives regulators and institutions the precision to identify and filter specific content, and demand is climbing not just from governments but from schools and enterprises that want more control over what happens on their internal networks too.

By End-use, BFSI dominates, retail grows fastest

Banking, financial services, and insurance accounted for about 29% of end-use demand in 2025, unsurprisingly, given how sensitive financial data is and how heavily regulated the sector remains. DPI plays a central role in protecting transactional data and spotting anomalies, and with customer trust and regulatory compliance both riding on network security, financial institutions have every incentive to invest heavily here.

Retail is the fastest-growing end-use segment, at roughly 27.95% CAGR, as the sector's rapid shift toward omnichannel platforms and online transactions creates a lot of new data worth protecting. Retailers process enormous volumes of consumer information now, and DPI's ability to support real-time monitoring and fraud detection has become fairly essential for protecting both brand reputation and the customer experience.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.0% |

|

Europe |

Germany |

23.0% |

|

Asia Pacific |

China |

40.0% |

|

Middle East & Africa |

UAE |

30.0% |

|

Latin America |

Brazil |

37.0% |

North America Deep Packet Inspection Market Insights

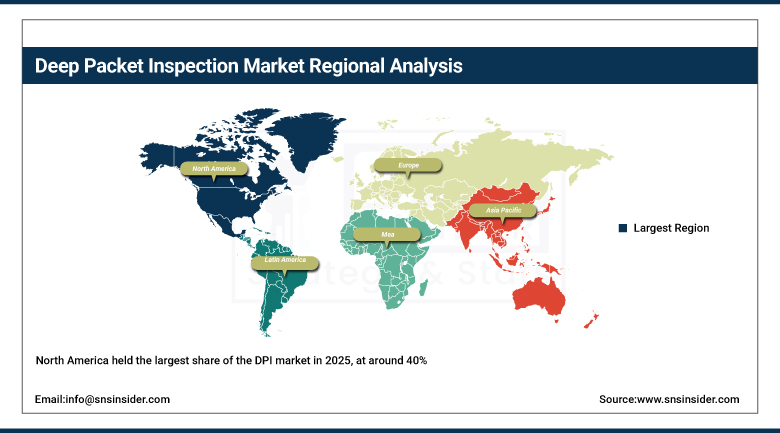

North America held the largest share of the DPI market in 2025, at around 40%, thanks to advanced digital infrastructure, early adoption of cybersecurity technology, and a heavy concentration of leading DPI vendors headquartered in the region. Strict regulatory requirements in sectors like finance, healthcare, and government mean deep visibility into data flows isn't optional here the way it might be elsewhere.

The sheer sophistication of cyber threats targeting the region keeps demand high for DPI solutions that can deliver real-time protection and help enforce compliance simultaneously. The United States drives the overwhelming majority of regional revenue, with vendors including Cisco, Palo Alto Networks, and Juniper Networks maintaining deep domestic roots, while Canada contributes a smaller, steadier share through its own financial and government sector investment.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Deep Packet Inspection Market Insights

Asia Pacific is the fastest-growing regional DPI market, with a projected CAGR of around 27.87% through 2035, propelled by rapid digitalization, rising internet penetration, and expanding mobile connectivity across the region. Governments and enterprises in emerging economies are pouring investment into network security infrastructure to support cloud adoption and protect data as more of everyday life moves online.

Regulatory shifts and national cybersecurity initiatives across countries like China and India are adding further fuel, particularly as these markets look for DPI solutions that can handle content monitoring, traffic management, and threat detection all at once in fast-growing, high-volume network environments. That combination of scale and urgency is exactly why this region keeps outpacing every other market in growth rate.

Europe Deep Packet Inspection Market Insights

Europe remains a technically sophisticated but more cautious DPI market, shaped heavily by GDPR and other strict data protection rules that limit how deeply organizations can inspect network traffic without running into legal trouble. Germany leads regional demand, supported by a strong industrial base and financial sector that still needs robust network security despite the regulatory complexity.

The UK, France, and the Netherlands round out demand, and European vendors have generally had to build DPI solutions with privacy compliance baked in from the start rather than bolted on afterward. That regulatory pressure has, if anything, pushed European DPI providers toward more privacy-conscious designs that are increasingly valued in other markets too as global privacy expectations rise.

MEA & Latin America Deep Packet Inspection Market Insights

The Middle East and Africa are an increasingly active DPI market, led by the UAE's investment in national cybersecurity infrastructure and network monitoring capabilities tied to its broader digital economy ambitions. Saudi Arabia is following a similar path, with government and telecom investment in network security tied to its Vision 2030 agenda, while South Africa anchors demand across the rest of the continent.

Latin America is seeing steady growth led by Brazil, where telecom operators and financial institutions are investing in DPI to manage rising data volumes and protect against a growing volume of cyber threats. Mexico follows as the region's second-largest market, with demand concentrated mostly among telecom providers and larger enterprises rather than yet reaching deep into the SME segment.

Market Dynamics

Growth Drivers: Escalating cyber threats keep pushing organizations toward deeper visibility

The rising volume and sophistication of cyberattacks is really the core driver behind this market. Organizations are facing everything from malware and ransomware to increasingly targeted data breaches, and DPI has become essential for spotting malicious activity hidden inside network traffic that simpler filtering tools would let straight through. Because DPI analyzes data at such a granular level, it can catch vulnerabilities and looming breaches in real time, which matters enormously in sectors handling sensitive information like healthcare, finance, and government.

As digital infrastructure keeps expanding and businesses lean harder on it every year, the case for DPI as a core piece of any serious cybersecurity strategy keeps getting stronger. Growing expectations around customized, personalized digital services only add more network complexity to secure, and that expanding threat landscape is what keeps DPI adoption climbing steadily across nearly every industry this report covers.

Restraints: Privacy law and public unease still slow DPI adoption in a lot of places

Legal and privacy concerns are a genuinely significant barrier to DPI adoption in a lot of markets. Inspecting the actual contents of data packets raises real privacy questions, especially when personal or sensitive information is involved, and regions with strict data protection rules, GDPR in the EU being the obvious example, can meaningfully limit how DPI tools get used or demand strict compliance before deployment.

Organizations have to navigate these regulatory regimes carefully to avoid legal exposure, and public wariness about surveillance doesn't help either, since a lot of people understandably view deep traffic inspection as an intrusion into their personal communications. That combination of legal complexity and public skepticism makes it genuinely harder for organizations to roll out DPI without running into pushback somewhere along the way.

Opportunities: AI is turning DPI into something closer to a predictive security tool

Pairing DPI with machine learning and AI opens up real opportunities for better performance and smarter security monitoring. These technologies let DPI systems spot anomalies automatically, anticipate likely threats before they materialize, and surface patterns in network traffic that would be nearly impossible to catch through manual review, taking a lot of routine burden off network administrators in the process.

AI-enhanced DPI can also fine-tune network performance in real time rather than just flagging problems after the fact, which raises its value considerably for organizations trying to protect critical infrastructure while keeping operations running smoothly. As AI and machine learning keep advancing, the ceiling for what DPI can do alongside these technologies keeps rising too, which is a genuinely exciting growth avenue for vendors positioned to capitalize on it.

Recent Developments:

-

2024: In February 2024, ipoque showcased its next-generation Deep Packet Inspection and Encrypted Traffic Intelligence solutions at MWC Barcelona, using machine learning and deep learning to improve application classification and reduce network blind spots.

-

2024: In October 2024, Juniper Networks introduced its Secure AI-Native Edge solution, integrating AI-driven networking and security under a unified cloud platform to strengthen threat detection and policy enforcement across enterprise environments.

-

2025: In late February 2025, NETSCOUT enhanced its Arbor Threat Mitigation System with additional AI and machine learning functionality built on deep packet inspection, aimed at better detecting and blocking malicious traffic amid rising DDoS attack volumes.

Deep Packet Inspection Market Key Players

-

Cisco Systems, Inc.

-

ipoque GmbH

-

ENEA

-

NexNet Solutions

-

Palo Alto Networks, Inc.

-

Zoho Corporation Pvt. Ltd.

-

Sandvine

-

Juniper Networks, Inc.

-

VIAVI Solutions Inc.

-

NETSCOUT

-

Fortinet, Inc.

-

Check Point Software Technologies Ltd.

-

F5, Inc.

-

SolarWinds Worldwide, LLC

-

A10 Networks, Inc.

-

Broadcom Inc.

-

Huawei Technologies Co., Ltd.

-

Allot Ltd.

-

Corigine (Netronome)

-

Rohde & Schwarz Cybersecurity

Deep Packet Inspection Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 39.81 Billion |

| Market Size by 2035 | USD 382.49 Billion |

| CAGR | CAGR of 25.39% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Component (Solution, Services) • by Installation (Integrated, Standalone) • by Enterprise Size (Small and Medium Size Enterprises, Large Size Enterprises) • by Application (Network Security, Network Management, Network & Subscriber Analysis, Content Regulation, Others) • by End-use (BFSI, Government, Healthcare, IT & Telecom, Manufacturing, Retail, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Cisco Systems, Inc., ipoque GmbH, ENEA, NexNet Solutions, Palo Alto Networks, Inc., Zoho Corporation Pvt. Ltd., Sandvine, Juniper Networks, Inc., VIAVI Solutions Inc., NETSCOUT, Fortinet, Inc., Check Point Software Technologies Ltd., F5, Inc., SolarWinds Worldwide, LLC, A10 Networks, Inc., Broadcom Inc., Huawei Technologies Co., Ltd., Allot Ltd., Corigine (Netronome), Rohde & Schwarz Cybersecurity |

Frequently Asked Questions

North America dominated the Deep Packet Inspection Market in 2025 with approximately 40% market share, while Asia Pacific is the fastest-growing region.

Solutions dominated with approximately 71% share in 2025, while Services is the fastest growing segment with a CAGR of approximately 26.63%.

The Deep Packet Inspection Market was valued at USD 39.81 Billion in 2025.

Escalating cybersecurity threats and rising network traffic volumes from IoT and 5G, both of which demand deeper, more granular network visibility.

Get in Touch