Degenerative Disc Disease Treatment Market Report Scope & Overview:

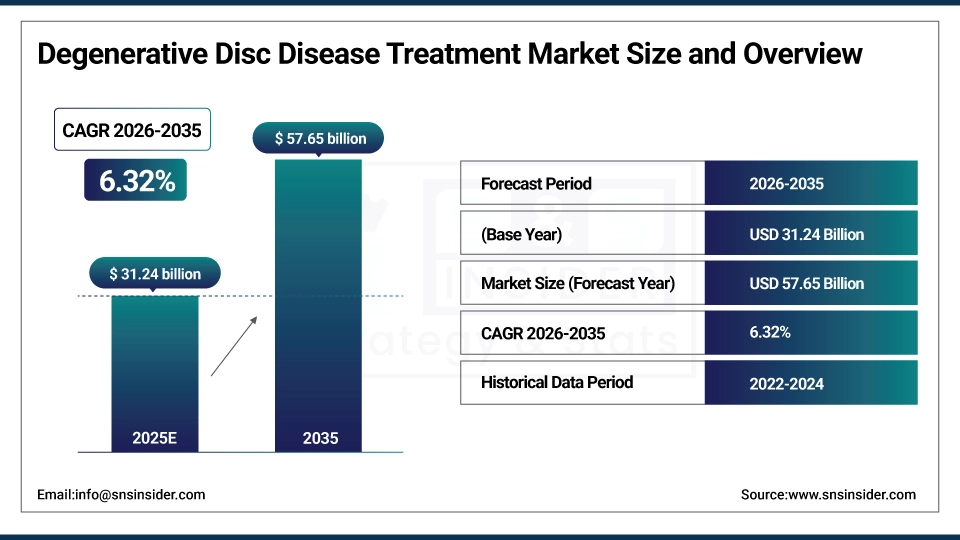

The Degenerative Disc Disease Treatment Market was valued at USD 31.24 billion in 2025 and is expected to reach USD 57.65 billion by 2035, growing at a CAGR of 6.32% from 2026-2035.

The degenerative disc disease treatment market report highlights the impact of the key trends, on the development of the modern industry, providing important insights into the trends that are shaping the market. It reviews prevalence and incidence data, underscoring the rising burden of degenerative disc disease among various populations. The research examines the adoption of different treatments, both surgical strategies and non-surgical strategies, along with trends in reimbursement and healthcare expenditures. It also evaluates the outcomes in regenerative medicine, biologics, and minimally invasive procedures that are spearheading innovation in the market. The report also explores regulatory updates, clinical developments, and R&D spending affecting the landscape of available treatments. Share of market with respect to drugs, therapeutics and surgical interventions are evaluated for all types of possibe growth avenues. Finally, it examines regional trends as well as competitive dynamics and forecasts, and outline the trends for the stakeholders.

Market Size and Forecast:

-

Market Size in 2025: USD 31.24 Billion

-

Market Size by 2035: USD 57.65 Billion

-

CAGR: 6.32% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information on Degenerative Disc Disease Treatment Market - Request Sample Report

Degenerative Disc Disease Treatment Market Trends

-

Increase in incidence and prevalence of spinal disorders and rapid growth of global geriatric population are some factors responsible for driving the market growth of degenerative disc disease treatment market.

-

This factor is contributing positively towards market growth in favorite of minimally invasive surgical procedures including spinal fusion and disc replacement.

-

Greater utilization of biologics, regenerative therapies and pain management solutions are improving patient outcomes.

-

Expanded orthopedic and neurosurgery center offerings increasing accessibility to treatment.

-

Implementation of new imaging and navigation technologies is facilitating accurate diagnosis and therapy.

-

Trends include increasing recognition of non-operative therapies (i.e. Physical therapy & Pharmacotherapeutic management).

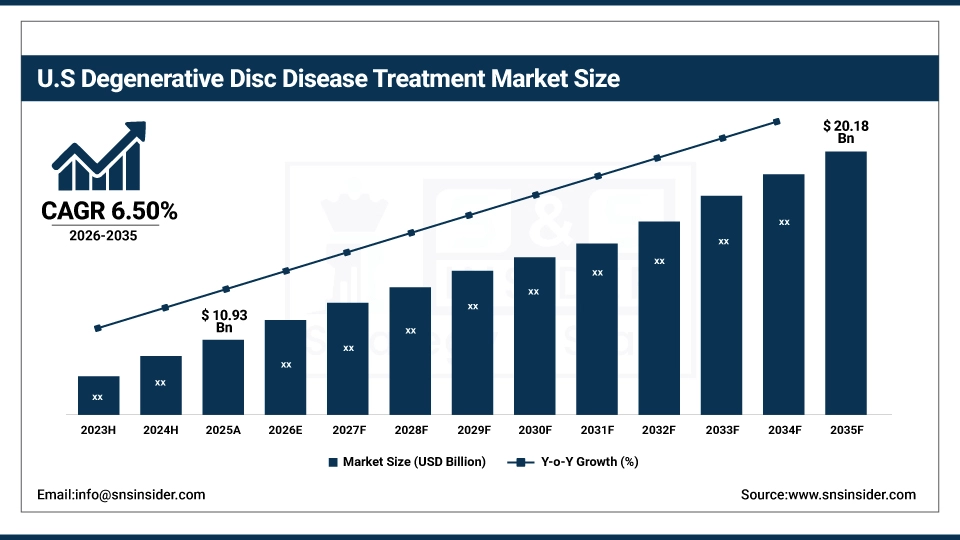

The U.S. Degenerative Disc Disease Treatment Market was valued at approximately USD 10.93 billion in 2025 and is expected to reach around USD 20.18 billion by 2035, growing at a CAGR of 6.50% from 2026–2035. Market growth is driven by the rising aging population, increasing prevalence of spinal disorders, growing demand for minimally invasive surgical procedures, advancements in regenerative therapies and spinal implants, and higher healthcare spending supporting early diagnosis and improved treatment accessibility.

Degenerative Disc Disease Treatment

Degenerative Disc Disease Treatment Market Growth Drivers:

- The rising geriatric population and increasing cases of chronic back pain drive the degenerative disc disease treatment market.

With rapid growth of old age population and rapid increasing number of cases with spinal degeneration and degenerative disc disease, receiver population for DDD treatment is also increasing. The surge in numbers globally of the age group either requiring or receiving effective treatment will be needed as well, as the United Nations estimates the world population aged 65 and over is expected to more than double by 2050, according to the statement. Moreover, the increasing cases of obesity and sedentary lifestyle population have increased the cases of early onset DDD cases thus increasing the market. Improved outcomes, led by different minimally invasive, regenerative, and biologic-based procedures, have resulted in wider use. In addition, the increasing government support for research funding and favorable reimbursement policies in developed economies also boost the market growth. Growing awareness and an increase in early diagnosis of DDD is also leading to an increase in demand for long-term and innovative treatment solutions.

Degenerative Disc Disease Treatment Market Restraints:

- High treatment costs and limited accessibility to advanced therapies restrain market growth.

Highly-priced degenerative disc disease treatments are a major restraint on the market as they reduce accessibility to the drugs, and this factor is expected to impact the growth of the market in low- and middle-income countries. These surgeries (minimally invasive spinal surgeries, artificial disc replacements, and regenerative therapies) are expensive, and as such cannot be afforded by a large patient population. As per anecdotal evidence, spinal fusion surgery costs between USD 50,000–150,000, and this exorbitant price often leaves many without the remedy they need. Patients' affordability is also restricted by the insufficient level of lump sum and/or reimbursement for innovative therapies provided by health insurers. In addition, the medical sector faces problems arising from uneven distribution of healthcare infrastructure, and with many rural areas unable to deliver the required facilities and expertise for specialized treatments. These limitations hinder the deployment of novel treatment modalities, impeding market growth despite the evolution of the medical device technology.

Degenerative Disc Disease Treatment Market Opportunities:

- Growing investment in regenerative medicine and stem cell therapy creates lucrative market opportunities.

Grow the regenerative medicine and stem cell therapy could trip the promising potential growth opportunity for DDD Treatment Market. The science of biologics has opened up new possibilities for researchers and biotechnology companies focusing on treatments such as stem cell injections and tissue engineering to repair damage to a disc and restore its function. As the National Institutes of Health (NIH) reports, regenerative medicine is an area where funding has grown rapidly in recent years and it is spurring some of the fastest innovating options for non-invasive treatment. Finally, clinical trials are in progress for growth factors, PRP, and gene therapy that may lead to a paradigm shift. These innovations are gaining wider acceptance among patients and treatment setting and regulatory approvals will continue to spur the market with less invasive and sustainable treatment options offered to patients.

Degenerative Disc Disease Treatment Market Segment Analysis

By End-User Industry, Hospitals lead the market share in Market

Hospitals segment leads the market share with 32%, as hospitals are the major treatment centers for DDD procedures. The presence of significant number of chronic back pain patients undergoing hospitalization and the development of the surgical infrastructure with high capabilities are some of the key market drivers helping the market grow. A slew of companies from Stryker to DePuy Synthes have rolled out cutting-edge robotic-assisted surgery systems for hospitals that improve procedural accuracy. Stryker Q Guidance System for navigation-assisted spine surgeries for launched in 2024 per. In addition, with increase in number of specialty spine centers in the hospitals, as well as the various investments done in the minimally invasive surgical procedures, accordingly the clinic have dominated the hospitals in DDD treatment market.

By Product Type, Devices dominate the Degenerative Disc Disease (DDD) Treatment Market.

In 2025, the device segment accounted for the largest share of 62.00% in revenue of the Degenerative Disc Disease (DDD) Treatment Market aided by the high adoption of spinal implants, artificial discs, and minimally invasive surgical devices. There were significant new uncemented spine fusion devices, artificial disc replacement systems by key players including Medtronic & Zimmer Biomet, that have favorably impacted the clinical course of many patients. In the second half of 2024, a few advances in spinal devices like Medtronic's Catalyft PL spinal system and NuVasive's Modulus ALIF implant with better stability and flexibility were included. The growth of the segment is also driven by an aging population, escalating adoption rates for minimally-invasive procedures and the evolution of robotic-assisted spinal surgeries as viable long-term, effective solutions for patients with DDD.

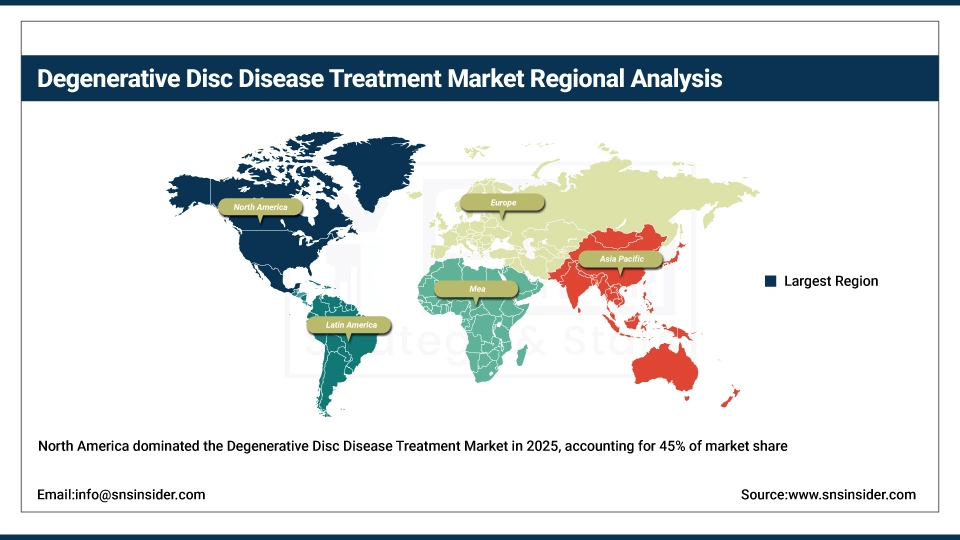

Degenerative Disc Disease Treatment Market Regional Analysis

North America Degenerative Disc Disease Treatment Market Insights

In 2025, North America dominated the Degenerative Disc Disease (DDD) Treatment Market, accounting for an estimated 45% market share. High health expenditure, developed medical infrastructure, and the presence of key market players are driving this dominance. In addition to this, an increasing geriatric population as well as the rising prevalence of spinal disorders will contribute to the market growth. According to the CDC, around 39% of U.S. adults have chronic back pain which has led to a greater need for minimally invasive spine surgeries. Regional presence have been reinforced by product developments from companies such as MedtronicEmploying, which most lately released its Catalyft Expandable Interbody System in 2023, and Stryker Employing. Also, the positive reimbursement policies in the U.S. and Canada promote patient acceptance of innovation DDD therapies, bolstering the North America position of such markets.

Do You Need any Customization Research on Degenerative Disc Disease Treatment Market - Enquire Now

Asia Pacific Degenerative Disc Disease Treatment Market Insights

Asia Pacific in 2024 is estimated to be the fastest-growing degenerate disc disease (DDD) treatment market, at a highest CAGR. Some of the key factors driving the growth include rising geriatric population, rising healthcare costs and availability of advanced spinal cord treatments. The UN in a news release adds that degenerative spinal disorders will be even more prevalent in the region, with Asia's ageing population double by 2050 from 2019. At this current time,China and India are also growing faster due to these government initiatives regarding better healthcare and efficient medical tourism. For example, China in its policy of "Healthy China 2030" urges us to advance new spinal interventions and regenerative medicine. Moreover, regional commercial launches of products such as Medtronic's Prestige LP Cervical Disc System is entering regional market space fuelling market growth across Asia Pacific for Zimmer Biomet and Medtronic.

Europe Degenerative Disc Disease Treatment Market Insights

Degenerative Disc Disease Treatment also shares the largest market in the Developed regions, where Europe is a dominant place due to the factors like spinal disorder prevalence in the region, aging population, and growth in the healthcare expenditure. Growth of the market is due to advanced surgical procedures, minimally invasive techniques and newly developed spinal implants. Presence of major players and ongoing clinical trials and initiatives from the governments to promote awareness regarding spinal health will boost up the market growth, and hence Europe as a region will contribute significantly to global growth.

Middle East & Africa and Latin America Degenerative Disc Disease Treatment Market Insights

Middle East & Africa and Latin America Degenerative Disc Disease Treatment Market is expanding at a steady rate due to rising hospital infrastructure investments and increasing awareness about spinal disorders. Market growth is attributed to factors such as growing adoption of complex surgical techniques, minimally invasive approaches, and new implantable spinal devices. The demand for Medical Device Packaging Market is also accentuated by government initiatives, improving healthcare access and increasing medical tourism putting both the regions on the market for growth potential map.

Degenerative Disc Disease Treatment Market Competitive Landscape:

Johnson & Johnson

Johnson & Johnson, founded in 1886, is a a globalization leader, has for years developed medical devices like orthopedics and surgery, prescription pharmaceuticals, and consumer health products. The company develops innovative solutions designed to improve patient outcomes across a range of conditions. Boasting substantial orthopedic research capabilities, spine research and care systems, and medical technology development that enhance the quality, durability and function of human life in the orthopedic sphere, Johnson & Johnson is well established as a leader in healthcare device innovation.

-

April 2024: Johnson & Johnson launched advanced artificial discs designed to enhance durability and improve patient outcomes for individuals suffering from degenerative disc disease (DDD).

DiscGenics Inc.

DiscGenics Inc., founded in 2008, DiscGenics, Inc. is a regenerative medicine company that develops therapies to treat spinal disorders. The company is developing cell-based therapeutics to restore and regenerate damaged intervertebral discs, focusing on conditions such as degenerative disc disease (DDD). DiscGenics is focused on using its proprietary allogeneic progenitor cell technology, to provide minimally invasive regenerative treatments for discs that improve disc function and reduce pain and disability in order to enable a new standard of care for spinal regenerative therapies.

-

January 2023: DiscGenics Inc. secured the U.S. FDA's Regenerative Medicine Advanced Therapy (RMAT) designation for its Injectable Disc Cell Therapy (IDCT), an allogeneic progenitor cell treatment designed to address symptomatic lumbar degenerative disc disease (DDD).

Companion Spine LLC

Companion Spine LLC, founded in 2007, designs and develops new spinal implants and surgical solutions. Focused on improving patient outcomes in spinal health through innovative technologies that address stability, mobility, and long-term recovery, the company creates solutions to restore mobility and promote healing Companion Spine brings together state-of-the-art tech and clinical acumen, striving to make more treatments available to more patients with degenerative spine conditions and empowering surgeons and patients alike with effective, safe and patient-focused solutions.

-

January 2023: Companion Spine LLC acquired Backbone SAS, expanding its portfolio with the LISA implant, a device aimed at enhancing lumbar stiffness augmentation for degenerative disc disease (DDD) patients.

Degenerative Disc Disease Treatment Market Key Players:

-

DiscGenics Inc.

-

Spine BioPharma Inc.

-

Johnson & Johnson Services, Inc.

-

Zimmer Biomet

-

B. Braun SE

-

RTI Surgical

-

Cousin Biotech

-

Ulrich Medical USA

-

Fresenius Kabi AG

-

Abbott

-

Spine Wave, Inc.

-

RIVANNA MEDICAL

-

ZAVATION

-

Orthofix US LLC.

-

Spinal Simplicity

-

Nexus Spine

-

NuVasive, Inc.

-

Aurora Spine, Inc.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 31.24 Billion |

| Market Size by 2035 | USD 57.65 Billion |

| CAGR | CAGR of 6.32% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Drugs, Devices) • By End User Industry (Hospitals, Ambulatory Surgical Centers, Orthopedic Centers, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | DiscGenics Inc., Medtronic, Spine BioPharma Inc., Globus Medical, Johnson & Johnson Services, Inc., Zimmer Biomet, B. Braun SE, RTI Surgical, Cousin Biotech, ulrich medical USA, Fresenius Kabi AG, Abbott, Spine Wave, Inc., RIVANNA MEDICAL, ZAVATION, Orthofix US LLC., Spinal Simplicity, Nexus Spine, NuVasive, Inc., Aurora Spine, Inc. |

Frequently Asked Questions

North America led the market in 2025 with approximately 45% share, owing to advanced healthcare infrastructure, high treatment adoption, and technological innovations.

The devices segment dominated the market, accounting for the largest share due to widespread use of implants, spinal fusion systems, and disc replacement technologies.

Increasing geriatric population, rising chronic back pain cases, and adoption of minimally invasive surgeries are key factors driving market growth.

The market was valued at USD 31.24 billion in 2025, driven by rising prevalence of spinal disorders and increasing demand for effective treatments.

The market is projected to grow at a CAGR of 6.32% from 2026 to 2035, reflecting steady expansion in treatment adoption and technological advancements.

Get in Touch