Dialysis Equipment Market Report Scope & Overview:

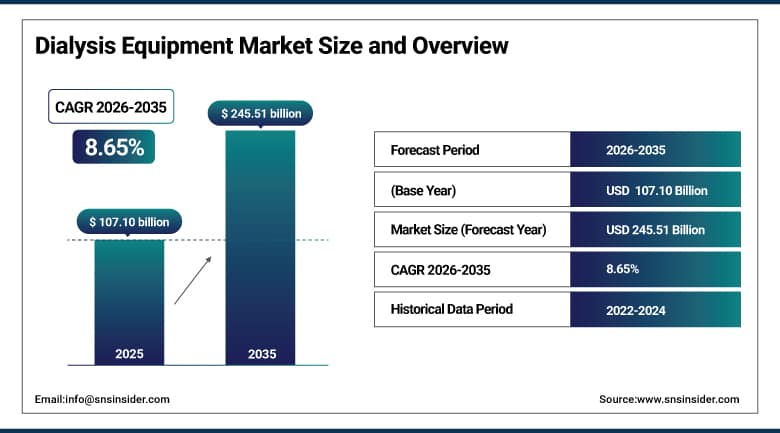

The Dialysis Equipment Market size was valued at USD 107.10 billion in 2025 and is expected to reach USD 245.51 billion by 2035, growing at a CAGR of 8.65% over the forecast period of 2026–2035.

The global dialysis equipment market is being driven by the rising cases of end-stage renal disease (ESRD) and chronic kidney disease (CKD), the rising number of diabetic patients, the rising number of hypertensive patients, and the rising demand for both hemodialysis and peritoneal dialysis. At the same time, the rising investments in the healthcare infrastructure of developing countries, the presence of a supportive reimbursement environment in developed countries, and the rising elderly population are boosting the global demand for advanced dialysis equipment.

For instance, according to the International Society of Nephrology (ISN), as of 2024, over 3.5 million patients worldwide receive regular dialysis therapy, and this number is projected to surpass 5.4 million by 2030, directly fueling demand for hemodialysis machines, dialyzers, peritoneal dialysis cyclers, and related consumables.

Dialysis Equipment Market Size and Forecast:

-

Market Size in 2025: USD 107.10 billion

-

Market Size by 2035: USD 245.51 billion

-

CAGR: 8.65% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get More Information On Dialysis Equipment Market - Request Free Sample Report

Dialysis Equipment Market Trends:

-

Rising global ESRD and CKD patient burden is driving persistent demand for hemodialysis machines, high-flux dialyzers, and peritoneal dialysis cyclers across both hospital and home settings.

-

Proliferation of home hemodialysis (HHD) and automated peritoneal dialysis (APD) programs supported by portable, user-friendly device platforms and expanding patient training infrastructure.

-

Integration of IoT-enabled smart dialysis machines, AI-assisted session monitoring, and real-time fluid management analytics to improve treatment adequacy and reduce adverse events.

-

Growing preference for single-use, high-biocompatibility dialyzers and low-volume dialysate systems to minimize infection risk and optimize patient outcomes in clinical settings.

-

Expansion of dialysis center networks in Asia-Pacific, Latin America, and the Middle East driven by public-private partnerships, national kidney care programs, and rising healthcare expenditure.

-

Strategic collaborations between equipment manufacturers, nephrologists, and payer organizations to develop cost-effective, value-based dialysis care delivery models globally.

-

Increasing regulatory scrutiny from the FDA, CE, and national health authorities on device biocompatibility, water quality standards, and software-enabled dialysis system safety.

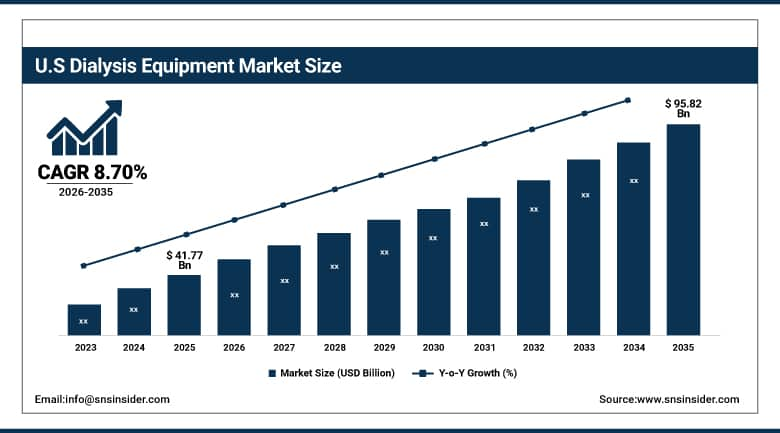

The U.S. Dialysis Equipment Market is estimated at USD 41.77 billion in 2025 and is expected to reach USD 95.82 billion by 2035, growing at a CAGR of 8.70% from 2026–2035. The United States is considered to be the largest single-country market for dialysis equipment, driven by a high ESRD prevalence rate of 2,500 per million population, Medicare ESRD program reimbursements for over 90% of ESRD patients, and high investments in the expansion of home dialysis. The Kidney Care Choices (KCC) model and ESRD Treatment Choices (ETC) mandate of the Centers for Medicare & Medicaid Services are encouraging the use of home-based hemodialysis and peritoneal dialysis, thereby increasing the use of connected equipment platforms.

Dialysis Equipment Market Growth Drivers:

-

Rising Global Burden of Chronic Kidney Disease and ESRD is Driving the Dialysis Equipment Market Growth

The rise in the incidence of CKD, which now affects 850 million worldwide as of 2024 according to the International Society of Nephrology, is the key market growth driver for dialysis equipment. With diabetes and hypertension being the two most common causes of ESRD, and these two factors responsible for more than 537 million and 1.3 billion adults worldwide, respectively, the pipeline of patients waiting for some form of RRT is only going to continue its rise. This is directly contributing to increased capital spending on hemodialysis equipment, dialyzers, and peritoneal dialysis consumables in healthcare systems worldwide.

For instance, in May 2024, the U.S. Renal Data System (USRDS) reported that ESRD incidence in the United States grew by 4.2% year-over-year in 2023, driving a corresponding 6.8% increase in dialysis equipment procurement across dialysis center networks nationwide.

Dialysis Equipment Market Restraints:

-

High Equipment Costs and Reimbursement Limitations are Hampering the Dialysis Equipment Market Growth

Higher capital costs of advanced hemodialysis equipment, smart peritoneal dialysis cyclers, and ultra-pure water treatment solutions are a major challenge for market acceptance, especially in low- and middle-income countries where health expenditure is limited. Furthermore, lack of clear reimbursement policies in emerging markets, limited insurance coverage for home dialysis supplies, and budgetary constraints in public health infrastructure in high-burden developing markets such as Sub-Saharan Africa and Southeast Asia are acting as market acceptance barriers, thereby affecting the overall market potential for these devices.

Dialysis Equipment Market Opportunities:

-

Home Dialysis Expansion and Wearable Dialysis Technology Create High-Value Growth Opportunities for the Dialysis Equipment Market

The overall shift towards more patient-centric and home-based kidney care represents a revolutionary growth opportunity for the dialysis equipment market, with more investment in the development of wearable artificial kidneys, miniaturized hemodialysis systems, and automated peritoneal dialysis systems. In addition, government initiatives on home dialysis incentives in the U.S., U.K., Australia, and Canada are providing growth opportunities for the dialysis equipment market. Furthermore, incorporation of machine learning algorithms for optimization of dialysis prescriptions and remote monitoring by a nephrologist is expected to improve patient outcomes and drive growth of advanced home-based dialysis systems.

For instance, in January 2025, the CMS reported that the percentage of new ESRD patients initiating home dialysis in the U.S. increased to 17.3%, up from 12.8% in 2020, validating the substantial and growing commercial opportunity for home hemodialysis and peritoneal dialysis equipment manufacturers.

Dialysis Equipment Market Segment Analysis

-

By type, hemodialysis equipment held the largest share of approximately 68.42% in 2025, while peritoneal dialysis equipment is expected to register the highest growth with a CAGR of 9.82%.

-

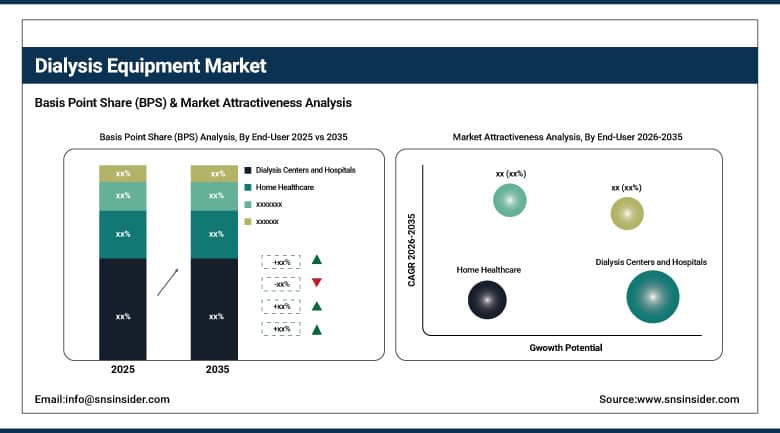

By end user, dialysis centers and hospitals dominated the market with around 71.63% share in 2025, while home healthcare is expected to register the highest growth with a CAGR of 10.14%.

By End User, Dialysis Centers and Hospitals Lead, While Home Healthcare Registers Fastest Growth

Based on end-uses, the dialysis centers and hospitals collectively accounted for the substantial share of 71.63% in 2025, due to the centralized nature of treatment provided and high patient throughputs, standardization of treatment protocols and capital investment capabilities for premium dialysis solutions in such setting. Finally, the concentration of ESRD patients in outpatient dialysis centers and the nephrology departments of acute care hospitals supports stable demand for dialysis devices and supplies. Nonetheless, during the 2026-2035 time frame, the home healthcare market category is anticipated to record the highest CAGR of 10.14%,directly stimulated by favourable CMS reforms for home dialysis cost coverage, the rising patient demand for home-based treatments that have the potential to ameliorate their quality of life, increasing patient/clinician training programs for home dialysis, as well as the solution availability of portable and easy-to-use home-based hemodialysis and peritoneal dialysis alternatives.

By Type, Hemodialysis Equipment Leads the Market, While Peritoneal Dialysis Equipment Registers Fastest Growth

Hemodialysis equipment has the highest revenue share of approximately 68.42% in 2025 due to the global acceptance of the standard approach of in-center HD for the treatment of patients with ESRD, the large quantity of dialyzers used during the process, and the general acceptance of the approach by healthcare providers due to the well-established vascular access-based treatment approach. On the other hand, the peritoneal dialysis equipment segment is expected to have the highest CAGR of 9.82% from 2026 to 2035 due to the increased acceptance of automated peritoneal dialysis cyclers globally, the government's initiatives to increase home dialysis among patients with ESRD, and the benefits of the CAPD approach for patients with ESRD, especially the pediatric and elderly populations.

Dialysis Equipment Market Regional Highlights:

North America Dialysis Equipment Market Insights:

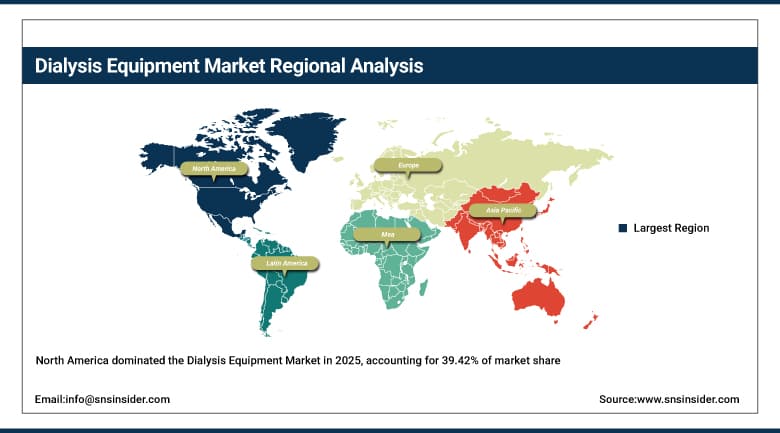

North America dominated the ESRD treatment market in terms of revenue share, i.e., 39.42% in 2025, driven by a mature ESRD environment in the United States, which has access to more than 7,500 outpatient dialysis facilities, a robust Medicare ESRD program for more than 750,000 patients, and a high acceptance of technologically advanced dialysis equipment. Federal policy initiatives such as the Advancing American Kidney Health (AAKH) Executive Order are continuing to change the ESRD treatment landscape by moving towards home-based ESRD treatment, thereby creating a long-term growth opportunity for portable ESRD equipment and monitoring systems. In addition, Canada is expanding its dialysis treatment infrastructure and has launched various home dialysis programs in different provinces.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Asia Pacific Dialysis Equipment Market Insights:

Asia Pacific is also the fastest-growing dialysis equipment regional segment, which is expanding at a CAGR of 10.42%. This is owing to the exceptionally high incidence of CKD in countries such as China, India, Japan, and Southeast Asia, along with rapidly expanding dialysis center infrastructure and government investment in renal programs. In fact, China alone contributes more than 25% of the global dialysis patients, and India has an incidence of ESRD of 230,000 fresh patients every year. Increasing healthcare expenditure per capita and better health insurance coverage, along with expanding dialysis equipment manufacturers in the region, are also strengthening the competitive landscape of Asia Pacific.

Europe Dialysis Equipment Market Insights:

The second largest regional market for Europe is served by universal health coverage in all major European economies, high quality device assurance through CE mark regulations, and high investments in national kidney care strategies in Germany, France, Italy, the U.K., and Spain. Europe is served by strong clinical research infrastructure for the uptake of high-flux dialyzers and online hemodiafiltration technology. Connected dialysis solutions compliant with GDPR regulations and cross-border health directives make it easier for the integrated delivery of renal care and device standardization in Europe.

Latin America (LATAM) and Middle East & Africa (MEA) Dialysis Equipment Market Insights:

In Latin America, Brazil and Mexico are identified as major markets that are expanding public dialysis center networks and private nephrology clinic investments to meet a growing need for dialysis services to treat a rapidly expanding ESRD patient population. In the Middle East & Africa, the UAE and Saudi Arabia are heavily investing in dialysis infrastructure upgrades as part of a larger Vision 2030 health system transformation plans in these countries. Improvements in mobile health connectivity are also supporting growth in home dialysis services. The growth in diabetes and hypertension comorbidities in both regions provides a structural growth story in dialysis equipment.

Dialysis Equipment Market Competitive Landscape:

Fresenius Medical Care AG & Co. KGaA (founded 1996) is the global market leader in the field of dialysis products and services, owning the largest number of dialysis clinics across the globe and providing a wide range of products like hemodialysis machines, high-flux dialyzers, and peritoneal dialysis products.

-

In January 2025, Fresenius Medical Care launched the 6008 CAREsystem hemodialysis platform with integrated AI-assisted fluid management and remote monitoring capabilities across its European and North American clinic networks, targeting improved clinical outcomes and operational efficiency.

Baxter International Inc. is a well-established company (incorporated 1931) specializing in the manufacture of peritoneal dialysis solutions, APD cyclers, and hemodialysis products. Its key area of expertise is home dialysis therapy equipment under the brand names of HOMECHOICE and AMIA APD system. Its strategic approach to renal care innovation and home therapy products portfolio is an added advantage for the company.

-

In September 2024, Baxter introduced the AMIA APD System with CloudConnect upgrades, enabling real-time therapy data transmission and remote patient monitoring for home peritoneal dialysis patients across the United States, Canada, and select European markets.

Nipro Corporation is a well-known Japanese dialysis equipment and consumable manufacturer, including high-performance dialyzers, bloodlines, and hemodialysis machines, with a strong commercial footprint in Asia Pacific, Europe, and emerging markets. Nipro's competitive advantage is its cost-efficient and high-volume manufacturing capabilities and its comprehensive range of disposable consumable products.

-

In March 2025, Nipro Corporation expanded its ELISIO-H high-flux dialyzer production capacity at its Thailand manufacturing facility by 30%, targeting growing demand from dialysis centers across Southeast Asia and the Middle East amid rising ESRD patient volumes.

Dialysis Equipment Market Key Players:

-

Fresenius Medical Care AG & Co. KGaA

-

Baxter International Inc.

-

Nipro Corporation

-

B. Braun Melsungen AG

-

Nikkiso Co., Ltd.

-

Asahi Kasei Medical Co., Ltd.

-

Toray Medical Co., Ltd.

-

Outset Medical, Inc.

-

Rockwell Medical, Inc.

-

Merit Medical Systems, Inc.

-

Teleflex Incorporated

-

Weigao Group (WEGO Medical)

-

Allmed Medical Products Co., Ltd.

-

AngioDynamics, Inc.

-

Mar Cor Purification (Cantel Medical)

-

Guangdong Biolight Meditech Co., Ltd.

-

Medtronic plc

-

Dirinco AG

-

Isopure Corp.

-

Huaren Pharmaceutical Co., Ltd.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 107.10 Billion |

| Market Size by 2035 | USD 245.51 Billion |

| CAGR | CAGR of 8.65% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Hemodialysis Equipment (Hemodialysis Machines, Hemodialysis Consumables, Peritoneal Dialysis Equipment (Peritoneal Dialysis Equipment Type), Peritoneal Dialysis Product (Cyclers, Fluids, Other Accessories)) • By End User (Dialysis Centers and Hospitals, Home Healthcare) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Fresenius Medical Care AG & Co. KGaA, Baxter International Inc., Nipro Corporation, B. Braun Melsungen AG, Nikkiso Co. Ltd., Asahi Kasei Medical Co. Ltd., Toray Medical Co. Ltd., Outset Medical Inc., Rockwell Medical Inc., Merit Medical Systems Inc., Teleflex Incorporated, Weigao Group (WEGO Medical), Allmed Medical Products Co. Ltd., AngioDynamics Inc., Mar Cor Purification (Cantel Medical), Guangdong Biolight Meditech Co. Ltd., Medtronic plc, Dirinco AG, Isopure Corp., Huaren Pharmaceutical Co. Ltd. |

Get in Touch