Drug Discovery Market Report Scope & Overview:

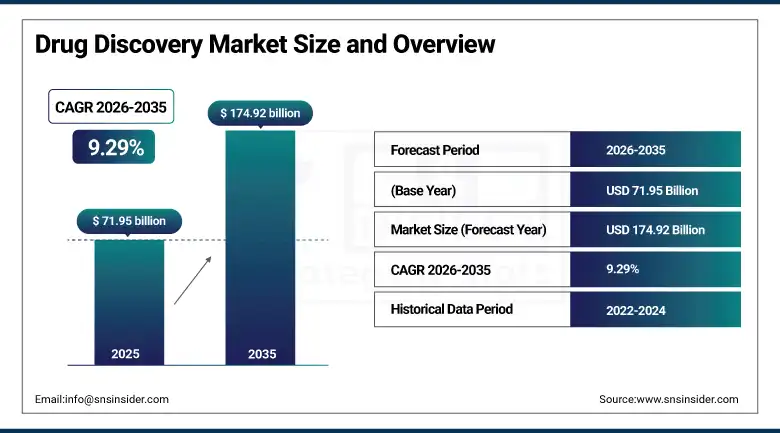

The Drug Discovery Market was estimated at USD 71.95 billion in 2025 and is expected to reach USD 174.92 billion by 2035 and grow at a CAGR of 9.29% over the forecast period of 2026-2035.

The drug discovery sits at the heart of the pharmaceutical and biotechnology industries as the critical research and development process. The process encompasses a sequence of increasingly refined scientific activities beginning with the identification of disease-relevant biological targets progressing through high-throughput screening of chemical and biological libraries. This process is being fundamentally accelerated and made more cost-efficient by the convergence of artificial intelligence-driven molecular property prediction, structural biology advances enabling atomic-resolution drug-target structure visualisation, CRISPR functional genomics screens identifying disease-relevant gene targets. The increasing willingness of large pharmaceutical companies to supplement their internal discovery capabilities through acquisitions, licensing agreements, and collaborative research arrangements is expanding the addressable market for external discovery services and technology providers that serve both sides of these collaborations.

The convergence of AI-driven molecular property prediction with structural biology data from cryogenic electron microscopy, fragment-based drug discovery, and DNA-encoded chemical libraries is compressing the time from target identification to development candidate nomination from the historical multi-year standard toward months, creating competitive pressure on all market participants to adopt next-generation discovery technologies.

Market Size and Forecast

-

Market Size in 2026E: USD 78.63 Billion

-

Market Size by 2035: USD 174.92 Billion

-

Growth Rate (2026–2035): 9.29%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information On Drug Discovery Market - Request Free Sample Report

Drug Discovery Market Trends

-

Accelerating integration of generative AI models into lead optimisation workflows, where large language models trained on chemical structure-activity relationship data are being used to propose novel molecular designs that human medicinal chemists then evaluate and synthesise, compressing the iteration cycle from weeks to days in programmes where experimental throughput permits rapid feedback.

-

Growing adoption of structure-enabled drug discovery facilitated by cryogenic electron microscopy structure determination of drug targets in physiologically relevant conformations, providing the atomic-level binding pocket information that enables rational drug design approaches previously limited by the resolution constraints of earlier structural biology techniques.

-

Rising use of CRISPR functional genomics screens in target identification and validation, enabling systematic interrogation of every gene in the human genome for its contribution to disease-relevant cellular phenotypes and providing target confidence evidence that historically required years of genetic model organism studies.

-

Increasing pharmaceutical outsourcing of drug discovery activities to contract research organisations in India, China, and Central and Eastern Europe where lower labour costs, growing scientific workforce quality, and improving infrastructure are enabling competitive discovery services at a fraction of the cost of equivalent internal programmes.

-

Expanding multi-omics data integration in early discovery programmes, where the combination of genomics, transcriptomics, proteomics, and metabolomics profiling of disease states and drug-treated cellular systems provides a richer biological rationale for target selection than any single data type could supply independently.

The U.S. Drug Discovery Market Outlook

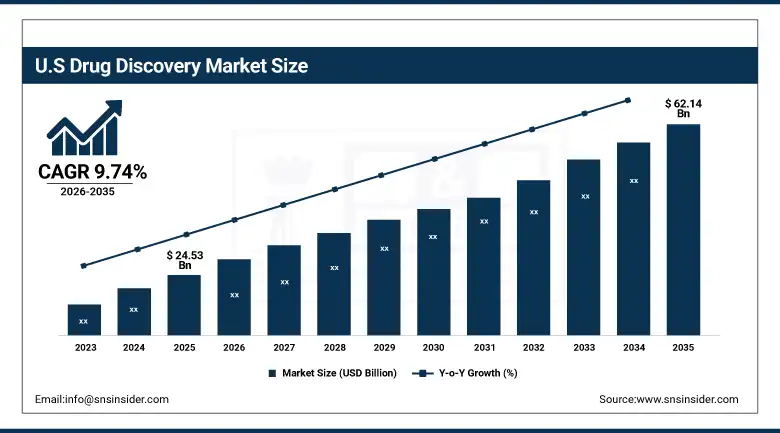

The U.S. Drug Discovery Market was valued at approximately USD 24.53 billion in 2025 and is expected to reach approximately USD 62.14 billion by 2035, growing at a CAGR of 9.74%.

The United States commands the global drug discovery market through its unique combination of academic research institutions generating fundamental biological insights, large pharmaceutical company R&D organisations that provide the clinical development and commercialisation infrastructure that biotechnology depends upon, and a contract research organisation industry that offers deep discovery science capabilities at competitive costs. Over 3,200 active drug discovery programmes were underway in the U.S. in 2025, spanning oncology, rare diseases, neurology, metabolic disease, and infectious disease, with AI-driven target identification and ML-accelerated lead optimisation features. The Inflation Reduction Act's drug pricing negotiation provisions are creating incentive structure changes for pharmaceutical companies' investment priorities between small-molecule and biologic drug discovery.

The National Institutes of Health's allocation of over USD 2 billion to the Advanced Research Projects Agency for Health since its establishment, combined with NIH's sustained investment in basic biomedical research across over 2,500 research-intensive institutions, maintains the fundamental biological knowledge base that commercial drug discovery depends upon and which sustains the United States' competitive advantage in discovery productivity relative to all other national research ecosystems.

Drug Discovery Market Segment Analysis

-

By Process, target identification & validation held the largest share at approximately 33.47% in 2025; candidate validation is the fastest-growing process segment at a CAGR of 10.45%.

-

By Technology, high-throughput screening held the largest share at approximately 41.29% in 2025; bioinformatics is the fastest-growing technology at a CAGR of 11.22%.

-

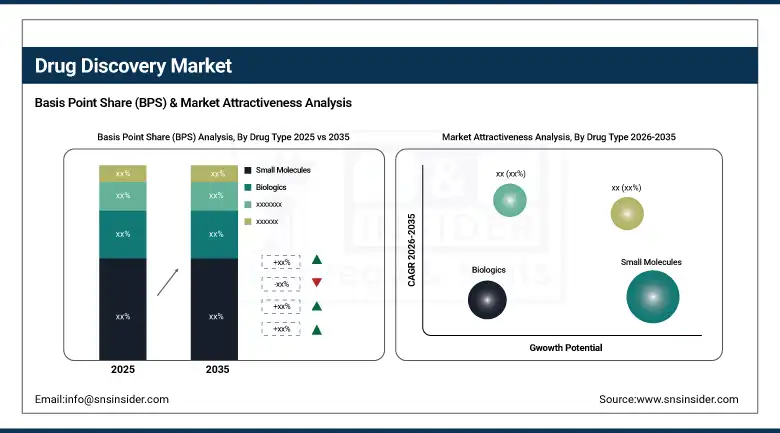

By Drug Type, small molecules dominated with approximately 59.41% of revenues in 2025; biologics are the fastest-growing drug type at a CAGR of 10.88%.

-

By End User, pharmaceutical & biotechnology companies held the largest share at approximately 52.56% in 2025; contract research organisations are the fastest-growing end-user category at a CAGR of 10.13%.

By Process, target identification & validation dominates, candidate validation is expected to grow fastest

Target identification & validation retained the largest process share at approximately 33.47% of drug discovery market revenues in 2025. The growing availability of human genetic association data from genome-wide association studies and exome sequencing cohorts, functional genomics data from CRISPR screens, and disease-relevant human tissue transcriptomics from single-cell RNA sequencing studies is expanding the evidence base for target selection and driving investment in computational target identification platforms that integrate these multiple data types.

Candidate Validation is the most rapidly growing segment within the processes category, showing a CAGR of 10.45% till 2035. The reason for this trend is the understanding of the pharmaceutical industry that the main factor contributing to failures during clinical trials stages in the development process is not the inefficiency or non-selectivity of a compound, but rather its unforeseen toxicity or non-translatability to humans.

By Technology, high-throughput screening dominates, bioinformatics is expected to grow fastest

High-throughput screening dominated the drug discovery market in 2025 with approximately 41.29% share due to its ability to rapidly evaluate millions of compounds against biological targets using automated robotics, miniaturized assays, and advanced analytical platforms. Increasing integration of AI-driven data analysis is further improving hit identification and screening efficiency.

The bioinformatics sector is expected to register the highest CAGR over 2035 owing to rapid advances in genomics, proteomics, sequencing technology, and the utilization of AI for biological data analytics. Cutting-edge computation, protein structure prediction software, and AI algorithms have been greatly enhancing target discovery and structure-based drug development.

By Drug Type, small molecules dominate, biologics are expected to grow fastest

Small molecules dominated the drug discovery market in 2025 with approximately 59.41% revenue share due to their oral bioavailability, cost-effective manufacturing, intracellular target accessibility, and well-established medicinal chemistry development frameworks. Their extensive clinical history and compatibility with AI-driven molecular design continue supporting widespread pharmaceutical discovery investment globally.

Biologics are projected to witness the fastest CAGR through 2035 driven by increasing development of monoclonal antibodies, vaccines, gene therapies, RNA therapeutics, and cell-based treatments. Rising investment in oncology, immunology, and rare disease therapeutics is accelerating biologics discovery and advanced therapeutic platform innovation worldwide.

By End User, pharmaceutical & biotechnology companies dominate, CROs are expected to grow fastest

The pharmaceutical and biotechnology firms dominated the drug discovery market during 2025 with a revenue share of around 52.56% owing to their high investment on research and development, effective development of clinical trials, strong understanding of regulations, and vast drug research activities. They are making huge investments in drug discovery related to oncology, rare diseases, immunology, and precision medicine.

Among these segments, Contract Research Organizations (CROs) are forecasted to have the highest CAGR till 2035, since pharmaceutical companies are outsourcing early stages of drug discovery, screening, bioinformatics, and preclinical studies to specialized organizations. Increased requirement for more efficient research models, technological advancements, and flexibility in discovery processes is fuelling growth in the CRO market.

Regional Insights:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

83% |

|

Europe |

Germany |

30% |

|

Asia Pacific |

China |

45% |

|

Middle East & Africa |

Israel |

22% |

|

Latin America |

Brazil |

38% |

North America Drug Discovery Market Insights

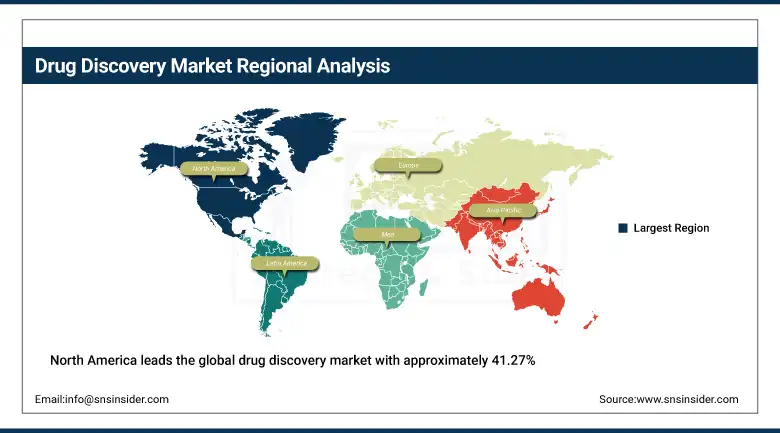

North America leads the global drug discovery market with approximately 41.27% of revenues in 2025, with the United States accounting for approximately 83% of North American revenues. The region's dominance reflects the world's largest concentration of pharmaceutical R&D investment, the most extensive biotechnology venture capital ecosystem financing early-stage discovery companies, the broadest CRO infrastructure spanning from discovery through clinical development, and the NIH research funding base that sustains the fundamental biomedical science on which commercial discovery builds. Over 3,200 active drug discovery programmes were underway in North America in 2025 spanning oncology, rare diseases, neurology, and metabolic conditions, with AI-driven discovery methodologies increasingly standard practice across both large pharmaceutical companies and early-stage biotechnology firms seeking to compress timelines and differentiate their pipeline productivity.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Drug Discovery Market Insights

Europe is a sophisticated and well-established drug discovery market anchored by the large-molecule discovery capabilities of Roche and Novartis in Switzerland, AstraZeneca's discovery centres in the United Kingdom and Sweden, Sanofi's research operations in France, and Bayer and Merck KGaA's programmes in Germany. The European biomedical research ecosystem benefits from substantial public investment through the EU's Horizon Europe research programme, the Innovative Medicines Initiative public-private partnership, and national research council funding across major European research nations. Cambridge, Oxford, London, Basel, Munich, and Stockholm have each developed biotechnology clusters where academic spin-outs and venture-backed discovery companies form a dynamic early-stage discovery ecosystem that supplies licensing opportunities to larger pharmaceutical companies maintaining discovery operations in the same geographies.

Asia Pacific Drug Discovery Market Insights

Asia Pacific is the fastest-growing drug discovery market with a projected CAGR of 9.82% from 2026 to 2035, driven by the rapid expansion of pharmaceutical R&D infrastructure in China and India, the growing regional biotechnology sector in South Korea, Japan, Singapore, and Australia, and the competitive cost advantages of Asian CRO partners that are attracting increasing volumes of discovery outsourcing from North American and European pharmaceutical companies. China's domestic pharmaceutical industry is transitioning from a generics manufacturing heritage toward innovative drug discovery investment, with both state-funded and venture-backed Chinese biotechnology companies building sophisticated discovery capabilities in oncology, immunology, and metabolic disease. India's combination of a large pool of scientifically trained pharmaceutical and chemistry graduates, established CRO industry with international quality standards, and growing domestic pharmaceutical company innovation programmes is positioning the country as an increasingly significant participant in global drug discovery activity.

Latin America and MEA Drug Discovery Market Insights

Latin America is gradually expanding its role in the drug discovery market through growing CRO services in Brazil and Mexico, offering cost-efficient chemistry and biology research support for global pharmaceutical companies. Increasing public research funding and domestic pharmaceutical innovation are strengthening regional oncology and infectious disease research activities.

Pharmaceutical research and discovery activity in the Middle East and Africa is gaining momentum, spearheaded by Israel’s leading edge in biotechnology together with increased health care research funding in the UAE, Saudi Arabia, and South Africa. International cooperation and biotechnology developments have been contributing towards pharmaceutical research advancement in the region.

Growth Drivers: AI-accelerated discovery workflows compressing timelines and expanding the tractable target space, combined with growing pipeline demand from rising chronic and rare disease prevalence

The Drug Discovery Market is primarily driven by rapid advancements in artificial intelligence and machine learning technologies that are significantly improving drug target identification, molecule design, candidate optimization, and biological data analysis. Pharmaceutical firms are adopting AI-based technologies to enhance their research and development efforts by making drug discovery processes quicker, more efficient, and more diverse. On the other hand, the prevalence rates of cancer, neurological conditions, metabolic diseases, and rare genetic disorders have been growing across the globe, thus fueling the demand for novel therapeutics. Increasing amounts invested into research and development of pharmaceutical products and biotechnology, together with advancing precision medicine and genomics, will continue driving the market up until 2035.

Restraints: Persistently high clinical failure rates depleting returns on discovery investment, regulatory pathway complexity for novel modalities, and growing competition for scarce discovery biology and chemistry talent

One major factor limiting the growth potential of the drug discovery market is the high rate of drug candidate failures during the clinical development phase, where a tiny fraction of drug candidates going through clinical trials actually obtain regulatory approval. The lengthy and expensive nature of creating new drugs means that there will always be immense pressure on drug manufacturing firms to raise funds. Additionally, growing complexities associated with regulations regarding gene editing, mRNA technology, CAR-T cell therapy, and RNA-based drugs have created additional uncertainty about their commercialization process. As a result, development of such sophisticated therapies has become increasingly challenging.

Opportunities: AI-native discovery companies building proprietary biological data assets, CRO sector expansion in Asia unlocking cost-competitive global discovery capacity, and data-driven rare disease drug discovery

Key opportunities in the drug discovery market include the fast-growing trend of AI-native drug discovery technologies and increased focus on rare disease drugs. Companies are developing novel biological data sets using AI to predict targets, optimize molecules, and forecast clinical results, thereby providing lucrative licensing options. Increasing trends of computation biology, generation of AI, and simulation technology are driving innovations in precision medicines development. Furthermore, there is also rising interest in rare disease drug discovery because of factors such as availability of orphan drug incentives, expedited approval processes, small trial demands, and extended market exclusivity. These key factors are prompting leading players in the pharmaceuticals and biotech sectors to invest more in innovative drug discovery processes.

Recent Developments:

-

2026: Eli Lilly expanded its AI-driven drug discovery collaboration platform to accelerate obesity, metabolic disorder, and neurodegenerative disease therapeutic development using advanced machine learning-based target identification technologies.

-

2026: Roche announced expansion of its precision oncology drug discovery programs integrating next-generation sequencing, biomarker analytics, and AI-assisted clinical candidate selection for personalized cancer therapies.

-

2026: Pfizer strengthened its biologics and RNA therapeutics discovery pipeline through new investments in mRNA research platforms and AI-enabled molecular design technologies targeting rare and infectious diseases.

Drug Discovery Market Key Players:

-

Eli Lilly

-

Johnson & Johnson

-

AbbVie

-

Merck & Co.

-

Roche

-

Pfizer

-

AstraZeneca

-

Novartis

-

Bayer

-

GlaxoSmithKline (GSK)

-

Amgen

-

Sanofi

-

Bristol Myers Squibb

-

Abbott Laboratories

-

Gilead Sciences

-

Regeneron Pharmaceuticals

-

Vertex Pharmaceuticals

-

Eisai Co., Ltd.

-

Takeda Pharmaceutical Company

-

Biogen

Drug Discovery Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 71.95 Billion |

| Market Size by 2035 | USD 174.92 Billion |

| CAGR | CAGR of 9.29% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Process (Target Identification & Validation, Hit-to-Lead Identification, Candidate Validation, Others) • By Technology (High-Throughput Screening, Bioinformatics, Molecular Modeling & Simulation, Genomics, Others) • By Drug Type (Small Molecules, Biologics, Others) • By End User (Pharmaceutical & Biotechnology Companies, Contract Research Organizations, Academic & Research Institutes, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Eli Lilly, Johnson & Johnson, AbbVie, Merck & Co., Roche, Pfizer, AstraZeneca, Novartis, Bayer, GlaxoSmithKline (GSK), Amgen, Sanofi, Bristol Myers Squibb, Abbott Laboratories, Gilead Sciences, Regeneron Pharmaceuticals, Vertex Pharmaceuticals, Eisai Co., Ltd., Takeda Pharmaceutical Company, Biogen |

Frequently Asked Questions

North America dominated with approximately 41.27% of revenues in 2025.

Small Molecules dominated with approximately 59.41% of revenues in 2025.

The integration of artificial intelligence and machine learning across all drug discovery process stages, from target identification through candidate validation.

The drug discovery market was valued at USD 71.95 billion in 2025.

The drug discovery market is expected to grow at a CAGR of 9.29% from 2026 to 2035.

Get in Touch