Wound Irrigation Systems Market Report Scope & Overview:

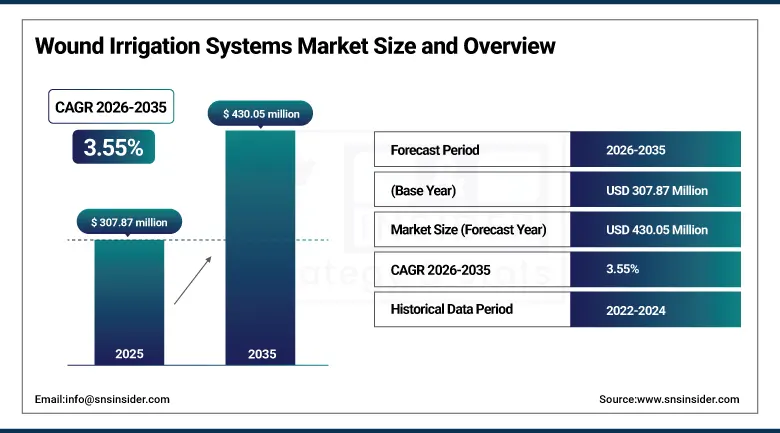

The Wound Irrigation Systems Market was valued at USD 307.87 Million in 2025 and is expected to reach USD 430.05 Million by 2035, growing at a CAGR of 3.55% from 2026 to 2035.

Wound Irrigation Systems are medical equipment used to provide a regulated flow of cleanser fluid into wound sites with a purpose to eliminate any particles, infections, dead skin, or other substances that hinder healing processes. The market of wound irrigation systems develops due to the worldwide diabetes pandemic because of the prediction by IDF about the number of patients suffering from diabetes reaching 783 million by 2045, which leads to an increasing number of people predisposed to developing diabetic foot ulcers and other complications. The increasing number of venous leg ulcers and postoperative complications among the elderly population drives the demand for wound irrigation systems due to the prolonged time frame.

In April 2024, Smith & Nephew launched the Renasys Edge negative pressure wound therapy system, an advanced portable and wearable device specifically designed for chronic wound patients including those with venous leg ulcers and diabetic foot complications. The product's integration of wound irrigation and negative pressure therapy capabilities demonstrated the clinical direction toward combined wound management systems that address multiple wound care requirements.

Market Size and Forecast

-

Market Size in 2026E: USD 318.80 Million

-

Market Size by 2035: USD 430.05 Million

-

CAGR: 3.55% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Wound Irrigation Systems Market - Request Free Sample Report

Wound Irrigation Systems Market Trends

-

Pulsed lavage systems are increasingly preferred over continuous irrigation for improved wound debridement and infection control.

-

Home-based wound irrigation is expanding due to outpatient care growth and cost reduction initiatives.

-

Integrated wound irrigation and negative pressure therapy systems are creating advanced combined treatment solutions.

-

Antimicrobial irrigation solutions are replacing traditional agents due to better biofilm removal and lower tissue toxicity.

-

Single-use wound irrigation devices are gaining adoption due to stricter hospital infection control requirements.

The U.S. Wound Irrigation Systems Market Outlook

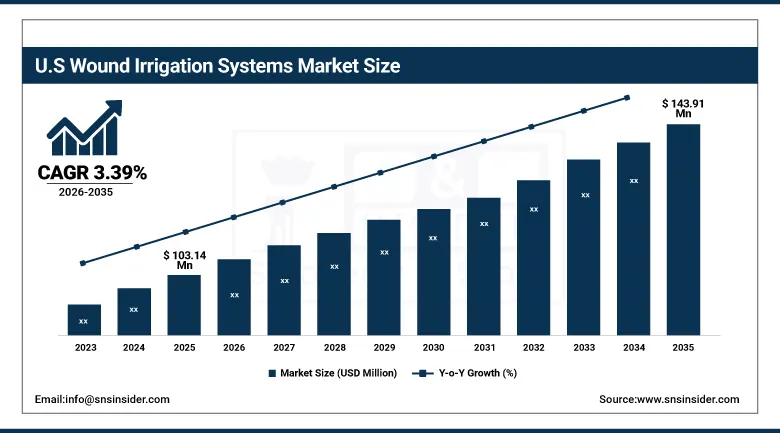

The U.S. Wound Irrigation Systems Market was valued at approximately USD 103.14 Million in 2025 and is expected to reach approximately USD 143.91 Million by 2035, growing at a CAGR of approximately 3.39%.

The USA is the largest consumer market for wound irrigation products. The prevalence of diabetes, obesity, and heart diseases leads to many patients having chronic wounds. There is a good network of ambulatory surgery centers that results in procedures being widely performed. There are also clinical practices and guidelines by the CDC and Joint Commission promoting wound irrigation for prevention of infections. With value-based payment programs, there is more incentive to adopt such devices. Wound irrigation products offer tangible savings in the form of better results.

Two new innovations of Valleylab FT10 Surgical Energy Generators from the company were launched in the month of September, 2025, in India, and had certifications from both the USFDA and CE. Even though the surgical device innovation was concentrated on energy generation and not on wound irrigation, it must be said that it is a sign that the surgical device manufacturers have begun moving into Asian nations.

Wound Irrigation Systems Market Segment Analysis

-

By Product Type, manual wound irrigation systems dominated the market with 53% share in 2025, while the battery-operated segment is the fastest growing product type during 2026 to 2035.

-

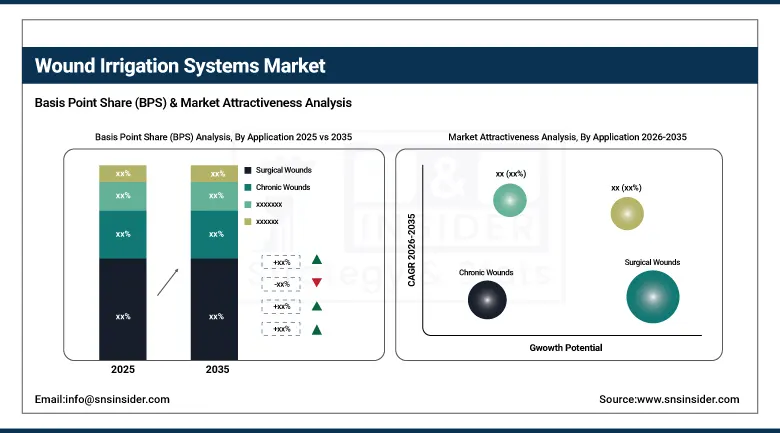

By Application, the surgical wounds segment held the largest market share in 2025, while the chronic wounds segment is the fastest growing application with a CAGR of 7.2% over the forecast period.

-

By End User, hospitals dominated the market with over 45% share in 2025, while ambulatory surgical centers are the fastest growing end user during 2026 to 2035.

By Application, surgical wounds dominate, chronic wounds grow fastest

Surgical wounds generated the largest application revenue share in 2025, reflecting the enormous volume of annual surgical procedures globally whose wound irrigation requirements at surgery, during closure, and post-operatively create a large and predictable demand base. Each of the estimated 313 million major surgical procedures performed annually represents a potential irrigation device usage event. Surgical site infection affecting an estimated 2 to 4% of surgical patients and adding USD 10,000 to USD 25,000 in treatment costs per episode provides a powerful economic incentive for thorough intraoperative wound irrigation whose per-procedure cost is a fraction of the avoided complication expense.

Chronic wounds are growing fastest with a documented CAGR of 7.2%, driven by the global epidemic of diabetes, obesity, venous insufficiency, and peripheral arterial disease that collectively create the largest growing chronic wound patient population in medical history. The International Diabetes Federation's projection of 783 million diabetic individuals by 2045 translates directly into a rapidly expanding diabetic foot ulcer patient population whose chronic wound management requirements, measured in weeks to months of active treatment per episode, create sustained per-patient wound irrigation device consumption that compounds with annual new wound incidence to create a chronically growing chronic wound irrigation market.

By Product Type, manual systems dominate, battery-operated systems grow fastest

Manual wound irrigation systems generated 53% of market revenue in 2025, maintaining dominance through clinical familiarity, low unit cost, and broad applicability across hospital wards, wound care clinics, and home settings. The clinical simplicity of manual irrigation makes it the universally accessible wound care intervention whose adoption barrier is lower than any powered alternative regardless of healthcare resource level. Piston syringes, bulb syringes, squeeze bottles, and thumb-controlled spray devices whose disposable design aligns with infection control requirements maintain the low per-procedure cost that high-volume wound care settings require for sustainable daily management.

Battery-operated wound irrigation systems are growing fastest as pulsed lavage technology's superior debridement capability in deep wounds, tunnelling ulcers, and contaminated surgical sites creates clinical pull from wound care specialists and orthopedic surgeons whose complex wound management requirements exceed the debridement efficacy that manual irrigation can deliver. Battery-operated devices providing electronically controlled pulsed fluid delivery at optimized pressure cycles between 4 and 15 psi create the mechanical disruption of wound biofilm and necrotic tissue whose removal is the rate-limiting step in healing acceleration for the most clinically challenging wound presentations.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

84.73% |

|

Europe |

Germany |

28.47% |

|

Asia Pacific |

China |

38.47% |

|

Middle East & Africa |

UAE |

22.84% |

|

Latin America |

Brazil |

43.84% |

North America Wound Irrigation Systems Market Insights

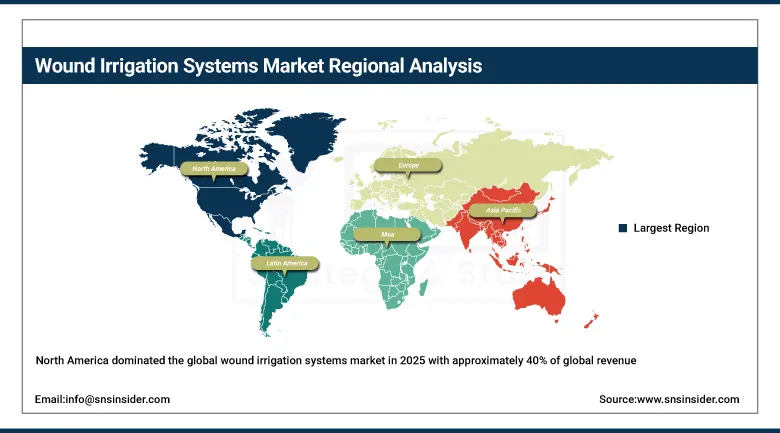

North America dominated the global wound irrigation systems market in 2025 with approximately 40% of global revenue, maintaining its leadership through advanced healthcare infrastructure, strong clinical awareness of wound irrigation best practices, and the presence of major wound care companies. The United States accounts for approximately 84.73% of regional revenue through its high surgical volume, large chronic wound patient population driven by diabetes and obesity prevalence, and the strong reimbursement framework for wound care procedures under Medicare and Medicaid whose coverage of wound management devices sustains clinical adoption.

The commercial presence of major wound irrigation system manufacturers including Stryker, Zimmer Biomet, and Becton Dickinson whose North American operations define product innovation and clinical education standards contributes to regional market leadership.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Wound Irrigation Systems Market Insights

Europe held a significant share of global Wound Irrigation Systems revenues in 2025. The United Kingdom, Germany, France, and the Netherlands are the leading national markets, each hosting advanced wound care clinical infrastructure and strong evidence-based wound management culture whose clinical guidelines explicitly incorporate wound irrigation as a standard care component. European public healthcare systems' cost efficiency focus creates consistent demand for wound irrigation products whose infection prevention value proposition reduces the more costly complication treatments that inadequate wound cleansing generates.

Germany accounts for approximately 28.47% of European revenues through its large hospital sector, high surgical procedure volume, and the commercial presence of European wound care companies whose product distribution sustains regional market activity.

Asia Pacific Wound Irrigation Systems Market Insights

Asia Pacific is the fastest-growing regional wound irrigation systems market, with a documented CAGR of 4.7% over the forecast period, driven by rapidly expanding healthcare infrastructure investment across China, India, South Korea, Japan, and Southeast Asian markets, growing surgical procedure volumes accompanying rising incomes and healthcare access, and the rapidly increasing diabetes prevalence across the region that is creating a large chronic wound patient population whose care requirements are driving wound care product adoption.

China accounts for approximately 38.47% of Asia Pacific revenues through its large hospital network, growing surgical procedure volumes, and government investment in healthcare quality improvement that includes wound care standardization programmes. India is growing particularly rapidly as its expanding medical infrastructure, increasing surgical capability, and growing diabetes burden create accelerating wound care demand.

MEA & Latin America Wound Irrigation Systems Market Insights

Middle East and Latin America are growing wound irrigation systems markets where improving healthcare access, expanding hospital infrastructure, and rising chronic disease burden are creating growing wound care product demand. The UAE leads MEA revenues at approximately 22.84% of the regional total through its world-class hospital infrastructure, high surgical procedure volume serving both domestic and medical tourism patients, and growing wound care specialization, whose clinical standards are progressively aligned with international best practice guidelines that specify wound irrigation as standard care.

Brazil leads Latin American revenues at approximately 43.84% of the regional total through its large public hospital network, growing diabetes burden that creates significant chronic wound patient volume, and progressive adoption of international wound care protocols by its medical community.

Market Dynamics

Growth Drivers: Rising chronic wound cases driven by diabetes and higher surgical volumes are key growth drivers for the wound irrigation systems market.

The wound irrigation systems market's growth is structurally driven by two converging patient population trends. The global diabetes epidemic creates approximately 7.4 million new diabetic foot ulcer cases annually, each requiring wound irrigation as standard clinical management, and the diabetic population is growing by approximately 10 million per year globally. The ageing population's elevated susceptibility to pressure ulcers, venous leg ulcers, and delayed surgical healing creates a second growing chronic wound cohort sustaining long-duration irrigation device consumption. Rising global surgical volumes create growing acute wound care requirements whose infection prevention imperative makes wound irrigation a consistent surgical site care protocol component.

Restraints: Limited awareness of proper wound irrigation technique in low-resource healthcare settings constrain adoption of advanced irrigation systems.

Wound irrigation's clinical benefit is heavily technique-dependent, requiring delivery of irrigation fluid at appropriate pressure, volume, and direction to achieve the mechanical debridement of wound contaminants. In healthcare settings where wound care education has not included systematic irrigation technique training, suboptimal manual irrigation with insufficient pressure or inadequate fluid volume fails to achieve the bacterial load reduction and debris removal creating a performance gap between potential and realized clinical benefit. Healthcare budget constraints in lower-income healthcare systems create barriers to adoption of battery-operated pulsed lavage systems whose capital and consumable costs substantially exceed manual irrigation alternatives despite their superior clinical outcomes in complex wound presentations.

Opportunities: Home care wound irrigation expansion and combination wound management system development represent growth opportunities.

The shift of wound care from inpatient to outpatient and home settings, driven by cost containment and telemedicine-enabled remote clinical supervision, is creating a growing market for home care-compatible irrigation devices. Patient-operated devices delivering appropriate therapeutic pressure without clinical training, portable enough for daily self-management, and priced within community nursing budgets represent a product development frontier whose successful resolution creates the largest untapped growth opportunity in the wound irrigation systems category. Each percentage point increase in chronic wound patients receiving home care multiplies the consumer product opportunity for manufacturers whose institutional product lines cannot address self-managed care contexts.

Recent Developments:

-

2026: Stryker expanded its surgical wound irrigation portfolio with enhanced pulsed lavage systems featuring improved pressure control and infection prevention capabilities for operating rooms.

-

2026: B. Braun introduced an upgraded wound irrigation platform with sterile single-use components, targeting hospital infection control programs and reducing cross-contamination risks in surgery settings.

-

2025: Medtronic expanded its advanced surgical device portfolio with the Valleylab FT10 surgical energy generator launch in India, reflecting the broader industry trend of major surgical device companies investing in Asian market infrastructure.

Wound Irrigation Systems Market key players are:

-

Stryker Corporation

-

Zimmer Biomet Holdings Inc.

-

Becton Dickinson and Company

-

Smith & Nephew PLC

-

Molnlycke Health Care AB

-

ConvaTec Group PLC

-

Medline Industries LP

-

Cardinal Health Inc.

-

B. Braun Melsungen AG

-

3M Company (Solventum)

-

Coloplast AS

-

Hollister Incorporated

-

SunMed LLC

-

Deroyal Industries Inc.

-

Bionix Development Corporation

-

CooperSurgical Inc.

-

Owens & Minor Inc.

-

Integra LifeSciences Corp.

-

Medtronic plc

-

HARTMANN Group

Wound Irrigation Systems Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 307.87 Million |

| Market Size by 2035 | USD 430.05 Million |

| CAGR | CAGR of 3.55% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Manual Wound Irrigation Systems, Battery-Operated Wound Irrigation Systems) • By Application (Surgical Wounds, Chronic Wounds, Traumatic Wounds, Burns, Others) • By End User (Hospitals, Ambulatory Surgical Centers, Wound Care Centers, Home Care Settings, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Stryker Corporation, Zimmer Biomet Holdings Inc., Becton Dickinson and Company, Smith & Nephew PLC, Molnlycke Health Care AB, ConvaTec Group PLC, Medline Industries LP, Cardinal Health Inc., B. Braun Melsungen AG, 3M Company (Solventum), Coloplast AS, Hollister Incorporated, SunMed LLC, Deroyal Industries Inc., Bionix Development Corporation, CooperSurgical Inc., Owens & Minor Inc., Integra LifeSciences Corp., Medtronic plc, HARTMANN Group |

Frequently Asked Questions

The Wound Irrigation Systems Market is expected to grow at a CAGR of 3.55% from 2026 to 2035.

The Wound Irrigation Systems Market was valued at USD 307.87 Million in 2025.

Rising global chronic wound prevalence driven by the diabetes epidemic creating millions of new wound patients annually.

The manual wound irrigation systems segment dominated the Wound Irrigation Systems Market.

North America dominated the Wound Irrigation Systems Market in 2025.

Get in Touch