Duodenoscopes Market Report Scope & Overview:

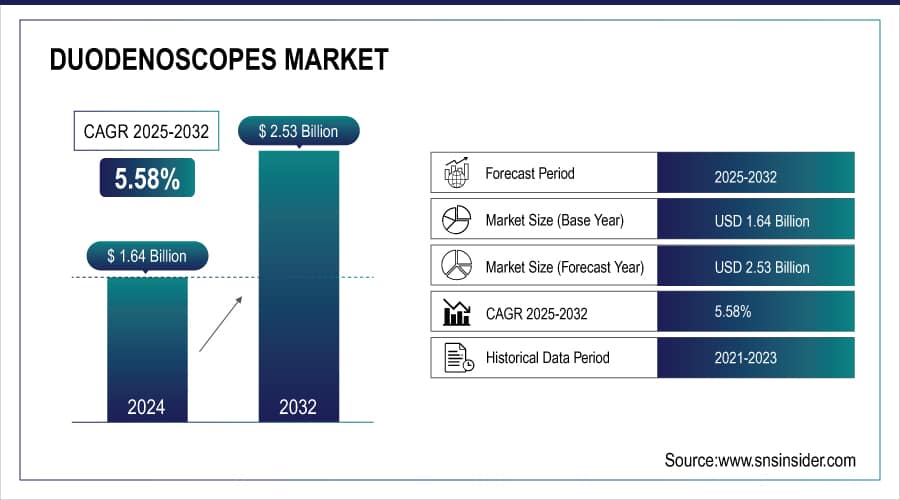

The Duodenoscopes Market size was valued at USD 1.64 billion in 2024 and is expected to reach USD 2.53 billion by 2032, growing at a CAGR of 5.58% over 2025-2032.

The global duodenoscopes market is growing steadily, driven by a rising number of cases of gastrointestinal disorders, such as pancreaticobiliary diseases, and an increasing preference for less invasive endoscopic surgeries. Technological advancements in endoscopy, combined with the rise in the geriatric population, also propel the duodenoscopes market's growth. A major factor is the increasing concerns about infections related to reusable duodenoscopes, which has led to regulatory action on single-use duodenoscopes, thus driving innovation and supply.

For instance, the U.S. FDA has urged a move to completely disposable models due to contamination risks, expediting R&D outlays, and regulatory approvals. Prominent players, such as Olympus Corporation, Pentax Medical, and Ambu A/S are making huge investments in designing advanced duodenoscopes with advanced safety and user-friendly features. Lesser budgets are being diverted to premium endoscopy equipment in hospitals, and a greater emphasis is being put on R&D funding in endoscopic visualization and disposable technologies. Moreover, favorable reimbursement structures and a rise in procedural volumes in nations, such as the U.S., Germany, and Japan are contributing to the duodenoscopes market trends.

In May 2024, Olympus Corporation received marketing authorization for the use of its TJF-Q290V duodenoscope in the EU with better reprocessing compatibility and infection control, to facilitate its duodenoscopes market share growth in the European Union.

Duodenoscopes Market Size and Forecast:

-

Market Size in 2024: USD 1.64 billion

-

Market Size by 2032: USD 2.53 billion

-

CAGR: 5.58% from 2025 to 2032

-

Base Year: 2024

-

Forecast Period: 2025–2032

-

Historical Data: 2021–2023

To Get More Information On Duodenoscopes Market - Request Free Sample Report

Duodenoscopes Market Trends

-

Rising prevalence of gastrointestinal disorders, pancreatic cancer, bile duct diseases, and gallstones is increasing the demand for advanced endoscopic procedures such as ERCP (Endoscopic Retrograde Cholangiopancreatography).

-

Growing preference for minimally invasive diagnostic and therapeutic procedures is driving adoption of advanced duodenoscopes in hospitals and ambulatory surgical centers.

-

Technological advancements, including disposable/single-use duodenoscopes, improved visualization systems, and enhanced infection control designs, are addressing cross-contamination risks and boosting market growth.

-

Increasing regulatory focus on patient safety and reprocessing standards is encouraging healthcare facilities to shift toward innovative and sterile device solutions.

-

Expansion of healthcare infrastructure and endoscopy units in emerging markets is supporting increased procedural volumes and equipment demand.

-

Strategic collaborations between medical device manufacturers and healthcare providers are accelerating product innovation and market penetration.

-

Integration of digital imaging, high-definition visualization, and AI-assisted endoscopy platforms is improving diagnostic accuracy and procedural efficiency.

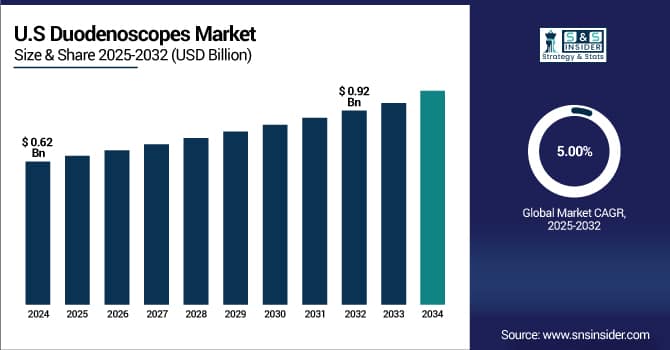

The U.S. Duodenoscopes Market size was valued at USD 0.62 billion in 2024 and is expected to reach USD 0.92 billion by 2032, growing at a CAGR of 5.00% over 2025-2032. The growth is also attributed to high FDA stringency levels that encourage a more safer endoscopy practices, which in turn lead to faster R&D investments and floor pricing strategies among leads, such as Ambu and Boston Scientific. It also gains from positive reimbursement policies and ongoing upgrades at hospitals to the endoscopy departments. Canada is observing increasing use in tertiary care centers and a start in robotic and AI-assisted scopes. High demand for infection-resistant and AI-powered models makes North America remain the largest duodenoscopes market statement globally.

Duodenoscopes Market Drivers:

-

Advancing Procedures, Innovation, and Safety Protocols Fuel Duodenoscopes Market Growth

The rising number of procedural volumes in ERCP (endoscopic retrograde cholangiopancreatography), which exceeds 500,000 procedures per year in the U.S., as per the American Society for Gastrointestinal Endoscopy, is also driving the duodenoscopes market growth. Increasing prevalence of pancreaticobiliary and duodenal disorders, and the ageing of the world population, have driven continuing procedural need. Moreover, adoption is being spurred by the introduction of antimicrobial-coated and robotic-assisted duodenoscopes, which are enhancing clinical success while minimizing the risk of infection.

Companies including Boston Scientific and Karl Storz are investing in innovation and clinical validation. Moreover, increasing expenditure on healthcare infrastructure and hospital purchase of advanced imaging techniques is a factor that significantly contributes to the demand for a robust duodenoscopes market. There are also positive developments in product innovation through partnerships between device manufacturers and academia. The R&D investment in endoscopic tools has increased significantly, with more than USD 1.5 billion invested in GI device innovation in 2023 by both private and public entities globally. In addition, the production of reprocessing-resistant materials and modular scope designs aligns with changing health care safety protocols and supports market growth.

Duodenoscopes Market Restraints:

-

Regulatory Hurdles, High Costs, and Infection Risks Hamper Widespread Adoption in the Duodenoscopes Market

The duodenoscopes market report has limitations such as infection control concerns and higher cost of capital for advanced models, even though great opportunities to grow are offered. Reusable duodenoscopes have been associated with several multidrug-resistant infection outbreaks and have attracted increased scrutiny and bad press. The FDA’s 2022 mandate of a transition to fully disposable or semi-disposable duodenoscopes has significant implications on hospitals and endoscopy centers in the U.S., being particularly burdensome in low-resource environments.

Moreover, due to high purchase costs, over USD 40,000 per unit, and ongoing charges associated with reprocessing and maintenance, mid-tier and public hospitals find it difficult to adopt the technology. Regulatory hurdles in certain emerging markets create delays in approvals, crimping product availability. Furthermore, the challenges in operation are their training difficulties and long learning curves of advanced scope models. For instance, with the delayed approvals from the European Medical Device Regulation (MDR), it has slowed down new device entrants. All these factors together limit the duodenoscopes market share, especially in cost-effective and resource-deprived healthcare settings.

Duodenoscopes Market Segmentation Analysis:

By Application

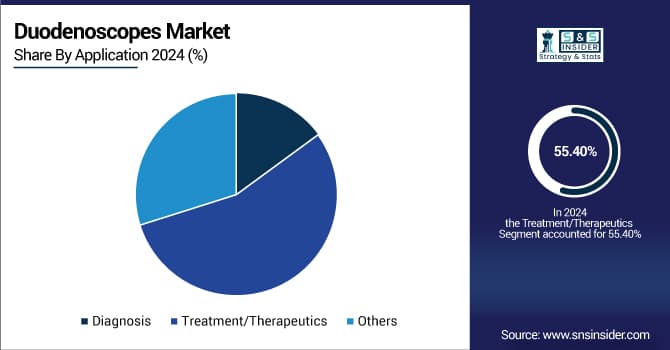

On the basis of application, the treatment/therapeutics segment was the market leader, contributing 55.4% share in 2024, since duodenoscopes are most frequently utilized for therapeutic ERCP procedures, such as bile duct stenting and stone extraction. The diagnosis segment is expected to register the highest CAGR in the market during the forecast period. The segment’s growth is driven by the increasing demand for early detection of GI disorders and combined advanced imaging modalities.

By Product Type

The flexible video duodenoscopes product type led the market in 2024 and held a share of about 52.8% of the duodenoscopes market. This leadership is attributed to the segment’s high-definition imaging, real-time navigation, and superior diagnostic accuracy that are vital for therapeutic ERCP procedures. Such devices are extensively utilized in tertiary care centers owing to their clinical reliability and compatibility with newer imaging modalities. Their easy access and ever-progressing digital optics technologies also identify their leadership in the international scene.

Rigid duodenoscopes are the fastest-growing product type. They have a narrow role, and recently, the role of tri-phasics in diagnostic interventions in specific situations and the pediatric age group has expanded. Moreover, their lower cost, lower risk of contamination, and ease of sterilization make them more attractive in low-resource and outpatient settings, where accuracy tolerance is not a top concern.

By Technology

Based on technology, the digital duodenoscopes technology segment accounted for the largest share of the market in 2024, due to the integration of digital systems with existing imaging platforms, real-time data sharing, and enhanced diagnostic yield. On the other hand, AI-integrated duodenoscopes are experiencing the fastest growth on account of being widely adopted in high-volume centers to minimize procedural time and enhance diagnostic accuracy.

By Usability

Reusable duodenoscopes held a market share of 63.2% in 2024 due to the existing resource base and cost effectiveness over repeated procedures. Disposable duodenoscopes is the fastest growing segment owing to growing infection control regulations, mandates by the FDA, and adoption of safer alternatives across the world.

By End-User

Based on end user, the hospitals held the majority of the share in 2024, i.e., 68.9% owing to a high patient pool, advanced healthcare infrastructure, and the presence of skilled professionals. However, ambulatory surgical centers (ASCs) are the fastest-growing end-user segment, owing to shorter recovery periods, lower procedural costs, and rising adoption of regulatory approvals on outpatient ERCPs.

Duodenoscopes Market Regional Analysis:

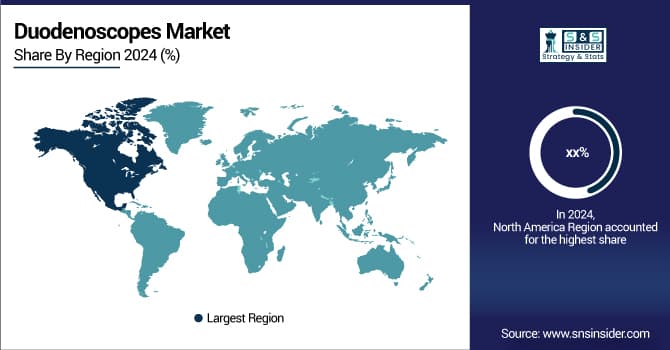

North America dominated the duodenoscopes market share in 2024, to some extent due to the high number of ERCPs being performed in the U.S., with over 500,000 cases being performed every year, well-established healthcare infrastructure, and early adoption of single-use duodenoscopes.

Get Customized Report as Per Your Business Requirement - Enquiry Now

The Asia Pacific region is the fastest-growing, fueled by rising healthcare spending, increasing GI health awareness, and a rapidly expanding number of tertiary care hospitals. The regional market is dominated by China, due to a high disease burden and favorable government policies that aggressively invest in hospital infrastructure and advanced diagnostic devices. The country is also investing in developing the local endoscope tools industry, reducing dependencies on imports.

India is rising rapidly due to the large patient population and growing affordability of procedures, but rural areas remain difficult to penetrate. Japan is a key market player due to its strong medical devices industry and technological leadership. It contributes to substation developments by integrating AI and smart duodenoscopes into clinical workflows. South Korea and Australia have stricter infection control measures and are rapidly switching to single-use models.

Duodenoscopes Market Key Players:

Leading duodenoscopes companies in the market include Olympus Corporation, Ambu A/S, Boston Scientific Corporation, PENTAX Medical (HOYA Corporation), FUJIFILM Holdings Corporation, KARL STORZ GmbH & Co. KG, Custom Ultrasonics Inc., ENDOMED, CONMED Corporation, Becton Dickinson and Company, B. Braun Melsungen AG, Cook Group Incorporated, SonoScape Medical Corp., Ottomed Endoscopy, Richard Wolf GmbH, Stryker Corporation, Smith & Nephew plc, Medtronic plc, MEDIVATORS Inc., and Mindray Medical International Limited.

Recent Developments:

In August 2024, Advanced Sterilization Products (ASP) teamed with PENTAX Medical to secure FDA clearance for the ULTRA GI Cycle in the STERRAD 100NX sterilizer, featuring ALLClear Technology. This hydrogen peroxide gas plasma cycle provides enhanced sterilization of reusable duodenoscopes, significantly elevating reprocessing safety standards.

In April 2024, Ambu received FDA approval for its next-generation system, aScope Duodeno 2, alongside the aBox 2 processor for ERCP procedures. The devices feature improved ergonomic design and streamlined workflow, speeding clinical uptake in high-volume settings.

| Report Attributes | Details |

|---|---|

| Market Size in 2024 | USD 1.64 billion |

| Market Size by 2032 | USD 2.53 billion |

| CAGR | CAGR of 5.58% From 2025 to 2032 |

| Base Year | 2024 |

| Forecast Period | 2025-2032 |

| Historical Data | 2021-2023 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Flexible Video Duodenoscopes, Flexible Non-Video Duodenoscopes, Rigid Duodenoscopes, Others (e.g., hybrid duodenoscopes with enhanced imaging features or ergonomic designs)) • By Technology (Optical Duodenoscopes, Digital Duodenoscopes, AI-Integrated or Smart Duodenoscopes, Others (e.g., HD or 4K scopes with image-enhancement technologies)) • By Usability (Reusable Duodenoscopes, Disposable Duodenoscopes, Duodenoscopes with Disposable Distal Caps, Others (e.g., reprocessable duodenoscopes with advanced sterilization technology)) • By Application (Diagnosis, Treatment/Therapeutics, Others (e.g., biopsy collection, ERCP-guided stent placement, gallstone retrieval)) • By End User (Hospitals, Ambulatory Surgical Centers (ASCs), Clinics, Pediatric Centers, Others (e.g., academic & research institutions, specialty GI centers)) |

| Regional Analysis/Coverage | North America (U.S., Canada), Europe (Germany, France, UK, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America) |

| Company Profiles | Olympus Corporation, Ambu A/S, Boston Scientific Corporation, PENTAX Medical (HOYA Corporation), FUJIFILM Holdings Corporation, KARL STORZ GmbH & Co. KG, Custom Ultrasonics Inc., ENDOMED, CONMED Corporation, Becton Dickinson and Company, B. Braun Melsungen AG, Cook Group Incorporated, SonoScape Medical Corp., Ottomed Endoscopy, Richard Wolf GmbH, Stryker Corporation, Smith & Nephew plc, Medtronic plc, MEDIVATORS Inc., and Mindray Medical International Limited. |

Frequently Asked Questions

Major trends include the rise of single-use duodenoscopes, integration of AI-enhanced imaging, and regulatory pressure for safer endoscopy practices.

Reusable duodenoscopes require high-level disinfection between uses, while disposable ones are designed for single use to eliminate cross-contamination risks.

Key players include Olympus Corporation, Ambu A/S, Boston Scientific, PENTAX Medical, FUJIFILM, and Custom Ultrasonics, among others.

PENTAX Medical holds a significant market share due to its strong portfolio of advanced optical and digital duodenoscopes, alongside Olympus and Boston Scientific.

Market growth is driven by rising gastrointestinal disease prevalence, increased adoption of minimally invasive procedures, and a shift toward infection prevention via disposable duodenoscopes.

Get in Touch