Heart Failure Drugs Market Report Scope & Overview:

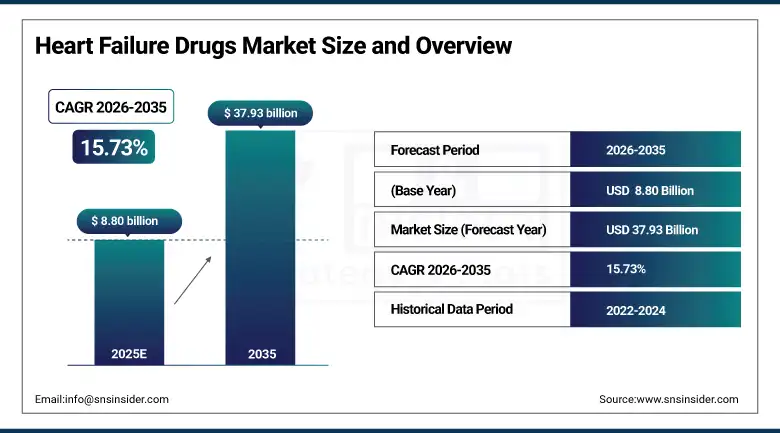

The Heart Failure Drugs Market Size is valued at USD 8.80 Billion in 2025 and is expected to reach USD 37.93 Billion by 2035 and grow at a CAGR of 15.73% over the forecast period 2026-2035.

The Heart Failure Drugs Market analysis, fueled by demographic and epidemiological trends. Globally, populations are ageing, which increases the risk of cardiovascular diseases and heart failure. At the same time, lifestyle‑related conditions such as hypertension, diabetes, obesity, and sedentary habits are on the rise. According to study, Globally, over 12–13% of adults aged 60+ are at risk of heart failure due to age-related cardiovascular degeneration.

Market Size and Forecast:

-

Market Size in 2025: USD 8.80 Billion

-

Market Size by 2035: USD 37.93 Billion

-

CAGR: 15.73% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information On Heart Failure Drugs Market - Request Free Sample Report

Heart Failure Drugs Market Trends:

-

Increasing prevalence of heart failure fuels demand for advanced drug therapies.

-

Growing adoption of ACE inhibitors, beta-blockers, and ARNI medications worldwide.

-

Rising obesity, diabetes, and sedentary lifestyles increase patient treatment needs.

-

High costs and reimbursement limitations restrict access in developing countries.

-

Investment in personalized medicine and combination therapies enhances treatment effectiveness.

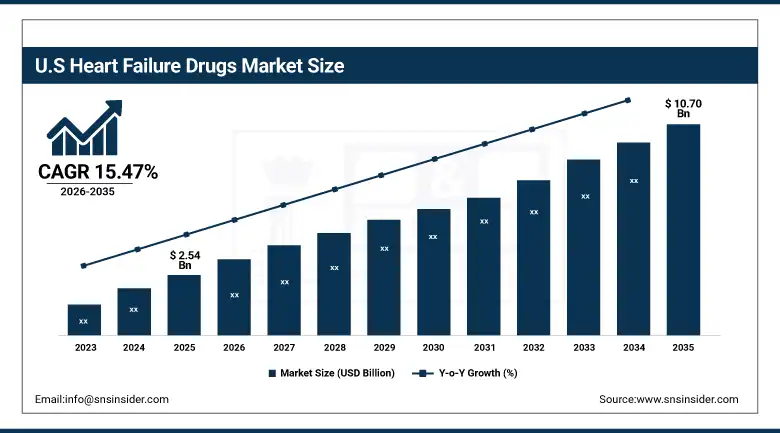

The U.S. Heart Failure Drugs Market size is USD 2.54 Billion in 2025 and is expected to reach USD 10.70 Billion by 2035, growing at a CAGR of 15.47% over the forecast period of 2026-2035, driven by a high prevalence of cardiovascular diseases, advanced healthcare infrastructure, widespread adoption of innovative therapies, strong patient awareness, and supportive reimbursement policies, ensuring sustained growth and robust treatment adoption.

Heart Failure Drugs Market Growth Drivers:

-

Rising global heart failure cases driving demand for effective drugs

A major driver for the heart failure drugs market growth is the growing global incidence of cardiovascular diseases, especially heart failure, driven by aging populations, rising obesity rates, diabetes, and sedentary lifestyles. As more patients are diagnosed with chronic heart conditions, the demand for effective pharmacological management, including ACE inhibitors, beta-blockers, ARNI (angiotensin receptor-neprilysin inhibitors), and SGLT2 inhibitors, is rising. Governments and healthcare providers are also emphasizing preventive care and early intervention, leading to higher prescriptions and wider adoption of heart failure drugs.

Novel drugs like ARNI and SGLT2 inhibitors projected 18–20% CAGR growth.

Heart Failure Drugs Market Restraints:

-

High therapy costs and limited reimbursement hinder widespread drug adoption

A significant restraint for the market is the high cost of advanced heart failure therapies and limited insurance coverage in certain regions. Novel drugs, such as ARNI and SGLT2 inhibitors, often come with premium pricing, making them less accessible in developing countries or among underinsured populations. Moreover, strict reimbursement policies and limited government support in low-income markets can hinder the adoption of new, clinically superior therapies.

Heart Failure Drugs Market Opportunities:

-

Innovation and personalized medicine create significant growth opportunities globally

A major opportunity exists in the development of next-generation therapies and personalized medicine approaches for heart failure management. Pharmaceutical companies are investing heavily in novel drug classes, combination therapies, and biomarkers-based personalized treatments that optimize efficacy and minimize side effects. Advances in genomic profiling and digital health integration allow clinicians to tailor drug regimens based on individual patient profiles. In addition, emerging markets with growing healthcare infrastructure and increasing awareness about chronic disease management present a substantial growth opportunity for companies to expand their footprint and introduce advanced heart failure medications.

Healthcare expenditure for heart failure drugs anticipated to grow over $45 billion by 2030.

Heart Failure Drugs Market Segmentation Analysis:

-

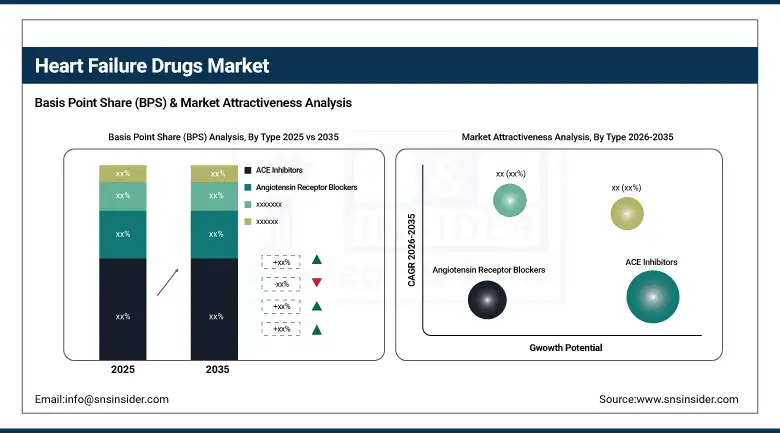

By Type: In 2025, ACE Inhibitors led the market with a share of 34.80%, while Beta Blockers is the fastest-growing segment with a CAGR of 12.90%.

-

By Application: In 2025, Tablets led the market with a share of 49.60%, while Injection is the fastest-growing segment with a CAGR of 11.70%.

-

By Distribution Channel: In 2025, Hospital Pharmacies led the market with a share of 45.20%, while Online Pharmacies is the fastest-growing segment with a CAGR of 14.80%.

-

By End Users: In 2025, Hospitals led the market with a share of 53.40%, while Specialty Centres is the fastest-growing segment with a CAGR of 12.10%.

By Type, ACE Inhibitors Lead Market and Beta Blockers Fastest Growth

In 2025, ACE inhibitors dominate the heart failure drugs market, due to their proven efficacy in reducing morbidity and mortality in chronic heart failure patients. They are widely prescribed across hospitals and outpatient clinics, supported by long-standing clinical guidelines and strong physician preference.

Meanwhile, Beta blockers are the fastest-growing segment, driven by rising awareness of their benefits in improving cardiac function and survival, and expanding adoption in combination therapies. Newer formulations with fewer side effects are encouraging rapid uptake across emerging and developed markets.

By Application, Tablets Leads Market and Injection Fastest Growth

In 2025, Tablets dominate the heart failure drugs market, as oral administration ensures patient convenience, adherence, and suitability for chronic treatment regimens. Tablets are widely used in hospitals, specialty centers, and home care, supporting long-term disease management.

Meanwhile, Injections are the fastest-growing application segment, primarily due to increasing use in acute heart failure management, hospital-based treatments, and emerging biologic therapies. Newer injectable formulations and improved hospital protocols are driving adoption, particularly in advanced care units and specialty centers where rapid therapeutic action is required.

By Distribution Channel, Hospital Pharmacies Lead Market and Online Pharmacies Fastest Growth

In 2025, Retail pharmacies lead the heart failure drugs market, as they provide easy access for chronic patients requiring regular refills. They ensure widespread availability of generics and branded medications and support patient counseling and adherence programs. Hospital pharmacies also play a critical role in inpatient care, but retail remains the primary channel for ongoing therapy management.

Meanwhile, Online pharmacies are the fastest-growing segment, driven by increasing e-commerce adoption, convenience, doorstep delivery, and growing digital health awareness. Telemedicine prescriptions and digital marketing by pharmaceutical companies are accelerating online purchases, especially in urban and semi-urban regions, providing patients with faster access to heart failure medications.

By End Users, Hospitals Leads Market and Specialty Centres Fastest Growth

In 2025, Hospitals dominate segment, being the primary sites for prescribing, monitoring, and managing heart failure therapies. Their role in chronic disease management, acute care, and patient follow-up ensures the highest volume of drug utilization.

Meanwhile, Specialty centers are the fastest-growing segment, including cardiac care units, outpatient heart clinics, and dedicated heart failure management programs. Increased awareness of specialized care benefits, combined with expanding infrastructure in emerging markets, drives higher adoption rates and growth in these focused healthcare settings.

Heart Failure Drugs Market Regional Analysis:

North America Heart Failure Drugs Market Insights:

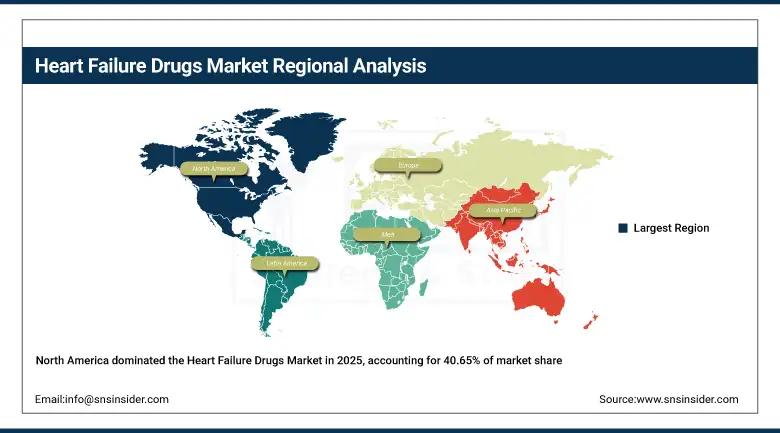

The North America dominated the Heart Failure Drugs Market in 2025E, with over 40.65% revenue share, due to high prevalence of cardiovascular diseases, advanced healthcare infrastructure, and strong adoption of innovative therapies. Availability of well-established healthcare facilities, easy access to prescription drugs, and high patient awareness drive demand. The region benefits from extensive clinical trials, robust R&D pipelines, and favorable reimbursement policies. Growing geriatric population and increasing incidence of chronic heart failure contribute to sustained market growth. North America continues to lead in the adoption of novel drugs such as SGLT2 inhibitors, ARNIs, and beta-blockers.

Get Customized Report as per Your Business Requirement - Enquiry Now

U.S. Heart Failure Drugs Market Insights

The U.S. and Canada lead the Heart Failure Drugs Market due to high disease prevalence, advanced healthcare infrastructure, and widespread adoption of innovative therapies. Patient awareness, clinical trials, and reimbursement policies support sustained growth in both countries.

Asia Pacific Heart Failure Drugs Market Insights:

The Asia-Pacific region is expected to have the fastest-growing CAGR 16.81%, driven by rising cardiovascular disease prevalence, improving healthcare access, and increasing awareness among patients. Expanding healthcare infrastructure, rising disposable incomes, and growing adoption of guideline-directed medical therapies support rapid market expansion. The region is witnessing increasing investments in chronic disease management and cardiovascular care programs. Urbanization, lifestyle changes, and a growing geriatric population are further boosting demand. Manufacturers are increasingly targeting Asia Pacific with localized strategies and affordable therapies, making it a key driver of global growth in the heart failure drugs market.

China and India Heart Failure Drugs Market Insights

China and India are driving market growth due to rising cardiovascular disease prevalence, increasing healthcare access, and expanding patient awareness. Urbanization, aging populations, and lifestyle-related risk factors drive adoption of heart failure drugs in both countries.

Europe Heart Failure Drugs Market Insights

Europe holds a strong position in the Heart Failure Drugs Market due to well-established healthcare systems, high cardiovascular disease burden, and strong adoption of guideline-recommended therapies. Continuous R&D investments and availability of advanced prescription drugs such as ACE inhibitors, beta-blockers, and ARNIs support market growth. Increasing awareness among patients and healthcare providers, along with favorable reimbursement policies, drives treatment adoption. The region benefits from a growing geriatric population and rising prevalence of comorbidities such as hypertension and diabetes, which increase the demand for heart failure management and expand market potential steadily.

Germany and U.K. Heart Failure Drugs Market Insights

The Germany and U.K. Heart Failure Drugs Market is mature with well-established healthcare systems and strong guideline-based therapy adoption. High cardiovascular burden, aging populations, and consistent R&D in novel heart failure drugs ensure steady growth.

Latin America (LATAM) and Middle East & Africa (MEA) Heart Failure Drugs Market Insights

Latin America is experiencing moderate growth in the Heart Failure Drugs Market, driven by increasing cardiovascular disease prevalence and improving healthcare access. Rising awareness of chronic heart failure management and gradual adoption of guideline-directed therapies support market expansion. Urbanization, lifestyle changes, and a growing elderly population contribute to higher demand for effective heart failure medications. Challenges such as limited access to advanced therapies and uneven healthcare infrastructure constrain faster growth. However, ongoing government initiatives, increasing availability of prescription drugs, and expanding cardiology services are steadily enhancing market penetration in the region.

Additionally, The Middle East & Africa region shows gradual growth in the Heart Failure Drugs Market, supported by rising cardiovascular disease prevalence and increasing patient awareness. Improved healthcare infrastructure, expanding hospital networks, and growing availability of prescription drugs are contributing factors. Market growth is slower due to affordability issues and limited access to advanced therapies in some areas. Urbanization, lifestyle changes, and increasing incidence of comorbidities like hypertension and diabetes are driving demand. Regional focus on cardiovascular disease management programs and investments in healthcare modernization is expected to support future market growth.

Heart Failure Drugs Market Competitive Landscape:

-

In July 2025, Bayer AG, the US FDA approved its drug Kerendia (finerenone) to treat heart failure in patients with left ventricular ejection fraction (LVEF) ≥ 40%, providing a new treatment option that reduces cardiovascular death and hospitalization risks in this patient group.

-

In 2025, Novartis announced a strategic partnership with a digital‑health firm to integrate AI‑driven analytics into its heart‑failure management programs, aiming to improve patient monitoring, personalized care, and long-term clinical outcomes.

-

In Dec 2024, Cytokinetics launched a confirmatory Phase 3 trial (COMET‑HF) for omecamtiv mecarbil in patients with symptomatic heart failure and severely reduced ejection fraction.

Heart Failure Drugs Market Key Players:

-

Merck & Co., Inc.

-

Bristol-Myers Squibb Company

-

Bayer AG

-

Amgen Inc.

-

Boehringer Ingelheim International GmbH

-

Eli Lilly and Company

-

GlaxoSmithKline plc

-

Johnson & Johnson

-

Teva Pharmaceutical Industries Ltd.

-

Sanofi S.A.

-

Gilead Sciences

-

Actelion Pharmaceuticals

-

Otsuka Pharmaceutical Co., Ltd.

-

Cytokinetics, Inc.

-

Cardior Pharmaceuticals

-

Mylan N.V.

-

Daiichi Sankyo Company Ltd.

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 8.80 Billion |

| Market Size by 2035 | USD 37.93 Billion |

| CAGR | CAGR of 15.73% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (ACE Inhibitors, Angiotensin Receptor Blockers, Beta Blockers, Diuretics, Others) • By Application (Injection, Capsule, Tablets) • By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies) • By End Users (Hospitals, Specialty Centres, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Novartis AG, AstraZeneca, Pfizer Inc., Merck & Co., Inc., Bristol-Myers Squibb Company, Bayer AG, Amgen Inc., Boehringer Ingelheim International GmbH, Eli Lilly and Company, GlaxoSmithKline plc, Johnson & Johnson, Teva Pharmaceutical Industries Ltd., Sanofi S.A., Gilead Sciences, Actelion Pharmaceuticals, Otsuka Pharmaceutical Co., Ltd., CYTOKINETICS, Inc., Cardior Pharmaceuticals, Mylan N.V., and Daiichi Sankyo Company Ltd.. |

Frequently Asked Questions

The Heart Failure Drugs Market is valued at USD 8.80 billion in 2025, reflecting steady growth driven by increasing cardiovascular disease prevalence.

The market is expected to reach USD 37.93 billion by 2035, indicating significant expansion over the forecast period.

The market is projected to grow at a CAGR of 15.73% from 2026 to 2035.

Key drivers include rising cases of heart failure, aging populations, advancements in drug therapies, and increased healthcare expenditure.

Major drug classes include ACE inhibitors, beta-blockers, ARBs, aldosterone antagonists, and novel therapies like ARNI drugs.

Get in Touch