Educational Robot Market Report Scope & Overview:

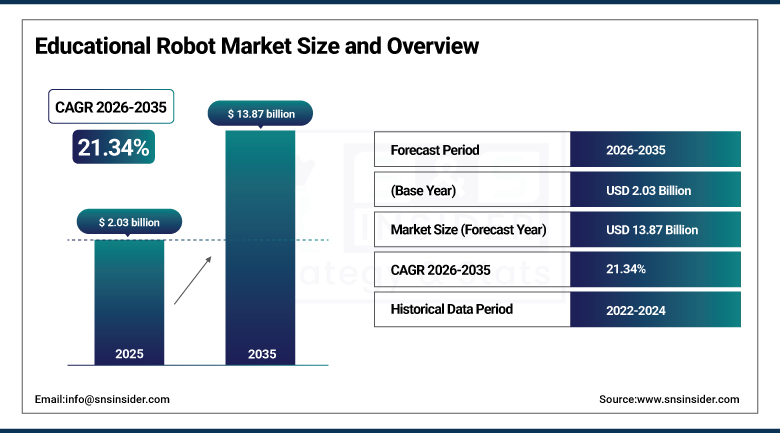

The Educational Robot Market was valued at USD 2.03 Billion in 2025 and is expected to reach USD 13.87 Billion by 2035, growing at a CAGR of 21.34% from 2026–2035.

The global educational robot market is growing at an exceptional pace. Educational robots are programmable and interactive robotic systems designed to facilitate learning across STEM subjects, coding, problem-solving, critical thinking, and social skills through hands-on experiential engagement that traditional classroom instruction cannot replicate equivalently. The market is driven by rising global emphasis on STEM education, rapidly increasing demand for AI-driven personalised learning experiences, government investments in robotics-integrated curricula, and the progressive recognition that early robotics exposure creates foundational technology literacy that sustains lifetime educational and career advantages.

In July 2023, ABB Robotics launched a complete robot training package to prepare students for the future of work, including an easy-to-use GoFa collaborative robot cell, 56 hours of teaching materials, and globally recognised STEM certification as part of its campaign to work with educators to close the automation skills gap. The package directly addresses the commercial recognition that workforce readiness for automated manufacturing and industrial robotics requires school-age exposure to collaborative robot interaction whose practical training creates technical confidence that theoretical curriculum alone cannot develop.

Market Size and Forecast

-

Market Size in 2026E: USD 2.46 Billion

-

Market Size by 2035: USD 13.87 Billion

-

CAGR: 21.34% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

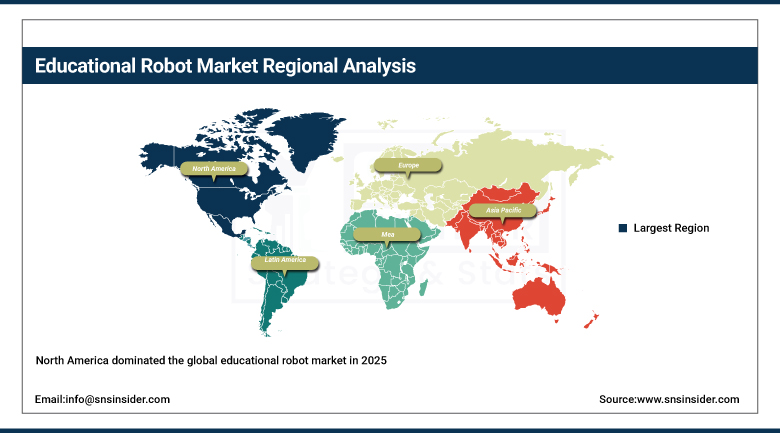

Largest Region: North America

To Get more information on Educational Robot Market - Request Free Sample Report

Educational Robot Market Trends

-

AI-powered educational robots are enabling personalized learning experiences by adapting content, pace, and instruction methods to individual student needs

-

Growing integration of collaborative robots in schools and universities is helping students develop practical skills aligned with Industry 4.0 and advanced manufacturing environments

-

Educational robots are increasingly being adopted in special education programs to support autism therapy, social interaction development, and individualized learning assistance

-

Cloud-connected robotics platforms are enabling remote content updates, student performance tracking, and subscription-based educational services

-

Affordable robotics kits are expanding access to STEM education by introducing coding, engineering, and robotics concepts to students at an early age across diverse learning environments

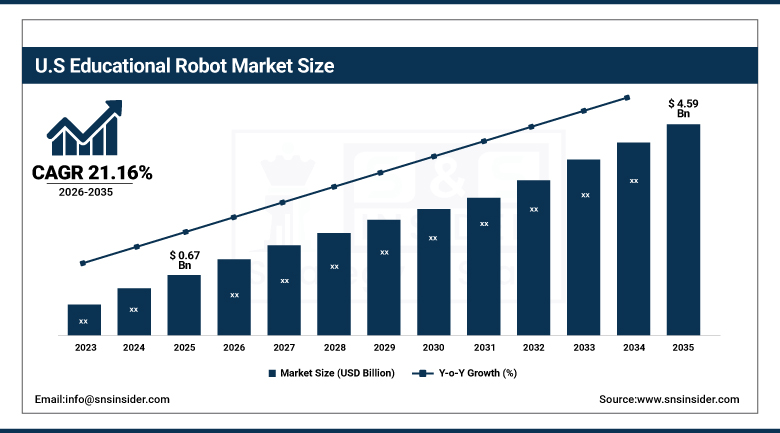

U.S. Educational Robot Market Outlook

The U.S. Educational Robot Market was valued at approximately USD 0.67 Billion in 2025 and is expected to reach approximately USD 4.59 Billion by 2035, growing at a CAGR of approximately 21.16%.

The U.S. is the most commercially significant educational robot market within North America’s dominant revenue position. ROBOTIS, iRobot Education, Wonder Workshop, Sphero, and Boston Dynamics’ education division collectively serve the domestic K-12 and higher education markets. Federal STEM education investment through NSF grants, Department of Education programmes, and state-level CS education mandates collectively create institutional procurement motivation. The U.S. Computer Science for All initiative, FIRST Robotics Competition’s school participation, and university robotics programme’s curriculum investment create the most commercially diverse educational robot deployment of any national market.

SoftBank Robotics expanded its Pepper humanoid robot educational programme in 2024 with new AI-powered social learning curriculum modules for K-12 schools, enabling teachers to deploy Pepper as an interactive coding and social skills teaching assistant. The expanded curriculum’s alignment with Common Core STEM objectives and its differentiated instruction capability for diverse learning needs creates school district procurement motivation whose institutional adoption creates consistent commercial relationships that sustain SoftBank’s educational humanoid programme.

Educational Robot Market Segment Analysis

-

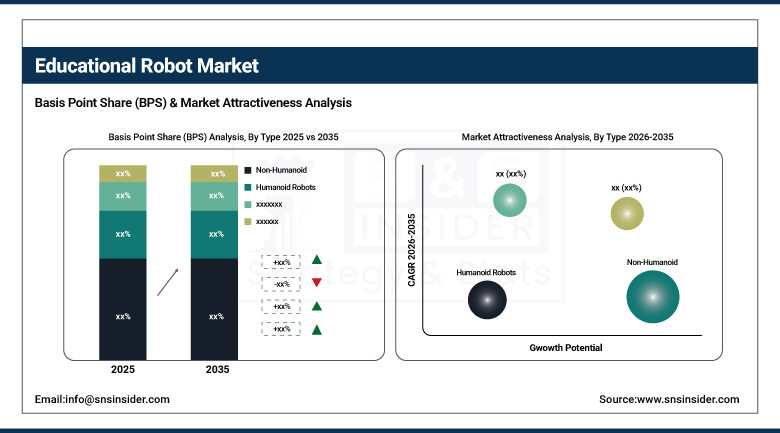

By Type, the Non-Humanoid/Programmable Robots segment dominated the Educational Robot Market with 62% share in 2025, while the Humanoid Robot segment is the fastest growing with a CAGR of 22.67%.

-

By Component, the Hardware segment dominated the Educational Robot Market with 64% share in 2025, while the Software segment is the fastest growing with a CAGR of 22.38%.

-

By Application, the Secondary Education segment dominated the Educational Robot Market with 40% share in 2025, while the Primary Education segment is the fastest growing with a CAGR of 22.79%.

-

By End User, the K-12 Schools segment dominated the Educational Robot Market with approximately 52% share in 2025, while the Higher Education Institutions segment is the fastest growing.

By Type, non-humanoid dominates, humanoid grows fastest

Non-humanoid programmable robots retained the dominant type position with 62% of the educational robot market in 2025. Non-humanoid’s commercial primacy reflects the cost-effectiveness, curriculum versatility, and implementation simplicity that robotic kits including Lego Mindstorms EV3, Makeblock mBot, Sphero BOLT, and ROBOTIS Engineer provide across primary and secondary school STEM programmes. Each robotic kit that enables students to build, programme, and test autonomous behaviour creates experiential coding and engineering learning whose hands-on character creates engagement that software-only alternatives cannot replicate. The broad curriculum alignment of non-humanoid programming robots with computer science, physics, and mathematics objectives creates institutional procurement motivation across diverse subject departments whose combined adoption sustains the type’s dominant commercial position.

Humanoid robots are the fastest-growing type at 22.67% CAGR because AI and machine learning advancement’s progressive improvement of social interaction quality, facial expression recognition, and natural language understanding creates humanoid robot capability whose human-like interaction creates learning engagement that non-humanoid alternatives cannot replicate in social emotional learning, language acquisition, and special education therapeutic contexts. NAO, Pepper, and Sophia’s educational deployments demonstrate the commercial trajectory toward AI-powered humanoid teacher assistants whose social learning facilitation creates institutional adoption motivation that compounds with AI capability improvement.

By Component, hardware dominates, software grows fastest

Hardware retained the dominant component position with 64% of the educational robot market in 2025. The physical robot kit, sensor array, actuator, controller, and communication module’s combined per-unit procurement value creates hardware’s commercial primacy across educational robot deployments. Each school that establishes a robotics programme creates hardware procurement whose robot fleet investment creates initial capital expenditure that substantially exceeds the annual software subscription. The hands-on learning philosophy’s foundational requirement for physical robot interaction, whose tangible feedback creates learning reinforcement that software simulation cannot replicate with equivalent effectiveness, sustains hardware’s dominant commercial position.

Software is the fastest-growing component at 22.38% CAGR because AI-driven adaptive learning platforms, cloud-connected curriculum management, and student progress analytics create software value that compounds with the hardware installed base’s expansion. Each educational robot deployment that connects to a cloud learning management platform creates software subscription procurement whose annual recurring revenue sustains commercial relationships beyond hardware replacement cycles. The progressive shift toward robot-agnostic software platforms that enable consistent curriculum delivery across diverse hardware creates software ecosystem value that sustains above-hardware growth rates.

By Application, secondary education dominates, primary grows fastest

Secondary education retained the dominant application position with 40% of the educational robot market in 2025. Middle school and high school’s STEM curriculum integration depth, the FIRST Robotics Competition’s secondary school participation, and the college preparation motivation that creates student investment in robotics skill development collectively sustain secondary education’s dominant procurement share. Each FIRST Robotics team’s school participation creates robot kit and component procurement whose competition-driven performance motivation creates above-average per-school investment. The secondary education robotics curriculum’s alignment with college admissions’ STEM emphasis creates institutional motivation for investment that sustains commercial relationships.

Primary education is the fastest-growing application at 22.79% CAGR because the global consensus around early STEM exposure’s foundational benefit for technology literacy creates government programme investment that sustains structured primary school robotics procurement. Each government STEM education initiative that funds primary school robotics kit provision creates procurement whose institutional scale compounds with programme coverage expansion. The commercial recognition that early robotics engagement creates lifetime technology confidence whose downstream value sustains investment in primary education robot adoption creates above-average per-student procurement motivation.

By End User, K-12 dominates, higher education grows fastest

K-12 schools retained the dominant end-user position with approximately 52% of the educational robot market in 2025. The K-12 system’s largest institutional scale, encompassing hundreds of thousands of schools globally, creates the most commercially significant aggregate educational robot procurement category. Each school that establishes a robotics lab, robotics club, or curriculum-integrated robotics programme creates hardware and software procurement whose institutional budget creates consistent commercial relationships. Government STEM education mandates’ progressive extension to K-12 robotics curriculum creates structured procurement motivation that sustains above-average institutional adoption growth.

Higher education institutions are the fastest-growing end user because university engineering, computer science, and AI research programmes’ advanced robot deployment creates premium procurement whose per-unit commercial value substantially exceeds K-12 consumer robot alternatives. Each university robotics research laboratory that deploys Boston Dynamics Spot, collaborative robot arms, or humanoid research platforms creates procurement whose research grant funding sustains above-standard technology specification. The workforce readiness programme’s practical industry robot training creates structured higher education procurement whose corporate partnership funding creates additional institutional investment motivation.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Educational Robot Market Insights

North America dominated the global educational robot market in 2025 as the region with the most commercially advanced STEM education infrastructure and highest per-student educational technology investment. The United States accounts for approximately 87.4% of North American revenues through ROBOTIS, Sphero, Wonder Workshop, and Boston Dynamics Education’s commercial operations, and federal STEM education programme funding that creates structured institutional procurement.

Canada contributes approximately 12.6% of North American revenues through its provincial curriculum robotics investment, university research programme’s advanced robot deployment, and the growing K-12 coding and robotics mandate that creates institutional procurement.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Educational Robot Market Insights

Europe is a technically sophisticated educational robot market where EU Horizon research programme’s robotics investment, LEGO Education’s Danish heritage, and the European robotics industry’s STEM workforce development motivation create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its engineering education tradition, KUKA and ABB’s educational robot programme, and the vocational training system’s industrial robot integration.

France, the United Kingdom, and Sweden are significant secondary markets where national digital education strategies, university robotics research, and K-12 coding curricula create consistent educational robot procurement.

Asia Pacific Educational Robot Market Insights

Asia Pacific is the fastest-growing regional educational robot market, driven by China’s extraordinary robotics education investment, Japan’s advanced robot culture creating above-average school adoption, South Korea’s technology education emphasis, and India’s rapidly expanding STEM education programme. China accounts for approximately 44.8% of Asia Pacific revenues through government AI and robotics curriculum integration, extraordinary primary and secondary school market scale, and the domestic educational robot manufacturer development.

South Korea’s government robotics education programme, Japan’s school robot adoption, and India’s rapidly growing EdTech market create significant secondary markets whose combined procurement reinforces Asia Pacific’s fastest-growing regional status.

MEA & Latin America Educational Robot Market Insights

UAE leads MEA revenues at approximately 38.4% through its extraordinary education technology investment, Mohammed bin Rashid Al Maktoum Global Initiatives’ STEM programme, and the government’s Future Skills initiative creating structured educational robot procurement. Brazil leads Latin American revenues at approximately 44.2% through its growing STEM education awareness, university research programme, and the government’s digital education transformation investment.

Saudi Arabia’s Vision 2030 education technology programme and South Africa’s STEM education initiative create significant MEA secondary markets whose educational robot procurement reflects the progressive governmental investment in technology-enabled learning.

Market Dynamics

Growth Drivers: Global STEM education emphasis and AI-powered personalised learning creating premium educational robot adoption

Rising global emphasis on STEM education is the educational robot market’s most commercially certain structural growth driver. Governments worldwide’s recognition that STEM competency creates national economic competitiveness creates legislation, curriculum mandate, and funding that sustains educational robot procurement across diverse economic contexts. Each national STEM education programme that specifies robotics as a curriculum component creates institutional procurement motivation whose aggregate across progressively more STEM-committed national education systems creates commercial scale. The OECD’s documentation that countries with stronger STEM education investment create above-average productivity growth creates policy motivation that sustains government educational robot funding.

AI-powered personalised learning robot’s ability to adapt instruction to individual student learning pace, comprehension level, and engagement pattern creates educational outcome improvement that standardised classroom instruction cannot replicate at equivalent personalisation. Each student whose AI robot interaction adapts to learning needs creates measurable academic outcome improvement whose evidence sustains institutional adoption motivation beyond technology novelty. The special education sector’s therapeutic robot benefit for autism spectrum disorder social skills development creates structured healthcare-education procurement that sustains above-average premium segment growth.

Restraints: High procurement cost limiting access in resource-constrained school systems and teacher training investment requirement

Premium educational robot systems’ procurement cost, ranging from USD 500 for basic kits through USD 10,000-50,000 for humanoid and advanced collaborative robot systems, creates access barriers for school districts whose technology budget cannot accommodate comprehensive robotics programme investment. Each school whose annual technology allocation cannot fund robotics programme creates market limitation that government subsidy, charitable programme, and corporate partnership must address to sustain adoption beyond well-resourced educational institutions.

Teacher training’s requirement for effective educational robot deployment creates implementation barriers whose professional development investment moderates adoption pace. Each school that acquires educational robots without adequate teacher training creates underutilisation whose programme ineffectiveness creates institutional motivation to not expand investment, creating adoption constraint that requires concurrent teacher development support.

Opportunities: AI teacher assistant humanoid deployment and corporate STEM partnership programme

AI teacher assistant humanoid deployment represents the most commercially transformative near-term opportunity whose conversational AI’s improvement of natural language understanding creates robot capability approaching genuine instructional effectiveness. Each humanoid robot that assists human teachers in differentiating instruction, monitoring student engagement, and providing immediate feedback creates institutional adoption motivation whose labour augmentation value sustains premium procurement.

Corporate STEM partnership programme represents the most commercially scalable funding mechanism for educational robot market development beyond government procurement. Each technology company, manufacturing firm, or automation operator that partners with school districts to provide educational robot equipment in exchange for workforce pipeline development creates procurement whose corporate sustainability and workforce development motivation sustains investment beyond educational budget cycle variation.

Recent Developments:

-

2023: ABB Robotics launched a complete robot training package in July 2023 including the GoFa collaborative robot cell, 56 hours of teaching materials, and globally recognised STEM certification to prepare students for future automated workplaces and close the automation skills gap.

-

2024: SoftBank Robotics expanded its Pepper humanoid robot educational programme in 2024 with new AI-powered social learning curriculum modules for K-12 schools enabling interactive coding and social skills instruction aligned with Common Core STEM objectives.

-

2024: LEGO Education launched the SPIKE Essential set in 2024 designed specifically for primary school coding and robotics introduction, providing curriculum-aligned building and programming activities that enable teachers without robotics background to deploy hands-on STEM learning.

Educational Robot Market Key Players

-

LEGO Education (The LEGO Group)

-

Softbank Robotics (NAO, Pepper)

-

Makeblock Co., Ltd.

-

ROBOTIS Inc.

-

Wonder Workshop Inc. (Dash & Dot)

-

Sphero Inc.

-

ABB Robotics (GoFa Education)

-

KUKA AG (Education Cells)

-

Boston Dynamics Inc. (Spot EDU)

-

Hanson Robotics (Sophia)

-

PAL Robotics

-

Modular Robotics (Cubelets)

-

Fischertechnik GmbH

-

Aldebaran Robotics (SoftBank)

-

RoboKind (Milo)

-

Ozobot (Evollve Inc.)

-

Learning Resources Ltd.

-

iRobot Education (iRobot Corp.)

-

Thymio (EPFL/ECAL)

-

CMU Robotics Academy

Educational Robot Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 2.03 Billion |

| Market Size by 2035 | USD 13.87 Billion |

| CAGR | CAGR of 21.34% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Type (Non-Humanoid/Programmable Robots & Robotic Kits, Humanoid Robots) • by Component (Hardware, Software, Services) • by Application (Primary Education, Secondary Education, Higher Education, Special Education) • by End User (K-12 Schools, Higher Education Institutions, Research & Training Centres, Corporate Training) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | LEGO Education, Softbank Robotics, Makeblock Co., Ltd., ROBOTIS Inc., Wonder Workshop Inc., Sphero Inc., ABB Robotics, KUKA AG, Boston Dynamics Inc., Hanson Robotics, PAL Robotics, Modular Robotics, Fischertechnik GmbH, Aldebaran Robotics, RoboKind, Ozobot , Learning Resources Ltd., iRobot Education, Thymio, CMU Robotics Academy |

Frequently Asked Questions

The Educational Robot Market is expected to grow at a CAGR of 21.34% from 2026 to 2035.

The Educational Robot Market was valued at USD 2.03 Billion in 2025.

Rising global emphasis on STEM education with government curriculum investment, and AI-powered personalised learning robots.

Non-Humanoid/Programmable Robots dominated the Educational Robot Market with 62% share in 2025, while the Humanoid segment is the fastest growing with a CAGR of 22.67%.

Secondary Education dominated the Educational Robot Market with 40% share in 2025, while Primary Education is the fastest growing with a CAGR of 22.79%.

Get in Touch