Preclinical Imaging Market Report Scope & Overview:

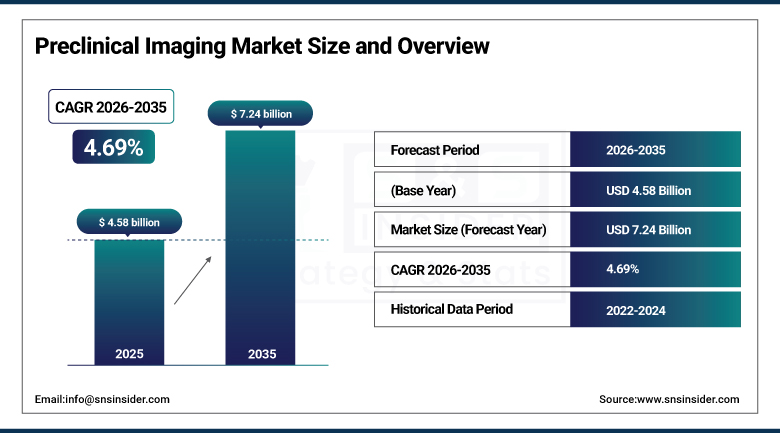

The Preclinical Imaging Market was valued at USD 4.58 Billion in 2025 and is expected to reach USD 7.24 Billion by 2035, growing at a CAGR of 4.69% from 2026–2035.

The global preclinical imaging market is growing at a sustained and commercially significant pace. Preclinical imaging encompasses non-invasive and minimally invasive imaging technologies applied to animal models before human clinical trials, enabling researchers to track disease progression, evaluate drug efficacy, monitor gene expression, characterize biological processes at molecular and cellular levels, and optimize lead compound selection during drug discovery. The market is expected to witness consistent growth because of increased investments in research and development, advancements in imaging systems technology, and increasing demand for non-invasive techniques in drug discovery and disease research. The use of multimodal imaging and growth in preclinical studies in oncology and neurology also contribute to market growth in pharmaceutical and biotechnology industries.

In March 2023, Cyceron in Caen, France, installed a Momentum CT Magnetic Particle Imaging (MPI) system to advance preclinical studies on inflammatory diseases including Multiple Sclerosis and Crohn’s Disease. This cutting-edge MPI technology provides highly sensitive in vivo imaging of previously undetectable pathological processes, enabling rigorous testing of imaging protocols and cell therapies. The installation demonstrates the research institution’s commercial investment in next-generation preclinical modalities whose sensitivity advantage over conventional MRI creates new disease mechanism characterization capability.

Market Size and Forecast

-

Market Size in 2026E: USD 4.80 Billion

-

Market Size by 2035: USD 7.24 Billion

-

CAGR: 4.69% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get more information on Preclinical Imaging Market - Request Free Sample Report

Preclinical Imaging Market Trends

-

AI-powered image analysis is automating biomarker quantification, tumor volume measurement, and longitudinal study tracking, significantly improving throughput and reducing manual interpretation requirements.

-

Multimodal imaging platforms integrating PET/CT, PET/MRI, and SPECT/CT are gaining adoption by providing comprehensive anatomical, functional, and molecular imaging data within a single workflow.

-

Magnetic Particle Imaging (MPI) is emerging as a promising modality for nanoparticle tracking and real-time 3D imaging, enabling advanced vascular imaging and cell-tracking research applications.

-

Growing adoption of 3Rs (Replacement, Reduction, Refinement) research principles is increasing demand for longitudinal imaging techniques that reduce animal usage while enhancing study accuracy and statistical reliability.

-

Expansion of organoid, tissue-engineering, and ex vivo imaging applications is creating new opportunities for micro-CT, optical coherence tomography, and advanced microscopy systems in preclinical research.

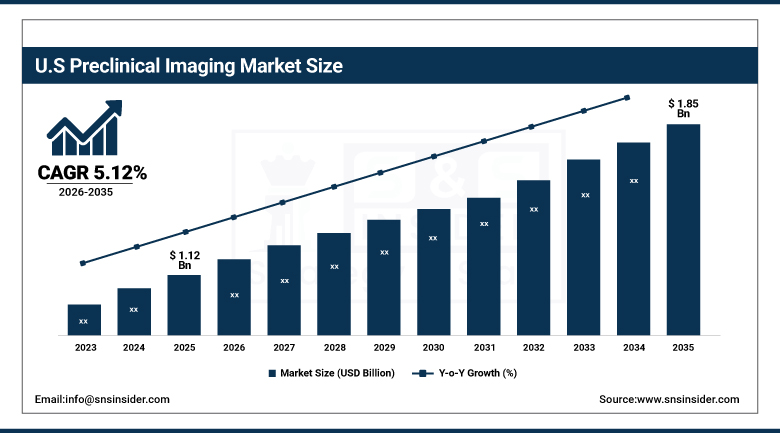

The U.S. Preclinical Imaging Market Outlook

The U.S. preclinical imaging market was valued at USD 1.12 Billion in 2025, is expected to reach USD 1.85 by 2035 at CAGR of 5.12%, with consistent growth driven by extraordinary pharmaceutical R&D investment, NIH funding, and the concentration of academic medical centres and CRO infrastructure.

The U.S. is the most commercially significant preclinical imaging market globally. Bruker Corporation, PerkinElmer, Mediso, MR Solutions, and Siemens Healthineers’ preclinical division collectively define the domestic commercial landscape. The NIH’s annual research funding exceeding USD 45 billion, the extraordinary U.S. pharmaceutical and biotechnology R&D investment, and the concentration of NCI-designated cancer centres whose oncology research creates preclinical imaging procurement collectively create the most commercially significant national market. FDA’s drug approval pathway’s preclinical safety and efficacy evidence requirement creates structured institutional demand.

Bruker Corporation expanded its preclinical imaging portfolio in 2024 with the BioSpec 21.1T ultra-high field MRI system for rodent brain imaging, providing unprecedented neuroanatomical resolution that enables cortical layer-specific imaging, white matter tract characterization, and functional connectivity mapping whose research application sustains premium procurement from neuroscience-focused research institutions and pharmaceutical companies with central nervous system drug development programmes.

Preclinical Imaging Market Segment Analysis

-

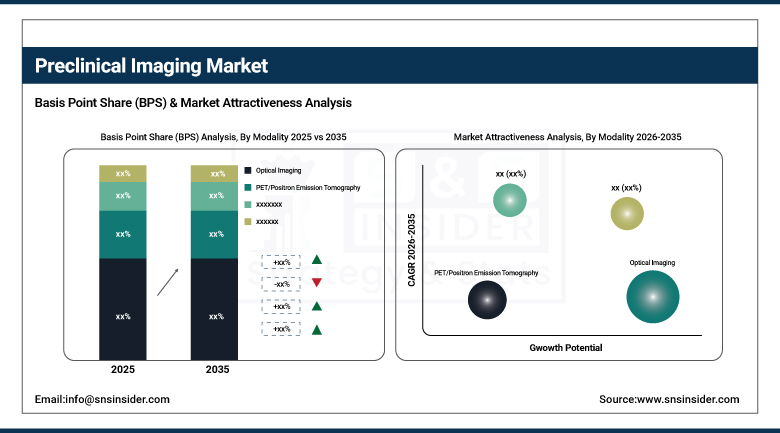

By Modality, optical imaging segment dominated the preclinical imaging market with 11.9% share in 2025, while the multimodal/hybrid imaging segment is expected to see the most rapid growth.

-

By Application, research & development segment dominated the preclinical imaging market with the highest revenue share in 2025, while the drug discovery & development segment is the fastest growing as the pharmaceutical industry’s progressive shift toward imaging biomarker-guided.

-

By End User, pharmaceutical & biotechnology companies segment dominated the preclinical imaging market with 35.9% share in 2025, while the research institutes & academic centres segment is expected to grow at the fastest pace.

By Modality, optical imaging dominates, multimodal grows fastest

Optical imaging retained the dominant modality position with 11.9% of the preclinical imaging market in 2025. Optical imaging’s commercial primacy reflects its position as the most accessible, cost-effective, and real-time molecular imaging modality whose bioluminescence and fluorescence imaging creates molecular process visualization accessible to the broadest range of research institutions. Bioluminescence imaging’s ability to track reporter gene expression, monitor tumor progression, and quantify cell engraftment in live animal models creates experimental design capability that non-molecular modalities cannot provide equivalently. PerkinElmer’s IVIS Spectrum, Bruker’s In-Vivo Xtreme, and Spectral Instruments Imaging’s Ami series collectively demonstrate the commercial ecosystem whose instrument portfolio creates institutional procurement.

Multimodal imaging is the fastest-growing modality because the research community’s progressive recognition that no single imaging modality provides all required information simultaneously creates systematic hybrid system adoption. PET/CT’s simultaneous metabolic and anatomical imaging for oncology, PET/MRI’s radiotracer distribution with soft tissue contrast, and SPECT/CT’s scintigraphic function with morphological context create research quality that sequential single-modality imaging cannot match. Each new hybrid system installation that creates multi-dimensional dataset quality creates research output improvement whose publication impact creates institutional adoption motivation.

By Application, R&D dominates, drug discovery grows fastest

Research and development retained the dominant application position in the preclinical imaging market in 2025. R&D’s commercial primacy reflects the preclinical imaging market’s foundational character as a research tool whose primary deployment context is academic and government-funded investigation of disease mechanisms, biological processes, and imaging technology development. Each NIH-funded grant that includes preclinical imaging as a core methodology creates institutional procurement whose aggregate across the extraordinary U.S. and global research grant ecosystem creates commercial scale. The academic medical centre’s longitudinal disease model characterization, biomarker validation study, and imaging contrast agent evaluation collectively create R&D application’s dominant market position.

Drug discovery and development is the fastest-growing application because the pharmaceutical industry’s progressive adoption of imaging biomarkers as efficacy endpoints in preclinical studies creates structured commercial growth that compounds with each new drug programme’s imaging-guided compound selection and dose optimization. Each oncology drug programme that uses tumor volume response as a preclinical efficacy endpoint creates optical imaging or PET procurement whose per-study commercial value reflects the imaging protocol’s complexity and time-point frequency.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

Israel |

31.2% |

|

Latin America |

Brazil |

44.2% |

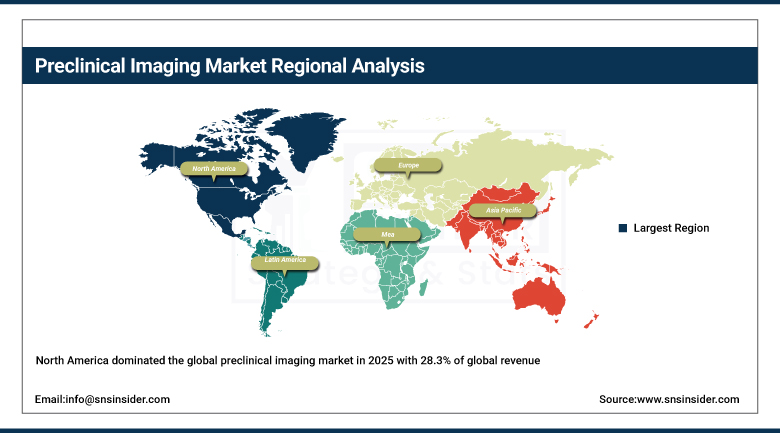

North America Preclinical Imaging Market Insights

North America dominated the global preclinical imaging market in 2025 with 28.3% of global revenue, driven by strong R&D investments, established pharmaceutical companies, and early adoption of advanced imaging technologies. The United States accounts for approximately 87.4% of North American revenues through Bruker, PerkinElmer, and the extraordinary concentration of NIH-funded research infrastructure.

Canada contributes approximately 12.6% of North American revenues through its NRC research programme, university medical research infrastructure, and the growing CRO sector’s preclinical imaging service procurement.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Preclinical Imaging Market Insights

Europe is a technically sophisticated preclinical imaging market where the European Research Council’s Horizon programme funding, Siemens Healthineers’ and Bruker’s European leadership, and the pharmaceutical industry’s Basel-to-Munich research corridor create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its pharmaceutical sector’s preclinical imaging investment, Max Planck Institute research programme, and Bruker’s Ettlingen headquarters proximity.

France, the United Kingdom, and Sweden are significant secondary markets where academic medical centre’s preclinical research, pharmaceutical company’s drug discovery programme, and CRO sector’s imaging service create consistent procurement.

Asia Pacific Preclinical Imaging Market Insights

Asia Pacific is the fastest-growing regional preclinical imaging market, driven by China’s extraordinary pharmaceutical R&D investment, Japan’s advanced preclinical research infrastructure, South Korea’s growing biotech sector, and India’s rapidly expanding CRO industry. China accounts for approximately 44.8% of Asia Pacific revenues through its government-funded biomedical research programme, domestic pharmaceutical company’s preclinical imaging investment, and the growing CRO sector’s imaging service procurement.

Japan’s advanced academic medical centre research infrastructure, South Korea’s biotech industry’s preclinical imaging adoption, and Australia’s research institution’s government-funded imaging programme create significant secondary markets.

MEA & Latin America Preclinical Imaging Market Insights

Israel leads MEA revenues through its extraordinary biotech research community, Weizmann Institute’s preclinical imaging programme, and the pharmaceutical sector’s drug development investment. Brazil leads Latin American revenues through its FAPESP-funded biomedical research programme, the growing CRO sector’s service capacity, and the pharmaceutical industry’s growing domestic research investment.

Market Dynamics

Growth Drivers: Increasing pharmaceutical R&D investment and demand for non-invasive preclinical imaging techniques

Increased investments in research and development, advancements in imaging systems technology, and increasing demand for non-invasive techniques in drug discovery and disease research are the preclinical imaging market’s most commercially certain structural growth drivers. The global pharmaceutical industry’s annual R&D investment exceeding USD 250 billion creates the financial foundation whose preclinical stage imaging component sustains consistent market procurement. Each new IND application whose preclinical pharmacology and toxicology evidence package includes imaging data creates procurement that compounds with the pharmaceutical pipeline’s growth. The FDA’s progressive endorsement of imaging biomarkers as surrogate endpoints creates regulatory motivation for imaging adoption that sustains procurement beyond research curiosity.

The use of multimodal imaging and growth in preclinical studies in oncology and neurology contribute significantly to market growth. Oncology’s tumor response imaging requirement and neurology’s longitudinal neurodegeneration monitoring create above-average per-study imaging procurement whose combined therapeutic area scale creates commercial momentum that sustains preclinical imaging market growth.

Restraints: High instrument acquisition cost and specialized technical operation requirement

Preclinical imaging instrument’s high acquisition cost, ranging from USD 200,000 for optical imaging systems through USD 2-5 million for hybrid PET/MRI and high-field MRI, creates capital investment barriers for smaller research institutions and emerging market universities whose equipment budget cannot accommodate premium system specification. Each institution whose capital budget creates single-modality specification motivation creates commercial limitation that moderates the hybrid system market’s adoption pace.

Specialized technical operation requirement, whose radiochemistry for PET imaging, radiofrequency coil selection for MRI, and image reconstruction expertise create human capital investment alongside instrument acquisition, moderates adoption in research environments without dedicated preclinical imaging staff.

Opportunities: AI-assisted image analysis and CRO outsourced imaging service expansion

AI-powered preclinical image analysis software represents the most commercially transformative near-term opportunity whose automated segmentation, biomarker quantification, and longitudinal change detection create analysis throughput that manual expert analysis cannot match at equivalent scale. Each pharmaceutical company that adopts AI-assisted preclinical imaging analysis creates software procurement whose per-study commercial value sustains recurring revenue.

CRO outsourced preclinical imaging service expansion represents the most commercially scalable market development opportunity whose pharmaceutical company’s asset-light outsourcing strategy creates structured service procurement from specialized imaging CROs whose equipment investment and operational expertise create commercial relationships that sustain above-average market growth.

Recent Developments:

-

2024: Bruker Corporation expanded its preclinical imaging portfolio in 2024 with the BioSpec 21.1T ultra-high field MRI system for rodent brain imaging, providing unprecedented neuroanatomical resolution for cortical layer-specific imaging and functional connectivity mapping in CNS drug development research.

-

2024: PerkinElmer (Revvity) launched enhanced IVIS Lumina Series X preclinical optical imaging system in 2024 with improved sensitivity, expanded spectral unmixing capability, and cloud-connected data management for multicenter preclinical studies whose longitudinal bioluminescence and fluorescence imaging data requires centralized analysis platform integration.

-

2023: Cyceron in Caen, France installed a Momentum CT Magnetic Particle Imaging (MPI) system in March 2023 to advance preclinical studies on inflammatory diseases including Multiple Sclerosis and Crohn’s Disease, demonstrating MPI technology’s highly sensitive in vivo imaging capability for previously undetectable pathological processes.

Preclinical Imaging Market Key Players are:

-

PerkinElmer Inc. (Revvity)

-

Bruker Corporation

-

Siemens Healthineers AG

-

GE HealthCare Technologies Inc.

-

FUJIFILM VisualSonics Inc.

-

MR Solutions Ltd.

-

Miltenyi Biotec B.V. & Co. KG

-

Mediso Ltd.

-

Aspect Imaging Ltd.

-

TriFoil Imaging Inc.

-

Scanco Medical AG

-

BioSpace Lab S.A.S.

-

LI-COR Biosciences, Inc.

-

Photon etc. Inc.

-

Rigaku Corporation

-

Canon Medical Systems Corporation

-

Agilent Technologies, Inc.

-

Thermo Fisher Scientific Inc.

-

Shimadzu Corporation

-

SMI (Sofie Molecular Imaging) Inc.

Preclinical Imaging Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 4.58 Billion |

| Market Size by 2035 | USD 7.24 Billion |

| CAGR | CAGR of 4.69% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Modality (Optical Imaging/Bioluminescence & Fluorescence Imaging, PET/Positron Emission Tomography, SPECT, MRI, CT, Ultrasound, Photoacoustic Imaging, Multimodal/Hybrid Imaging Systems) • By Application (Research & Development, Drug Discovery & Development, Toxicology Studies, Disease Mechanism Studies, Oncology Research, Neurology Research, Others) • By End User (Pharmaceutical & Biotechnology Companies, Research Institutes & Academic Centres, Contract Research Organizations, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | PerkinElmer Inc. (Revvity), Bruker Corporation, Siemens Healthineers AG, GE HealthCare Technologies Inc., FUJIFILM VisualSonics Inc., MR Solutions Ltd., Miltenyi Biotec B.V. & Co. KG, Mediso Ltd., Aspect Imaging Ltd., TriFoil Imaging Inc., Scanco Medical AG, BioSpace Lab S.A.S., LI-COR Biosciences, Inc., Photon etc. Inc., Rigaku Corporation, Canon Medical Systems Corporation, Agilent Technologies, Inc., Thermo Fisher Scientific Inc., Shimadzu Corporation, and SMI (Sofie Molecular Imaging) Inc. |

Frequently Asked Questions

The Preclinical Imaging Market was valued at USD 4.58 Billion in 2025.

Increased investments in research and development, advancements in imaging systems technology, and increasing demand for non-invasive techniques in drug discovery and disease research contributing to market growth.

Optical Imaging dominated the Preclinical Imaging Market with 11.9% share in 2025.

North America dominated the global preclinical imaging market in 2025 with 28.3% of global revenue.

Get in Touch