Electronic Medical Record (EMR) Systems Market Report Scope & Overview:

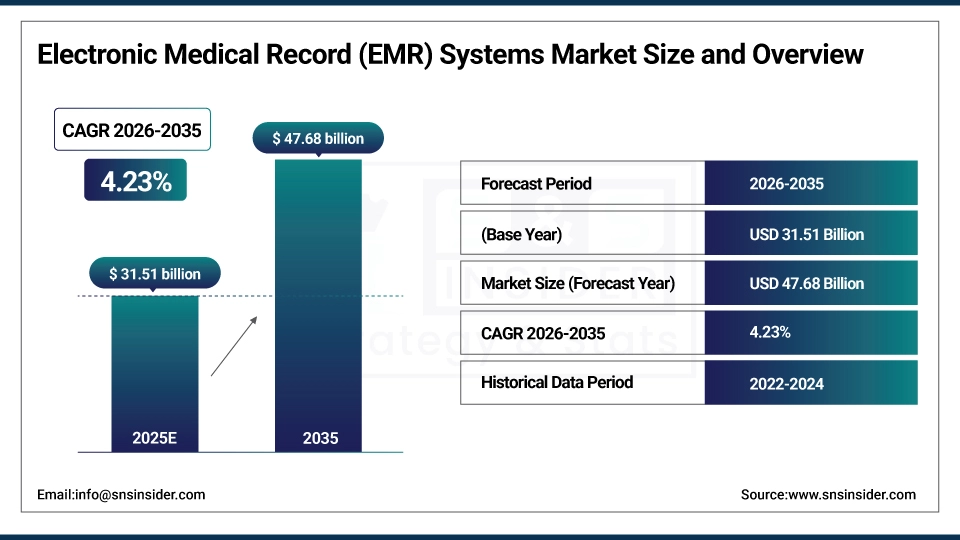

The Electronic Medical Record (EMR) Systems Market size was valued at USD 31.51 billion in 2025 and is expected to reach USD 47.68 billion by 2035, growing at a CAGR of 4.23% over the forecast period of 2026-2035.

The global electronic medical record systems market trend is a growing demand for digital health documentation solutions such as specialty EMR platforms, cloud-based clinical data management systems, and integrated healthcare IT infrastructure. Also driven by a growing adoption of value-based care reimbursement models and the growing focus on reducing clinical documentation errors and administrative overhead as healthcare providers become more focused on improving operational efficiency and are more willing to invest in advanced EMR software and services, resulting in growth in the domestic and international market for both on-premise and cloud-based electronic medical record system deployments across small, medium, and large hospital settings.

Electronic Medical Record (EMR) Systems Market Size and Forecast:

-

Market Size in 2025: USD 31.51 billion

-

Market Size by 2035: USD 47.68 billion

-

CAGR: 4.23% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Electronic Medical Record (EMR) Systems Market - Request Free Sample Report

Electronic Medical Record (EMR) Systems Market Trends

-

EMR system solutions are being adopted because hospitals and physician practices demand faster clinical documentation, streamlined patient record management, and seamless integration with laboratory and imaging systems.

-

Customized specialty EMR platforms based on clinical workflows, treatment protocols, and specialty-specific documentation requirements to improve care outcomes and reduce physician burnout.

-

The development of AI-powered clinical documentation assistants, voice recognition tools, and ambient charting solutions to improve physician efficiency and reduce manual data entry burden across hospital settings.

-

Interoperability frameworks, HL7 FHIR-based data exchange standards, and patient data sharing networks are all available to ensure continuous care coordination and accurate medical history transfer across provider networks.

-

Increased demand for cloud-based EMR deployments, mobile-responsive clinical interfaces, and software-as-a-service models to help lower implementation costs and improve system scalability for hospitals of all sizes.

-

Collaboration between EMR vendors, health IT integrators, and payer organizations to develop connected clinical record ecosystems and improve standards of data interoperability and care transition documentation.

-

ONC, CMS, and Joint Commission promoting standards for data privacy, HIPAA compliance, meaningful use requirements, and clinical documentation integrity across certified EMR platforms.

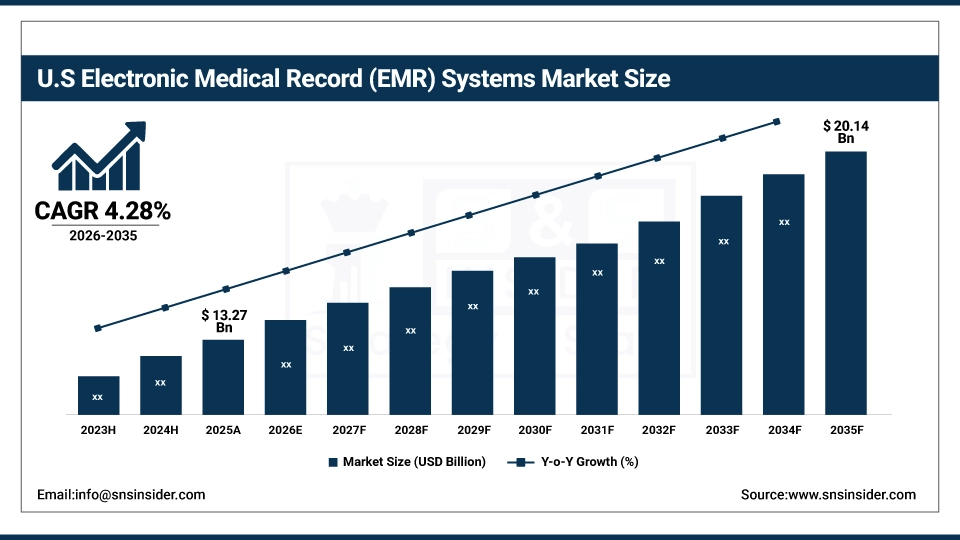

The U.S. Electronic Medical Record (EMR) Systems Market was valued at USD 13.27 billion in 2025 and is expected to reach USD 20.14 billion by 2035, growing at a CAGR of 4.28% from 2026-2035. The United States represents the largest market for electronic medical record systems, primarily driven by near-universal EHR/EMR adoption mandates, federal laws facilitating interoperable patient data access, and well-developed healthcare IT infrastructure across large and community hospital networks. Also, the U.S. is the largest regional market in the world, due to the regulatory support and swift adoption of cloud-based and AI-integrated electronic medical record solutions.

Electronic Medical Record (EMR) Systems Market Growth Drivers:

-

Government Mandates and Regulatory Support is Driving the Electronic Medical Record (EMR) Systems Market Growth

Government mandates and regulatory support take the center stage as a growth driver for the electronic medical record systems market share, and are driven by the implementation of meaningful use criteria, 21st Century Cures Act interoperability provisions, and HIPAA regulations for expanded patient data accessibility and clinical documentation transparency. These requirements for healthcare digitization and care record standardization are expanding the base of the market, the penetration of cloud-based and specialty EMR platforms, and adding to the overall market share globally.

For instance, in June 2024, cloud-based and certified EMR systems accounted for ~64% of the total U.S. hospital technology investments in clinical documentation infrastructure, reflecting growing institutional preference and expanding market share.

Electronic Medical Record (EMR) Systems Market Restraints:

-

High Implementation Costs and Physician Adoption Challenges are Hampering the Electronic Medical Record (EMR) Systems Market Growth

High implementation costs and physician adoption challenges of electronic medical record systems also restrict the electronic medical record systems market growth, as a large number of small and medium-sized hospitals that have deployed EMR platforms face difficulties with system customization, workflow disruption, and physician resistance to digital documentation processes. This might lead to underutilization, increased administrative burden on clinical staff, and reduced return on investment for healthcare organizations. As a result, patient record accuracy suffers, and market growth is stunted in regions where rural hospital IT budgets are constrained and physician digital literacy remains limited.

Electronic Medical Record (EMR) Systems Market Opportunities:

-

AI-Powered Clinical Documentation and Cloud Migration Drive Future Growth Opportunities for the Electronic Medical Record (EMR) Systems Market

The opportunity in AI-powered clinical documentation and cloud migration in the electronic medical record systems market is in the form of ambient charting solutions, automated coding suggestions, and real-time clinical decision prompts embedded within EMR workflows. These solutions provide for reduced physician documentation time, improved coding accuracy for revenue cycle management, and real-time patient data synchronization across care settings. Through enhanced clinical efficiency, reduced physician burnout rates, and lower total cost of ownership for cloud-based deployments, particularly in small and medium-sized hospital segments with limited on-premise IT resources, these technologies may improve documentation quality, accelerate cloud adoption, and expand the market.

For instance, in April 2024, the ONC reported that 78% of U.S. non-federal acute care hospitals were actively using certified electronic medical record systems, highlighting the near-saturated platform availability and increasing demand for next-generation EMR upgrades and specialty-focused documentation tools.

Electronic Medical Record (EMR) Systems Market Segment Analysis

-

By type, general EMR solutions held the largest share of around 61.43% in 2025, and the specialty EMR solutions segment is expected to register the highest growth with a CAGR of 4.89%.

-

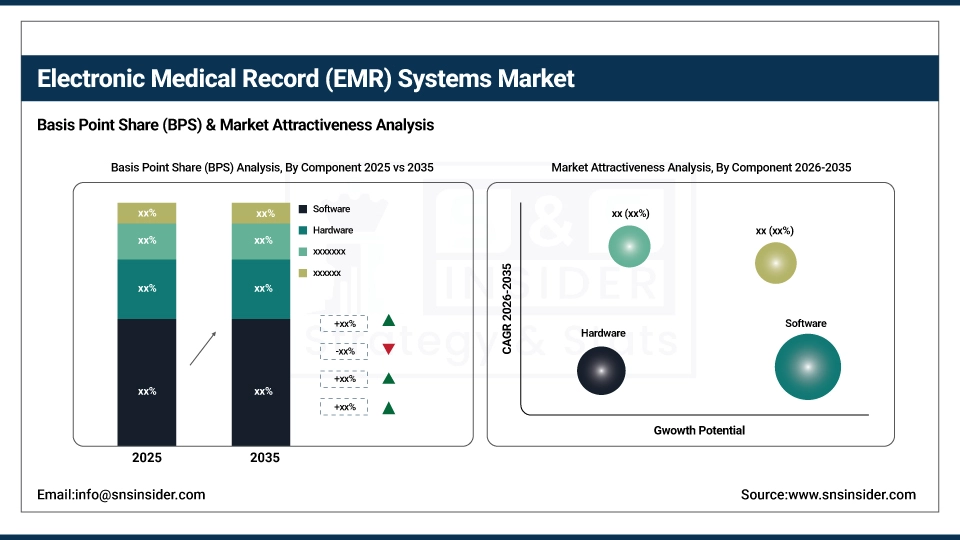

By component, the software segment dominated the market with approximately 54.76% share in 2025E, while the services segment is expected to register the highest growth with a CAGR of 4.61%.

-

By hospital size, large hospitals accounted for the leading share of nearly 58.32% in 2025E, and the small and medium-sized hospitals segment is expected to register the highest growth with a CAGR of 4.94%.

-

By delivery mode, the cloud-based segment dominated the market with approximately 52.18% share in 2025E, while the on-premise segment is expected to maintain steady adoption among large hospital systems with complex integration requirements.

By Component, Software Dominates, while Services Segment Shows Rapid Growth

By 2025, the software segment contributed the largest revenue share of 54.76% due to continuous upgrades in clinical documentation modules, AI-powered charting tools, and integrated patient data management capabilities that drive consistent licensing and subscription revenues for EMR vendors. Growing adoption of software-as-a-service models coupled with cloud migration trends, providers are increasingly shifting toward subscription-based EMR software that lowers upfront capital expenditure.

The services segment is projected to grow at the highest CAGR of about 4.61% between 2026 and 2035 due to the growing need for implementation support, staff training, system customization, and ongoing maintenance across hospitals upgrading to next-generation EMR platforms. Some of the reasons include increasing complexity of EMR migrations, growing demand for interoperability consulting, and healthcare organizations' preference for managed service models that reduce in-house IT dependency.

By Type, General EMR Solutions Lead the Market, While Specialty EMR Solutions Register Fastest Growth

The general EMR solutions segment accounted for the highest revenue share of approximately 61.43% in 2025, owing to widespread hospital adoption of standardized clinical documentation platforms, strong integration capabilities with laboratory, pharmacy, and radiology systems, and healthcare provider preference for unified record management environments. Emerging trends, including increasing requirements for consolidated patient documentation workflows and regulatory emphasis on clinical data continuity across care transitions.

The specialty EMR solutions segment is anticipated to achieve the highest CAGR of nearly 4.89% during the 2026–2035 period, driven by the increasing demand from oncology, cardiology, orthopedics, ophthalmology, and behavioral health practices for condition-specific documentation templates, workflow customization, and specialty billing modules. Drivers include rising adoption among independent specialty physician groups, the preference for purpose-built clinical charting features, and the growing shift of specialty care toward ambulatory and outpatient settings that require tailored EMR capabilities.

By Hospital Size, Large Hospitals Lead, and Small and Medium-sized Hospitals Register Fastest Growth

Large hospitals accounted for the largest share of the electronic medical record systems market with about 58.32%, owing to their higher IT investment capacity, complex multi-department documentation requirements, and early adoption of enterprise-grade EMR platforms with advanced analytics and revenue cycle integration. Reasons driving the large hospital segment include increasing regulatory reporting obligations, growing patient volumes requiring scalable documentation infrastructure, and direct incentives tied to Promoting Interoperability performance metrics.

The small and medium-sized hospitals segment is slated to grow at the fastest rate with a CAGR of around 4.94% throughout the forecast period of 2026–2035, as community hospitals, critical access facilities, and independent practices seek affordable cloud-based and vendor-hosted EMR solutions that reduce upfront hardware investment. Increased availability of modular and scalable EMR platforms contribute to their adoption, while improved vendor support and lower total cost of ownership for cloud deployments drive continued investment.

Electronic Medical Record (EMR) Systems Market Regional Highlights:

North America Electronic Medical Record (EMR) Systems Market Insights:

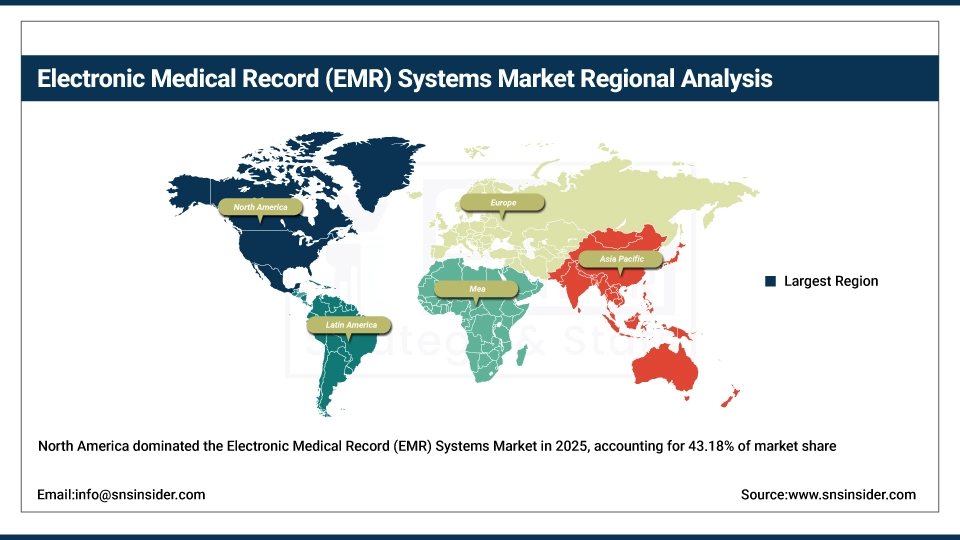

North America held the largest revenue share of over 43.18% in 2025 of the electronic medical record systems market due to an established health IT ecosystem, stringent federal requirements for certified EMR adoption, and increased provider awareness regarding the clinical and financial advantages of digital medical record management. Drivers include near-universal acute care hospital EMR penetration, improved broadband network infrastructure, growing physician demand for mobile-accessible documentation tools, and greater institutional commitment to interoperability following 21st Century Cures Act enforcement. At the same time, various government incentives, Promoting Interoperability requirements, and enormous investments in healthcare IT from hospital systems and physician organizations are anchoring EMR software and services in the market, and ensuring multibillion dollar revenues around the world.

Get Customized Report as per Your Business Requirement - Enquiry Now

Asia Pacific Electronic Medical Record (EMR) Systems Market Insights:

Asia Pacific is the fastest-growing segment in the electronic medical record systems market with a CAGR of 5.42%, as the awareness about digital health record management, government hospital digitization programs, and healthcare IT infrastructure modernization in countries such as China, India, Japan, South Korea, and Australia is growing. Factors including rapid expansion of private hospital chains, rising middle-class population with growing health insurance coverage, and increasing uptake of cloud-based clinical management systems are stimulating the market growth. National eHealth initiatives and government-sponsored EMR adoption programs have been instrumental in improving clinical documentation standards, especially in semi-urban and rural hospital networks. Public-private partnerships and regional health IT funding programs also help in advancing healthcare delivery digitization and EMR platform expansion. Increase in demand in the Asia Pacific region owing to rising healthcare expenditure against historical spending levels and growing affordability and accessibility of cloud-hosted EMR solutions across small and medium-sized hospital facilities.

Europe Electronic Medical Record (EMR) Systems Market Insights:

The electronic medical record systems market in Europe is the second-dominating region after North America on account of an increase in the adoption of electronic health records, robust data protection regulations including GDPR, and increasing national digital health strategies across Germany, the UK, France, the Netherlands, and the Nordic countries. Rising implementation of the European Health Data Space (EHDS) framework, advanced cross-border health data exchange initiatives, favorable government funding for hospital digitization projects, and interoperability mandates are also contributing to the sustained growth of the market in leading European countries.

Latin America (LATAM) and Middle East & Africa (MEA) Electronic Medical Record (EMR) Systems Market Insights:

In Latin America, and Middle East & Africa, the growing hospital digitization efforts and increase in internet connectivity with mobile device penetration support the electronic medical record systems market growth. The rising popularity of affordable cloud-based EMR solutions and multilingual platform capabilities, along with public sector healthcare modernization programs, will aid clinical documentation quality and patient record accessibility. The increasing urban hospital infrastructure investment and improving healthcare delivery standards in these regions are continuing to encourage market growth.

Electronic Medical Record (EMR) Systems Market Competitive Landscape:

Epic Systems Corporation (est. 1979) is a leading electronic health and medical record software developer that focuses on integrated clinical documentation and patient data management solutions for hospitals and health systems of all sizes. It uses its comprehensive EMR platform and deep provider relationships to produce advanced clinical charting, specialty documentation, and interoperability tools with seamless workflow integration.

-

In February 2025, it expanded its EMR platform capabilities with AI-powered ambient documentation and automated clinical coding features, aiming to reduce physician charting burden and improve documentation accuracy across its large hospital and health system client network.

Cerner Corporation (Oracle Health) (est. 1979) is a well-known global health information technology company focused on clinical EMR software, population health management, and revenue cycle solutions for large hospital networks and community health systems. It invests in interoperable electronic medical record platforms and cloud-based clinical data management tools with the hopes of revolutionizing care documentation with secure, scalable, and real-time digital health record capabilities.

-

In May 2024, launched an enhanced cloud-based EMR module featuring real-time clinical documentation synchronization and integrated specialty workflow templates across North American hospital systems, enhancing physician efficiency and cross-department care coordination.

athenahealth, Inc. (est. 1997) is a leading cloud-based healthcare technology provider in the fields of electronic medical record management, revenue cycle services, and clinical documentation solutions for ambulatory and hospital settings. The company's EMR product portfolio focuses on user-friendly clinical interfaces and mobile-first documentation design, and features a strong commitment to regulatory compliance and continuous innovation to complement a strong market presence among small, medium, and large healthcare organizations.

-

In September 2024, introduced advanced specialty EMR documentation templates and AI-assisted clinical note generation features for its athenaClinicals platform, strengthening physician productivity and expanding adoption among independent specialty practices and multi-site ambulatory care groups.

Electronic Medical Record (EMR) Systems Market Key Players:

-

Epic Systems Corporation

-

athenahealth, Inc.

-

Allscripts Healthcare Solutions

-

NextGen Healthcare, Inc.

-

eClinicalWorks

-

MEDITECH

-

Greenway Health

-

GE HealthCare Technologies Inc.

-

Siemens Healthineers

-

CureMD Healthcare

-

AdvancedMD

-

Kareo (Tebra)

-

Practice Fusion

-

drchrono

-

Netsmart Technologies

-

Prompt EMR

-

ChartLogic

-

WRS Health

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 31.51 Billion |

| Market Size by 2035 | USD 47.68 Billion |

| CAGR | CAGR of 4.23% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (General EMR Solutions, Specialty EMR Solutions)• By Component (Services, Software, Hardware)• By Hospital Size (Small and Medium-sized Hospitals, Large Hospitals)• By Delivery Mode (On-premise, Cloud-based) •By Indication (Body Contouring & Body Toning, Obesity & Weight Management, Chronic Disease Management, Fitness & Performance Enhancement, Others) •By Procedure (Mechanical, Electrical & Laser/Ultrasound) •By Distribution Channel (Retail Stores, Online Platforms (Direct Sales & Healthcare Providers) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | Epic Systems Corporation; Oracle Health; athenahealth, Inc.; Allscripts Healthcare Solutions; NextGen Healthcare, Inc.; eClinicalWorks; MEDITECH; Greenway Health; McKesson Corporation; GE HealthCare Technologies Inc.; Siemens Healthineers; CureMD Healthcare; AdvancedMD; Tebra (formerly Kareo); Practice Fusion; drchrono; Netsmart Technologies; Prompt EMR; ChartLogic; WRS Health |

Frequently Asked Questions

Ans: North America dominated the Electronic Medical Record (EMR) Systems Market in 2025

Ans: The General EMR Solutions segment dominated the Electronic Medical Record (EMR) Systems Market in 2025.

Ans: Government Mandates and Regulatory Support is Driving the Electronic Medical Record (EMR) Systems Market Growth.

Ans: The Electronic Medical Record (EMR) Systems Market size was valued at USD 31.51 billion in 2025 and is expected to reach USD 47.68 billion by 2035.

Ans: The Electronic Medical Record (EMR) Systems Market is expected to grow at a CAGR of 4.23% over the forecast period.

Get in Touch