Clinical Documentation Improvement Market Size Analysis:

Get more information on Clinical Documentation Improvement Market - Request Sample Report

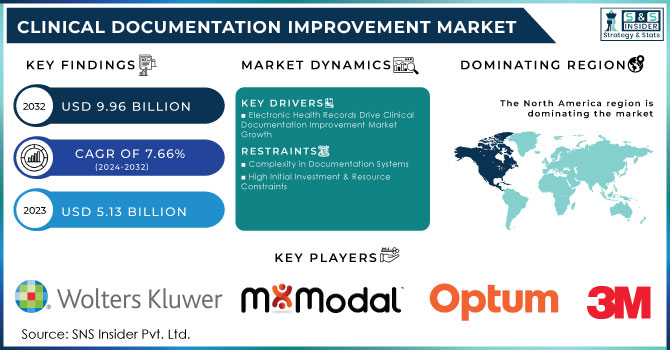

The Clinical Documentation Improvement Market Size was assessed to be worth USD 5.13 billion in 2023 and is expected to increase to USD 9.96 billion by 2032, extending at a CAGR of 7.66% from 2024 to 2032.

The clinical documentation improvement market is growing at a tremendous pace due to the rapid adoption of EHR systems and changes from traditional fee-for-service care models to value-based models. This can improve patient care, ensure regulatory compliance, and optimize revenue cycle management. Moreover, CDI solutions help enhance documentation accuracy, risk adjustment, and performance measurement and reporting areas that are central to the goals of value-based care. Under tremendous pressure to stay in compliance with a wide array of government regulations, including ICD-10 coding standards and the Health Insurance Portability and Accountability Act (HIPAA), there is much greater demand for CDI solutions.

The CDI solutions will also be further influenced by advanced technologies such as artificial intelligence, NLP, and predictive analytics, which will be much more effective in offering clinical decision support, automating workflows, and insights into documentation gaps and coding opportunities in real-time. CDI functionalities integrated within EHR systems streamline the documentation processes and improve efficiency for service providers in healthcare. As healthcare is more integrated and patient-centric, the scope of CDI extends from acute care to ambulatory, post-acute, and specialty care settings.

However, some drawbacks may be witnessed in terms of resistance from the physician community, limitations of availability of resources, and regulatory complexity. Lack of IT infrastructure in developing regions and data security issues also pose a threat. Despite these challenges, the market for CDI will only experience growth further as hospitals and healthcare facilities invest in CDI programs to reduce the risk of denials and improve reimbursement and patient safety. Virtual CDI solutions have also gained popularity as they open up more remote access to CDI services, further amplifying the potential of the market.

| Quality Criteria | Description |

|---|---|

| Documentation Completeness | Ensures comprehensive clinical data is documented, covering diagnoses, treatments, and patient outcomes. |

| Specificity of Diagnoses | Detailed and specific documentation of all diagnoses, including severity, complications, and comorbidities. |

| Capture of Procedures | Precise documentation of all procedures performed, ensuring correct coding and classification. |

| Accurate Coding | Use of accurate and up-to-date coding systems (ICD-10, CPT) for diagnoses and procedures. |

| Consistency Across Documentation | Consistency in documentation across various sources (e.g., physician notes, nursing notes, lab reports). |

| Timeliness of Documentation | Clinical documentation should be completed in a timely manner, adhering to regulatory and institutional standards. |

| Compliance with Regulatory Standards | Adherence to regulatory requirements such as CMS guidelines, Joint Commission standards, and payer policies. |

| Physician Engagement and Queries | Physicians should respond to CDI queries to clarify documentation and ensure accuracy in coding. |

| Clinical Relevance | Documentation should be clinically relevant, ensuring that it reflects the actual patient condition and treatment. |

| Improvement in Case Mix Index (CMI) | Monitoring the impact of documentation improvements on hospital CMI and reimbursement accuracy. |

| Reduction in Denials | Tracking reduction in claim denials due to accurate and complete documentation. |

| Educational Feedback | Providing regular feedback to healthcare providers on documentation quality and areas for improvement. |

Clinical Documentation Improvement Market Dynamics

Drivers

-

Electronic Health Records Drive Clinical Documentation Improvement Market Growth

The major growth driver of the Clinical Documentation Improvement market has been the trend towards the widespread adoption of Electronic Health Records or EHRs. Through EHR systems, healthcare providers can store and manage patient data in electronic formats, thereby considerably improving the efficiency of clinical documentation processes. This is because, through automation of the work of generation of patient summaries, progress notes, and medication prescriptions, EHRs enable the professionals in healthcare to spend a quality amount of time engaging in direct patient care, thus enhancing the quality of healthcare. This upsurge in the adoption of EHRs has directly led to the call for solutions within CDI that ensure proper and detailed documentation.

The biggest driver for this is the need for quality clinical documentation that is exact, and one way of achieving this remains effective documentation. Accurate documentation, hence becomes necessary not only for the safety of a patient but also to prove that care standards are followed. Care standards will be observed clearly, in minute detail when there is a defined and detailed clinical record outlining a patient's medical history, condition, and treatment plan. With quality documentation now a much more in-focus domain, the demand for CDI solutions should rise accordingly.

Another factor for growth in the CDI market is the growing interest in regulatory compliance. The number of regulations and guidelines healthcare providers must adhere to is constantly rising- HIPAA, Joint Commission standards, and CMS guidelines, for example. Applying CDI solutions will help providers come into compliance with these regulatory mandates by freeing them from backbreaking paperwork, eliminating errors, and ensuring that documentation is thorough, complete, and accurate. This has improved operational efficiency and led to driving market growth.

Restraints

-

Complexity in Documentation Systems

-

High Initial Investment & Resource Constraints

Clinical Documentation Improvement Market Segment Overview

By Product and Service

The Solutions segment emerged as the market leader in 2023, accounting for over 65.0% of the Clinical Documentation Improvement (CDI) market. This is mainly because the adoption rates for high-end CDI software solutions are highly high since they simplify documentation processes, reduce errors, and enhance coding accuracy. Those solutions interface with electronic health records to automate the recording of patient documents and enable health providers to maintain accurate and high-quality documents of patients to improve care outcomes and comply with regulatory requirements in electronic health records.

The Consulting Services segment will have the highest growth rate over the forecast period. Growth drivers include ever-burgeoning needs for expert advice in implementing CDI systems related to compliance regulation navigation, as well as optimization of operations-driven workflows. The consulting services requirements of these healthcare organizations drive this fast-growing area through their requirements to train staff, better document care delivery, and comply with new demands from regulations.

By End Users

The Healthcare Providers segment was the largest end-user segment in 2023, accounting for more than 70.0% of the CDI market. It is for this reason that healthcare providers-which include hospitals, clinics, and long-term care facilities-increase the adopt CDI solutions because the critical need will always be there: accuracy and timeliness of clinical documentation. Multiple widespread applications of EHRs, along with unprecedented interest in patient safety, quality of care, and regulatory compliance, have pushed CDI solutions into leadership positions in the market.

The healthcare payers segment is predicted to grow the fastest. Accordingly, payers are increasingly recognizing clinical data capture as a part of reducing errors, increasing claim reimbursements, and cutting down fraud. With the emphasis placed on value-based care by insurers and governments, along with streamlined and efficient claims processing, there will be a huge demand for CDI solutions among payers, pushing them further in terms of expansion in the market.

Clinical Documentation Improvement Market Regional Analysis

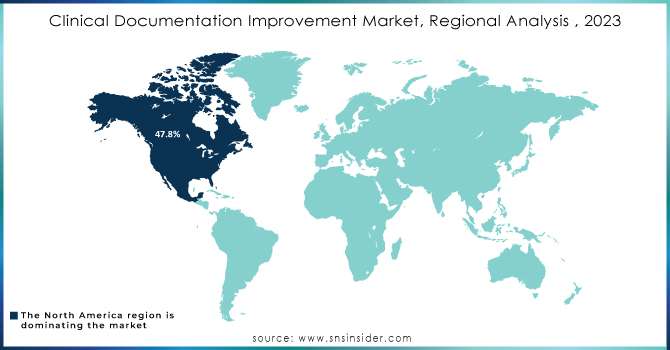

In 2023, North America dominated the Clinical Documentation Improvement market with a market share of 47.8%. This region is primarily driven by the presence of the largest healthcare providers, strict regulatory frameworks, and well-established healthcare infrastructure. Advanced EHR adoption and its strong healthcare quality, combined with increasing strict adherence to HIPAA and CMS guidelines, have ensured this leading market share for North America. The region has also enjoyed the benefits of significant investments from CDI solutions, where clinical documentation is much more efficient and patient care is improved.

The second largest market share of CDI lies in Europe. Several European nations such as the UK, France, and Germany are key contributors to this growth in the regional market. Here, strong government initiatives, proper healthcare regulations, and a highly digitized healthcare system have acted as contributing factors in bringing CDI solutions into practice across the region. Healthcare providers in these countries are keenly focused on documentation improvement and compliance, further advancing market growth.

The Asia-Pacific region, in particular, is slated to grow significantly in the CDI market in the years to come. These include health care expenses, population increase, and government-initiated efforts to improve the quality of health care. The current rate at which China, India, and Japan, among other countries, are demanding better healthcare technologies, which include CDI solutions, to improve clinical results and organize the documentation process, is impressive. APAC growth is brisk with a rise in the importance given to upgrading healthcare infrastructure and meeting regulatory compliance.

Need any customization research on Clinical Documentation Improvement Market - Enquiry Now

Key Clinical Documentation Improvement Companies:

Clinical Documentation Improvement Solutions

-

3M Health Information Systems

-

MModal

-

Aviacode

-

Cotiviti, Inc.

-

R1 RCM, Inc.

-

Craneware

Consulting Services for Clinical Documentation

-

The HCI Group, Inc.

-

Ingenious Med, Inc.

-

SSI Group, LLC

Documentation and Data Capture Solutions

-

ClinCapture

-

PerfectServe, Inc.

-

Health Language, Inc.

-

ChartMaxx

Recent Developments

In March 2024, Abridge, a generative AI company, announced a strategic partnership with NVIDIA aimed at enhancing clinician workflows and patient care through AI-driven solutions. As part of this collaboration, Abridge also secured investment from NVentures, NVIDIA’s venture capital branch.

In October 2023, Nuance Communications acquired Saykara, a provider of AI-powered Clinical Documentation Improvement solutions, to strengthen its CDI offerings.

| Report Attributes | Details |

|---|---|

| Market Size in 2023 | US$ 5.13 billion |

| Market Size by 2032 | US$ 9.96 billion |

| CAGR | CAGR of 7.66% From 2024 to 2032 |

| Base Year | 2023 |

| Forecast Period | 2024-2032 |

| Historical Data | 2020-2022 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product and Service [Solutions (Clinical Documentation, Clinical Coding, Charge Capture, Clinical Documentation Improvement, Others), Consulting Services] |

| • By End Users [Healthcare Providers (Inpatient Settings, Outpatient Settings), Healthcare Payers) | |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | 3M Health Information Systems, Wolters Kluwer Health, MModal, Optum360, Aviacode, Cotiviti, Inc., R1 RCM, Inc., Craneware, The HCI Group, Inc., Ingenious Med, Inc., SSI Group, LLC, ClinCapture, PerfectServe, Inc., Health Language, Inc., ChartMaxx |

| Key Drivers | • Electronic Health Records Drive Clinical Documentation Improvement Market Growth |

| Restraints | • Complexity in Documentation Systems |

| • High Initial Investment & Resource Constraints |

Frequently Asked Questions

Infrastructure Shortages in Developing Nations are the restraints of Clinical Documentation Improvement Market

Clinical Documentation Improvement Market is divided into two segments By Product & Service, and By End User

North America's market is well-established, with the US leading the market there. The US healthcare delivery system is largely influenced by the healthcare insurance sector, which administers programmes like Medicare and Medicaid

Ans: The Clinical Documentation Improvement Market size was valued at USD 5.13 billion in 2023.

Ans:- The Clinical Documentation Improvement market is expected to grow at a CAGR of 7.66% over the forecast period 2024-2032.

Get in Touch