Embedded AI Market Report Scope & Overview:

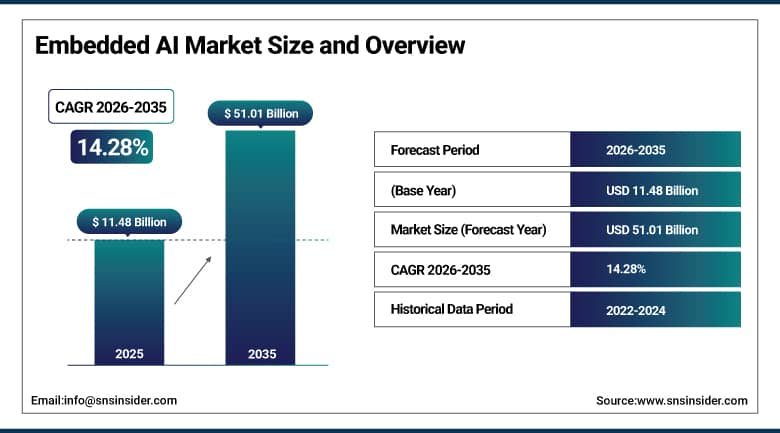

The Embedded AI Market was valued at USD 11.48 Billion in 2025 and is expected to reach USD 51.01 Billion by 2035, growing at a CAGR of 14.28% from 2026–2035.

The global embedded AI market is experiencing exceptional growth driven by increasing consumer adoption of AI-driven technologies, significant investments in AI research and development, and the integration of AI into edge devices and embedded systems across industries. Embedded AI refers to artificial intelligence algorithms and models integrated directly into hardware devices and embedded systems, enabling real-time local inference and decision-making without dependence on cloud computing infrastructure. The market is shaped by expanding IoT adoption requiring real-time device intelligence, advancements in AI hardware miniaturization reducing the computational power requirement for on-device inference, trends toward cost reduction in AI hardware and software solutions, and the growing need for AI capability in bandwidth-constrained and privacy-sensitive applications where cloud connectivity is impractical or undesirable.

In 2024, NVIDIA launched its Jetson Orin NX embedded AI module in expanded configurations targeting industrial automation, healthcare imaging, and autonomous robotics applications, delivering up to 100 TOPS of AI performance at 10-25 watts of power consumption. The product expansion reflects the commercial direction of embedded AI hardware development toward above-performance-per-watt optimization whose energy efficiency improvement creates deployment viability in battery-powered and thermally constrained embedded applications that prior-generation compute platforms could not serve.

Market Size and Forecast:

-

Market Size in 2026E: USD 13.12 Billion

-

Market Size by 2035: USD 51.01 Billion

-

CAGR: 14.28% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: North America

To Get More Information On Embedded AI Market - Request Free Sample Report

Embedded AI Market Trends:

-

Development of neuromorphic computing chips is advancing next-generation embedded AI systems by delivering significantly higher energy efficiency for pattern recognition, sensing, and edge intelligence applications

-

Growing feasibility of on-device large language models (LLMs) is enabling conversational AI and intelligent processing directly on embedded devices without continuous cloud connectivity

-

Increasing adoption of federated learning is supporting privacy-preserving AI deployments by enabling model training across distributed devices while keeping sensitive data local

-

Specialized AI accelerators such as NPUs and edge AI processors are driving performance improvements for embedded applications in consumer electronics, automotive, and industrial systems

-

Rising use of embedded AI for predictive maintenance is enabling real-time monitoring and anomaly detection in industrial equipment through local analysis of sensor data, reducing downtime and maintenance costs

U.S. Embedded AI Market Outlook:

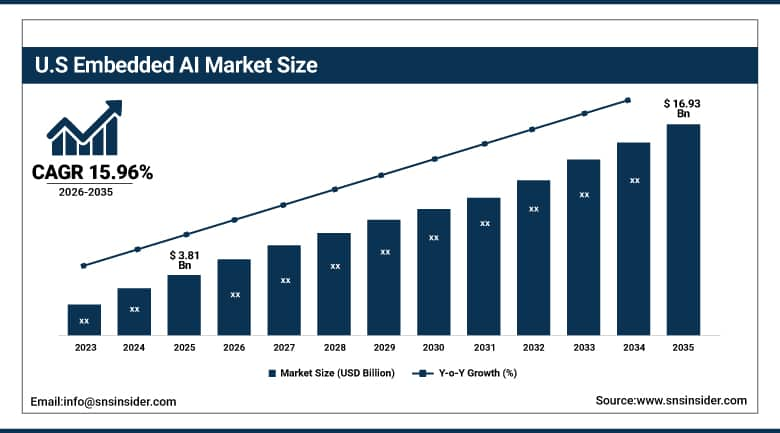

The U.S. Embedded AI Market was valued at approximately USD 3.81 Billion in 2025 and is expected to reach approximately USD 16.93 Billion by 2035, growing at a CAGR of approximately 15.96%.

The U.S. is the most commercially advanced embedded AI market within North America's dominant revenue position. NVIDIA, Qualcomm, Intel, Apple, Google, and Texas Instruments collectively define the domestic embedded AI hardware landscape whose silicon innovation creates the embedded AI processing platforms adopted globally. The U.S. automotive industry's ADAS and autonomous vehicle development creates structured embedded AI semiconductor procurement. The healthcare sector's point-of-care medical AI, the consumer electronics industry's neural processing unit integration, and the industrial automation sector's edge intelligence deployment collectively sustain above-average U.S. embedded AI commercial demand

In 2023, Qualcomm launched its Snapdragon 8 Gen 2 with enhanced Hexagon NPU delivering 4.35 TOPS of dedicated AI performance for smartphone and embedded applications, enabling on-device inference for generative AI applications including image generation, voice processing, and contextual recommendation. The processor demonstrates the commercial direction of mobile and embedded AI silicon toward dedicated neural processing hardware whose energy efficiency improvement per AI operation creates practical on-device AI application capability that previous mobile processors could not sustain within thermal and battery constraints.

Embedded AI Market Segment Analysis:

-

By Offering, the Hardware segment dominated the Embedded AI Market with approximately 58% share in 2025, while the Software segment is the fastest growing.

-

By Data Type, the Sensor Data segment dominated the Embedded AI Market with approximately 32% share in 2025, while the Image & Video Data segment is the fastest growing.

-

By Vertical, the Healthcare segment dominated the Embedded AI Market with approximately 24% share in, while the Automotive segment is the fastest growing.

By Offering, hardware dominates, software grows fastest

Hardware retained the dominant offering position with approximately 58% of the embedded AI market in 2025. The hardware segment's commercial primacy reflects the foundational requirement for embedded AI processing infrastructure whose deployment is the prerequisite for all subsequent software and services layer commercial activity. Embedded AI processors including NVIDIA Jetson modules for industrial and robotics applications, Qualcomm Snapdragon NPU-integrated mobile processors for consumer devices, Google Coral Edge TPU for inference acceleration, and Arm Cortex-M55 with Ethos-U NPU for microcontroller applications collectively define the commercial hardware landscape. Each embedded AI device deployed creates hardware procurement whose commercial aggregate across billions of deployed IoT, consumer electronics, automotive, and industrial devices creates the market's largest commercial category.

Software is the fastest-growing offering because the expanding embedded AI installed hardware base creates growing demand for model development frameworks, edge inference optimization tools, and AI application lifecycle management platforms whose recurring revenue compounds with the hardware installed base growth. TensorFlow Lite, ONNX Runtime, PyTorch Mobile, and vendor-specific edge AI SDKs collectively create the software ecosystem whose tooling improves developer productivity and sustains embedded AI application development investment. The commercial maturation of embedded AI application development creates software procurement whose subscription and license revenue grows independently of new hardware installation rates.

By Data Type, sensor data dominates, image & video grows fastest

Sensor data retained the dominant data type position with approximately 32% of the embedded AI market in 2025. The extraordinary deployment scale of IoT sensors across industrial equipment, smart infrastructure, consumer devices, and environmental monitoring creates the largest aggregate embedded AI inference workload of any data type category. Each industrial motor, conveyor belt, HVAC system, and production equipment that integrates vibration, temperature, or acoustic sensor embedded AI creates predictive maintenance intelligence whose real-time anomaly detection requires on-device processing that cloud-dependent analysis cannot provide with equivalent responsiveness. The simplicity of sensor data relative to image and video data creates lower embedded AI processing requirements that enable cost-effective deployment across a broader range of microcontroller-class embedded hardware.

Image and video data is the fastest-growing type because embedded computer vision adoption in automotive ADAS, security surveillance, healthcare imaging devices, and smart retail creates above-average embedded AI hardware procurement for high-performance edge vision processors. Each camera-based ADAS feature that processes real-time image data for pedestrian detection, lane keeping, and traffic sign recognition creates embedded vision processor procurement that compounds with ADAS feature proliferation across vehicle segments. The surveillance camera market's adoption of on-device AI for real-time object detection and facial recognition creates embedded vision processor demand that compounds with global smart city infrastructure investment.

By Vertical, healthcare dominates, automotive grows fastest

Healthcare retained the dominant vertical position with approximately 24% of the embedded AI market in 2025. The healthcare sector's unique requirement for reliable on-device AI processing, whose patient safety implications demand continuous local operation without network connectivity dependence, creates embedded AI procurement that prioritizes reliability and certification over cost optimization. Medical device embedded AI encompasses continuous glucose monitoring AI interpretation, cardiac rhythm analysis in wearable ECG devices, patient vital sign anomaly detection in ICU monitoring equipment, and robotic surgical system vision and motion processing whose combined procurement creates the most commercially concentrated healthcare embedded AI application portfolio.

Automotive is the fastest-growing vertical because ADAS feature regulatory mandates, autonomous driving development investment, and in-vehicle AI assistant deployment create above-average embedded AI semiconductor procurement per vehicle whose commercial scale compounds with global vehicle production volume. Each ADAS feature that requires real-time camera, radar, and LiDAR data fusion for pedestrian detection, lane keeping, and adaptive cruise control creates embedded AI processor procurement whose per-vehicle cost grows with ADAS feature count. The NCAP mandatory ADAS feature requirement, NHTSA automatic emergency braking mandate, and equivalent Asian standards collectively create defined adoption timelines whose procurement compounds with global vehicle production.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

44.8% |

|

Middle East & Africa |

UAE |

38.4% |

|

Latin America |

Brazil |

44.2% |

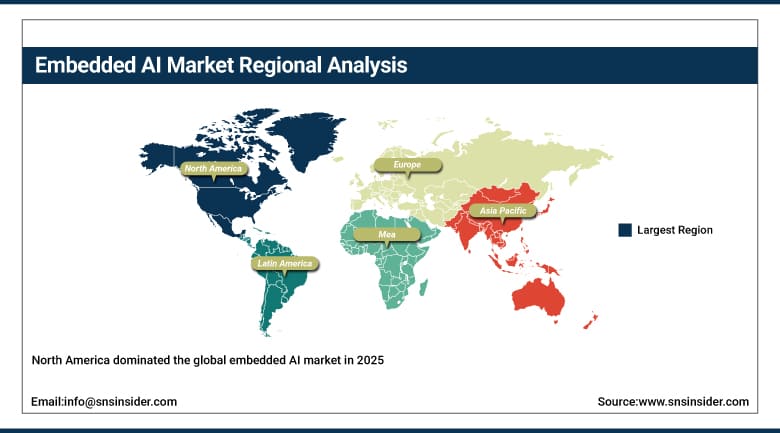

North America Embedded AI Market Insights

North America dominated the global embedded AI market in 2025 through the concentration of leading AI chip manufacturers including NVIDIA, Qualcomm, Intel, Google, and Apple whose silicon innovation defines the embedded AI hardware platform adopted globally. The United States accounts for approximately 87.4% of North American revenues through its semiconductor leadership, the automotive industry’s ADAS and AV development, the consumer electronics market’s AI feature integration, and the healthcare sector’s medical device AI adoption.

Canada contributes approximately 12.6% of North American revenues through its AI research community, the growing embedded AI startup ecosystem, and the manufacturing sector’s industrial edge AI adoption.

Get Customized Report as Per Your Business Requirement - Enquiry Now

Europe Embedded AI Market Insights

Europe is a technically sophisticated embedded AI market where the automotive industry’s ADAS investment, the industrial automation sector’s edge intelligence adoption, and EU AI Act compliance motivating on-device processing of sensitive data create structured institutional demand. Germany accounts for approximately 22.3% of European revenues through its automotive manufacturing sector’s embedded AI semiconductor procurement, Siemens’ and Bosch’s industrial IoT AI investment, and the manufacturing sector’s Industry 4.0 edge AI deployment.

The United Kingdom, France, and Sweden are significant secondary markets where the automotive sector, aerospace industry, and consumer electronics manufacturing create consistent embedded AI demand. STMicroelectronics’ Swiss-Italian operations and NXP Semiconductors’ Dutch headquarters sustain European embedded AI silicon supply from established commercial presences.

Asia Pacific Embedded AI Market Insights

Asia Pacific is the fastest-growing regional embedded AI market, driven by China's extraordinary electronics manufacturing scale, Japan's robotics and automotive AI investment, South Korea's Samsung and SK Hynix embedded AI memory leadership, Taiwan's semiconductor manufacturing, and India's growing IoT and consumer electronics sector. China accounts for approximately 44.8% of Asia Pacific revenues through its consumer electronics production scale, the automotive industry’s embedded AI semiconductor demand, and domestic AI chip developer investment including Huawei HiSilicon and Horizon Robotics.

Taiwan represents a strategically significant secondary market where TSMC's advanced semiconductor manufacturing creates the fabrication infrastructure for global embedded AI chip production, and MediaTek’s and Realtek’s IoT AI semiconductor portfolios create domestic commercial procurement.

MEA & Latin America Embedded AI Market Insights

UAE leads MEA revenues at approximately 38.4% through its smart city infrastructure investment, the consumer electronics market, and the growing manufacturing sector’s IoT AI adoption. Saudi Arabia’s NEOM smart city programme and Vision 2030 technology investment add substantial complementary Gulf demand. Brazil leads Latin American revenues at approximately 44.2% through its consumer electronics market, growing automotive ADAS adoption, and manufacturing industrial IoT investment. Mexico’s electronics manufacturing and Colombia’s smart infrastructure investment collectively sustain Latin American embedded AI market growth through 2035.

Market Dynamics:

Growth Drivers: IoT expansion requiring on-device intelligence and edge computing adoption eliminating cloud latency

IoT expansion is the embedded AI market's most commercially certain structural growth driver. The IHS Markit projection of over 75 billion connected IoT devices by 2025 creates an extraordinary embedded AI deployment opportunity who’s on-device intelligence requirement compounds with device count growth. Each IoT device category that adopts embedded AI for anomaly detection, predictive maintenance, or contextual response capability creates procurement that multiplies across the category's global deployment scale. The manufacturing sector's IIoT adoption, the smart home market's voice assistant and sensor intelligence, and the healthcare sector's continuous monitoring device deployment collectively sustain IoT-driven embedded AI demand.

Edge computing adoption's systematic shift of AI inference from cloud to device eliminates the latency, bandwidth cost, and connectivity dependence that cloud-based AI creates in latency-sensitive applications. Each industrial automation system, autonomous vehicle, and medical monitoring device that requires sub-millisecond AI response creates embedded AI hardware procurement whose latency requirement cannot be satisfied by cloud inference regardless of network quality improvement. The reliability advantage of on-device processing in connectivity-challenged environments creates additional embedded AI adoption motivation beyond latency improvement alone.

Restraints: Power consumption challenges in battery-constrained applications and limited on-device memory for large AI models

Power consumption constraints in battery-powered embedded devices create embedded AI deployment limitations whose computational intensity depletes battery life in wearables, remote sensors, and portable consumer electronics below acceptable operation duration. Each AI workload that exceeds the thermal dissipation capability of the embedded hardware creates performance throttling or device heating whose user experience impact limits aggressive embedded AI specification in power-constrained form factors.

Limited on-device memory and compute create model size constraints that prevent deployment of large-parameter AI models on microcontroller-class embedded hardware without model compression that may compromise inference accuracy. Each embedded AI application whose performance requirement cannot be satisfied by compressed model variants within device memory constraints creates deployment barriers that sustain the boundary between cloud-hosted and edge-hosted AI inference.

Opportunities: On-device LLM deployment and embedded AI for autonomous industrial systems

On-device large language model deployment represents the most commercially transformative emerging opportunity as model compression, quantization to 4-bit integer precision, and hardware-accelerated matrix operations progressively enable transformer-based LLM inference within embedded processor constraints. Each smartphone, smart speaker, and computing device that enables fully private on-device LLM inference without cloud connectivity creates premium product differentiation whose privacy advantage sustains consumer preference and embedded AI hardware specification investment.

Embedded AI for autonomous industrial systems represents a growing premium commercial opportunity whose real-time machine vision, robotic motion planning, and production quality inspection create structured procurement from manufacturing automation investment. Each new collaborative robot, industrial inspection system, and autonomous mobile robot that requires embedded AI for real-time environment perception creates commercial procurement whose aggregate grows with the global industrial automation investment pace.

Recent Developments:

-

2024: NVIDIA expanded its Jetson Orin NX embedded AI module configurations in 2024, delivering up to 100 TOPS of AI performance at 10-25 watts, targeting industrial automation, healthcare imaging, and autonomous robotics applications requiring high-performance edge AI within tight power envelopes.

-

2024: Qualcomm launched its Snapdragon 8 Elite mobile processor in 2024 with an enhanced Hexagon NPU delivering above 45 TOPS of on-device AI performance, enabling generation AI features including on-device image synthesis, real-time video enhancement, and context-aware assistant capabilities without cloud connectivity.

-

2024: STMicroelectronics launched the STM32N6 microcontroller family in 2024 with an integrated Neural Processing Unit delivering 600 TOPS/W energy efficiency for ultra-low-power embedded AI applications in industrial IoT sensors, smart meters, and battery-powered edge AI devices.

-

2023: Qualcomm launched its Snapdragon 8 Gen 2 processor in 2023 with enhanced Hexagon NPU delivering 4.35 TOPS of dedicated AI performance, enabling on-device inference for generative AI smartphone applications including image generation, voice processing, and contextual recommendation.

-

2023: Google expanded its Edge TPU ecosystem in 2023 with new Coral Dev Board Micro modules and updated TensorFlow Lite runtime optimization for sub-milliwatt embedded inference, targeting battery-constrained IoT sensor and wearable device embedded AI applications.

Embedded AI Market Key Players:

-

NVIDIA Corporation

-

Qualcomm Incorporated

-

Intel Corporation

-

NXP Semiconductors N.V.

-

STMicroelectronics N.V.

-

Texas Instruments Incorporated

-

Arm Holdings plc

-

Google LLC (Edge TPU)

-

Apple Inc. (Neural Engine)

-

Renesas Electronics Corporation

-

Microchip Technology Inc.

-

Lattice Semiconductor Corporation

-

Hailo Technologies Ltd.

-

Kneron Inc.

-

Edge Impulse Inc.

-

Syntiant Corp.

-

SiMa.ai

-

Eta Compute Inc.

-

DeepVision Inc.

-

Expedera Inc.

Embedded AI Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 11.48 Billion |

| Market Size by 2035 | USD 51.01 Billion |

| CAGR | CAGR of 14.28% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • by Offering (Hardware, Software, Services) • by Data Type (Sensor Data, Image & Video Data, Numeric Data, Categorical Data, Others) • by Vertical (Healthcare, BFSI, IT & Telecom, Retail & E-Commerce, Media & Entertainment, Automotive, Manufacturing, Others) |

| Regional Analysis/Coverage | North America (US, Canada, Mexico), Europe (Eastern Europe [Poland, Romania, Hungary, Turkey, Rest of Eastern Europe] Western Europe] Germany, France, UK, Italy, Spain, Netherlands, Switzerland, Austria, Rest of Western Europe]), Asia Pacific (China, India, Japan, South Korea, Vietnam, Singapore, Australia, Rest of Asia Pacific), Middle East & Africa (Middle East [UAE, Egypt, Saudi Arabia, Qatar, Rest of Middle East], Africa [Nigeria, South Africa, Rest of Africa], Latin America (Brazil, Argentina, Colombia, Rest of Latin America) |

| Company Profiles | NVIDIA Corporation, Qualcomm Incorporated, Intel Corporation, NXP Semiconductors N.V., STMicroelectronics N.V, Texas Instruments Incorporated, Arm Holdings plc, Google LLC (Edge TPU), Apple Inc. (Neural Engine), Renesas Electronics Corporation, Microchip Technology Inc., Lattice Semiconductor Corporation, Hailo Technologies Ltd., Kneron Inc., Edge Impulse Inc., Syntiant Corp., SiMa.ai, Eta Compute Inc., DeepVision Inc., Expedera Inc. |

Frequently Asked Questions

The Embedded AI Market is expected to grow at a CAGR of 14.28% from 2026 to 2035.

The Embedded AI Market was valued at USD 11.48 Billion in 2025.

Increasing IoT device adoption requiring on-device AI intelligence for real-time decision-making without cloud connectivity dependence, and edge computing adoption eliminating cloud latency and connectivity requirements in time-critical and privacy-sensitive embedded AI applications.

Hardware dominated the Embedded AI Market with approximately 58% share in 2025, while Software is the fastest growing segment.

North America dominated the Embedded AI Market in 2025 through concentration of leading AI chip manufacturers, while Asia Pacific is the fastest-growing region.

Get in Touch