Endoscopic Submucosal Dissection Market Report Scope & Overview:

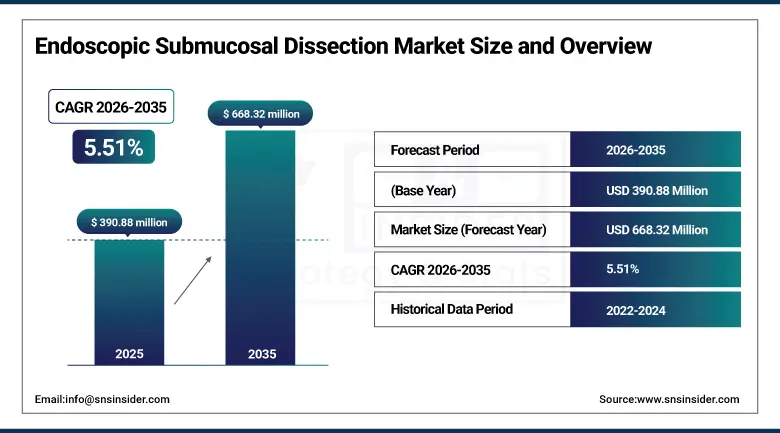

The Endoscopic Submucosal Dissection Market size was estimated at USD 390.88 million in 2025 and is expected to reach USD 668.32 million by 2035, growing at a CAGR of 5.51% over the forecast period of 2026-2035.

The global endoscopic submucosal dissection (ESD) market shows steady growth driven by rising early-stage gastrointestinal cancer incidence, increased adoption of minimally invasive endoscopic resection over open surgery, and advances in ESD tools including dissection knives, submucosal injection agents, and high-definition scopes. Growing physician proficiency in ESD across North America and Europe, supported by training programs and international guidelines, is expanding volumes beyond Japan, South Korea, and China. Healthcare systems favor ESD for achieving en bloc resection with clear histological margins in early gastric, colorectal, and esophageal lesions, reducing recurrence and limiting surgical need. Ongoing investment in hybrid ESD platforms, underwater techniques, and AI-assisted real-time lesion delineation is further shaping competition and accelerating market maturity.

For instance, in January 2024, the American Society for Gastrointestinal Endoscopy reported that ESD procedure adoption rates in the United States increased by approximately 18.4% year-over-year between 2022 and 2023, driven by expanded endoscopist training initiatives and growing recognition of ESD's superiority over piecemeal endoscopic mucosal resection for lesions exceeding 20 mm in diameter.

Endoscopic Submucosal Dissection Market Size and Forecast:

-

Market Size in 2025: USD 390.88 million

-

Market Size by 2035: USD 668.32 million

-

CAGR: 5.51% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Endoscopic Submucosal Dissection Market - Request Free Sample Report

Endoscopic Submucosal Dissection Market Trends

-

Accelerating global adoption of ESD as the standard of care for early gastrointestinal neoplasms, supported by updated clinical guidelines from ESGE and JGES, is expanding procedure eligibility criteria and increasing annual case volumes.

-

Introduction of next-generation ESD knives with insulated tips, dual-mode cutting capability, and ergonomically optimized handles is improving procedural precision, reducing perforation rates, and shortening procedure duration across academic and community endoscopy centers.

-

Growing utilization of novel viscous submucosal injection agents, including HPMC and hyaluronic acid-based solutions, is improving submucosal cushion longevity and enhancing safety profiles for challenging colorectal and esophageal ESD cases.

-

Emergence of robotic and semi-automated ESD platforms equipped with tremor-filtering and tissue tension monitoring capabilities is reducing the operator learning curve and enabling broader geographic dissemination of ESD competency beyond high-volume tertiary centers.

-

Integration of artificial intelligence and computer-aided detection systems into ESD-compatible endoscopic platforms is enabling real-time mucosal boundary delineation, lesion depth assessment, and procedural guidance, improving en bloc resection rates and reducing intraoperative complications.

-

Rapid expansion of ambulatory surgical centers and outpatient endoscopy facilities in North America and Europe is creating new high-volume ESD procedure settings, shifting a portion of inpatient-based ESD volume to lower-cost, higher-throughput outpatient environments.

-

Structured ESD training programs using ex vivo animal tissue models, virtual reality simulators, and proctored live case workshops are accelerating competency development among gastroenterology and surgical endoscopy fellows, increasing the qualified ESD operator pool across Western markets.

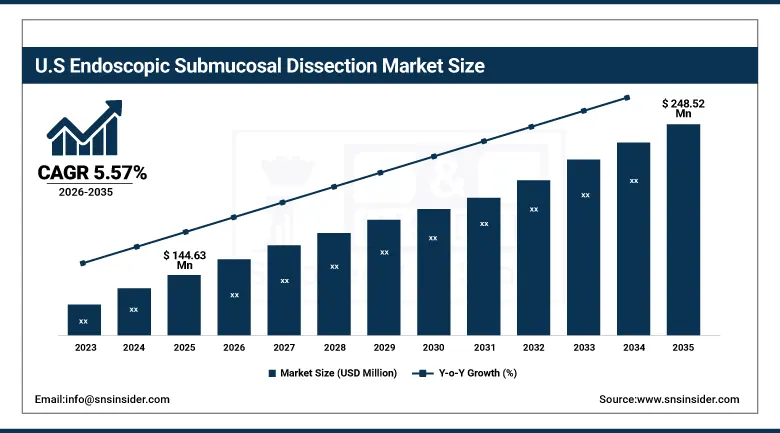

The U.S. Endoscopic Submucosal Dissection Market was valued at USD 144.63 million in 2025 and is expected to reach USD 248.52 million by 2035, growing at a CAGR of 5.57% from 2026–2035. The United States is the largest country market for endoscopic submucosal dissection outside Asia, driven by high colorectal cancer screening prevalence, rising diagnosis of early-stage gastric and esophageal lesions suitable for endoscopic resection, and strong investment in advanced endoscopy infrastructure. Expanding Medicare and private payer coverage for ESD procedures, along with Centers of Excellence at major academic medical centers, is accelerating standardization and improving patient access. The presence of leading device manufacturers and ongoing FDA 510(k) clearances for new ESD instruments further supports market growth.

Endoscopic Submucosal Dissection Market Growth Drivers:

-

Rising Global Incidence of Early Gastrointestinal Cancers and Increasing Preference for Organ-Preserving Resection Techniques is Driving the Endoscopic Submucosal Dissection Market Growth

The escalating global burden of gastric, colorectal, and esophageal cancers, with the World Health Organization estimating over 1.09 million new gastric cancer cases and 1.93 million new colorectal cancer cases diagnosed worldwide in 2024, is creating a large and structurally expanding patient population for whom early-stage ESD resection is clinically appropriate and guideline-recommended. Increasing national colorectal cancer screening program penetration across the U.S., European Union, Japan, and South Korea is identifying higher proportions of early-stage mucosal lesions eligible for curative endoscopic resection, directly driving ESD procedure volume growth. Healthcare providers and payers increasingly recognize ESD's cost-effectiveness relative to surgical resection for T1a and select T1b lesions, further accelerating adoption across both academic and community endoscopy settings.

For instance, in April 2024, a multicenter European study published in Endoscopy International Open demonstrated that ESD achieved an en bloc resection rate of 96.2% and an R0 resection rate of 91.8% for early colorectal neoplasms exceeding 20 mm, reinforcing ESD's clinical superiority over alternative endoscopic resection techniques and supporting its broader adoption in Western endoscopy practice.

Endoscopic Submucosal Dissection Market Restraints:

-

High Procedural Complexity and Extended Operator Learning Curve are Hampering Endoscopic Submucosal Dissection Market Growth

Despite its well-established clinical efficacy, ESD remains a technically demanding procedure requiring extensive operator training, with most international endoscopy societies recommending a minimum of 30 to 40 supervised gastric ESD cases before independent practice certification. The high risk of procedure-related adverse events, including perforation rates of 1.2% to 5.8% and delayed bleeding rates of 0.8% to 3.6% in Western cohorts reported through 2024, discourages adoption among endoscopists without dedicated advanced endoscopy fellowship training. Limited reimbursement parity for ESD relative to surgical alternatives in several European and emerging market healthcare systems, combined with the capital investment required for dedicated ESD endoscopy suites and instrumentation inventories, further constrains procedure volume growth in cost-sensitive healthcare environments.

Endoscopic Submucosal Dissection Market Opportunities:

-

Robotic-Assisted ESD Platforms and AI-Integrated Endoscopy Systems Present Significant Growth Opportunities for the Endoscopic Submucosal Dissection Market

The development and commercialization of robotic-assisted ESD systems capable of delivering tremor suppression, force feedback, and semi-automated submucosal dissection represent a transformative growth opportunity that could fundamentally lower the technical barriers to ESD adoption in Western markets. Companies including Medtronic and emerging medtech start-ups are advancing endoscopic robotics platforms into clinical trials, with initial indications targeting colorectal and gastric ESD. Simultaneously, the integration of deep learning-based lesion assessment and real-time margin delineation tools into ESD-compatible endoscopy platforms is projected to reduce procedure time by an estimated 22% to 31%, improve R0 resection rates, and enable confident ESD practice expansion beyond high-volume tertiary centers into community hospital endoscopy programs.

For instance, in October 2024, a prospective clinical trial evaluating an AI-assisted ESD navigation system at three high-volume endoscopy centers in Japan and South Korea reported a statistically significant reduction in mean procedure time from 68.4 minutes to 49.7 minutes for early gastric lesions, alongside a perforation rate reduction from 3.1% to 0.9%, demonstrating the transformative procedural safety and efficiency potential of next-generation AI-integrated ESD platforms.

Endoscopic Submucosal Dissection Market Segment Analysis

-

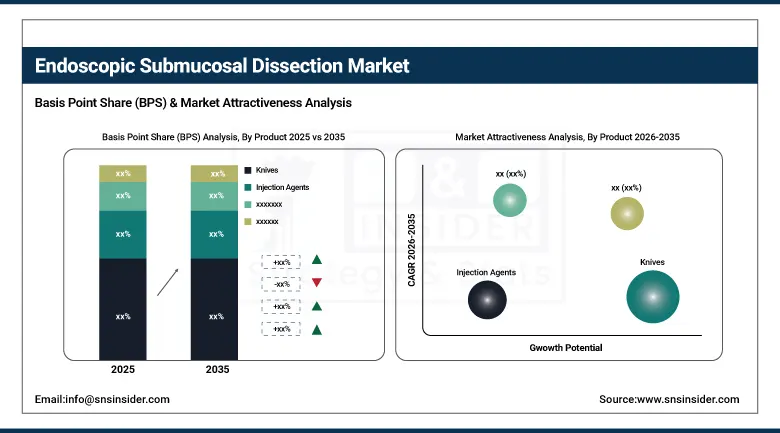

By product, knives held the largest share of approximately 33.47% in 2025, while the injection agents segment is expected to register the highest CAGR of 6.82% through 2035.

-

By indication, stomach cancer dominated with a share of approximately 38.14% in 2025, while the colon cancer segment is expected to register the highest CAGR of 6.24% over the forecast period.

-

By technology, conventional ESD accounted for the leading share of approximately 57.63% in 2025, while the underwater ESD segment is expected to register the highest CAGR of 7.46% through 2035.

-

By end use, hospitals accounted for the largest share of approximately 61.82% in 2025, while ambulatory surgical centers are expected to register the highest CAGR of 7.18% through 2035.

By Product, Knives Lead the Market, While Injection Agents Register Fastest Growth

ESD knives held the largest revenue share of ~33.47% in 2025, driven by their essential role in all ESD procedures and wide availability across insulated tip, hook, flex, and dual configurations. Olympus Corporation and FUJIFILM Holdings led knife segment revenues in 2025 due to strong innovation, global distribution, and installed base. Injection agents are projected to grow at the highest CAGR of ~6.82% (2026–2035), supported by rising preference for viscous submucosal agents over saline, increased availability of HPMC and sodium hyaluronate injectables, and evidence of reduced complications. Gastroscopes and colonoscopes accounted for ~26.73% share in 2025, supported by replacement cycles and adoption of advanced imaging systems.

By Indication, Stomach Cancer Leads, While Colon Cancer Registers Fastest Growth

Stomach cancer held the largest share of ~38.14% in 2025, driven by established guidelines and mature ESD practices in Japan, South Korea, and China. Japan alone contributed ~28.6% of global gastric ESD procedures in 2024. Colon cancer is expected to grow at the highest CAGR of ~6.24%, supported by screening expansion, higher detection of complex lesions, and increasing endorsement by ESGE and American College of Gastroenterology. Esophageal cancer held ~21.38% share in 2025, supported by Barrett’s esophagus surveillance programs.

By Technology, Conventional ESD Leads, While Underwater ESD Registers Fastest Growth

Conventional ESD led with ~57.63% share in 2025 due to standardized protocols, high adoption, and strong instrument ecosystem. It remains dominant in Asia Pacific and is expanding in Western markets. Underwater ESD is projected to grow at the highest CAGR of ~7.46% (2026–2035), driven by reduced procedure time, no injection requirement in select cases, better visualization, and lower perforation risk. Hybrid ESD held ~19.24% share in 2025 and is gaining adoption as a transition approach from EMR.

By End Use, Hospitals Lead, While Ambulatory Surgical Centers Register Fastest Growth

Hospitals held the largest share of ~61.82% in 2025 due to advanced infrastructure, multidisciplinary teams, and complication management capabilities. Major centers across Japan, Germany, the UK, and the US drive global volumes. Ambulatory surgical centers are projected to grow at the highest CAGR of ~7.18% through 2035, supported by outpatient approvals, favorable reimbursement, and demand for same-day procedures. Specialty clinics accounted for ~12.47% in 2025, mainly in advanced Asian markets.

Endoscopic Submucosal Dissection Market Regional Highlights:

Asia Pacific Endoscopic Submucosal Dissection Market Insights:

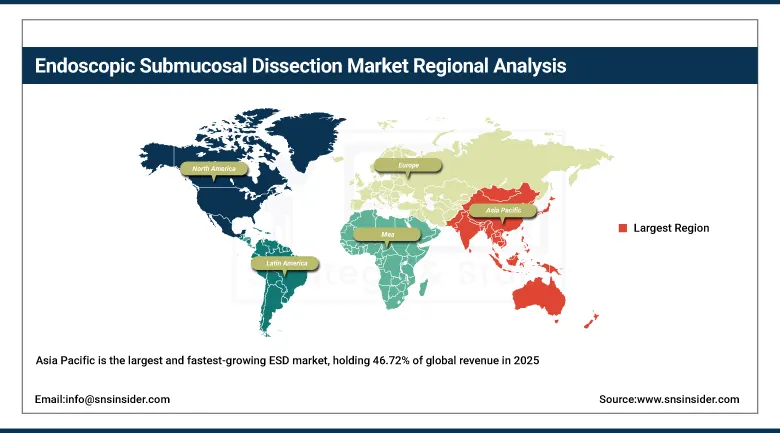

Asia Pacific is the largest and fastest-growing ESD market, holding 46.72% of global revenue in 2025 and projected to grow at a CAGR of 7.18% through 2035. Japan leads globally with national insurance coverage for gastric, esophageal, and colorectal ESD and the highest per-capita procedure rates. South Korea and China are the next-largest contributors, driven by high gastric cancer incidence, expanding screening programs, and growing domestic device manufacturing. India, Vietnam, and other emerging markets are expanding ESD training centers and procedure capacity alongside improving healthcare infrastructure and early GI cancer detection.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Endoscopic Submucosal Dissection Market Insights:

North America held 36.84% revenue share in 2025, supported by high healthcare spending, a growing advanced endoscopy workforce, strong equipment adoption, and increased colorectal cancer screening. The U.S. is seeing rising ESD adoption due to ASGE and ACG guideline support, expanding training programs, and increasing FDA clearances. Canada supports growth through expanded screening programs and investment in advanced endoscopy at cancer centers.

Europe Endoscopic Submucosal Dissection Market Insights:

Europe accounted for 11.63% of global revenue in 2025, with Germany, France, the UK, and Italy leading growth. The market benefits from ESGE guidelines supporting ESD for lesions >20 mm, expanded training programs, and improving reimbursement coverage. Cross-border training via the European Endoscopy Academy is accelerating adoption in Central and Eastern Europe, increasing demand for ESD tools and consumables.

Latin America (LATAM) and Middle East & Africa (MEA) Endoscopic Submucosal Dissection Market Insights:

LATAM and MEA are emerging markets driven by rising gastric and colorectal cancer incidence, improving infrastructure, and growing awareness of minimally invasive treatments. Brazil leads LATAM with expanding referral centers, while Mexico and Argentina contribute through private sector investment. In MEA, the UAE and Saudi Arabia lead due to trained specialists, government-funded hospital upgrades, and growing medical tourism in advanced endoscopy.

Endoscopic Submucosal Dissection Market Competitive Landscape:

Olympus Corporation (est. 1919) is the global leader in endoscopic submucosal dissection instrumentation, holding dominant positions across ESD knives, injection needles, gastroscopes, colonoscopes, and electrosurgical generators. Its ESD ecosystem, including the KD-650 series and HybridKnife platform co-developed with Erbe, along with its global distributor network and training infrastructure, sustains its position as the reference brand for ESD practitioners worldwide.

-

In November 2024, Olympus launched the EVIS X1 endoscopy system with enhanced texture and color enhancement imaging (TXI) and AI-integrated lesion detection optimized for ESD guidance, strengthening its leadership in advanced endoscopy.

Boston Scientific Corporation (est. 1979) is a global medical device company with expanding presence in advanced GI endoscopy and endoscopic resection. Its Resolution 360 Clip, Inject and Cut biliary and GI injection needle systems, and growing hemostasis portfolio are increasingly integrated into ESD workflows, supported by clinical development and physician education.

-

In June 2024, Boston Scientific received CE Mark for SpyGlass DS II Direct Visualization System expanded GI applications and advanced its ESD clip and tissue management line into European launch, reinforcing its position in endoscopic resection instrumentation.

FUJIFILM Holdings Corporation (est. 1934) is a major competitor in the ESD market with advanced imaging platforms, ESD-compatible gastroscopes and colonoscopes, and dissection accessories. Its Linked Color Imaging (LCI) and Blue Light Imaging (BLI) enhance mucosal visualization for precise lesion identification, with products available across Asia Pacific, Europe, and North America.

-

In February 2025, FUJIFILM received FDA clearance for the ELUXEO 7000 Series in the United States, featuring multi-light imaging and AI-assisted lesion characterization for ESD planning and real-time margin assessment, strengthening its position in North America.

Endoscopic Submucosal Dissection Market Key Players:

-

Olympus Corporation

-

FUJIFILM Holdings Corporation

-

Boston Scientific Corporation

-

Medtronic plc

-

Hoya Corporation (Pentax Medical)

-

Karl Storz SE & Co. KG

-

Cook Medical LLC

-

Micro-Tech Endoscopy

-

Erbe Elektromedizin GmbH

-

Sumitomo Bakelite Co., Ltd.

-

Medi-Globe GmbH

-

CONMED Corporation

-

Ovesco Endoscopy AG

-

Kaneka Corporation

-

Endo-Flex GmbH

-

Aohua Endoscopy Co., Ltd.

-

STERIS plc

-

Nanjing Micro-Tech Co., Ltd.

-

Hobbs Medical Inc.

-

Richard Wolf GmbH

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 390.88 million |

| Market Size by 2035 | USD 668.32 million |

| CAGR | CAGR of 5.51% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product (Gastroscopes & Colonoscopes, Knives, Injection Agents, Tissue Retractors, Graspers & Clips, and Others) • By Indication (Stomach Cancer, Colon Cancer, Esophageal Cancer, and Others) • By End Use (Hospitals, Ambulatory Surgical Centers (ASCs), Specialty Clinics, and Others) • By Technology (Hybrid ESD, Conventional ESD, and Underwater ESD) |

| Regional Analysis/Coverage | North America (U.S., Canada), Europe (Germany, France, UK, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America) |

| Company Profiles |

Olympus Corporation, FUJIFILM Holdings Corporation, Boston Scientific Corporation, Medtronic plc, Hoya Corporation (Pentax Medical), Karl Storz SE & Co. KG, Cook Medical LLC, Micro-Tech Endoscopy, Erbe Elektromedizin GmbH, Sumitomo Bakelite Co., Ltd., Medi-Globe GmbH, CONMED Corporation, Ovesco Endoscopy AG, Kaneka Corporation, Endo-Flex GmbH, Aohua Endoscopy Co., Ltd., STERIS plc, Nanjing Micro-Tech Co., Ltd., Hobbs Medical Inc., Richard Wolf GmbH |

Frequently Asked Questions

The Endoscopic Submucosal Dissection Market is driven by rising early-stage gastrointestinal cancer incidence, increasing preference for minimally invasive procedures, and advancements in ESD tools and AI-assisted endoscopy systems.

The Endoscopic Submucosal Dissection Market is expected to reach USD 668.32 million by 2035, growing steadily due to expanding global adoption and technological advancements.

Asia Pacific dominates the Endoscopic Submucosal Dissection Market due to high gastric cancer prevalence, established clinical guidelines, and widespread adoption of ESD procedures in countries like Japan, South Korea, and China.

The Endoscopic Submucosal Dissection Market is projected to grow at a CAGR of 5.51% from 2026 to 2035, supported by increasing training programs and expanding clinical applications.

Key trends in the Endoscopic Submucosal Dissection Market include the adoption of AI-integrated endoscopy, development of robotic-assisted ESD platforms, growing use of advanced injection agents, and expansion of outpatient endoscopy centers.

Get in Touch