Herbal Medicine Market Report Scope & Overview:

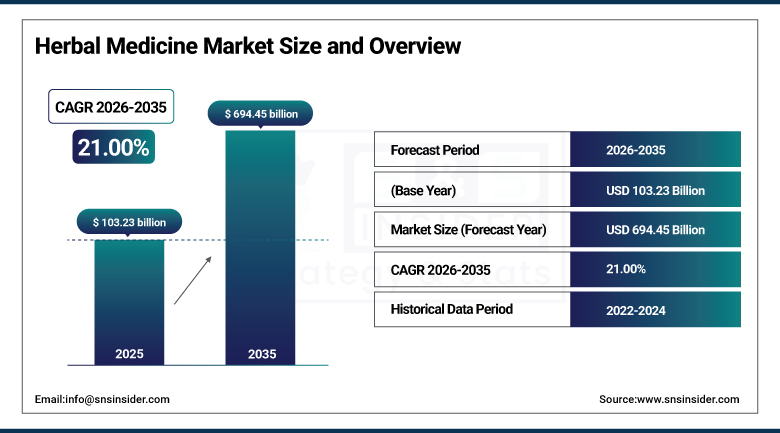

The Herbal Medicine Market was valued at USD 103.23 Billion in 2025 and is expected to reach USD 694.45 Billion by 2035, growing at a CAGR of 21.00% from 2026–2035.

The increasing use of natural medicines, herbal medicines, and botanicals in the global scenario leads to increased growth rate in the herbal medicines market. The increased use of both traditional herbal medicines and organic herbal medicines for chronic ailments will cause huge market growth, as per the WHO estimates that about 80% of the population depends on herbal medicines for health care. There has been an increasing demand for herbal medicines in the global environment which has also been reflected through regulation standardization, such as FDA guidelines on complementary and alternative medicine and EMA herbal monograph.

The WHO Global Centre for Traditional Medicine in India, which was set up in 2024, operates worldwide in the scientific validation of herbal medicines, fostering global integration and policy change within the field of traditional medicine. The prominent players in the industry such as Himalaya, Blackmores, and Nature's Bounty keep investing substantially in Ayurvedic medicine and Chinese herbal medication range.

Market Size and Forecast

-

Market Size in 2026E: USD 124.90 Billion

-

Market Size by 2035: USD 694.45 Billion

-

CAGR: 21.00% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Europe

To Get more information on Herbal Medicine Market - Request Free Sample Report

Herbal Medicine Market Trends

-

Increasing investment in phytopharmaceutical research and clinical studies is strengthening the scientific validation and global acceptance of herbal medicines.

-

Advances in extraction, formulation, and standardization technologies are improving the efficacy, safety, and shelf life of herbal medicine products.

-

Rapid growth of e-commerce and digital health platforms is expanding consumer access to herbal medicines across both developed and emerging markets.

-

Rising clinical trial activity for botanical therapeutics is accelerating product innovation and supporting evidence-based adoption of herbal treatments.

-

Manufacturers are expanding herbal product portfolios while investing in quality assurance and clinical substantiation to meet growing consumer demand and regulatory expectations.

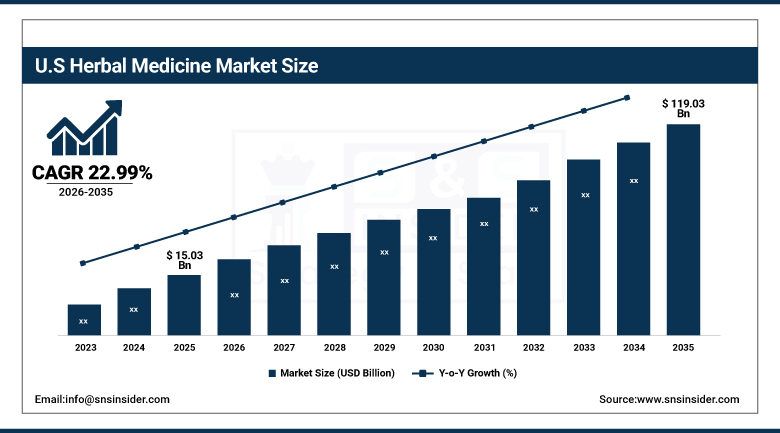

The U.S. Herbal Medicine Market Outlook

The U.S. herbal medicine market was valued at approximately USD 15.03 Billion in 2025 and is expected to reach approximately USD 119.03 Billion by 2035, growing at a CAGR of approximately 22.99%.

The market for herbal medicines in the USA is still being driven by increased knowledge about integrative healthcare and the change in strategy in the larger healthcare industry. Regulations such as those put forward by the FDA's guidelines on complementary and alternative medicine have ensured that more consumers become confident, while also making it easier to obtain regulatory approval for products. The continued growth of the market in North America has been driven by increased consumer expenditure of over USD 12 billion per year on dietary and herbal supplements.

The National Center for Complementary and Integrative Health, alongside broader FDA regulatory efforts, continues to increase consumer recognition and prompt further clinical research on herbal medical products. Credibility within the sector has been spurred, in part, by the increasing popularity of naturopathic treatment and its incorporation into wellness programs at institutions including the Mayo Clinic, reinforcing the U.S. market's position at the forefront of integrative healthcare adoption.

Herbal Medicine Market Segment Analysis

-

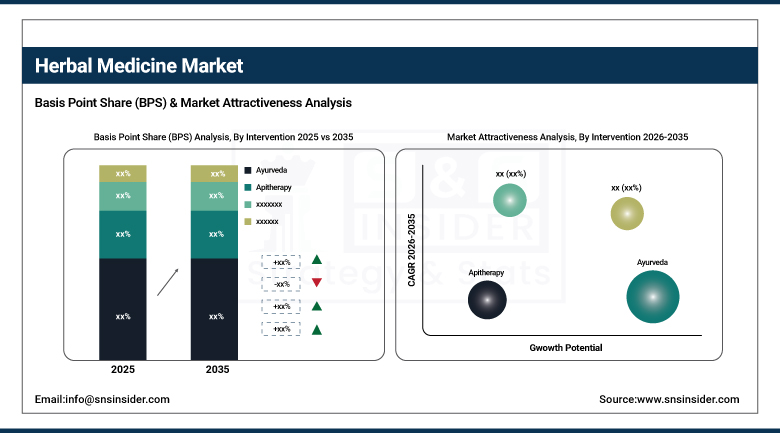

By Intervention, the ayurveda segment dominated the herbal medicine market with a 29.9% revenue share in 2025, while the apitherapy segment is the fastest growing category.

-

By Product Form, the tablets/capsules segment dominated the herbal medicine market with a 48.2% revenue share in 2025, while the powder segment is the fastest growing.

-

By Source, the roots segment dominated the herbal medicine market with a 42.03% revenue share in 2025, while the leaves segment is the fastest growing.

-

By Distribution Channel, the direct sales segment dominated the herbal medicine market with a 69.9% revenue share in 2025, while the e-sales segment is the fastest growing.

By Intervention, Ayurveda leads the market, Apitherapy registers the fastest growth

In 2025, Ayurveda had a considerable share of 29.9% in the market of herbal medicines due to the historical background, growing global awareness, and its inclusion into the health care systems of countries such as India. The methods of treatment using herbs have become popular due to their effectiveness in treating chronic diseases like stress, arthritis, metabolic issues, etc. Moreover, foreign firms are making investments in the development of Ayurvedic products.

Apitherapy is the most rapidly expanding intervention category, driven by increasing application of bee products including honey, propolis, and royal jelly within dermatology, immunological support, and wound healing. Growing consumer interest in natural, potent, multifaceted remedies continues to drive segment popularity, and scientific research demonstrating the anti-inflammatory and antibacterial properties of bee products continues to facilitate segment expansion within the broader herbal medicine market.

By Product Form, tablets and capsules dominate, powder registers the fastest growth

The tablets and capsules dosage forms were found to hold the maximum share of revenue at 48.2% in 2025 as a result of consumers' preference for their convenience of use, accurate dosing, portability, and extended shelf-life compared to traditional dosage forms such as decoctions. Both developed and developing countries have a preference for this dosage form, especially among the younger generation and professionals. Pharmaceutical and nutraceutical companies are producing their standardized formulations in this form.

The powder format is witnessing the highest growth on account of increasing use of the formats in functional foods, health beverages, and shakes. The consumer demand for natural and personalized health treatments is driving the demand for powders of ashwagandha, moringa, and turmeric, with the additional benefits of low processing, enhanced bioavailability, and economics adding to the popularity of the format.

By Source, roots dominate the market, leaves register the fastest growth

In the year 2025, roots will maintain a dominance in the market based on the sources, which constituted 42.03% of the total revenue. These roots were widely used in Chinese herbal medicines, Ayurveda medicines, and other traditional herbal medicines because of their efficacy due to their strong medicinal properties from their bioactive compounds, hence increasing consumer acceptance and tolerance and encouraging more industry growth through formulations of phytochemicals from roots.

Leaves represent the most rapidly growing source category, driven by increasing demand for neem, green tea, and moringa across skin care, detox, and metabolic products. Rich in antioxidants, leaves take many forms, including organic herbal products, tablets, and teas, with easier production and cultivation relative to roots enabling scale advantages that support growth across both mainstream and specialty botanical supplement channels.

By Distribution Channel, direct sales dominate, e-sales register the fastest growth

Direct sales formed the biggest market share of 69.9%, especially in rural and semi-urban areas where there is high consumer trust in the recommended herbal products for treatment by practitioners. Herbal clinics, health stores, and ayurvedic centers continue to be the main outlets of distribution because of the consumer preference of personalized consultations and products, with Dabur and Himalaya being some of the firms that have continued with direct sales.

E-sales represent the most rapidly expanding distribution channel, driven by increasing digitization and e-commerce growth that provides access to global brands, greater product variety, and doorstep delivery. Consumers increasingly prefer the convenience of accessing over-the-counter herbal drugs online, with health-oriented platforms including iHerb and Amazon Wellness transforming how consumers purchase botanical supplements and alternative medicine products, accelerating growth within this digital channel.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

Europe |

Germany |

32.0% |

|

North America |

United States |

78.0% |

|

Asia Pacific |

China |

39.0% |

|

Latin America |

Brazil |

37.0% |

|

Middle East & Africa |

South Africa |

28.0% |

North America Herbal Medicine Market Insights

The herbal medicine industry within North America continues to grow steadily, driven by the rising health consciousness, increased supply of herbal over-the-counter products, and the increasing use of organic herbal products, with the total annual expenditure of consumers for dietary and botanical supplements being in excess of USD 12 billion. Within North America, the United States forms the leading market for herbal medicines owing to the continued interaction of the FDA with the herbal medicines market.

Canada's diverse population and favorable regulatory environment under Health Canada's Natural Health Products Directorate continue to propel regional development, complementing the strong U.S. market position and supporting sustained North American growth throughout the forecast period.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Herbal Medicine Market Insights

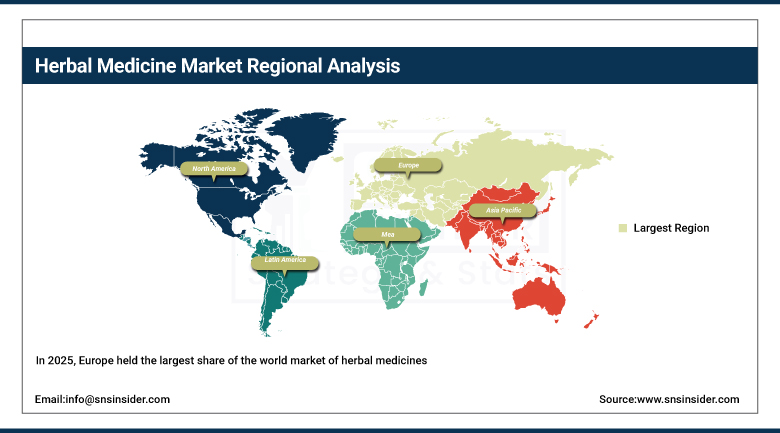

In 2025, Europe held the largest share of the world market of herbal medicines, due to the efficient legal framework, widespread usage of botanic supplements, and heightened awareness about the benefits of alternative medicine among the masses. The European Medicines Agency has set up the scientific framework regarding herbal medicinal products, thus raising the standard of products, with Germany holding the top position among the regions in the demand for herbs, owing to its rich tradition in using herb products.

More than 70% of Germans use herbal medicine, with phytopharmaceuticals widespread across both prescription and over-the-counter segments. France and UK provide similar examples of high consumption owing to the growing trend in buying natural cosmetics and organic herbal medicines, while Italy and Poland exhibit rising integration of traditional herbal medicines in treatment methods, strengthening their regional market dominance through successful European companies in the field of herbal medicines and research and development.

Asia Pacific Herbal Medicine Market Insights

Asia Pacific is the fastest-growing region in the herbal medicine market, driven by intensive cross-cultural integration of Japanese Kampo medicine, Chinese traditional therapy, and Ayurvedic therapy. Growing demand for plant-based pharmaceuticals in preventative medicine, government support, and rising R&D expenditure all contribute to sustained regional development, with India and China representing the two largest markets within the region.

The Indian market is favored due to the already existing infrastructure of Ayurveda complemented by the AYUSH initiatives supported by the government, and over 8,000 approved manufacturing facilities. In addition, the market potential of China is evident considering the fact that over 60 percent of the nation's population makes regular use of traditional Chinese medicine. The inclusion of herbal medicinal products in hospitals and health insurance systems is making their presence more widespread.

MEA & Latin America Herbal Medicine Market Insights

The Middle East, Africa, and Latin America region is experiencing steady growth in the herbal medicine market, driven by increasing urbanization, renewed interest in ethnobotanical methods, and expansion of retail outlets for herbal remedies. Influence of Brazil is quite large in Latin America due to its abundant biodiversity and the government’s involvement in incorporating traditional medicine in its healthcare sector, while Argentina is next due to the growing need for complementary medicine in connection with wellness tourism and community healthcare.

South Africa constitutes the biggest market in the MEA region due to the development of a robust domestic market for herbs and native treatment practices. With rising urbanization and retail infrastructure in both regions, further growth of the market is expected in the forecast period.

Market Dynamics

Growth Drivers: Expanding consumer acceptance and regulatory support fuel growth

Growing health consciousness, demand for plant-based remedies, and increasing awareness of the negative effects associated with synthetic medications continue to drive herbal medicine market growth. People are now using traditional herbal treatments for problems such as anxiety, inflammation, and gastro-intestinal issues, with many people having at least some experience with herbal supplementation products, showing that there is heavy dependence on these products by consumers.

Regulatory guidelines supportive of these objectives such as the WHO Traditional Medicine Strategy and simple registration procedures for traditionally used herbal medicines will still remain instrumental in bringing herbal products into healthcare systems. Some companies like Gaia Herbs and Nature's Way have been showing increasing interest in the herbal extracts market through product diversification and increasing efforts at clinical substantiation research, with an annual increase of 28% in global phytopharmaceutical studies in the last five years.

Restraints: Lack of standardization and scientific validation impede market growth

Though there have been remarkable advancements in the market performance of this sector, it still remains to be a victim of many difficulties due to standardization issues, low-quality products, and ineffective clinical verification of such herbs. Variations in terms of dose, safety, and effectiveness of herbs are mainly caused by the absence of global standardized regulation since most of these herbs enter the market without adequate information and regulatory control.

According to research carried out in 2022 by JAMA Internal Medicine, roughly 20% of OTC herbal supplements sold in the United States are contaminated with undeclared drugs, which continues to erode faith in these medications. Moreover, lack of funding for Chinese and Ayurvedic herbal medicines limits innovation and clinical research on them, whereas the intellectual property rights and the rules concerning biodiversity limit production of the herbs commercially.

Opportunities: Expanding scientific validation and e-commerce access create growth potential

The dramatic five- to ten-fold growth in clinical trials involving botanical supplements over the past decade represents a substantial opportunity for manufacturers positioned to develop scientifically validated herbal therapeutics. As phytopharmaceutical research funding continues to expand and regulatory bodies including the WHO Global Traditional Medicine Center work to standardize evidence-based herbal medicinal products globally, companies investing in rigorous clinical substantiation stand to capture growing market credibility and consumer trust.

Widening e-commerce access continues to present meaningful growth opportunity as well, particularly across metropolitan and emerging market regions where digital platforms are extending herbal product availability beyond traditional retail and practitioner-based distribution channels. As the global supply chain continues to grow and as the digital health platforms offer more botanical supplements, companies that take advantage of this trend have a chance of gaining considerable demand during the forecast period.

Recent Developments:

-

2024: Established in India in 2024, the WHO Global Traditional Medicine Center began operating globally in the scientific authentication of herbal medicinal products, promoting international integration and policy reform.

-

2024: In August 2024, herbal medicine manufacturer Pascoe Naturmedizin partnered with SNP to transition its ERP system to SAP S/4HANA, aiming to enhance operational efficiency and support future scalability.

-

2025: A 2025 study published in Frontiers in Pharmacology revealed a five- to ten-fold growth in clinical trials involving botanical supplements over the past decade, reflecting firm R&D expansion across the market.

Herbal Medicine Market key players are:

-

Sheng Chang Pharmaceutical Co., Ltd.

-

Nordic Nutraceuticals (Oy Verman Ab)

-

AYUSH Ayurvedic Pte Ltd.

-

Herbal Hills

-

Herb Pharm

-

LKK Health Products Group

-

International Chinese Body Care Houses

-

KindCare Medical Center

-

Pascoe Natural Medicine

-

Bionorica SE

-

Ming Chen Clinic

-

The Center for Natural and Integrative Medicine

-

Sinomedica

-

Himalaya Wellness Company

-

Blackmores Limited

-

Nature's Bounty Co.

-

Dabur India Limited

-

Gaia Herbs

-

Nature's Way Products, LLC

-

Arizona Natural Products

Herbal Medicine Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 103.23 Billion |

| Market Size by 2035 | USD 694.45 Billion |

| CAGR | CAGR of 21.00% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Intervention (Ayurveda, Apitherapy, Naturopathic Medicine, Traditional Chinese Medicine, Traditional Korean Medicine, Traditional Japanese Medicine, Others) • By Product Form (Powder, Liquid/Gel, Tablets/Capsules, Others) • By Source (Barks, Leaves, Roots, Others) • By Distribution Channel (Direct Sales, E-sales) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Sheng Chang Pharmaceutical Co., Ltd., Nordic Nutraceuticals (Oy Verman Ab), AYUSH Ayurvedic Pte Ltd., Herbal Hills, Herb Pharm, LKK Health Products Group, International Chinese Body Care Houses, KindCare Medical Center, Pascoe Natural Medicine, Bionorica SE, Ming Chen Clinic, The Center for Natural and Integrative Medicine, Sinomedica, Himalaya Wellness Company, Blackmores Limited, Nature's Bounty Co., Dabur India Limited, Gaia Herbs, Nature's Way Products, LLC, Arizona Natural Products |

Frequently Asked Questions

Europe dominated the Herbal medicine market.

The market continues to be plagued by serious issues due to poor standardization, inconsistent product quality, and inadequate clinical verification.

Growing consciousness of health, demand for vegetable remedies, and knowledge of the negative effects of synthetic medications drive the herbal medicine market share forward.

The market is expected to reach USD 391.59 billion by 2032, increasing from USD 85.31 billion in 2024.

The Herbal medicine market is anticipated to grow at a CAGR of 21% from 2025 to 2032.

Get in Touch