Energy Storage Market Report Scope & Overview:

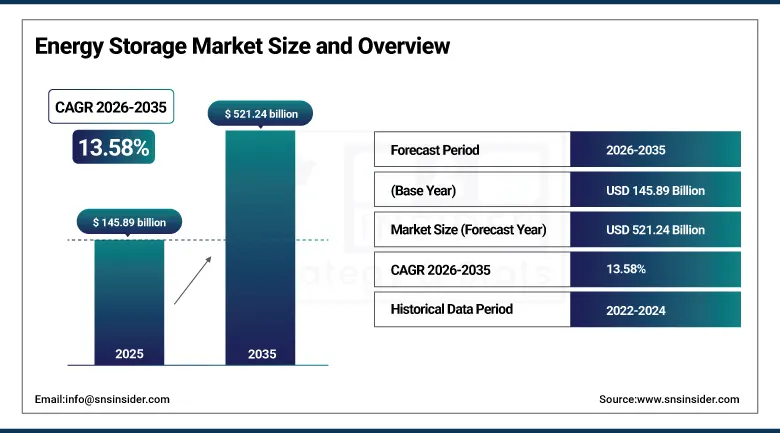

The Energy Storage Market was valued at USD 145.89 billion in 2025 and is expected to reach USD 521.24 billion by 2035, growing at a CAGR of 13.58% from 2026–2035.

The global energy storage market is at the epicentre of the clean energy transition, serving as the critical enabling technology that determines whether the world’s accelerating deployment of variable renewable electricity generation from solar photovoltaic and wind resources can translate into reliable, dispatchable power supply at the grid scale. Battery manufacturing scale-up is driving lithium-ion battery pack costs below USD 100 per kWh, while policy support across the U.S. Inflation Reduction Act, EU Battery Regulation, and China’s 14th Five-Year Plan is directing hundreds of billions in capital toward storage capacity development. CATL’s unveiling of the TENER Stack 9 MWh ultra-large energy storage system in May 2025 and Tesla’s September 2025 Megablock launch with 23% faster setup and 40% lower construction costs collectively illustrate the product innovation acceleration that is simultaneously improving storage performance and reducing deployment economics across the segments that define the market’s growth frontier.

The IEA’s World Energy Outlook 2025 projection that grid-scale battery storage capacity must grow to 1,500 GWh globally by 2030 under its Net Zero Emissions scenario, compared to approximately 280 GWh operational at end-2024, defines both the extraordinary investment scale that the energy storage market must sustain and the commercial opportunity that manufacturers, developers, and system integrators are competing to capture across every dimension of the storage value chain.

Market Size and Forecast

-

Market Size in 2026E: USD 165.69 Billion

-

Market Size by 2035: USD 521.24 Billion

-

CAGR (2026-2035): 13.58%

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get more information on Energy Storage Market - Request Free Sample Report

Energy Storage Market Trends

-

Accelerating deployment of long-duration energy storage technologies including flow batteries, compressed air energy storage, gravity storage, and thermal storage systems that can economically discharge energy over 6 to 100-hour windows, addressing the multi-day renewable intermittency challenge.

-

Growing integration of AI and advanced energy management software within battery energy storage systems that optimise charge and discharge scheduling across multiple simultaneous revenue streams including frequency regulation, peak shaving, arbitrage, and capacity market participation, improving the blended revenue realisation of deployed storage assets.

-

Rapid expansion of co-located solar-plus-storage and wind-plus-storage project development, as the combination of renewable generation and on-site storage enables developers to offer firmed renewable power products to offtakers under power purchase agreements.

-

Rising adoption of second-life battery repurposing programmes that recover used electric vehicle battery packs whose state-of-health has declined below automotive performance requirements but remains commercially viable for stationary energy storage applications.

-

Growing development of sodium-ion battery technology as a commercially competitive alternative to lithium-ion for stationary energy storage applications, as sodium’s abundance and lower extraction environmental impact combined with advancing cell chemistry performance metrics.

The U.S. Energy Storage Market Outlook

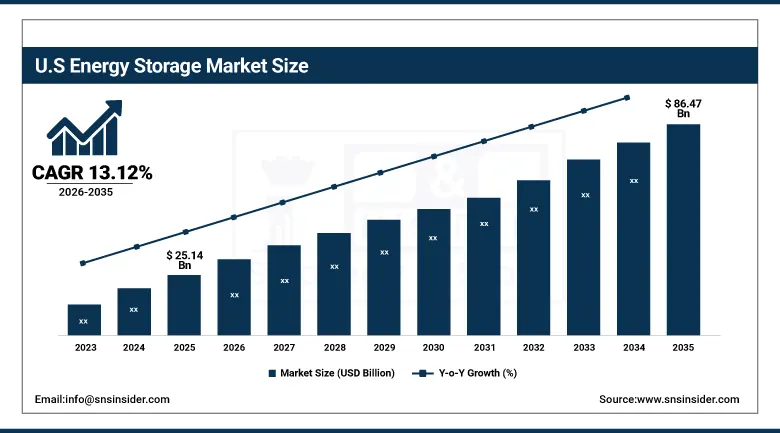

The U.S. energy storage market was valued at approximately USD 25.14 billion in 2025 and is expected to reach approximately USD 86.47 billion by 2035, growing at a CAGR of 13.12%.

The United States energy storage market is defined by the extraordinary commercial momentum created by the IRA’s 30% Investment Tax Credit for standalone storage, which eliminated the previous requirement that storage must be paired with co-located renewable generation to qualify for federal tax incentives and dramatically expanded the addressable storage development pipeline. California, Texas, and the Southwest are leading U.S. storage deployment as regions whose combination of high renewable penetration, favourable solar irradiation, and progressive renewable energy mandates creates the most commercially active storage procurement environment. The U.S. residential storage market is simultaneously experiencing rapid growth driven by the IRA’s residential clean energy credit covering battery storage installation costs alongside solar equipment, combined with growing consumer awareness of energy independence and grid resilience motivations following major weather-related grid outages.

Tesla’s September 2025 launch of the Megablock utility-scale storage system, claiming 23% faster installation times and 40% lower construction costs through modular stacking architecture and simplified site preparation requirements, represents a direct commercial response to the cost pressure that the IRA-driven U.S. utility storage procurement market is creating and demonstrates the product innovation velocity that the U.S. market’s scale and competitiveness is generating across the global storage technology supply chain.

Energy Storage Market Segment Analysis

-

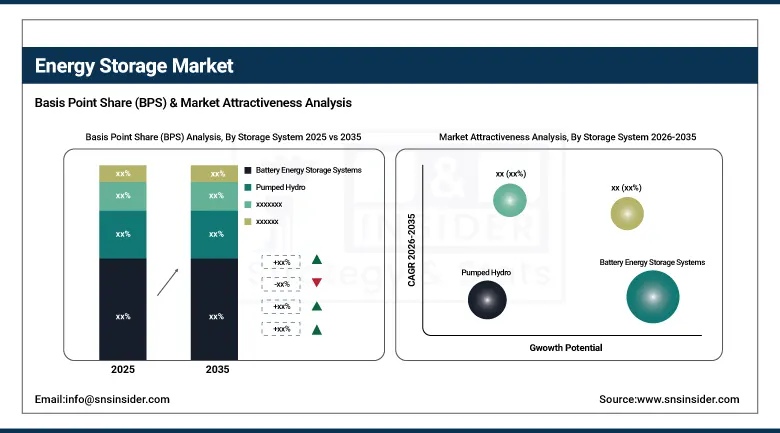

By storage system, battery energy storage systems (BESS) dominated the market with approximately 52.34% share in 2025; electrochemical capacitors are the fastest-growing segment at a CAGR of approximately 7.20%.

-

By battery type, lithium-ion batteries led the market with approximately 48.67% share in 2025; flow batteries are the fastest-growing battery type at a CAGR of approximately 8.14%.

-

By application, utility-scale storage dominated the market with approximately 50.21% share in 2025; residential storage is the fastest-growing application at a CAGR of approximately 7.50%.

By Storage System, BESS dominates, electrochemical capacitors grow fastest

Battery energy storage systems retained the dominant storage system position with approximately 52.34% of the energy storage market in 2025, a dominance reflecting the extraordinary commercial momentum of lithium-ion battery technology whose manufacturing scale-up across Chinese, Korean, Japanese, and U.S. gigafactories has driven system costs below the commercial viability thresholds required for utility-scale grid applications, residential solar-plus-storage deployments, and commercial and industrial peak management installations. CATL’s May 2025 TENER Stack 9 MWh ultra-large energy storage system, Tesla’s September 2025 Megablock promising 40% lower construction costs, and BYD’s MC Cube battery storage system collectively represent competitive intensity in utility BESS product innovation whose pace consistently expands the commercial use cases where BESS outcompetes alternative storage technologies on a levelised cost basis. Pumped hydro storage retains a meaningful share of total installed energy storage capacity globally given the decades of existing amortised infrastructure, but new pumped hydro development’s multi-decade construction timelines, geographic site constraints, and environmental permitting complexity mean it cannot contribute meaningfully to the new storage capacity additions that the energy transition timeline requires.

Electrochemical capacitors are the fastest-growing storage system segment at a CAGR of approximately 7.20% through 2035, propelled by the growing demand for ultra-fast power response storage applications including grid frequency regulation, power quality conditioning, electric vehicle regenerative braking energy capture, and short-duration industrial power backup where capacitors’ millisecond-to-second charge and discharge capability and virtually unlimited cycle life without capacity degradation provide performance advantages that battery chemistry alternatives cannot match. The proliferation of grid-connected renewable energy at increasingly high penetration rates is creating growing frequency regulation and voltage support requirements that electrochemical capacitor systems can address with higher round-trip efficiency and longer operational life than equivalent battery systems deployed for the same high-frequency cycling applications.

By Battery Type, lithium-ion batteries dominate, flow batteries grow fastest

Lithium-ion batteries retained the dominant battery type position with approximately 48.67% of the energy storage market in 2025, anchored by their position as the global standard chemistry for utility-scale BESS, commercial and industrial peak management, and residential solar-plus-storage applications that collectively constitute the majority of current energy storage revenue. The commercial competitiveness of lithium-ion for stationary storage is reinforced by the development of lithium iron phosphate chemistry variants whose superior thermal stability, cycle life, and safety profile relative to earlier NMC chemistries makes them the preferred choice for stationary storage applications where the energy density advantage of NMC provides less commercial value than LFP’s safety, cycle life, and operational simplicity advantages.

Flow batteries are the fastest-growing battery type at a CAGR of approximately 8.14% through 2035, driven by the growing recognition among utility grid operators and renewable energy developers that the multi-hour discharge capability, independent power and energy capacity sizing, and long calendar life of flow battery systems provide compelling advantages over lithium-ion for long-duration energy storage applications that accelerating renewable penetration is making increasingly commercially necessary. Vanadium redox flow batteries from market leaders including Invinity Energy Systems, VRB Energy, and Sumitomo Electric are demonstrating 20-year plus operational life, unlimited cycle capacity without degradation, and full depth of discharge capability in utility deployments that provide verifiable evidence of the total cost of ownership advantages over lithium-ion in high-cycle-frequency, long-duration applications.

By Application, utility-scale storage leads, residential grows fastest

Utility-scale storage retained the dominant application position with approximately 50.21% of the energy storage market in 2025, driven by the extraordinary scale of grid-connected battery storage procurement being executed by utilities, independent power producers, and grid operators in response to renewable energy integration requirements creating frequency regulation, voltage support, peak capacity, and multi-hour energy time-shifting service demands. The utility-scale storage market’s commercial development is driven by competitive procurement dynamics of organised wholesale electricity markets where storage operators can stack revenue across multiple services simultaneously, with optimised dispatch algorithms enabling utility-scale BESS to earn revenues from frequency regulation, energy arbitrage, capacity market participation, and ancillary services in combinations that make large-scale storage project economics compelling without reliance on any single revenue stream.

Residential storage is the fastest-growing application at a CAGR of approximately 7.50% through 2035, propelled by the falling total installed cost of residential battery storage systems led by Tesla Powerwall, sonnen, Enphase Energy, and LG Energy Solution whose per-kWh costs are progressively approaching the levels where storage economics are compelling on the basis of electricity bill savings alone. The growing frequency and severity of grid outages driven by extreme weather events is creating a resilience-driven demand motivation that supplements the economics-based investment rationale for residential storage, as homeowners who experience prolonged outages develop lasting prioritisation of energy backup capability that sustains storage purchasing decisions even when electricity tariff structures do not independently justify the investment.

Regional Analysis

|

Region |

Major Country |

Share Within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

87.4% |

|

Europe |

Germany |

22.3% |

|

Asia Pacific |

China |

61.7% |

|

Middle East & Africa |

Saudi Arabia |

38.4% |

|

Latin America |

Brazil |

44.2% |

North America Energy Storage Market Insights

North America is a rapidly growing and commercially sophisticated energy storage market primarily driven by the transformative impact of the U.S. IRA’s standalone storage tax credit that has made the United States the world’s second-largest and fastest-growing market for grid-scale battery storage deployment outside Asia Pacific. The United States accounts for approximately 87.4% of North American energy storage revenues through its combination of IRA policy incentives, the most commercially active utility procurement market globally, a rapidly growing residential and commercial storage sector, and domestic manufacturing investment by Tesla, Fluence, Stem, and international suppliers establishing U.S. production capacity to qualify for IRA domestic content requirements. Canada contributes approximately 12.6% of North American revenues through significant provincial renewable energy development programmes and growing provincial utility storage procurement.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Energy Storage Market Insights

Europe is the world’s third-largest energy storage market where the EU’s REPowerEU programme targets, grid flexibility needs from rapidly growing variable renewable generation, and the EU Battery Regulation’s supply chain sustainability requirements are creating both strong demand and distinctive commercial characteristics. Germany accounts for approximately 22.3% of European energy storage revenues through the world’s most successful residential solar-plus-storage market whose combination of high electricity prices, generous historical solar subsidies, and cultural willingness to invest in energy independence has created the world’s largest residential battery storage installed base, alongside a growing utility-scale storage market responding to Germany’s rapid renewable energy buildout. The European energy storage market’s EU Battery Regulation carbon footprint declaration and due diligence requirements are creating competitive differentiation pressure on battery manufacturers whose supply chains can demonstrate lower carbon intensity and responsible sourcing.

Asia Pacific Energy Storage Market Insights

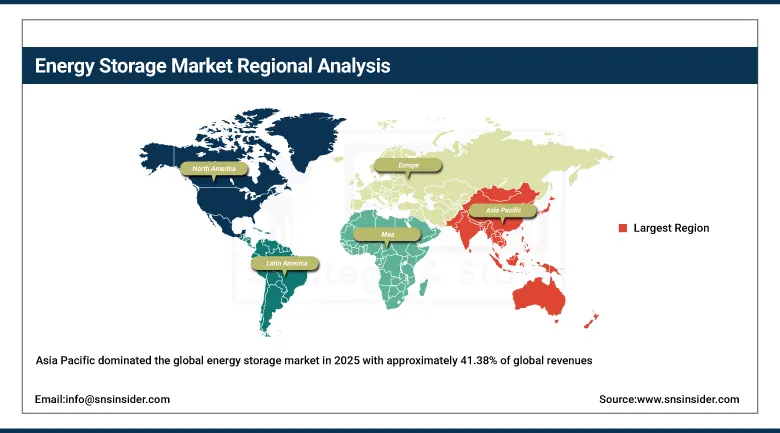

Asia Pacific dominated the global energy storage market in 2025 with approximately 41.38% of global revenues and is simultaneously projected to grow at the fastest CAGR of approximately 14.01% through 2035, driven by China’s extraordinary combination of the world’s largest battery manufacturing industry, the most aggressive utility-scale renewable energy deployment programme globally, and national policy support including mandatory storage quotas for new renewable energy projects that generate institutional storage procurement volumes unmatched by any other national market. China accounts for approximately 61.7% of Asia Pacific energy storage revenues through the combined effect of the world’s largest renewable energy development pipeline creating storage demand, domestic battery manufacturers including CATL, BYD, EVE Energy, and CALB supplying the most competitive lithium-ion cells globally, and government policy incentives directing public and private investment toward grid-scale storage capacity expansion. Japan, South Korea, India, and Australia represent secondary Asia Pacific markets whose combination of high renewable energy ambition, grid modernisation investment, and domestic battery industry development is creating growing storage deployment volumes that contribute meaningfully to the region’s market leadership position.

Latin America and MEA Energy Storage Market Insights

Latin America and the Middle East and Africa are rapidly developing energy storage markets where extraordinary solar resource availability, rapidly falling renewable and storage costs, and the economic and energy security benefits of reducing fossil fuel generation dependency are creating growing storage market development. Brazil accounts for approximately 44.2% of Latin American revenues through utility-scale BESS procurement supporting wind and solar integration, a growing residential and commercial solar-plus-storage market, and government energy security policy identifying domestic storage deployment as a strategic infrastructure priority. Saudi Arabia leads Middle East and Africa revenues at approximately 38.4% of the regional total, driven by Vision 2030’s renewable energy programme targeting 50% renewable electricity by 2030 requiring utility-scale storage to firm generation capacity and NEOM’s ambition to operate on 100% renewable energy requiring substantial grid-scale storage infrastructure.

Market Dynamics

Growth Drivers: Accelerating renewable energy deployment creating grid-scale storage procurement demand

The primary structural growth drivers for the energy storage market are the renewable energy deployment acceleration creating grid flexibility needs at a scale and urgency only addressable through storage capacity additions, combined with the policy support frameworks in the U.S., EU, China, and India providing investment certainty and financial incentive support across all deployment scales. Battery manufacturing cost trajectories are simultaneously improving storage economics at an annual rate that consistently reduces the breakeven capital cost threshold below which storage investment is commercially rational across an expanding range of applications, creating a self-reinforcing cycle where lower costs enable new commercial applications whose market development generates manufacturing volume driving further cost reduction.

Restraints: Critical mineral supply chain constraints creating battery material cost and availability risk

A significant restraint on the energy storage market is the critical mineral supply chain dependency characterising lithium-ion battery manufacturing, where the concentration of lithium, cobalt, nickel, and manganese production and processing in a small number of countries creates supply chain concentration risk that has manifested as price volatility and availability constraints during periods of demand acceleration. Grid interconnection queue delays represent a persistent operational restraint in developed markets where the volume of generation and storage project applications has grown faster than the grid operator staffing and process infrastructure needed to assess and approve them, creating multi-year delays between investment decision and commercial operation.

Opportunities: Long-duration storage market development for grid decarbonisation, second-life battery market creating lower-cost residential storage supply

Long-duration energy storage represents the most commercially significant untapped opportunity in the global energy storage market, as the resolution of multi-day renewable intermittency challenges creates a commercially addressable market for flow batteries, compressed air energy storage, hydrogen-coupled storage, gravity storage, and thermal storage technologies whose combined potential deployment scale vastly exceeds current commercial activity and whose development is being actively supported by dedicated public funding programmes including the U.S. DOE’s Long Duration Storage Shot initiative.

Recent Developments

-

2025: Tesla launched the Megablock utility-scale energy storage system in September 2025, claiming 23% faster installation times and 40% lower construction costs through modular stacking architecture and simplified site preparation, targeting the growing utility-scale storage procurement market where construction cost and schedule certainty are critical procurement criteria.

-

2025: CATL unveiled the TENER Stack 9 MWh ultra-large energy storage system in May 2025, designed as a mass-producible utility-scale storage platform that significantly improves volume utilisation and energy density relative to previous system generations, providing project developers with a standardised high-capacity storage module.

-

2025: Fluence Energy expanded its partnership portfolio with major utility clients across North America and Europe, deploying its AI-powered Mosaic software platform across its installed BESS fleet to optimise dispatch across multiple revenue streams simultaneously.

Energy Storage Market Key Players are:

-

CATL (Contemporary Amperex Technology Co. Limited)

-

Tesla Energy Inc.

-

BYD Company Limited

-

Fluence Energy Inc.

-

LG Energy Solution Ltd.

-

Samsung SDI Co., Ltd.

-

Panasonic Corporation

-

ABB Ltd.

-

Siemens Energy AG

-

GE Vernova Inc.

-

Honeywell International Inc.

-

sonnen GmbH (Shell)

-

Enphase Energy Inc.

-

Stem Inc.

-

Invinity Energy Systems plc

-

Eaton Corporation plc

-

Schneider Electric SE

-

EVE Energy Co., Ltd.

-

CALB Group Co., Ltd.

-

SolarEdge Technologies Inc.

Energy Storage Market Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 145.89 Billion |

| Market Size by 2035 | USD 521.24 Billion |

| CAGR | CAGR of 13.58% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Storage System (Battery Energy Storage Systems (BESS), Pumped Hydro, Flywheel Energy Storage, Compressed Air Energy Storage, Electrochemical Capacitors, Others) • By Battery Type (Lithium-Ion Batteries, Flow Batteries, Lead-Acid Batteries, Sodium-Ion Batteries, Others) • By Application (Utility-Scale Storage, Commercial & Industrial Storage, Residential Storage) • By End User (Utilities, Residential, Commercial & Industrial) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | CATL (Contemporary Amperex Technology Co. Limited), Tesla Energy Inc., BYD Company Limited, Fluence Energy Inc., LG Energy Solution Ltd., Samsung SDI Co., Ltd., Panasonic Corporation, ABB Ltd., Siemens Energy AG, GE Vernova Inc., Honeywell International Inc., sonnen GmbH (Shell), Enphase Energy Inc., Stem Inc., Invinity Energy Systems plc, Eaton Corporation plc, Schneider Electric SE, EVE Energy Co., Ltd., CALB Group Co., Ltd., SolarEdge Technologies Inc. |

Frequently Asked Questions

Asia Pacific dominated the energy storage market in 2025, accounting for approximately 41.38% of global revenues, with China as the leading national market.

Battery Energy Storage Systems (BESS) dominated with approximately 52.34% revenue share in 2025.

The accelerating global deployment of variable renewable energy creating grid flexibility requirements that only storage can address at scale, combined with the IRA and equivalent policy frameworks.

The energy storage market was valued at USD 145.89 billion in 2025.

The energy storage market is expected to grow at a CAGR of 13.58% from 2026 to 2035.

Get in Touch