Engineered Quartz Surface Market Report Scope & Overview:

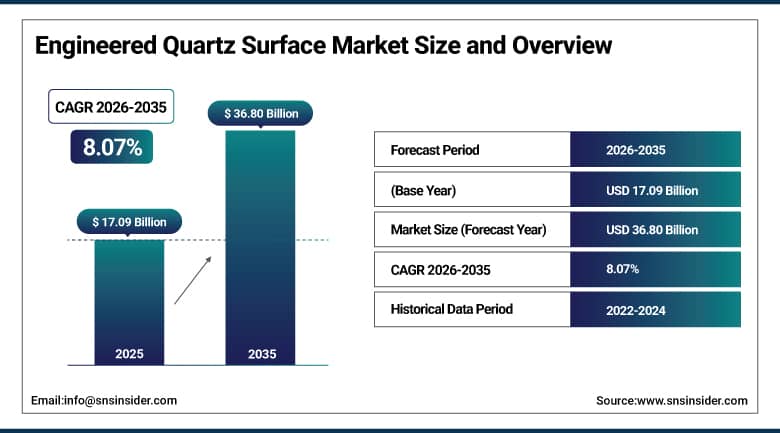

The Engineered Quartz Surface Market was valued at USD 17.09 Billion in 2025 and is expected to reach USD 36.80 Billion by 2035, growing at a CAGR of 8.07% from 2026 to 2035.

The engineered quartz surface market is experiencing robust structural transformation driven by rising residential and commercial construction activity and growing consumer preference for low-maintenance premium surfacing materials. It is increasingly displacing natural stone, solid surfaces, and laminates across kitchen countertops, bathroom vanities, flooring, and wall cladding applications worldwide. Engineered quartz is produced using the Bretonstone process, combining around 90–93% crushed quartz with polyester resins, pigments, and additives under vacuum vibrocompression. This results in a non-porous, durable surface offering high scratch, stain, and impact resistance, along with superior design consistency and color uniformity required for large-scale architectural and commercial interior projects.

In 2025, global engineered quartz surface demand was strongly supported by government housing programs and large-scale infrastructure investments across key regions. In the United States, the Infrastructure Investment and Jobs Act (IIJA), with USD 550 billion allocated, continued to drive residential, commercial, and public infrastructure construction, boosting demand for interior materials. In India, the Pradhan Mantri Awas Yojana accelerated urban housing development toward its 10 million-unit target. These initiatives sustained strong construction pipelines supporting quartz adoption in interiors. Leading manufacturers such as Cosentino, Caesarstone, and Compac expanded sustainable portfolios with low-VOC resins and recycled quartz aligned with global green building certification standards.

Market Size and Forecast:

-

Market Size in 2026E: USD 18.30 Billion

-

Market Size by 2035: USD 36.80 Billion

-

CAGR: 8.07% from 2026 to 2035

-

Fastest Growing Region: Asia Pacific

-

Largest Region: Asia Pacific

To Get More Information On Engineered Quartz Surface Market - Request Free Sample Report

Engineered Quartz Surface Market Trends:

-

Large engineered quartz slabs improve aesthetics by reducing seams and increasing adoption in premium commercial interior hospitality and retail spaces.

-

Growing demand for marble-like quartz is driving investment in digital printing and advanced pigment dispersion technologies.

-

Increasing healthcare adoption of engineered quartz is driven by non-porous, hygienic surfaces and compatibility with strict disinfection protocols.

-

Online quartz distribution expansion improves sample ordering, visualization tools, and direct procurement, reshaping traditional supply chains and market access.

-

Growing sustainability regulations are driving recycled quartz, bio-based resins, and certified products for green building standards like LEED and BREEAM.

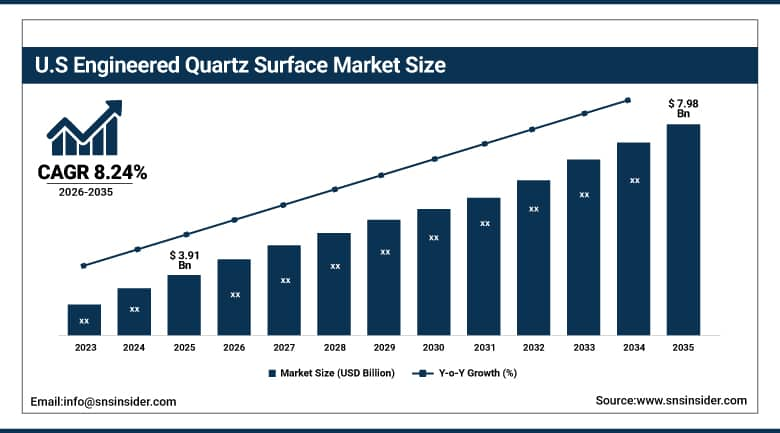

U.S. Engineered Quartz Surface Market Outlook:

The U.S. Engineered Quartz Surface Market was valued at approximately USD 3.91 Billion in 2025 and is expected to reach approximately USD 7.98 Billion by 2035, growing at a CAGR of approximately 8.24%.

The United States is the largest national market for engineered quartz surfaces, driven by the scale of its residential remodeling and new construction sectors and a highly developed kitchen and bath trade channel. Engineered quartz has become a preferred countertop material across entry-level homes, mid-market housing, and luxury custom residences due to its durability and design versatility. Federal housing programs, including the U.S. Department of Housing and Urban Development’s HOME Investment Partnerships Program and Housing Choice Voucher initiatives, support ongoing residential construction and renovation activity. These programs sustain consistent demand across commodity and mid-tier quartz product segments, reinforcing long-term market stability and growth.

The U.S. National Association of Home Builders, in collaboration with the Home Innovation Research Labs, launches updated residential construction material specification benchmarking data in 2025 confirming that new engineered quartz had displaced granite as the most commonly specified new residential kitchen countertop material in the United States for the third consecutive year, with quartz specified in approximately 41% of new single-family home kitchen countertop installations compared with granite's 29% share. This trend is further reinforced by HUD Affordable Housing Programs, including the HOME Investment Partnerships and Housing Choice Voucher initiatives, which are driving residential renovation and new housing developments, strengthening demand across builder and remodeling channels for quartz surface manufacturers such as Cosentino, Caesarstone, Cambria, and MSI Surfaces.

Engineered Quartz Surface Market Segment Analysis:

-

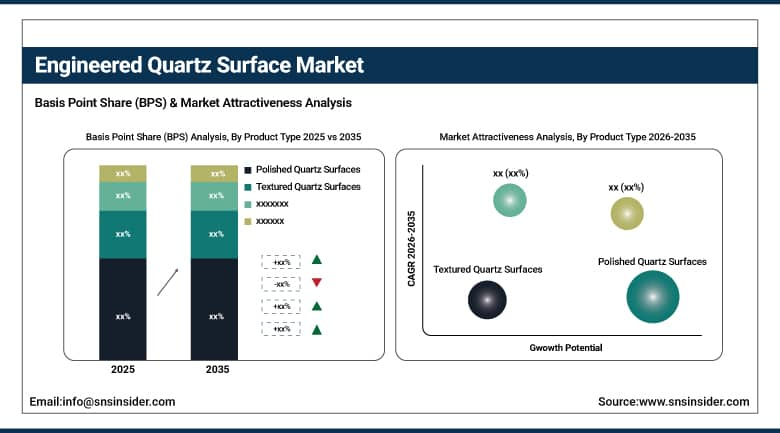

By Product Type, the polished quartz surfaces segment dominated the engineered quartz surface market with 60.18% share in 2025, while the premium designer quartz slabs segment is the fastest growing product type with the highest CAGR of 9.63% from 2026 to 2035.

-

By Application, the residential construction segment dominated the engineered quartz surface market with 55.13% share in 2025, while the commercial construction segment is the fastest growing application with CAGR of 9.24% during 2026 to 2035.

-

By End-Use Area, the kitchen countertops segment dominated the engineered quartz surface market with 45.48% share in 2025, while the table tops & furniture surfaces segment is the fastest growing end-use area with CAGR of 9.90% during 2026 to 2035.

-

By Distribution Channel, the direct sales segment dominated the engineered quartz surface market with 40.42% share in 2025, while the online/e-commerce channels segment is the fastest growing distribution channel with CAGR of 9.98% during 2026 to 2035.

By Product Type, polished quartz surfaces dominate, premium designer quartz slabs grow fastest

Polished quartz surfaces accounted for 60.18% of engineered quartz surface market revenue in 2025, reflecting the strong dominance of high-gloss finishes across residential and commercial applications. This finish remains the default specification for kitchen countertops, bathroom vanities, and interior surfaces due to its reflective quality, color depth, and broad affordability across mid-market and premium segments. Its durability, stain resistance, and ease of maintenance further reinforce its widespread adoption. While matte and leather finishes are gaining traction in premium residential and hospitality projects for their differentiated aesthetics, polished quartz continues to lead global demand due to its established design preference and versatility.

Premium designer quartz slabs represent the fastest-growing product type segment in the engineered quartz surface market, driven by increasing demand for luxury and customized interior solutions. The segment benefits from adoption of jumbo-format slabs featuring digitally reproduced marble veining, book-matched patterns, and metallic pigment enhancements. These designs are widely specified in luxury residential renovations, high-end hospitality spaces, spa environments, premium retail stores, and corporate headquarters interiors. Such applications prioritize aesthetic differentiation, architectural uniqueness, and brand-driven design identity. Premium quartz slabs offer enhanced visual appeal and performance benefits, enabling manufacturers to capture higher margins compared to standard polished quartz offerings globally.

By Application, residential construction dominates, commercial construction grows fastest

Residential construction accounted for 55.13% of engineered quartz surface application revenue in 2025, highlighting its dominant role in global demand. This leadership is driven by the widespread adoption of engineered quartz as a preferred material for kitchen countertops and bathroom vanities across North America, Europe, and Asia. Its durability, hygienic properties, and design flexibility have enabled it to replace natural granite, solid surfaces, and ceramic tiles across all housing segments, from affordable to luxury homes. Ongoing urbanization, household formation growth, and government-backed affordable housing initiatives continue to support residential construction activity, reinforcing consistent demand for engineered quartz surfaces globally.

Commercial construction represents the fastest-growing application segment in the engineered quartz surface market, driven by expanding investments in hospitality, retail, office, healthcare, and institutional infrastructure projects worldwide. Increasing demand for durable, low-maintenance, and aesthetically premium interior surfaces in high-traffic environments is accelerating quartz adoption across commercial interiors. Large-scale hotel developments, shopping malls, corporate headquarters, and public infrastructure projects are key contributors to growth. Rising urbanization, global tourism recovery, and government-backed infrastructure modernization programs further support commercial construction activity. The segment benefits from design standardization and bulk procurement, reinforcing strong demand momentum for engineered quartz surfaces across global commercial applications.

By End-Use Area, kitchen countertops dominate, table tops & furniture surfaces grow fastest

Kitchen countertops accounted for 45.48% of engineered quartz end-use revenue in 2025, highlighting their dominant role in global market demand. This segment forms the commercial foundation of the engineered quartz industry due to its strong alignment with key performance requirements such as heat resistance, scratch resistance, stain resistance, and non-porous surface properties. These characteristics have enabled engineered quartz to replace natural stone, laminate, and solid surfaces across residential and commercial kitchens. Additionally, the kitchen is a key focus in home renovation and property value enhancement decisions, further strengthening its leadership position across global residential and commercial interior applications.

Table tops and furniture surfaces represent the fastest-growing end-use segment in the engineered quartz market, driven by increasing adoption across residential, commercial, and hospitality interiors. Engineered quartz is increasingly specified for dining tables, coffee tables, office desks, and retail display fixtures due to its superior durability, scratch resistance, and dimensional stability. Its design versatility, including a wide range of colors, textures, and marble-like finishes, allows it to replace traditional materials such as wood, glass, and natural stone. Growing demand for premium interior aesthetics and low-maintenance surfaces in modern architectural design continues to accelerate the use of engineered quartz in furniture applications globally.

By Distribution Channel, direct sales dominate the engineered quartz surface market, while online/e-commerce channels grow fastest

Direct sales accounted for 40.42% of engineered quartz surface revenue in 2025, underscoring their dominant role in global market distribution. This channel is strengthened by direct manufacturer–fabricator relationships, long-term commercial contracts, and close engagement with architects, contractors, and project developers. It enables better pricing control, customized product offerings, and efficient supply chain coordination, particularly for large-scale residential and commercial construction projects. Direct sales also support streamlined communication and faster project execution across complex installations. This distribution model remains the preferred channel for leading manufacturers in North America, Europe, and Asia, reinforcing its leadership in high-value engineered quartz transactions worldwide across multiple applications.

Online and e-commerce channels represent the fastest-growing distribution segment in the engineered quartz surface market, driven by rapid digitalization of the construction materials supply chain and increasing demand for simplified procurement processes. This channel enables sample ordering, virtual visualization tools, and direct-to-fabricator supply models, improving accessibility for small and mid-sized buyers. Expansion of digital B2B platforms and improved logistics infrastructure are accelerating market penetration, particularly in emerging economies. The shift toward online procurement is further supported by cost efficiency, faster transaction cycles, and enhanced product transparency. These factors collectively position e-commerce as a key growth driver for global engineered quartz distribution.

Regional Analysis:

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

83.19% |

|

Europe |

Germany |

28.46% |

|

Asia Pacific |

China |

32.74% |

|

Middle East & Africa |

UAE |

17.21% |

|

Latin America |

Brazil |

25.68% |

Asia Pacific Engineered Quartz Surface Market Insights

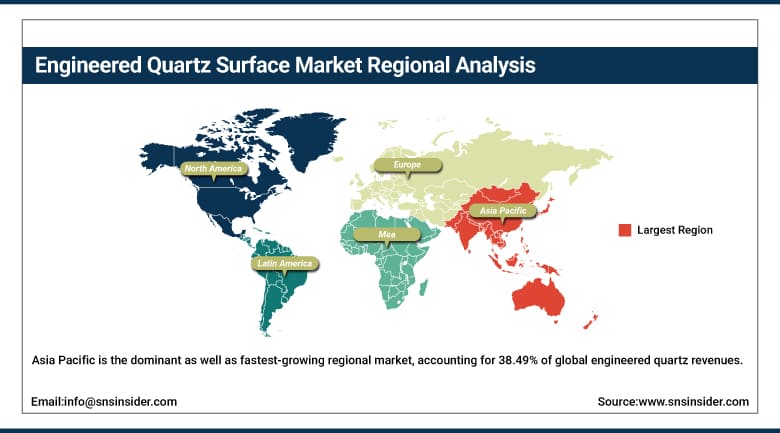

Asia Pacific is the dominant as well as fastest-growing regional market, accounting for 38.49% of global engineered quartz revenues in 2025 and expanding at a CAGR of approximately 8.78% through 2035. China contributes around 32.74% of regional demand, supported by its position as both a major production hub and a rapidly growing consumption market. Growth is driven by rising urban middle-class households, expanding premium residential construction in Tier 1 and Tier 2 cities, and increasing use in hospitality and retail interiors. India is the fastest-growing country market, supported by the Pradhan Mantri Awas Yojana housing program and strong residential development across major metropolitan cities, driving adoption in mid and premium housing segments.

China's Ministry of Housing and Urban-Rural Development, under its 14th Five-Year Plan urban renewal programme allocating USD 1.4 Trillion toward residential renovation and new urban housing development, directly accelerated the specification of premium interior surface materials in government-supported housing projects, prompting Cosentino and Wanfeng Stone to enter a strategic distribution partnership in 2025 covering 23 Chinese provinces, and enabling Wanfeng to integrate Cosentino's Silestone Ultra Compact product line into its fabrication and installation service network serving tier 1 and tier 2 city residential and commercial construction programs.

Get Customized Report as Per Your Business Requirement - Enquiry Now

North America Engineered Quartz Surface Market Insights

North America accounted for 27.53% of global engineered quartz surface revenues in 2025, with the United States contributing about 83.19% of regional demand. The region’s strong position is supported by the deep penetration of engineered quartz in residential kitchen and bathroom remodeling, alongside robust new housing construction activity. A mature retail and distribution ecosystem enables efficient product flow from leading manufacturers such as Cosentino, Caesarstone, Cambria, and MSI Surfaces to fabricators, designers, and retailers. The U.S. National Kitchen and Bath Association, with over 14,000 members, plays a key role in shaping specifications and reinforcing engineered quartz as a preferred countertop material.

The U.S. Department of Energy's Better Buildings Initiative, in partnership with the National Association of Realtors and the Green Building Council, expanded its sustainable interior materials specification guidance in 2025 to explicitly recognize low-VOC engineered quartz surfaces as a preferred specification for ENERGY STAR certified homes, prompting Cambria and MSI Surfaces to jointly develop and launch a new range of LEED v4.1-compliant engineered quartz products incorporating a minimum 15% pre-consumer recycled quartz content, targeting the growing segment of green-certified residential and commercial construction projects whose sustainability specification requirements are reshaping premium surfacing material procurement criteria.

Europe Engineered Quartz Surface Market Insights

Europe accounted for 22.10% of global engineered quartz surface revenues in 2025, expanding at a steady CAGR through 2035. The region is defined by a sophisticated interior design and architecture ecosystem, supported by stringent sustainability regulations under the EU Energy Performance of Buildings Directive. Strong participation from manufacturers such as Cosentino and Compac reinforces deep integration with European design and specification networks. Germany leads regional demand with around 28% share, driven by its large residential renovation market and high-end kitchen manufacturing cluster. Continued commercial and residential refurbishment activity further strengthens Europe’s position as a key engineered quartz market.

The European Union’s Green Deal Renovation Wave Strategy targets the renovation of nearly 35 million buildings by 2030 and aims to double the annual renovation rate from about 1% to 2% across member states, significantly increasing demand for interior surfacing materials such as engineered quartz. This initiative is supported by the Energy Performance of Buildings Directive (EPBD), which enforces stricter energy efficiency standards across over 30 million commercial and residential buildings in the EU. Together, these policies are driving an estimated USD 150–200 billion annual investment pipeline into sustainable construction and renovation, accelerating adoption of premium, low-emission engineered quartz surface solutions across Europe.

Middle East & Africa and Latin America Engineered Quartz Surface Market Insights

Middle East & Africa and Latin America are emerging growth-stage markets for engineered quartz surfaces, driven by rising premium construction activity, increasing disposable incomes, and expanding distribution networks. MEA accounted for 4.07% of global revenues in 2025, with the UAE contributing around 17.21% due to strong hospitality development, luxury residential projects, and its role as a regional specification hub. Saudi Arabia’s NEOM and Red Sea projects are generating significant demand for high-end interior applications. Latin America represented about 7.81% of global revenues, with Brazil leading at 46%, supported by residential construction growth and expanding premium kitchen and bathroom renovation activity.

The Dubai 2040 Urban Master Plan targets a population of 5.8 million residents by 2040, with over 60% of urban land designated for sustainable and mixed-use development, significantly boosting demand for premium interior materials such as engineered quartz. This is complemented by the UAE Tourism Strategy 2031, which aims to attract 40 million hotel guests annually, driving large-scale hospitality construction and luxury interior fit-outs. In Brazil, the Minha Casa Minha Vida Housing Program has supported the delivery of more than 2 million housing units, with an additional 2 million planned, strengthening residential construction activity and expanding adoption of engineered quartz surfaces in mid-income housing segments.

Market Dynamics:

Growth Drivers: Accelerating residential and commercial construction activity upgrade from natural stone is the primary structural growth catalyst

The sustained growth of global residential and commercial construction, driven by urbanization, rising household formation, increasing disposable incomes in emerging markets, and government housing investment programs, is a key demand driver for the engineered quartz surface market. Consumption is closely linked to new construction and renovation activities across kitchen, bathroom, and commercial interior applications. A major structural shift is the ongoing replacement of natural granite and marble with engineered quartz, supported by its superior durability, dimensional consistency, and low maintenance requirements. Expanding design capabilities that replicate premium natural stone aesthetics further strengthen adoption, enabling sustained market growth independent of broader construction cycles globally.

India's Ministry of Housing and Urban Affairs, under the smart cities mission and Pradhan Mantri Awas Yojana–Urban 2.0 programme committing USD 29.5 Billion toward affordable and mid-market urban housing construction through 2027, directly accelerated premium interior surface material specification in government-supported housing projects across 500 Indian cities, prompting Kajaria Ceramics and Stonecraft India to jointly develop and launch an affordable engineered quartz product range in 2025 targeting the USD 800–1,200 per square foot price segment, achieving distribution through 2,400 retail and trade channel partner outlets across 18 Indian states within six months of commercial launch.

Restraints: Raw material supply concentration and resin price volatility create cost structure uncertainty for engineered quartz manufacturers

The engineered quartz manufacturing supply chain faces structural cost pressures due to the geographic concentration of high-purity quartz aggregate supply in limited mining regions such as Spruce Pine in the United States, Norway, and Brazil. These sources provide essential silica with purity levels required for consistent slab performance, creating dependency and exposure to logistics constraints and supply fluctuations. Additionally, polyester and epoxy resin binders, which account for approximately 15–20% of total production costs, are influenced by petrochemical price volatility. This results in periodic margin compression for manufacturers, particularly in competitive pricing segments where limited flexibility restricts full cost pass-through to downstream buyers.

Opportunities: Sustainable product innovation and healthcare sector specification represent high-growth commercial frontiers

The growing use of engineered quartz in healthcare, laboratory, pharmaceutical, and food processing facility interiors represents a structurally expanding demand segment driven by stringent hygiene and safety requirements. Its non-porous surface, resistance to chemical disinfectants, and ease of sterilization make it a preferred alternative to natural stone, ceramic tile, and solid surfaces in institutional environments where infection control and regulatory compliance are critical. At the same time, increasing adoption of bio-based resin binders, recycled quartz content, and Cradle to Cradle certified products is shaping sustainability-driven innovation. These advancements align with green building standards such as LEED, BREEAM, WELL, and Living Building Challenge globally.

Recent Developments:

-

2026: Cosentino launched Silestone XM with at least 20% recycled quartz and bio-based resin, achieving Cradle to Cradle Gold certification. The product targets LEED v4.1 and WELL-certified projects across North America and Europe, supporting demand for sustainable, high-performance engineered quartz in commercial and institutional construction.

-

2026: Caesarstone and IKEA partnered to co-develop an affordable engineered quartz surface range for IKEA’s kitchen systems, targeting high-volume flat-pack consumers. The collaboration simplifies countertop specification and installation, reduces fabrication complexity, and expands access to engineered quartz for first-time homeowners and apartment renovation segments globally.

-

2025: Compac Quartz, supported by Spain’s ICEX Export Promotion Programme, expanded its distribution network into 14 Asia Pacific and Middle East markets, including Vietnam, Indonesia, the UAE, and Saudi Arabia. The initiative strengthened fabrication partnerships, reduced market entry costs, and accelerated regional distribution development compared to direct subsidiary expansion strategies.

-

2025: MSI Surfaces launched its Q Premium Natural Quartz Pura collection with 24 marble-inspired colorways, developed with Breton SpA, targeting premium residential renovation demand for Calacatta and Statuario aesthetics, reflecting the fastest-growing engineered quartz countertop trend in the U.S. and Canadian markets.

Engineered Quartz Surface Market Key Players Are:

-

Cosentino Group (Silestone)

-

Caesarstone Ltd.

-

Cambria Company LLC

-

MSI Surfaces

-

Compac Quartz

-

Vicostone Joint Stock Company

-

Pokarna Engineered Stone Limited (Quantra)

-

LG Hausys (HI-MACS & Viatera)

-

Samsung SDI (Staron)

-

Hanwha L&C Corporation

-

Quarella S.p.A.

-

Levantina Group

-

Diresco N.V.

-

Oppein Home Group

-

Wanfeng Stone

-

BITTO Stone

-

Pental Surfaces

-

Agl Surfaces

-

Stonemark Granite

-

Aristech Surfaces LLC

Engineered Quartz Surface Marke Report Scope:

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 17.09 Billion |

| Market Size by 2035 | USD 36.80 Billion |

| CAGR | CAGR of 8.07% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Product Type (Polished Quartz Surfaces, Matte/Leather Finish Quartz, Textured Quartz Surfaces, Premium Designer Quartz Slabs, Others), • By Application (Residential Construction, Commercial Construction, Hospitality & Retail Interiors, Healthcare & Institutional Spaces, Others), • By End-Use Area (Kitchen Countertops, Bathroom Vanities, Flooring Applications, Wall Cladding, Table Tops & Furniture Surfaces, Others), • By Distribution Channel (Direct Sales, Specialty Stone Retailers, Home Improvement Stores, Online/E-commerce Channels, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Cosentino Group (Silestone), Caesarstone Ltd., Cambria Company LLC, MSI Surfaces, Compac Quartz, Vicostone Joint Stock Company, Pokarna Engineered Stone Limited (Quantra), LG Hausys (HI-MACS & Viatera), Samsung SDI (Staron), Hanwha L&C Corporation, Quarella S.p.A., Levantina Group, Diresco N.V., Oppein Home Group, Wanfeng Stone, BITTO Stone, Pental Surfaces, Agl Surfaces, Stonemark Granite, Aristech Surfaces LLC. |

Frequently Asked Questions

The engineered quartz surface market is expected to grow at a CAGR of 8.07% from 2026 to 2035.

The engineered quartz surface market was valued at USD 17.09 Billion in 2025.

The primary growth factors include accelerating global residential and commercial construction activity sustaining structural countertop and interior surface specification demand, the progressive displacement of natural granite and marble.

The polished quartz surfaces segment dominated the engineered quartz surface market with 60.18% share in 2025.

Asia Pacific dominated the engineered quartz surface market in 2025, holding approximately 38.49% of global revenues, with China accounting for 32.74% of Asia Pacific revenues as the world's largest engineered quartz production and consumption base.

Get in Touch