Polypropylene Market Report Scope & Overview:

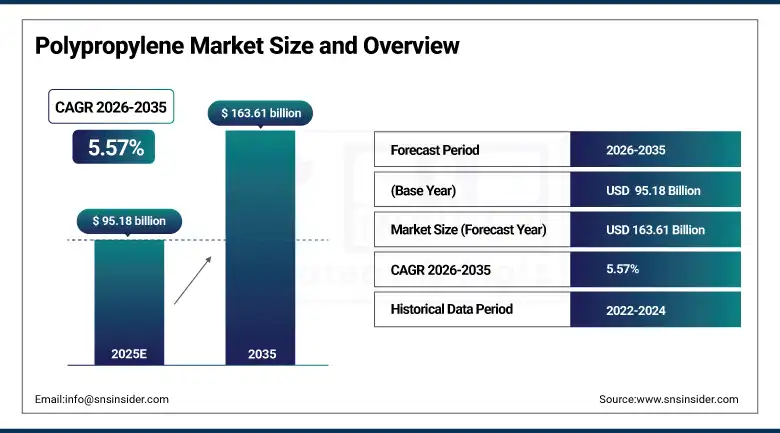

Polypropylene Market was valued at USD 95.18 billion in 2025 and is expected to reach USD 163.61 billion by 2035, growing at a CAGR of 5.57% from 2026-2035.

The growth of polypropylene can be attributed to its high demand from the packaging industry, the automotive industry, and the construction industry. Being light-weighted, strong, and cheap makes it the right choice for making fuel efficient cars and flexible packaging. Increased use of consumer goods, urbanization, and development of infrastructures continue to fuel its demand. Further improvements in recycling processes and sustainable use of plastics are propelling the growth of the market.

The U.S. Department of Energy reports polypropylene is among the five highest-volume plastics manufactured in the United States. The American Chemistry Council estimates PP production capacity in North America exceeded 12 million metric tons annually in 2024 serving packaging, automotive, and consumer goods sectors.

Polypropylene Market Size and Forecast

-

Market Size in 2025: USD 95.18 Billion

-

Market Size by 2035: USD 163.61 Billion

-

CAGR: 5.57% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026-2035

-

Historical Data: 2022-2024

To Get more information On Polypropylene Market - Request Free Sample Report

Polypropylene Market Trends

-

Mono-material PP packaging where film, closure, and label are all polypropylene is gaining traction as brand owners pursue recyclable packaging designs ahead of EU and UK single-use plastic regulations.

-

Glass-fiber reinforced polypropylene compounds are capturing metal substitution opportunities in automotive structural components where the weight-to-stiffness ratio makes them competitive alternatives to die-cast aluminum.

-

Medical-grade PP demand is growing faster than the broader market as pharmaceutical manufacturers expand single-dose injection device production and diagnostic laboratory consumable volumes.

-

Bio-based polypropylene from sugarcane-derived propylene is under active commercial development by companies including Braskem, targeting premium pricing from sustainability-committed brand owners.

-

PDH (propane dehydrogenation) capacity additions in China and the Middle East are bringing new propylene feedstock supply that will keep PP cost-competitive versus alternative polymers through the forecast period.

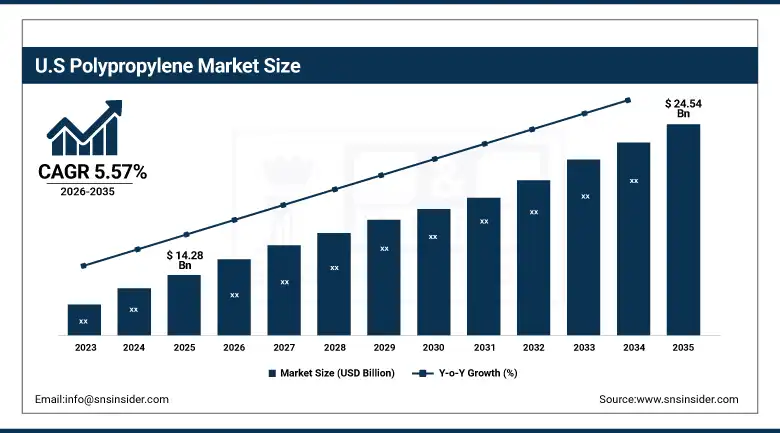

U.S. Polypropylene Market was valued at USD 14.28 billion in 2025 and is expected to reach USD 24.54 billion by 2035, growing at a CAGR of 5.57% from 2026-2035.

The U.S. polypropylene market is structurally well-positioned because the country operates one of the most cost-competitive propylene supply chains in the world, underpinned by abundant shale-derived propane that feeds PDH units at attractive economics relative to European or Asian naphtha-based production.

The U.S. Food and Drug Administration maintains strict specifications for medical-grade polypropylene used in drug packaging and medical devices under 21 CFR standards. The American Chemistry Council reports that PP is the fastest-growing major thermoplastic in U.S. healthcare applications driven by expansion of single-use medical device manufacturing.

Polypropylene Market Segment Analysis

-

By Type, Homopolymer segment dominated the Polypropylene Market in 2025; Copolymer segment growing in impact-critical automotive and appliance applications.

-

By Processing Technology, Injection Molding segment dominated the Polypropylene Market in 2025; Extrusion Molding segment growing strongly for film and fiber applications.

-

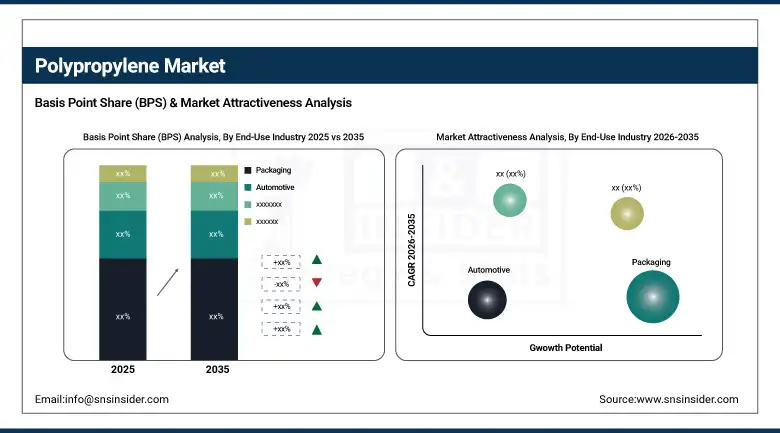

By End Use Industry, Packaging segment dominated with ~36% share in 2025; Automotive segment fastest growing (CAGR) driven by lightweighting and EV structural demand.

By Type, Homopolymer segment dominates the Polypropylene Market, Copolymer segment growing in performance applications

Homopolymer polypropylene held the dominant type share in 2025, reflecting its commanding position in the highest-volume PP applications including flexible and rigid packaging, consumer product housings, laboratory consumables, fibers and nonwovens, and injection-molded closures. Homopolymer PP's higher crystallinity relative to copolymer grades produces greater stiffness and a lower cost per unit of structural performance attributes that make it the default specification for applications where impact resistance at low temperatures is not a primary concern. Packaging film, bottle caps, straws, food containers, and the entire woven and nonwoven fabric product range use homopolymer PP at the vast majority of installations.

Copolymer polypropylene produced by adding ethylene or butene comonomer to the polymerization reaction sacrifices some stiffness in exchange for dramatically improved impact resistance, particularly at low temperatures where pure homopolymer PP becomes brittle. This property profile is indispensable in automotive bumpers, dashboards, door panels, and appliance components that must survive cold weather impact events without cracking. Random copolymer PP additionally provides improved optical clarity compared to homopolymer, making it the preferred material for transparent food packaging including yogurt pots, deli containers, and medical packaging where visual product inspection is required.

By Processing Technology, Injection Molding segment dominates the Polypropylene Market, Extrusion Molding segment growing for films and fibers

The Injection Molding process continued to have the largest share of the Polypropylene Processing Technology in the Polypropylene Market in 2025, due to the sheer volume of closures used in packaging, housings for consumer products, interior parts used in the automobile industry, healthcare products, and many industrial parts which can only be produced cost-effectively via injection molding processes.

Extrusion Molding is one of the fastest-growing categories, owing largely to PP films, sheets, and fibers for uses such as sustainable packaging, non-woven fabrics, and geotextile materials for industries. For example, there is growth in Biaxially Oriented PP (BOPP) films for food packaging, cast PP film used for laminated film and PP sheets for thermoformed containers. Another fast-growing segment involves PP fiber extrusion for applications such as carpet backing, agricultural textiles, geotextiles, and hygiene materials.

By End Use Industry, Packaging segment dominates the Polypropylene Market, Automotive segment expected to grow fastest

Packaging held approximately 36% of Polypropylene Market revenue in 2025, reflecting PP's deep penetration across rigid and flexible packaging formats for food, beverage, consumer goods, pharmaceutical, and industrial product containment. PP's combination of food contact safety, heat sealability, moisture resistance, and formability at low cost makes it the dominant polymer for a wide range of packaging applications from microwave-safe containers to thin-wall injection molded yogurt tubs to biaxially oriented film pouches.

Automotive is the fastest-growing end-use segment, driven by the global automotive industry's systematic effort to reduce vehicle weight through material substitution and the specific needs of electric vehicles where reducing body and component weight directly extends battery range. PP compounds particularly short and long glass fiber-reinforced grades are replacing die-cast aluminum and even some steel in under-hood components, battery housing elements, and structural brackets. An average passenger vehicle today contains 40-50 kg of polypropylene, and that figure is rising as EV architectures drive more aggressive lightweighting programs.

Polypropylene Market Regional Analysis

|

Region |

Major Country |

Share within Region (%) |

|

Asia Pacific |

China |

58% |

|

North America |

United States |

85% |

|

Europe |

Germany |

26% |

|

Middle East & Africa |

Saudi Arabia |

48% |

|

Latin America |

Brazil |

52% |

Asia Pacific Polypropylene Market Insights

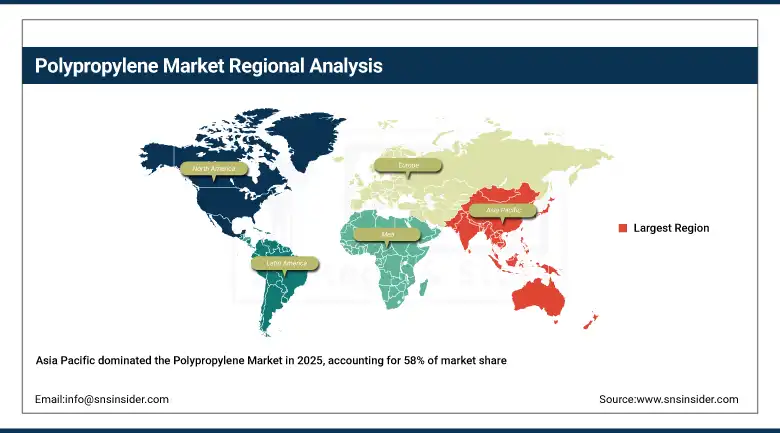

Asia Pacific dominated the global Polypropylene Market with approximately 58% revenue share in 2025, anchored by China's position as both the world's largest PP consumer and increasingly its largest producer. China's packaging industry, its enormous automotive manufacturing base, its consumer goods production, and its fast-growing medical device sector collectively create the most diverse and largest national PP demand pool in the world. China has also been aggressively building propane dehydrogenation capacity to reduce dependence on imported PP and propylene, a self-sufficiency drive that is reshaping global PP trade flows. India's rapidly growing consumer goods, automotive, and packaging sectors are making it the most dynamic individual growth market within Asia Pacific, with PP consumption growth rates consistently exceeding the regional average.

China's National Bureau of Statistics reports polypropylene production reached over 35 million metric tons in 2024 with domestic consumption exceeding production and imports meeting the gap. India's Ministry of Chemicals and Fertilizers projects domestic PP demand to reach 10 million metric tons annually by 2030 driven by packaging and automotive sector growth.

Get Customized Report as per Your Business Requirement - Enquiry Now

North America Polypropylene Market Insights

North America held approximately 15% of global Polypropylene Market revenue in 2025, with the U.S. as the dominant national market supported by cost-competitive PDH and refinery-integrated propylene supply. The region's PP market is characterized by high sophistication in compound development particularly for automotive, medical, and consumer electronics applications and strong demand for premium high-melt-flow and high-clarity specialty grades that command pricing above commodity PP. The IRA-driven investment in domestic EV manufacturing is creating a structural shift in automotive PP demand toward glass-filled compounds and specialty grades used in electric vehicle battery housings, charge port components, and interior structural systems that differ significantly from traditional internal combustion vehicle PP applications.

The U.S. Environmental Protection Agency's Safer Choice program recognizes polypropylene as a preferred polymer for food contact applications due to its low migration of chemical additives. The EPA's updated packaging guidelines explicitly support PP as a preferred material in sustainable packaging applications that meet recyclability criteria.

Europe Polypropylene Market Insights

Europe held approximately 16% of the global Polypropylene Market in 2025, with demand concentrated in Germany, France, Italy, and the UK. European PP demand is being shaped by two powerful regulatory forces moving in opposite directions the Single-Use Plastics Directive and Extended Producer Responsibility regulations are creating pressure to reduce certain PP applications and increase recycled content, while the automotive industry's electrification program and the growth of advanced medical device manufacturing are creating new premium demand streams that more than offset volume pressure in commoditized packaging categories. European PP resin producers including Borealis, SABIC's European operations, and TotalEnergies Polymers are investing in circular economy capabilities including mechanical and chemical recycled PP to meet brand owner specifications.

The EU Single-Use Plastics Directive mandates recycled content minimums of 25% for PP beverage bottles by 2025 and 30% by 2030. The European Plastics Converters Association (EuPC) reports that demand for food-contact-approved recycled polypropylene (rPP) exceeded supply capacity across Europe in 2024.

Middle East & Africa and Latin America Polypropylene Market Insights

The Middle East is a globally significant PP producing and exporting region, with Saudi Arabia's SABIC, TASNEE, and Borouge joint venture operations representing major production assets that serve both domestic and international markets from advantaged naphtha and ethane feedstock positions. The Middle East's PP production economics are among the most competitive globally, which gives the region an important structural role in international PP trade flows. In Latin America, Brazil is the dominant PP market with Braskem the world's leading producer of bio-based polypropylene as the primary domestic producer. Brazil's food and beverage packaging industry, automotive manufacturing sector, and growing consumer goods market sustain consistent domestic PP consumption. Mexico's manufacturing export sector, particularly automotive and electronics, is another growing PP demand center in the region.

Saudi Aramco subsidiary SABIC operates over 4 million metric tons of annual polypropylene production capacity in the Middle East. Braskem's Green Plastics bio-PP, produced from sugarcane ethanol in Brazil, holds International Sustainability and Carbon Certification (ISCC) and is sold under long-term supply agreements to global consumer goods brands.

Polypropylene Market Growth Drivers:

-

Accelerating packaging industry demand and automotive lightweighting trends sustaining robust global polypropylene consumption growth worldwide

Polypropylene demand growth is fundamentally structural rather than cyclical it is driven by secular trends in how goods are packaged, transported, and how vehicles are engineered, rather than by short-term economic conditions. The packaging sector's shift toward lightweight, resealable, and microwaveable formats is systematically pulling PP share from glass and metal containers. The automotive industry's mandated fuel efficiency and emissions targets are compelling systematic replacement of metal components with lighter plastic alternatives, with PP compounds the primary beneficiary across interior, exterior, and under-hood applications. These demand drivers operate independently across geographies, meaning that even when one regional economy slows, demand growth from another typically maintains global market momentum. The additional growth from medical device expansion, EV component development, and nonwoven fabric applications creates a diversification of demand that reinforces the market's resilience.

The International Energy Agency projects that global EV sales will exceed 45 million units annually by 2030 with each EV containing 15-20% more polymer content than a comparable ICE vehicle. Automotive PP compound demand is expected to grow at nearly double the overall PP market CAGR through 2035 driven by vehicle electrification globally.

Polypropylene Market Restraints:

-

Fluctuating propylene feedstock prices and mounting environmental pressure against single-use plastics constraining polypropylene market expansion

Polypropylene faces two distinct restraints that pull in somewhat different directions. The first is feedstock cost volatility: propylene pricing is tied to crude oil, natural gas, and regional cracker economics in ways that create significant margin variability for PP producers and price uncertainty for downstream converters who are trying to develop long-term material specifications. The energy shock of 2022, subsequent propylene margin compression, and ongoing crude oil price volatility have demonstrated how quickly PP market economics can shift in ways that destabilize investment decisions across the supply chain. The second restraint is the regulatory and consumer pressure against plastic packaging particularly single-use formats that affects PP's largest end-use segment.

Polypropylene Market Opportunities:

-

Growing adoption of recyclable PP packaging and medical-grade polypropylene expansion creating new commercial opportunities globally

The circular economy transition that is creating regulatory headwinds for virgin PP in some applications is simultaneously creating opportunities for PP producers and converters who invest in recycled content capabilities. Post-consumer recycled PP (rPP) that meets food contact and medical purity specifications is a genuinely scarce commercial product with growing brand-owner demand, and the supply-demand imbalance is attracting significant capital into PP sorting, washing, and purification infrastructure. Chemical recycling of PP depolymerizing mixed plastic waste to recover propylene feedstock for new polymerization is advancing toward commercial scale through companies including PureCycle Technologies in the U.S. and Borealis in Europe, and could ultimately allow recycled PP to meet performance specifications that mechanical recycling cannot achieve. In the medical segment, the shift toward single-use sterile devices accelerated by COVID-19 supply chain lessons is creating durable demand growth for medical-grade PP that commands significant price premiums over commodity grades and sustains attractive margins for specialty producers.

Recent Developments:

-

2026: SABIC launched a new line of certified recycled content polypropylene compounds for automotive interior applications, incorporating 30% post-consumer recycled PP sourced from sorted household waste streams and meeting automotive OEM mechanical and flammability specifications for interior trim applications without performance compromise.

-

2025: PureCycle Technologies commenced commercial operations at its Ironton, Ohio PP purification facility, producing food-contact-approved ultra-pure recycled polypropylene from post-consumer packaging waste using the company's proprietary solvent-based purification technology under long-term offtake agreements with major consumer goods packaging companies.

-

2025: LyondellBasell inaugurated its Circular Steam Cracker project at its Wesseling site in Germany, co-processing certified waste-derived liquid feedstocks alongside virgin naphtha to produce circular propylene for polypropylene production under ISCC PLUS mass balance certification supporting European brand-owner recycled content procurement commitments.

Polypropylene Market Key Players

Some of the Polypropylene Market Companies

-

LyondellBasell Industries Holdings B.V.

-

ExxonMobil Chemical Company

-

SABIC (Saudi Basic Industries Corporation)

-

Borealis AG

-

TotalEnergies SE

-

Braskem S.A.

-

Mitsui Chemicals, Inc.

-

Sumitomo Chemical Co., Ltd.

-

INEOS Group Holdings S.A.

-

Reliance Industries Limited

-

Formosa Plastics Corporation

-

Sinopec Corp. (China Petroleum & Chemical)

-

PetroChina Company Limited

-

Haldia Petrochemicals Ltd.

-

Hyosung Corporation

-

SCG Chemicals Co., Ltd.

-

BASF SE

-

Toray Industries, Inc.

-

Repsol S.A.

-

PKN Orlen S.A.

Polypropylene Market Report Scope

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 95.18 Billion |

| Market Size by 2035 | USD 163.61 Billion |

| CAGR | CAGR of 5.57% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Type (Homopolymer, Copolymer), By Processing Technology (Injection Molding, Blow Molding, Extrusion Molding, Others) • By End Use Industry (Packaging, Automotive, Construction & Infrastructure, Consumer Goods, Healthcare & Pharmaceuticals, Electrical & Electronics, Agriculture, Others) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | LyondellBasell Industries Holdings B.V., ExxonMobil Chemical Company, SABIC (Saudi Basic Industries Corporation), Borealis AG, TotalEnergies SE, Braskem S.A., Mitsui Chemicals, Inc., Sumitomo Chemical Co., Ltd., INEOS Group Holdings S.A., Reliance Industries Limited, Formosa Plastics Corporation, Sinopec Corp. (China Petroleum & Chemical), PetroChina Company Limited, Haldia Petrochemicals Ltd., Hyosung Corporation, SCG Chemicals Co., Ltd., BASF SE, Toray Industries, Inc., Repsol S.A., and PKN Orlen S.A. |

Frequently Asked Questions

Asia Pacific dominated the Polypropylene Market in 2025.

The Automotive segment is expected to register the fastest CAGR in the Polypropylene Market through 2035.

The Packaging segment dominated the Polypropylene Market with approximately 36% share in 2025.

The Polypropylene Market was valued at USD 95.18 billion in 2025.

The Polypropylene Market is expected to grow at a CAGR of 5.57% from 2026 to 2035.

Get in Touch