Extruded Polystyrene Market Report Scope & Overview:

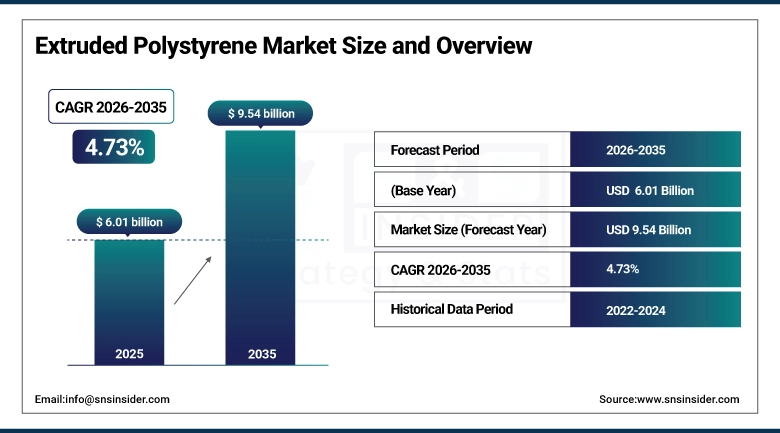

The Extruded Polystyrene Market size was estimated at USD 6.01 billion in 2025 and is expected to reach USD 9.54 billion by 2035, growing at a CAGR of 4.73% over the forecast period of 2026-2035.

The global extruded polystyrene market trend is a growing demand for high-performance rigid thermal insulation solutions such as roof insulation boards, below-grade foundation panels, and below-slab floor insulation sheets as the growth of the market is driven by increasing green building construction activity, government mandates for energy-efficient building envelopes, and contractor preference for moisture-resistant and compressive-strength insulation materials in residential and commercial construction projects. This trend is also driven by a growing adoption of net-zero energy building standards and the growing focus on reducing lifecycle carbon emissions in construction as builders and specifiers become more focused on achieving building energy code compliance and are more willing to invest in continuous insulation systems, resulting in growth in the domestic and international market for board-form and panel-form extruded polystyrene insulation solutions.

For instance, in March 2024, growing enforcement of updated energy efficiency building codes in North America drove a 19% increase in extruded polystyrene insulation procurement volumes for commercial construction projects, boosting continuous insulation adoption and below-grade waterproofing material integration across new builds.

Extruded Polystyrene Market Size and Forecast:

-

Market Size in 2025: USD 6.01 billion

-

Market Size by 2035: USD 9.54 billion

-

CAGR: 4.73% from 2026 to 2035

-

Base Year: 2025

-

Forecast Period: 2026–2035

-

Historical Data: 2022–2024

To Get more information on Extruded Polystyrene Market - Request Free Sample Report

Extruded Polystyrene Market Trends

-

Extruded polystyrene insulation boards are being adopted because builders demand high compressive strength, low moisture absorption, and consistent thermal resistance (R-value) performance across roof, wall, and below-grade foundation applications.

-

Increased integration of continuous insulation systems in commercial building envelope assemblies to meet updated ASHRAE 90.1 energy code requirements and achieve LEED certification targets across new construction projects.

-

The development of blowing-agent reformulations using hydrofluoroolefin (HFO) and CO2-based technologies to reduce global warming potential (GWP) of extruded polystyrene manufacturing while maintaining thermal performance specifications.

-

Increased demand for pre-engineered panel systems, tapered insulation roof board configurations, and thermally broken wall assembly designs to improve building energy performance and reduce on-site labor costs.

-

Collaboration between extruded polystyrene manufacturers, building product distributors, and construction specification consultants to develop project-specific insulation system designs and improve building code compliance documentation.

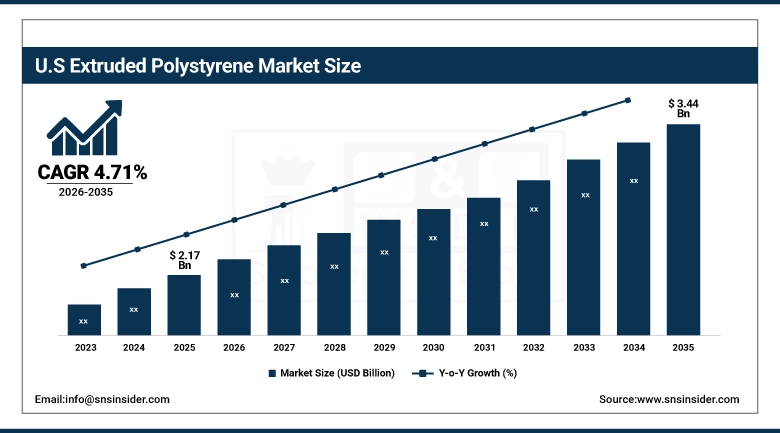

The U.S. Extruded Polystyrene Market was valued at USD 2.17 billion in 2025 and is expected to reach USD 3.44 billion by 2035, growing at a CAGR of 4.71% from 2026-2035.

The United States represents the largest market for extruded polystyrene, primarily driven by the mandatory continuous insulation requirements under IECC 2021, widespread residential and commercial construction activity across Sunbelt and Mid-Atlantic states, and well-established specialty building products distribution networks. Strong builder awareness of moisture management in below-grade applications, growing adoption of inverted roof membrane assemblies, and increased contractor spending on code-compliant building envelope systems help to drive growth in the market.

Extruded Polystyrene Market Growth Drivers:

-

Stringent Building Energy Codes and Green Construction Activity is Driving the Extruded Polystyrene Market Growth

Stringent building energy codes and green construction activity take the center stage as a growth driver for the extruded polystyrene market share, and are driven by the enforcement of IECC 2021 continuous insulation requirements, ASHRAE 90.1 commercial building envelope standards, and LEED v4.1 material specification criteria for reduced thermal bridging and moisture control in building assemblies. These solutions for building energy performance improvement and long-term thermal resistance retention are driving the base of the market, the penetration of board and panel insulation formats, and adding to the overall market share globally.

Extruded Polystyrene Market Restraints:

-

Volatile Raw Material Prices and Environmental Concerns Over Blowing Agents are Hampering the Extruded Polystyrene Market Growth

Volatile raw material prices and environmental concerns over blowing agents also restrict the extruded polystyrene market growth, as a large number of mid-sized insulation manufacturers and regional construction product distributors who depend on stable styrene monomer and blowing agent supply chains remain exposed or face difficulties managing input cost fluctuations and regulatory compliance timelines for HFC-to-HFO blowing agent transitions. This might lead to margin compression, reduced product availability in price-sensitive construction segments, and limited investment in manufacturing capacity expansion for affected producers. As a result, smaller market participants face competitive disadvantages, and market growth is stunted in regions where raw material import dependency and environmental compliance infrastructure remain underdeveloped.

Extruded Polystyrene Market Opportunities:

-

Net-Zero Building Programs and Cold Chain Infrastructure Expansion Drive Future Growth Opportunities for the Extruded Polystyrene Market

The opportunity in the net-zero building programs and cold chain infrastructure expansion in extruded polystyrene market is in the form of high-R-value continuous insulation system specifications, low-GWP product reformulation platforms, and purpose-engineered cold storage panel assemblies. These solutions provide for improved building envelope airtightness performance, individualized thermal resistance design recommendations for climate-specific construction zones, and reliable below-freezing temperature insulation continuity for refrigerated facilities. Through enhanced building energy compliance, cold storage operational efficiency gains, and construction specification influence, particularly in areas with active net-zero retrofit programs and expanding food and pharmaceutical cold chain infrastructure needs, these products may improve building lifecycle energy performance, decrease heating and cooling operational costs, and expand the market.

Extruded Polystyrene Market Segment Analysis

-

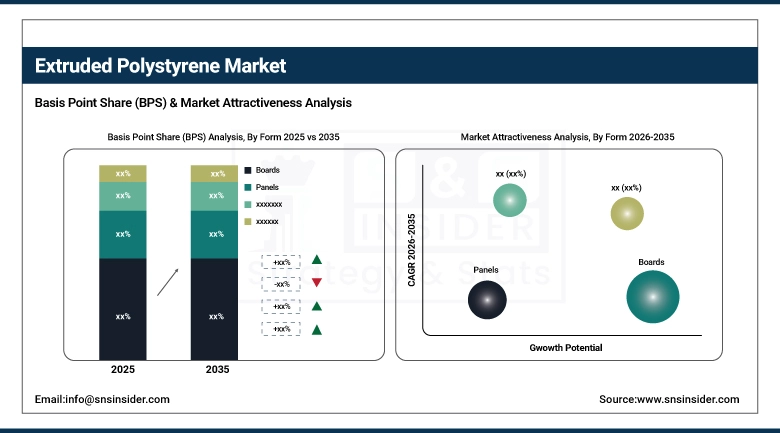

By form, boards held the largest share of around 52.37% in 2025, and the panels segment is expected to register the highest growth with a CAGR of 5.14%.

-

By distribution channel, direct sales (B2B) dominated the market with approximately 46.82% share in 2025, while the online sales segment is expected to register the highest growth with a CAGR of 6.38%.

-

By application, roof insulation accounted for the leading share of nearly 34.56% in 2025, and the foundation segment is expected to register the highest growth with a CAGR of 5.27%.

-

By end-use industry, residential construction held the largest share of about 43.19% in 2025, and the infrastructure segment is expected to register the highest growth with a CAGR of 5.61%.

By Form, Boards Lead the Market, While Panels Register Fastest Growth

The boards segment accounted for the highest revenue share of approximately 52.37% in 2025, owing to widespread use in roof insulation assemblies, broad availability across standard thickness ranges from building product distributors, and strong contractor preference for rigid board formats in below-grade foundation and above-grade continuous insulation applications. Emerging trends, including increasing specification of tapered board roofing systems and thermally enhanced board products with graphite-modified polystyrene cores, are reinforcing the boards segment’s market leadership position across commercial and residential construction programs. The panels segment is anticipated to achieve the highest CAGR of nearly 5.14% during the 2026–2035 period, driven by the increasing demand from modular and prefabricated construction programs, reduced on-site labor requirements for factory-finished panel assemblies, and growing contractor preference for integrated structural insulated panel systems.

By Distribution Channel, Direct Sales (B2B) Dominates, while Online Sales Registers Fastest Growth

By 2025, the direct sales (B2B) segment contributed the largest revenue share of 46.82% due to the volume-purchase requirements of commercial and industrial construction contractors, established procurement relationships between major extruded polystyrene manufacturers and large regional building product distributors, and project-specific technical specification support provided through direct sales channels. Growing preference for manufacturer-direct pricing agreements and specification consulting services for large-scale commercial construction projects are making building owners and general contractors increasingly aware of direct procurement cost advantages. The online sales segment is projected to grow at the highest CAGR of about 6.38% between 2026 and 2035 due to the growing need for convenient small-quantity purchasing among residential contractors, remodeling professionals, and DIY insulation installation customers.

By Application, Roof Insulation Leads, and Foundation Registers Fastest Growth

The roof insulation segment accounted for the largest share of the extruded polystyrene market with about 34.56%, owing to high volume requirements in flat and low-slope commercial roofing assemblies, strong specification support from roofing system manufacturers integrating extruded polystyrene in protected membrane and inverted roof membrane assembly systems, and established contractor familiarity with board insulation installation in new roofing and re-roofing construction programs. Reasons driving the roof insulation segment include increasing commercial building re-roofing activity and growing adoption of tapered insulation systems for improved drainage performance. In addition, the foundation segment is slated to grow at the fastest rate with a CAGR of around 5.27% throughout the forecast period of 2026–2035, as residential and commercial construction developers seek high-compressive-strength below-grade insulation materials, frost-protected shallow foundation system specifications, and drainage-integrated foundation panel solutions for new construction in cold and mixed climate zones.

By End-Use Industry, Residential Construction Leads, and Infrastructure Registers Fastest Growth

The residential construction segment accounted for the highest revenue share of approximately 43.19% in 2025, owing to high volume demand for below-grade foundation insulation, above-grade continuous wall insulation, and attic and crawlspace floor insulation in new single-family and multifamily housing construction across North America and Europe. Emerging trends, including increasing energy code stringency for residential building envelopes and growing homebuilder adoption of continuous insulation in wood-frame wall assemblies, are sustaining the residential segment’s leading market position. In comparison, the infrastructure segment is anticipated to achieve the highest CAGR of nearly 5.61% during the 2026–2035 period, driven by the increasing demand for extruded polystyrene in road sub-base frost protection, highway embankment lightweight fill applications, and airport runway and taxiway insulation programs in cold climate regions.

Extruded Polystyrene Market Regional Highlights:

Asia Pacific Extruded Polystyrene Market Insights:

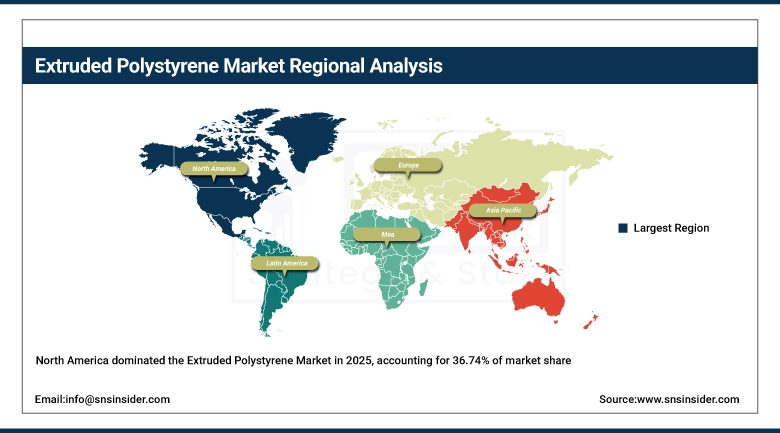

Asia Pacific is the fastest-growing region in the extruded polystyrene market with a CAGR of 5.89%, as the awareness about energy-efficient building insulation materials, government green building certification program requirements, and building construction infrastructure investment in China, India, and South Korea is growing. Factors including China’s national building energy conservation standards enforcement, India’s Smart Cities Mission construction activity, and South Korea’s Green New Deal building retrofit program investment are stimulating the market growth. Cold storage facility construction and food supply chain infrastructure development have been instrumental in improving extruded polystyrene adoption, especially in high-density urban industrial and logistics corridor construction. Government-backed building energy code updates and OEM localization of extruded polystyrene production capacity also help in advancing insulation material adoption and regional construction sector digital transformation.

North America Extruded Polystyrene Market Insights:

North America held the largest revenue share of over 36.74% in 2025 of the extruded polystyrene market due to a well-established building products manufacturing base, stringent state-level adoption of IECC 2021 continuous insulation requirements, and increased builder and specifier awareness of extruded polystyrene thermal and moisture performance advantages in mixed and cold climate construction. Drivers include widespread commercial re-roofing demand, an improved cold chain and food logistics construction pipeline, growing adoption of frost-protected shallow foundation systems, and greater acceptance of below-grade insulation drainage board assemblies across residential and light commercial new construction.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Extruded Polystyrene Market Insights:

The extruded polystyrene market in Europe is the second-dominating region after North America on account of European Union Energy Performance of Buildings Directive (EPBD) recast requirements mandating near-zero energy building standards, well-established building insulation material certification frameworks under CE marking and ETA approvals, and increasing building deep renovation activity across Germany, France, and the Nordic countries. Rising implementation of national building stock decarbonization programs, updated EU F-Gas Regulation blowing agent compliance timelines, favorable government renovation subsidy programs for energy-efficient insulation upgrades, and cross-border harmonization of building thermal performance standards are also contributing to the sustained growth of the market in leading European construction economies.

Latin America (LATAM) and Middle East & Africa (MEA) Extruded Polystyrene Market Insights:

In Latin America, and Middle East & Africa, the growing construction sector modernization programs and increase in cold storage and food processing facility investment with expanding retail and logistics infrastructure support the extruded polystyrene market growth. The rising adoption of energy-efficient building envelope specifications and locally adapted insulation product distribution capabilities, along with government commercial building energy efficiency programs, will aid construction insulation material accessibility and extruded polystyrene product adoption. The increasing urban residential and infrastructure construction activity and improving building material supply chain infrastructure in these regions are continuing to encourage market growth.

Extruded Polystyrene Market Competitive Landscape:

Owens Corning (est. 1938) is a leading building and industrial insulation materials manufacturer that focuses on extruded polystyrene board insulation, roofing systems, and composite building products for residential, commercial, and industrial construction applications. It uses its FOAMULAR® NGX extruded polystyrene product platform and established national distribution relationships to produce high-R-value, low-GWP building insulation solutions, with a strong commitment to HFO blowing agent reformulation and sustainable product innovation.

-

In October 2024, expanded the FOAMULAR® NGX product line with new thickness configurations and compressive strength grades targeting below-grade foundation insulation and commercial plaza deck applications, strengthening extruded polystyrene specification support for architects and building enclosure consultants across North American construction markets.

Dow Inc. (est. 1897) is a well-known global specialty materials and building science solutions provider focused on STYROFOAM™ brand extruded polystyrene insulation products, building envelope systems, and construction adhesive and sealant technologies. It invests in low-GWP blowing agent technology, building science testing programs, and contractor education initiatives with the hopes of revolutionizing building envelope thermal performance with science-backed continuous insulation product systems and specification support for code-compliant construction applications globally.

-

In April 2024, launched updated STYROFOAM™ Brand XPS insulation boards with next-generation HFO blowing agent formulation delivering over 90% reduction in global warming potential compared to prior HFC-blown product grades, targeting commercial roofing, below-grade, and cold storage construction specifications across North America and Europe.

BASF SE (est. 1865) is a leading global chemical company in the fields of extruded polystyrene insulation production, construction chemical solutions, and performance materials for building and infrastructure applications. The company’s Styrodur® XPS insulation product portfolio focuses on high compressive strength performance and dimensional stability, and features a strong commitment to environmental product compliance and continuous thermal performance innovation to complement the strong market presence in both European residential renovation and new commercial construction programs.

-

In February 2025, introduced Styrodur® C grades with updated CO2-based blowing agent formulation compliant with revised EU F-Gas Regulation 2024 requirements, expanding availability across Germany, France, and Poland for below-grade insulation, inverted roof, and highway frost protection civil engineering applications.

Extruded Polystyrene Market Key Players:

-

Owens Corning

-

Dow Inc.

-

BASF SE

-

Saint-Gobain S.A.

-

Kingspan Group plc

-

Recticel NV

-

URSA Insulation S.A.

-

Austrotherm GmbH

-

Soprema Group

-

Synthos S.A.

-

Knauf Insulation GmbH

-

JACKON Insulation GmbH

-

Plasti-Fab Ltd.

-

Versico Roofing Systems

-

Atlas Roofing Corporation

-

Foamex International Inc.

-

Poly-Tech Industrial Inc.

-

Sika AG

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 6.01 Billion |

| Market Size by 2035 | USD 9.54 Billion |

| CAGR | CAGR of 4.73% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Form: Boards, Panels, Sheets, Others (e.g., customized shapes) • By Distribution Channel: Direct Sales (B2B), Retail Stores, Online Sales, Distributors & Wholesalers • By Application: Roof Insulation, Wall Insulation, Floor & Ceiling Insulation, Foundation, Others (e.g., cavity walls, inverted roofs) • By End-Use Industry: Residential Construction, Commercial Construction, Industrial Construction, Infrastructure |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, France, UK, Italy, Spain, Poland, Russsia, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia,ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, Egypt, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia Rest of Latin America) |

| Company Profiles | Owens Corning, Dow Inc., BASF SE, Saint-Gobain S.A., Kingspan Group plc, Recticel NV, Ravago Group, URSA Insulation S.A., Austrotherm GmbH, Soprema Group, Synthos S.A., Knauf Insulation GmbH, Fibran S.A., JACKON Insulation GmbH, Plasti-Fab Ltd., Versico Roofing Systems, Atlas Roofing Corporation, Foamex International Inc., Poly-Tech Industrial Inc., and Sika AG. |

Frequently Asked Questions

The boards segment holds the largest market share, accounting for approximately 45% due to widespread use in thermal insulation systems.

The booming construction sector, especially in infrastructure and urban housing, is significantly increasing the demand for XPS insulation.

Key applications include roof, wall, and floor insulation in residential, commercial, and industrial buildings.

Europe leads the market due to stringent energy codes, followed by North America and Asia-Pacific with increasing construction activities.

Rising demand for energy-efficient insulation in green buildings and government incentives for retrofitting are key growth drivers.

Get in Touch