Eye Care Services Market Report Scope & Overview:

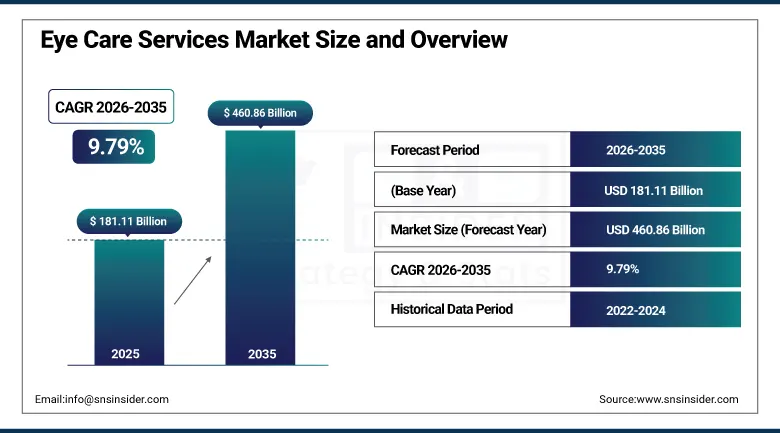

The Eye Care Services Market was valued at USD 181.11 Billion in 2025 and is expected to reach USD 460.86 Billion by 2035, growing at a CAGR of 9.79% from 2026 to 2035.

The Eye Care Services Market is expected to witness an increase as a result of rising needs for vision correction procedures, the increasing establishment of ophthalmology services infrastructure within healthcare markets, and increasing cases of age-related eye diseases among the increasing elderly population, which will lead to changes in the delivery of eye care services globally. Rising number of patients with vision problems, aging population, technological advances, and increased awareness about eye care are some factors fueling the market growth in various categories such as surgical, diagnostic, and specialist services. Increased technological advances in laser surgery and minimally invasive surgeries are leading to increased recovery times, hence encouraging patients to seek treatment rather than waiting.

EssilorLuxottica continued expanding its integrated eye care service network in 2025, reinforcing its global leadership position by combining vision correction manufacturing capability with an extensive retail and professional eye care service footprint spanning multiple continents.

Market Size and Forecast

- Market Size in 2026E: USD 198.84 Billion

- Market Size by 2035: USD 460.86 Billion

- CAGR: 9.79% from 2026 to 2035

- Fastest Growing Region: Asia Pacific

- Largest Region: North America

To Get more information On Eye Care Services Market - Request Free Sample Report

Eye Care Services Market Trends

- Developments in laser and minimally invasive surgical procedures continue resulting in faster patient recovery rates.

- Global health campaigns and public-private partnerships continue improving eye care access in low- and middle-income countries.

- Rising screen time and urban lifestyles continue accelerating diagnosis and correction of refractive errors worldwide.

- Expanding ambulatory surgical center infrastructure continues shifting eye surgery away from traditional hospital settings.

- Growing adoption of advanced diagnostic imaging technology continues improving early detection of age-related eye conditions.

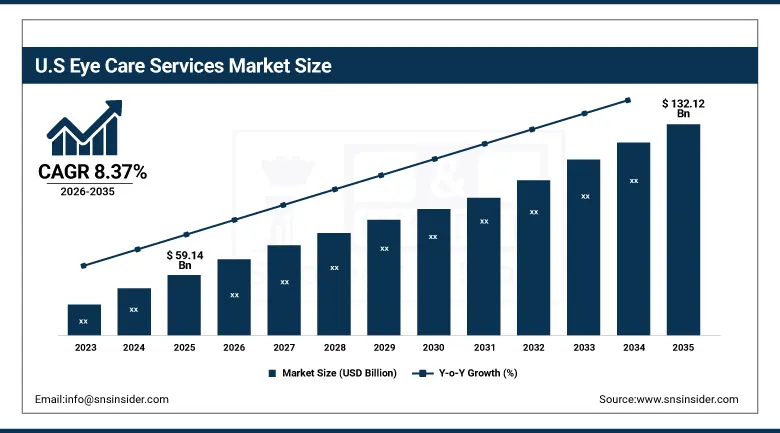

The United States Eye Care Services Market Outlook

The United States Eye Care Services Market was valued at USD 59.14 Billion in 2025 and is expected to reach USD 132.12 Billion by 2035, growing at a CAGR of 8.37% from 2026 to 2035.

The United States was leading in terms of demand for eye care services in North America due to the presence of many people who have problems with their eyesight, high growth rate of elderly population, and improvement in diagnostic and surgical technologies. The official statistics show that approximately twelve million people above the age of forty in the United States have problems with their eyesight, out of which one million are blind, and the increasing number of elderly population above the age of sixty-five has increased the demand for eye care services.

National Vision Holdings, headquartered in Duluth, Georgia, continued expanding its retail optical and eye care service footprint across the United States in 2025, reinforcing its position as one of the largest operators of optical retail locations offering integrated eye exam and vision correction services.

Eye Care Services Market Segmentation Analysis

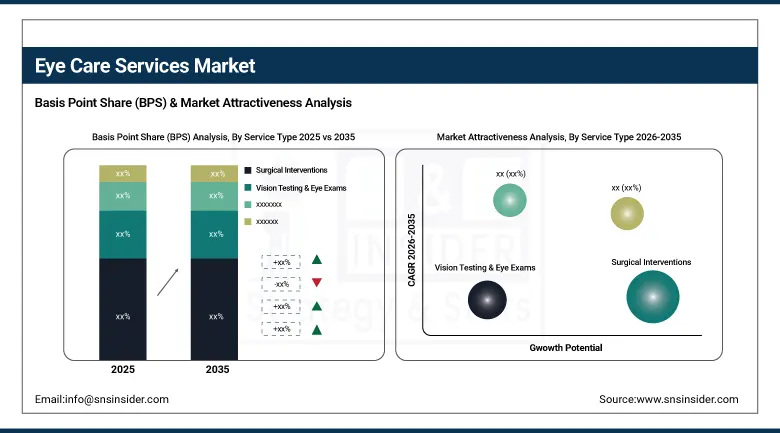

- By Service Type, the surgical interventions segment held approximately 45.92% share in 2025, while the specialty advanced services segment is the fastest growing.

- By Indication, the refractive errors segment held approximately 39.00% share in 2025, while the age-related eye conditions segment is the fastest growing.

- By End-User, the hospitals clinics segment held the largest share in 2025, while the ambulatory surgical centers segment is the fastest growing.

- By Age Group, the geriatric population segment held the largest share in 2025, while the pediatric population segment is the fastest growing.

By Service Type, surgical interventions led the market, specialty advanced services grew fastest

The surgical interventions segment dominated the service type category in 2025, holding approximately 45.92% of total revenue, owing to the large burden of remediable diseases including cataracts, retinal disorders, and refractive errors that require procedural treatment. Developments in laser and minimally invasive surgical procedures continue resulting in faster recovery rates, encouraging patients to opt for surgical treatment, while aging populations around the globe continue contributing to increased demand for surgical eye care that keeps this service category firmly at the top of the broader segmentation.

The specialty advanced services segment is projected to grow at the fastest CAGR during the forecast period, as advancing diagnostic technology and treatment protocols for complex retinal, corneal, and neuro-ophthalmic conditions continue expanding beyond routine vision correction. Rising demand for these more sophisticated, technology-intensive service categories continues pushing this service type's growth rate ahead of the broader service type segmentation.

By Indication, refractive errors led the market, age-related eye conditions grew fastest

The refractive errors segment held the largest indication share in 2025, at approximately 39.00%, owing to higher screen time, urban lifestyles, and aging populations that continue driving myopia, hyperopia, and astigmatism diagnosis and correction. The topmost market positioning of this indication continues being encouraged by increasing diagnostic knowledge and availability, an uptake in corrective surgeries, and expanding lens accessibility across both developed and developing regions.

The age-related ocular diseases segment, which includes cataracts, macular degeneration, and glaucoma, is expected to exhibit the highest CAGR through the forecast period, driven by the susceptibility of the elderly population towards such diseases amid an increasing geriatric population base across the globe. An increasing life expectancy is driving the pace of growth in the indication segmentation above other segments.

By End-User, hospitals clinics led the market, ambulatory surgical centers grew fastest

The hospitals clinics segment held the largest end-user share in 2025, playing a key role in distributing comprehensive eye care services, particularly complex procedures requiring professional diagnosis and supervision. These establishments continue offering comprehensive care services, including consultations, diagnostics, and treatment, ensuring personalized solutions that keep hospitals and clinics firmly at the center of overall eye care services demand across nearly every major healthcare market worldwide.

The ambulatory surgical centers segment is projected to grow at the fastest CAGR during the forecast period, as the shift toward minimally invasive, same-day surgical procedures continues favoring these lower-cost, higher-throughput care settings over traditional inpatient hospital surgery. Rising patient and payer preference for cost-effective, convenient surgical settings continues pushing this end-user category's growth rate ahead of the broader end-user segmentation.

By Age Group, geriatric population led the market, pediatric population grew fastest

The geriatric population segment held the largest age group share in 2025, anchored by the rapidly expanding elderly population worldwide that continues experiencing the highest burden of cataracts, macular degeneration, glaucoma, and other age-related eye conditions. That substantial and growing patient population keeps the geriatric age group firmly at the center of overall eye care services demand across nearly every major regional market.

The pediatric population segment is projected to grow at the fastest CAGR during the forecast period, driven by rising global myopia prevalence among children linked to increased screen time and reduced outdoor activity. Growing awareness of early childhood vision screening and intervention continues pushing this age group category's growth rate ahead of the broader age group segmentation.

Regional Analysis

|

Region |

Major Country |

Share within Region, 2025 (%) |

|---|---|---|

|

North America |

United States |

85.30% |

|

Europe |

Germany |

27.20% |

|

Asia Pacific |

China |

36.50% |

|

Middle East & Africa |

UAE |

26.40% |

|

Latin America |

Brazil |

37.30% |

North America Eye Care Services Market Insights

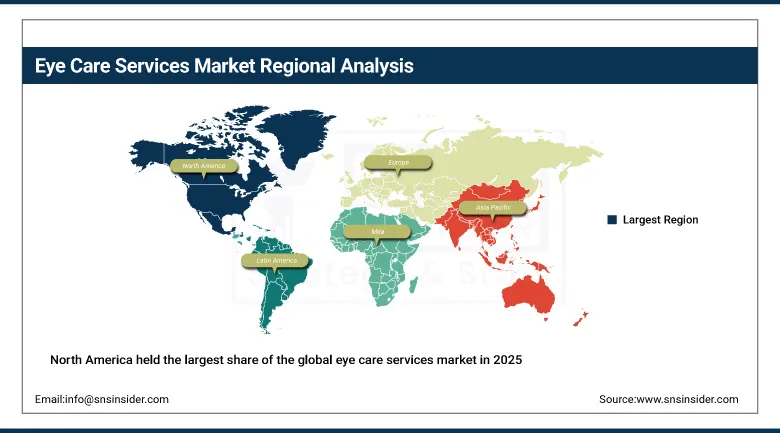

North America held the largest share of the global eye care services market in 2025, at approximately 39.90%, supported by a well-established healthcare infrastructure, high adoption of premium ophthalmic products, and a strong presence of major market players focused on continuous innovation in vision correction technology. Increasing prevalence of vision problems due to digital device usage continued reinforcing this leadership position throughout the year.

North America dominated this particular market with the US being responsible for approximately 85.30% of regional revenue. This was due to the presence of key players in the market who offered eye care services in North America and good insurance coverage. Canada provided a growing contribution of regional revenue and hence continued to be dominant in the market.

Get Customized Report as per Your Business Requirement - Enquiry Now

Europe Eye Care Services Market Insights

Europe held a substantial share of the global eye care services market in 2025, supported by well-established national health insurance coverage and strong ophthalmic technology adoption across the continent. Germany accounted for roughly 27.20% of regional revenue, supported by its concentration of eye care providers and advanced diagnostic and surgical technology infrastructure.

France, the United Kingdom, and Italy followed a broadly similar trajectory, as continued aging population trends and vision correction demand extended eye care services adoption across the continent's largest healthcare markets. Continued emphasis on preventive eye care is expected to keep supporting steady European demand through the remainder of the forecast period.

Asia Pacific Eye Care Services Market Insights

Asia Pacific was the fastest-growing region in the global eye care services market, driven by rapidly expanding healthcare infrastructure investment, rising myopia prevalence among children, and growing government-backed eye care access initiatives across the region's most populous economies. Rising middle-class healthcare spending continued driving regional demand at a pace considerably faster than more mature Western markets.

China accounted for roughly 36.50% of regional revenue, supported by expanding domestic healthcare infrastructure and rising awareness of preventive eye care. India and Southeast Asian markets contributed significant additional regional demand through their own rapidly expanding eye care access programs, reinforcing Asia Pacific's position as the clear growth leader in this market.

MEA & Latin America Eye Care Services Market Insights

Eye care services witnessed consistent growth during the year 2025 in the Middle East and Africa region owing to an increase in the investments made in the infrastructure of healthcare facilities, coupled with the government’s initiatives in providing vision care in the Gulf countries. In the region, UAE alone contributed about 26.40% of the total revenues due to technological advancements in eye care.

Latin America expanded at a comparable pace, led by Brazil at roughly 37.30% of regional revenue, where growing healthcare infrastructure investment continued to support category growth. Mexico and Argentina followed a similar trajectory as regional eye care access expanded further through the remainder of the forecast period.

Growth Drivers: Aging population and expanding surgical technology access

The increasing number of individuals experiencing vision-related issues, a quickly aging population, advancements in technology, and heightened awareness regarding eye care continue to be the central force behind eye care services market growth. Developments in laser and minimally invasive surgical procedures continue resulting in faster recovery rates, encouraging patients to opt for surgical treatment rather than delaying necessary intervention.

Global health campaigns and public-private partnerships continue improving awareness and access to eye care services, especially in low- and middle-income countries where historical access has been limited. Rising screen time, urban lifestyles, and lifestyle-related diseases including diabetes and hypertension that affect vision continue reinforcing structural demand growth across nearly every major eye care services category worldwide.

Restraints: Access disparities and specialized workforce shortages

Persistent access disparities in rural and underserved regions continue restricting comprehensive eye care services availability, even as urban and higher-income areas experience robust growth in service infrastructure. That access gap continues requiring sustained public health investment and outreach programs to extend eye care services to populations that have historically lacked adequate access.

A shortage of trained ophthalmologists and optometrists in many regions continues constraining the pace at which eye care service capacity can expand to meet growing patient demand. That specialized workforce constraint continues concentrating the most advanced eye care services within urban centers that have adequate training infrastructure and provider density.

Opportunities: Pediatric myopia intervention and ambulatory surgical center expansion

Growing global myopia prevalence among children presents substantial opportunity for eye care providers positioned to serve this expanding pediatric patient population through early screening and intervention programs. Providers capable of delivering accessible, affordable pediatric vision care stand to capture a growing share of demand as childhood myopia continues rising worldwide.

Expanding ambulatory surgical center infrastructure presents a further significant growth avenue, as patients and payers increasingly favor these lower-cost, higher-throughput care settings over traditional inpatient hospital surgery for routine eye procedures. Providers capable of delivering high-quality, cost-effective ambulatory surgical eye care stand to capture meaningful new revenue streams through 2035.

Recent Developments:

- 2026: Alcon reported strong first-quarter 2026 growth driven by new eye care product launches, including the Unity VCS/CS surgical platform, PanOptix Pro, Tryptyr, and Precision7, reinforcing its leadership in ophthalmic surgical and vision care solutions.

- 2025: Alcon continued expanding its surgical ophthalmology portfolio, strengthening its position serving eye care providers with advanced cataract and vision correction surgical technology across global markets.

- 2025: Aravind Eye Care System continued expanding its high-volume, low-cost cataract surgery model across India, reinforcing its position as one of the world's largest and most efficient eye care service providers.

Eye Care Services Market key players are:

- Aravind Eye Care System

- Alcon Inc.

- Asia Pacific Eye Centre

- Topcon Corporation

- iCare Health Solutions

- EssilorLuxottica SA

- Bausch + Lomb Corporation

- Johnson & Johnson Vision Care, Inc.

- Carl Zeiss Meditec AG

- Nidek Co., Ltd.

- Vision Group Holdings, LLC

- TLC Laser Eye Centers

- National Vision Holdings, Inc.

- MyEyeDr.

- Warby Parker Inc.

- Specsavers Optical Group

- Kaiser Permanente Ophthalmology

- LensCrafters

- America's Best Contacts & Eyeglasses

- Vision Source

Eye Care Services Market Report Scope :

| Report Attributes | Details |

|---|---|

| Market Size in 2025 | USD 181.11 Billion |

| Market Size by 2035 | USD 460.86 Billion |

| CAGR | CAGR of 9.79% From 2026 to 2035 |

| Base Year | 2025 |

| Forecast Period | 2026-2035 |

| Historical Data | 2022-2024 |

| Report Scope & Coverage | Market Size, Segments Analysis, Competitive Landscape, Regional Analysis, DROC & SWOT Analysis, Forecast Outlook |

| Key Segments | • By Service Type (Surgical Interventions, Vision Testing Eye Exams, Specialty Advanced Services, Others) • By Indication (Refractive Errors, Age-Related Eye Conditions, Others) • By End-User (Hospitals Clinics, Ambulatory Surgical Centers) • By Age Group (Geriatric Population, Pediatric Population) |

| Regional Analysis/Coverage | North America (US, Canada), Europe (Germany, UK, France, Italy, Spain, Russia, Poland, Rest of Europe), Asia Pacific (China, India, Japan, South Korea, Australia, ASEAN Countries, Rest of Asia Pacific), Middle East & Africa (UAE, Saudi Arabia, Qatar, South Africa, Rest of Middle East & Africa), Latin America (Brazil, Argentina, Mexico, Colombia, Rest of Latin America). |

| Company Profiles | Aravind Eye Care System, Alcon Inc., Asia Pacific Eye Centre, Topcon Corporation, iCare Health Solutions, EssilorLuxottica SA, Bausch + Lomb Corporation, Johnson & Johnson Vision Care, Inc., Carl Zeiss Meditec AG, Nidek Co., Ltd., Vision Group Holdings, LLC, TLC Laser Eye Centers, National Vision Holdings, Inc., MyEyeDr., Warby Parker Inc., Specsavers Optical Group, Kaiser Permanente Ophthalmology, LensCrafters, America's Best Contacts & Eyeglasses, Vision Source |

Frequently Asked Questions

The Eye Care Services Market is expected to grow at a CAGR of 9.79% from 2026 to 2035.

The Eye Care Services Market was valued at USD 181.11 Billion in 2025.

An aging population combined with advancements in laser and minimally invasive surgical technology is the major growth factor.

The Surgical Interventions segment held approximately 45.92% share in 2025.

North America held the largest share of the Eye Care Services Market in 2025, at approximately 39.90%.

Get in Touch